The choice between these two routes differs not just in eligibility thresholds but in regulatory scrutiny, investor composition, capital scale, compliance burden, and long-term strategic positioning. Getting the decision right at the start shapes the entire IPO outcome. Companies raising ₹10–₹25 crore face fundamentally different cost structures, liquidity profiles, and post-listing obligations than those raising ₹500 crore. This guide breaks down the differences clearly so founders can choose the route that fits their business today—and where it's heading tomorrow.

Key Takeaways

- SME IPOs target companies with post-issue paid-up capital between ₹1 crore and ₹25 crore; Mainboard requires at least ₹10 crore

- Mainboard IPOs face SEBI-level DRHP review; SME IPOs are vetted by stock exchanges, making timelines faster

- Minimum application size is ₹2 lakh for SME IPOs versus ₹10,000–₹15,000 for Mainboard, attracting different investor profiles

- SME promoters face 5-year lock-in; Mainboard promoters face 18 months

- The right route depends on your capital size, governance readiness, and listing timeline — not just which exchange sounds more prestigious

Mainboard IPO vs SME IPO: At a Glance

| Parameter | SME IPO (BSE SME / NSE Emerge) | Mainboard IPO (BSE / NSE) |

|---|---|---|

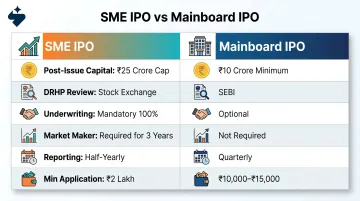

| Post-issue paid-up capital | Not exceeding ₹25 crore | Minimum ₹10 crore (profitability route) |

| Listing exchange | BSE SME or NSE Emerge | BSE or NSE main boards |

| DRHP review authority | Stock exchange (BSE/NSE) | SEBI (observation letter within 30 days) |

| Minimum allottees | 50 (being raised to 200 per SEBI Dec 2024 reforms) | 1,000 |

| Minimum application size | ₹2,00,000 (raised from ₹1,00,000 in 2025) | ₹10,000–₹15,000 |

| Underwriting | 100% mandatory; merchant banker underwrites min 15% | Not mandatory |

| Market maker obligation | Mandatory for 3 years post-listing | Not mandatory |

| Financial reporting | Half-yearly | Quarterly |

| Issue size range (typical) | ₹10–₹100 crore | ₹100 crore+ |

The table covers regulatory thresholds, but strategic factors like investor visibility, post-listing liquidity, and institutional appetite carry equal weight in practice. A company may clear the Mainboard eligibility bar yet still be better served by an SME listing first — particularly if its story needs seasoning before facing QIB scrutiny. Eligibility sets the floor; your growth stage and capital roadmap determine the right choice.

What is a Mainboard IPO?

A Mainboard IPO is a company's first public sale of shares listed on the main boards of BSE or NSE, subject to SEBI's full regulatory framework under ICDR Regulations. This route is intended for established, scaled businesses that can sustain the scrutiny, compliance cost, and institutional investor expectations that come with a Main Board listing.

Eligibility Criteria

SEBI's ICDR Regulations define two primary routes for Mainboard eligibility:

Profitability Route (Regulation 6(1)):

- Net tangible assets of at least ₹3 crore in each of the preceding 3 full years

- Average operating profit of at least ₹15 crore during the preceding 3 years, with operating profit in each of those years

- Net worth of at least ₹1 crore in each of the preceding 3 full years

- Aggregate issue size must not exceed 5 times the pre-issue net worth

QIB Route (Regulation 6(2)) for companies without profit track record:

- Issue must be through book-building process

- At least 75% of the net offer must be allotted to Qualified Institutional Buyers (QIBs)

- If 75% QIB subscription is not achieved, the entire issue must be refunded

Regulatory Process

SEBI reviews and comments on the DRHP directly, adding a layer of scrutiny that typically makes the timeline longer but also adds credibility to the listing. SEBI provides an observation letter within 30 days of DRHP receipt, which remains valid for 12 months. The overall process from DRHP filing to listing typically takes 6 to 12 months depending on company readiness and regulatory queries.

The company must respond to SEBI observations before the Red Herring Prospectus is filed. Disclosure requirements are more extensive than the SME route, covering:

- Risk factors and management discussion & analysis (MD&A)

- Corporate governance disclosures

- Audited financials restated per Ind-AS

Investor Base and Minimum Investment

Mainboard IPOs attract a broad mix of:

- Qualified Institutional Buyers (QIBs): Mutual funds, insurance companies, foreign portfolio investors, and pension funds

- Non-Institutional Investors (NIIs): High-net-worth individuals and corporates

- Retail Individual Investors (RIIs): General public

Minimum application size is approximately ₹10,000–₹15,000, making Mainboard IPOs accessible to the widest possible retail base. At least 1,000 allottees are required for a successful listing, ensuring broad distribution.

