Introduction

Most founders spend months perfecting their product but only days preparing their pitch — yet investors spend an average of just 2 minutes and 24 seconds reviewing a startup pitch deck. According to DocSend's annual pitch deck report, that number has fallen 24% since 2021. For seed-stage companies, it's even lower: under 2 minutes. Investors typically decide within the first 10 to 60 seconds of scanning whether a deck is worth their time.

Your pitch isn't just a presentation — it's the first filter between your company and capital. This article covers what investors actually evaluate, how to build a deck that earns attention, how to deliver it with confidence, and how to follow up without losing momentum.

Key Takeaways

- Investors bet on founders as much as ideas — your domain expertise, credibility, and execution track record matter as much as your business concept

- A winning pitch deck follows a narrative arc: problem, solution, market opportunity, traction, team, and a specific ask — told as a story, not a checklist

- Pitching is a learnable skill: most founders need 20–30 rehearsals before they can deliver smoothly under pressure, so start practising early

- The pitch opens a relationship, not closes a deal. Follow up within 24 hours to show investors you operate with the same discipline you're pitching them on

What Investors Are Really Looking For

Founder-Market Fit: The Unfair Advantage

At early stages, investors evaluate whether you are uniquely positioned to solve this problem. Founder-market fit is the tight alignment between your lived experience and the urgent pain of the market you're serving — creating unfair insight, faster iteration, and easier customer trust.

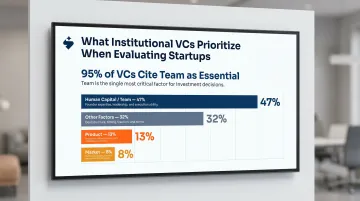

Survey data from 885 institutional VCs reveals that 95% cite the team as essential, and 47% rank human capital as the single most significant factor in startup success — versus only 13% for product and 8% for market. Y Combinator reinforces this: 40% of YC companies joined with "just an idea," because YC prioritizes founder quality and market insight over product maturity.

What this means for your pitch:

- Lead with why you're the right person to solve this problem

- Highlight the hardest thing you've ever done, even if it isn't a traditional credential

- Show how your lived experience gives you insight others don't have

Team Credibility: The Proxy for Execution

Investors use your most impressive accomplishment — a technical project, unconventional success, or relevant domain experience — as a proxy for your ability to navigate startup chaos. The data tells a different story from Silicon Valley lore: the average successful founder is 45 years old, and the average unicorn founder started their first unicorn at 35.

VCs probe team dynamics carefully. They ask "How did you meet?" to understand history and mutual respect. They test self-awareness with questions like "What are you most insecure about?" Answering "I'm really not insecure about anything" is a red flag for lack of self-awareness.

Red flags investors watch for:

- Management team conflict (up to 65% of high-growth startups fail due to this)

- Inability of the CEO to speak fluently across market, product, financials, and team

- Lack of visible respect or coordination between co-founders during the pitch

The Value of a Non-Obvious Insight

Strong team credibility earns the room — but what you know about the problem earns conviction. Investors reward founders who teach them something they didn't know. A specific, data-backed fact about the problem space signals mastery. Founders who recycle generic headlines about "a trillion-dollar market" without showing underlying math or customer-level evidence rarely leave a lasting impression.

For Indian founders preparing for public markets, this principle extends to institutional investors (QIBs and anchor investors) during roadshows. Clear narratives backed by evidence are what separate compelling pitches from forgettable ones.

Market Size: Tight Beats Inflated

Investors project your startup's success case to venture scale, but they don't trust top-down TAM figures from analyst reports. Richard Dulude, Partner at Underscore VC, calls the market size slide "one of the most commonly wasted slides in a pitch deck."

Use bottom-up market sizing:

- Formula: [Number of Customers] x [Price They Will Pay]

- Explain TAM, SAM, and SOM with your math visible

- A tight, well-defined customer segment beats an inflated addressable market claim every time

Citing inflated TAM figures — for example, "₹10 lakh crore market" — without bottom-up modeling signals insufficient research and erodes trust quickly.

Traction as the Earliest Proof of Conviction

Even pre-revenue signals matter. Customer conversations, letters of intent (LOIs), waitlists, or strong engagement metrics show that the market responds. Institutional investors evaluate conversion intent, not just raw numbers. Effective LOIs include named companies, stated pricing ranges, and defined use cases. Vague LOIs are discounted.

Strong pre-revenue traction signals include:

- Named LOIs with pricing and scope defined

- Waitlists showing active engagement, not just email signups

- Pilot programs with documented learnings and success criteria

Traction discipline doesn't stop at customer signals. Founders who build clean financial records from the early days carry that credibility forward — especially in the Indian IPO context, where SEBI requires three years of audited financials and evidence-linked disclosures. The companies that stumble in later fundraising rounds are usually the ones that treated bookkeeping as an afterthought.

How to Build a Pitch Deck That Actually Works

Core Slides: The Structural Backbone

Every pitch deck needs these slides, each answering a specific question for the investor:

- Problem — What urgent pain are you solving?

- Solution — How does your product address this pain?

- Market Opportunity — Who are your customers, and how big is the opportunity?

- Business Model — How do you make money?

- Traction or Key Metrics — What proof do you have that this works?

- Team — Why are you the right people to execute?

- The Ask — How much are you raising, and what will it unlock?

Y Combinator recommends keeping each section to one slide (maximum three). "Focus on narrative. The rest is commentary."

The Narrative Arc: Tell a Story, Not a Checklist

Your pitch deck should read like a story. Each slide should logically flow from the last and answer the investor's implicit "so what?" The goal is for the investor to retell your story convincingly to a colleague after the meeting.

Avoid the "Frankenstein deck" — gradually adding slides in response to investor feedback until the narrative collapses under its own weight. Periodically rebuild from scratch, letting your memory of what mattered most drive the new version.

Specificity Beats Jargon Every Time

Weak product description: "We leverage AI-powered automation to revolutionize enterprise workflows and deliver next-generation productivity solutions."

Strong product description: "We built a Google-style typeahead search for Magento stores — it increases search-to-purchase conversion and average order value."

Concrete descriptions help investors picture your product and explain it to others. Jargon obscures; specificity sells.

Slide Design: The 10/20/30 Rule

Guy Kawasaki's framework is simple: 10 slides maximum, 20-minute delivery window (even if you have an hour), 30-point minimum font. The logic behind each rule:

- 10 slides — most people can't absorb more than ten concepts in a single meeting

- 20 minutes — accounts for setup delays and leaves 40 minutes for real discussion

- 30-point font — forces concision and stops founders from reading slides aloud

No more than one-quarter of your slides should be text-heavy. Sparse, well-designed slides show investors you know how to communicate clearly — and that matters.

The Ask Slide: Make the Call to Action Unambiguous

Many founders omit or bury their funding ask. This is a critical mistake. Your ask slide should include:

- The specific amount being raised (rounded, not a range like "₹5-10 Cr")

- The primary use of funds (visual breakdown preferred)

- 2-4 specific milestones the capital will unlock

Structure milestones to show a clear path to the next funding round, typically covering 18 months. As Stephane Nasser, founder of OpenVC, puts it: "No Funding Ask Slide = no action."

Delivering Your Pitch With Confidence

The First 60 Seconds: Hook Them Fast

Investors form strong impressions almost immediately. Guy Kawasaki recommends opening with three questions: "How much time do I have?", "What are the three most important things I can explain?", "Can questions be held until the end?" This creates a verbal commitment framework and sets expectations.

Lead with a punchy statistic, a short story, or a provocative reframe of the problem — not a company history monologue. Most decks lose the investor by slide three. The first five slides set the tone:

- Problem — Is this real and significant?

- Solution — Does this actually solve it?

- Market — Is the opportunity worth pursuing?

- Business Model — How does money flow?

- Traction — What evidence exists?

If the hook isn't established before slide three, many investors have already moved on.

One Spokesperson, Fully Prepared

A single well-rehearsed presenter consistently outperforms a tag-team approach. The CEO should be fluent across all sections of the deck, including market, product, financials, and team. If the CEO cannot cover all sections, that gap itself is a signal — and investors will notice.

Practice Is Not Optional

Kawasaki puts the number at 25 rehearsals before a founder becomes "truly smooth." Treat it like a performance skill, not a slide review.

Effective rehearsal methods:

- Record yourself and watch for pacing, filler words, and clarity

- Pitch to trusted critics who will ask hard questions

- Periodically throw away the entire deck and rebuild from memory — this forces retention of only the most important points

- Track where the narrative loses momentum and tighten those sections

Mastering Q&A and Post-Pitch Protocol

How you handle questions matters as much as the pitch itself. In the room:

- Take visible notes — it signals you value the feedback

- Answer difficult questions directly, without deflecting

- If you don't know something, say so and commit to following up

The behavior after the room is equally important.

Send a follow-up email within 24 hours. Include the deck, notes on open questions, and a clear next step. Kawasaki is explicit: "The clock expires 24 hours after you walk out the door."