Market Performance

That broad investor base translated into strong market activity. According to KPMG's FY2024-25 IPO report, 80 mainboard IPOs raised approximately ₹1,63,000 crore — a 163% increase over FY2023-24's ₹61,900 crore from 76 IPOs. Average oversubscription reached 102x for QIBs and 35x for retail investors.

Use Cases of a Mainboard IPO

Mainboard listings suit:

- Manufacturing companies with large capex requirements and established production capacity

- Financial services firms meeting RBI/IRDAI thresholds with audited AUM or credit book scale

- Healthcare companies with regulatory track records and multi-site infrastructure

- Technology firms with ₹100 crore+ revenue scale and clear unit economics

Average issue size in FY2024-25 was approximately ₹20,375 crore, driven by large offerings like Hyundai Motor India's ₹27,859 crore IPO. Typical issues outside that range raise ₹100–500 crore, supporting expansion mandates, debt retirement, or acquisitions.

What is an SME IPO?

An SME IPO is a public offering by a small or medium enterprise listed on a dedicated SME platform—BSE SME or NSE Emerge—designed to give growth-stage businesses access to public capital with a lighter regulatory framework than the Main Board. This route exists because SEBI recognised that standard Mainboard requirements would be prohibitive for smaller businesses with strong fundamentals but limited scale.

Eligibility Criteria

BSE SME Criteria:

- Company incorporated under Companies Act; post-issue paid-up capital not exceeding ₹25 crore

- Track record of at least 3 years (or 1 full financial year if project appraised by NABARD/SIDBI/banks)

- Net worth of at least ₹1 crore for the preceding 2 full financial years

- Net tangible assets of at least ₹3 crore in the last preceding full financial year

- Operating profit (EBITDA) of at least ₹1 crore in at least 2 out of 3 preceding financial years

NSE Emerge Criteria (slightly lower barriers):

- Net worth must be positive (no minimum floor)

- Net tangible assets: no specific minimum threshold

- Profitability metric: positive cash accruals in 2/3 years

- Track record: 3 years

The DRHP is reviewed by the stock exchange, not SEBI directly, which compresses the timeline significantly. Typical SME IPO execution takes 2–3 months from engagement to listing.

Key Structural Differences Specific to SME IPOs

- Mandatory full underwriting of the issue: Merchant banker must underwrite minimum 15% on own account

- Mandatory market maker appointment post-listing: Provides liquidity for 3 years, holding minimum 5% of total issue size

- Requirement for only 50 allottees (BSE SME) or a defined minimum (NSE Emerge)—a far lower bar than the 1,000-allottee Mainboard requirement

Minimum Lot Sizes and Investor Profile

SME IPO lot sizes are larger in practice—typically ₹2 lakh per application following SEBI's 2025 reforms. This in practice limits participation to HNIs and sophisticated retail investors. The higher minimum keeps less experienced investors out — SME stocks carry meaningfully higher risk and lower liquidity than Mainboard listings.

Benefits and Limitations

Benefits:

- Faster process: 2–3 months versus 6–12 months

- Lower cost of listing: approximately 9.18% of issue size versus 3–8% for Mainboard

- Access to public capital at early stage

- Stepping stone toward Mainboard migration

Limitations:

- Lower visibility and less institutional coverage

- Smaller addressable investor base

- Lower post-listing liquidity despite market maker support

- Higher proportional costs due to fixed fee components

Market Trends

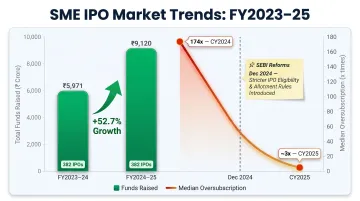

According to a Prime Database Group report (October 2025), FY2024-25 saw 382 SME IPOs raising ₹9,120 crore, up 52.7% from FY2023-24's ₹5,971 crore. Fresh capital constituted 91.5% of total SME IPO proceeds.

That momentum has since cooled. Median oversubscription dropped from 174x in CY2024 to approximately 3x in CY2025 following SEBI's December 2024 regulatory tightening — a clear signal of market correction and increased scrutiny.