Tailoring Your Pitch to the Right Investors

Do Your Homework Before Every Meeting

Walking into an investor meeting unprepared wastes everyone's time. Before any roadshow presentation or anchor conversation, research who's in the room — their sector focus, past investments, and how they've historically approached companies in your industry. Relevance matters more than volume.

Practical research checklist:

- Review the firm's or fund's portfolio companies

- Identify sector focus and stage preferences

- Read recent blog posts or interviews from partners

- Check if they've invested in adjacent or competing companies

Customize the Delivery, Not the Deck

Keep the core pitch deck consistent, but adjust the verbal emphasis based on what each investor prioritizes. Institutional investors typically focus on financial discipline, regulatory compliance, and sector tailwinds. Retail-facing presentations may lean harder on growth narrative and promoter credibility. Read the room — and adapt your emphasis accordingly without changing your underlying numbers.

The Value of a Warm Introduction

The quality of your introduction shapes how seriously an investor reads your materials. A strong warm intro comes from a credible mutual contact who can speak specifically to your business — not a generic forwarded email. One practitioner's analysis found cold outreach yields a 1-2% response rate versus 70-80% for quality warm introductions.

A low-quality warm intro — a generic email from a distant contact with no real context — can actually work against you by signaling weak networks. Where warm introductions aren't available, structured access through merchant banker networks or SEBI-registered intermediaries provides a more credible path than cold outreach.

Common Mistakes That Kill Pitch Meetings

Vague Claims and Unsubstantiated Statements

Red-flag phrases investors hear constantly:

- "We have no competition" — VCs hear "no market"

- "The market is worth trillions" — signals no bottom-up modeling

- "Our customers are everyone" — signals lack of focus

- Buzzword-dense product descriptions without clear value proposition

How to reframe each mistake:

| Mistake | Fact-Backed Alternative |

|---|---|

| "No competition" | "We compete with manual spreadsheets and legacy software X; here's how we're differentiated" |

| "Trillion-dollar market" | "Our SAM is 50,000 mid-market retailers in India at ₹2 lakh ARR = ₹10,000 Cr opportunity" |

| "Customers are everyone" | "We serve Series A SaaS companies with 20-50 employees in the first 18 months" |

Skipping the Follow-Up

Failing to follow up promptly after a pitch meeting is one of the most common and most avoidable mistakes. Investors interpret silence as disorganization.

Follow-up checklist (within 24 hours):

- Send a thank-you note referencing specific discussion points

- Resend the deck with any updates discussed

- Address open questions with cited sources

- Propose a clear next step with timing

Additional Red Flags That Kill Deals

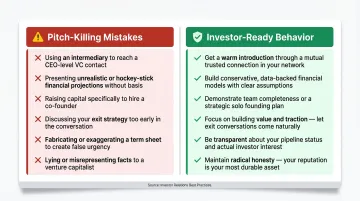

Follow-up discipline is table stakes. Beyond that, Alex Iskold, Managing Partner at 2048 Ventures, lists 18 mistakes that consistently derail deals. Key ones include:

- Using an intermediary instead of the CEO for outreach

- Unrealistic financial projections (₹0 to ₹100 Cr in 5 years)

- Raising money specifically to hire a technical co-founder

- Talking about an exit too early — signals "mercenary" not "visionary"

- Faking a term sheet — VCs can usually tell

- Lying to a VC — that relationship ends immediately and permanently

Frequently Asked Questions

What is startup pitching?

Startup pitching is the structured process of presenting a business idea or company to potential investors, covering the problem being solved, the solution, the market opportunity, and the funding ask, in order to secure capital and build investor relationships.

What is an example of a pitch?

"We built a Google-style typeahead search for Magento stores — it increases search-to-purchase conversion and average order value." It's specific, grounded in a familiar reference, and communicates value in one sentence.

What are the 3 C's of pitching?

The 3 C's are Clarity, Conciseness, and Conviction — meaning the investor understands your product, you respect their time, and you signal genuine belief in your ability to execute.

What is the 10/20/30 rule for pitch decks?

Guy Kawasaki's rule states: no more than 10 slides, delivered in 20 minutes or less, using a minimum font size of 30 points. The principle forces founders to prioritize the most important information and respect the investor's limited attention span.

How long should a startup pitch be?

Most investor pitches run 10–20 minutes, even when given a longer slot, leaving time for Q&A. Elevator pitches should distill the core message into 60–90 seconds.

What should a startup pitch deck include?

A strong deck covers: problem, solution, market opportunity, business model, traction or key metrics, team, and a clear funding ask. Structure it as a narrative — not a data dump.