Use Cases of an SME IPO

SME listings suit:

- Early-stage businesses with post-issue capital under ₹25 crore

- Niche regional players with defensible local market positions

- Family-owned businesses formalising their capital structure

- Companies in high-growth sectors seeking a first-mover advantage in public markets

- Businesses that need a verified public track record before approaching institutional investors at scale

Mainboard vs SME IPO: Which Route is Right for Your Business?

The choice between SME and Mainboard is not purely about eligibility—it's about strategic fit. A company can be technically eligible for Mainboard but operationally better served by an SME listing first.

Key Factors to Evaluate

| Factor | SME IPO | Mainboard IPO |

|---|---|---|

| Capital requirement | ₹10–₹100 crore | ₹100 crore+ |

| Governance standard | Basic Companies Act; exempt from SEBI LODR 17–27 | Independent directors, audit committees, LODR 17–27 compliant |

| Promoter lock-in | 5 years (minimum 20% contribution) | 18 months |

| Investor base | HNIs and sophisticated retail (₹2 lakh minimum) | QIBs, NIIs, and broad retail (₹10,000 minimum) |

When to Choose SME

- Post-issue paid-up capital between ₹1 crore and ₹25 crore

- Capital requirement of ₹10–₹100 crore

- 3+ years of operations but without a clean Mainboard-ready audit history

- Need for brand visibility and public track record before scaling to Mainboard

- Promoters comfortable with 5-year lock-in and limited near-term liquidity

When to Choose Mainboard

- Capital requirement exceeding ₹100 crore

- Strong 3-year profit track record with Ind-AS-compliant audited financials

- Expectation of institutional investors (mutual funds, FIIs) anchoring the book

- Brand equity of a Mainboard listing is strategically valuable

- Promoters seeking liquidity post-18-month lock-in

The Hidden Cost Dimension

Cost structure differs significantly between routes — and it affects net proceeds more than most promoters anticipate.

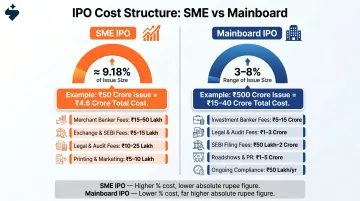

Mainboard IPOs can total 3–8% of offer size in fees — banker, legal, SEBI filing, roadshows, and ongoing compliance — per Blume Ventures' analysis. For a ₹500 crore issue, that's ₹15–40 crore in total expenses.

SME IPO costs run higher as a percentage — approximately 9.18% of total issue size, per the RBI Bulletin — but the absolute outlay is far smaller. A ₹50 crore SME IPO implies roughly ₹4.6 crore in total costs. Fixed charges like merchant banker fees (₹15–50 lakh), exchange fees, and legal and audit work consume a larger share of smaller raises, but remain manageable in rupee terms.

How S45 Can Help

S45 works across both Mainboard and SME listings. Our AI-powered readiness assessment identifies which route a company is genuinely prepared for — surfacing governance gaps, documentation issues, and capital structure problems before they stall the process mid-filing. Most assessments flag the critical blockers within the first two to three weeks.

What Happens After the Listing: Compliance, Liquidity, and Migration

Choosing the right IPO route is only the beginning. Post-listing compliance burdens, liquidity profiles, and migration pathways differ sharply between SME and Mainboard.

Post-Listing Compliance Differences

Mainboard-listed companies must:

- File quarterly financial results within 45 days (60 days for Q4)

- File quarterly shareholding patterns within 21 days

- Maintain independent director requirements per LODR (1/3 if non-exec chair, 1/2 if exec chair)

- Maintain audit, nomination, and remuneration committees with strict composition rules

- File Business Responsibility and Sustainability Reports (BRSR) if among top 1,000 listed entities

- Publish financial results in newspapers (1 English + 1 regional)

SME-listed companies:

- File half-yearly financial results within 45 days

- File half-yearly shareholding patterns within 21 days

- Exempt from SEBI LODR Regulations 17–27 (corporate governance, board composition, audit committee, related-party transaction thresholds)

- Follow Companies Act requirements only for board and audit committee structure

- No mandatory BRSR reporting

- No newspaper publication of results

Founders routinely underestimate this gap. Mainboard listing means dedicated investor relations teams, compliance officers, and legal counsel — just to keep up with quarterly filings and regulatory coordination. SME-listed companies carry none of that overhead.

Liquidity and Market Depth

The two platforms serve very different investor bases, and that shapes liquidity from day one.

Mainboard listings attract higher daily trading volumes, analyst coverage, and institutional participation. Stocks trade in lots of 1 share, giving retail investors flexible entry and exit.

SME listings carry lower float and thinner order books, with price stability dependent on the market maker. Market makers must provide two-way quotes for at least 75% of trading time and hold a minimum 5% of total issue size for 3 years. Trading occurs in standardised lots valued at approximately ₹1 lakh or more.

For founders, thinner SME liquidity can constrain follow-on fundraising and limit exit options for early investors — worth factoring in before choosing a platform.

Migration from SME to Mainboard

The SME platform is not necessarily a permanent home. Once a company meets Mainboard eligibility thresholds, migration is straightforward — and for many founders, it was the plan all along.

BSE Migration Criteria (effective March 1, 2026):

- Paid-up capital: at least ₹10 crore

- Market capitalisation: average ₹100 crore over preceding 6 months OR revenue ₹100 crore+ for each of preceding 3 years

- Operating profit (EBITDA): average ₹15 crore over preceding 3 years; minimum ₹10 crore in each year

- Net tangible assets: ₹3 crore in each of preceding 3 years

- Net worth: ₹1 crore in each of preceding 3 years

- Public shareholders: minimum 1,000

- SME listing tenure: at least 3 years

Approximately 360 SME companies have successfully migrated to the mainboards of NSE and BSE cumulatively. Many use the SME listing deliberately — building track record, governance infrastructure, and investor confidence before stepping into deeper capital pools on the Main Board.

Conclusion

SME IPOs and Mainboard IPOs are not competing products—they serve different stages of a company's growth. The right route depends on where the business is today and where it intends to go. Rushing to Mainboard before the fundamentals support it is as damaging as under-listing on SME when the company is ready for more.

Founders must evaluate capital needs, governance readiness, promoter liquidity timelines, and compliance capacity —without flattering assumptions—before choosing a route. That decision shapes not just the listing outcome but the company's capacity to raise follow-on capital and attract institutional investors over the long term.

Getting this choice right—grounded in accurate readiness data, not optimism—determines whether the IPO opens clean or unravels under scrutiny. S45 is India's first AI-native investment bank, having executed 26 IPOs since July 2023 and raised ₹1,180+ Cr across both Main Board and SME routes. The firm pairs sector bankers with proprietary analytics to assess readiness, draft DRHP, manage bookbuilding, and support post-listing IR—all from one team.

Ready to evaluate your IPO readiness? Connect with S45 for a comprehensive readiness assessment and a clear roadmap to listing.

Frequently Asked Questions

What is SME IPO vs normal IPO?

An SME IPO lists on BSE SME or NSE Emerge for companies with post-issue paid-up capital up to ₹25 crore, reviewed by the stock exchange. A normal (Mainboard) IPO lists on the main BSE/NSE exchanges for larger companies, with stricter SEBI scrutiny, higher capital requirements (₹10 crore minimum), and a broader investor base.

Which IPO is better, SME or mainboard?

Neither is universally better. Mainboard suits larger companies needing substantial capital (₹100 crore+) and institutional investor participation. SME suits growth-stage businesses seeking a faster, lower-cost route to public markets with ₹10–₹100 crore capital needs — the right fit depends on company size, governance readiness, and how much you're raising.

Is it good to invest in SME IPO?

SME IPOs can offer high return potential but carry higher risk: lower liquidity, limited analyst coverage, and larger minimum lot sizes (₹2 lakh). Best suited for risk-tolerant investors who conduct thorough due diligence before committing capital.

Can I sell SME IPO shares immediately?

Retail investors who receive allotment can sell on listing day. However, liquidity in SME stocks tends to be lower than Mainboard stocks due to higher lot sizes and thinner order books. Promoters face a 5-year lock-in on their minimum 20% contribution; anchor investors face 30-day and 90-day lock-ins on their allocations.

Can companies listed on SME be migrated to main board?

Yes. Key eligibility criteria include ₹10 crore paid-up capital, ₹100 crore average market cap over 6 months, ₹15 crore average operating profit over 3 years, at least 1,000 public shareholders, and a minimum 3-year SME listing tenure. Approximately 360 companies have successfully migrated to date.

Who is eligible for main board listing?

Companies need post-issue paid-up capital above ₹25 crore (or ₹10 crore minimum under the profitability route) and a 3-year operating history under the same management. SEBI's ICDR thresholds also apply: ₹3 crore net tangible assets, ₹15 crore average operating profit, or 75% QIB subscription for non-profitable issuers.