This guide covers the SEBI ICDR framework, what the DRHP must contain, financial and non-financial disclosure obligations, how requirements differ for SME vs Main Board, and the most common gaps that delay listings.

TLDR:

- SEBI ICDR 2018 governs all IPO disclosures; compliance mapping is mandatory before drafting

- DRHP must include risk factors, audited KPIs, restated financials, promoter backgrounds, and use-of-proceeds schedules

- November 2022 amendments introduced peer-benchmarked KPI disclosures certified by auditors

- SME requirements now mirror Main Board after March 2025 reforms

- Common delays stem from MD&A inconsistencies, vague risk factors, and incomplete related-party disclosures

The SEBI ICDR Framework: India's Governing Law for IPO Disclosures

The primary legal instrument governing IPO disclosures in India is the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (SEBI ICDR). Notified on September 11, 2018 and effective from November 10, 2018, it replaced the 2009 regulations and introduced stricter, more detailed disclosure requirements. The regulation has been amended multiple times, most recently in May 2024.

SEBI's Role and the Observation Process

SEBI reviews the Draft Red Herring Prospectus (DRHP) filed by the issuer and the Book Running Lead Managers (BRLMs). Within 30 days of receiving a complete filing, SEBI issues an observation letter identifying required clarifications or corrections. In practice, including clarification cycles, the process typically extends to 60-90 days. Each query resets the review timeline, so completeness at first submission is critical.

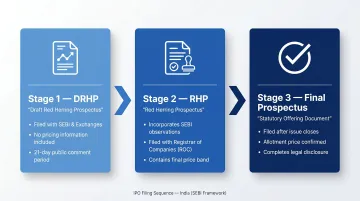

DRHP, RHP, and Final Prospectus: The Three Stages

The filing sequence follows a strict order:

- Draft Red Herring Prospectus (DRHP): Filed with SEBI and stock exchanges for regulatory review and public comments (minimum 21 days). Does not contain final pricing.

- Red Herring Prospectus (RHP): Updated with SEBI observations, filed with the Registrar of Companies before the issue opens. Contains all information except the final price.

- Final Prospectus: Filed after the issue closes and pricing is determined through book-building.

Layered Regulatory Obligations

Indian IPO issuers face three concurrent compliance frameworks from the moment of DRHP filing:

- SEBI ICDR 2018: Governs pre-listing disclosures, eligibility, pricing, and allotment

- SEBI LODR 2015: Post-listing continuous disclosure obligations, including quarterly use-of-proceeds reporting under Regulation 32

- Companies Act 2013: Board composition (Section 149), prospectus filing with ROC, statutory audit requirements

A deficiency in one framework—such as inadequate independent director appointment before DRHP filing—can trigger delays across all three simultaneously. SEBI has continued tightening these obligations through a series of reforms, with the most consequential changes arriving between 2022 and 2025.

Landmark 2022-2025 Amendments

November 2022: Mandated KPI disclosures in the "Basis for Issue Price" section, requiring 3-year historical KPIs, peer comparison with listed companies, and auditor certification. Issuers can no longer rely on narrative alone — every valuation claim must be anchored to audited, comparable data.

February 2025: Established the Industry Standards Forum (ISF) for sector-wise standardised KPIs, ensuring uniform benchmarking across industries.

March 2025: Overhauled the SME IPO framework with four specific changes:

- Restated financials requirement increased from 2 to 3 years

- Profitability thresholds introduced as an eligibility condition

- General Corporate Purpose (GCP) utilisation caps tightened

- Minimum QIB allocation raised to 25%

These changes substantially narrow the gap between SME and Main Board standards, raising the bar for smaller issuers across the board.

The DRHP Explained: Structure and Mandatory Disclosure Sections

SEBI ICDR prescribes a specific structure for the DRHP. Deviations in format, omissions of required sections, or vague language trigger observations that delay the process.

Risk Factors

Material risks must be listed in descending order of materiality, with the most significant risks to investors appearing first. Generic or boilerplate risk factors are flagged by SEBI. Each risk must reflect company-specific vulnerabilities, not industry-wide conditions that apply to all issuers.

Business Overview

A detailed operational and competitive narrative covering business model, revenue streams, operational facilities, and market positioning. This section must align directly with the financial statements—inconsistencies between narrative and numbers are the most common reason for SEBI queries.

Industry Overview

Must be supported by a report from an independent research agency. If the issuer commissioned or paid for the report, this fact must be disclosed. The report cannot be selective or promotional.

Objects of the Issue

Requires a granular utilisation plan for proceeds with basis and justification for each object. Key regulatory caps and monitoring requirements:

| Rule | Main Board | SME (Post-March 2025) |

|---|---|---|

| GCP Cap | 25% of total proceeds | ~10% or ₹10 crore, whichever is lower |

| Monitoring Agency Threshold | Proceeds exceeding ₹100 crore | Proceeds exceeding ₹20 crore |

Where a monitoring agency is required, the issuer must appoint a SEBI-registered agency to track deployment and submit quarterly reports until full utilisation.

Management Discussion and Analysis (MD&A)

Issuers must disclose historical financial performance with explanations for material changes, segment-level data where applicable, and key business drivers.

SEBI frequently raises queries when MD&A narratives contradict the numbers—describing "strong growth" when revenue declined, or citing operational efficiency when margins compressed.

Litigation and Legal Proceedings

All pending cases above a materiality threshold (defined by the company's board and disclosed in the DRHP) must be listed with status, amounts involved, and potential impact on operations. Promoter litigation, regulatory notices, and tax disputes require separate disclosure.

KPI Disclosure Requirements

Following the November 2022 amendment, issuers must:

- Disclose historical KPIs for at least 3 full financial years

- Compare KPIs with listed Indian peers and, where applicable, global peers of comparable size

- Obtain auditor certification for all disclosed KPIs

- Disclose all KPIs shared with any investor during the 3 years preceding DRHP filing

- Continue disclosing KPIs post-listing for at least one year or until proceeds are fully utilised

Selective KPI definitions are prohibited. If an issuer highlights "customer growth" but omits "customer churn," SEBI will flag the omission. The Industry Standards Forum provides sector-wise standardised KPIs precisely to prevent this kind of partial disclosure—issuers should cross-check their KPI set against the relevant sector framework before filing.

Financial Disclosures: Standards, Audits, and Restatements

Restated Financial Statements

SEBI requires restated financial statements for a minimum of 3 full financial years preceding the filing, certified by the statutory auditor and reviewed by a peer reviewer. These must eliminate prior-period errors and reflect consistent accounting policies under Ind AS (Indian Accounting Standards).

Unlike standard annual reports, restated financials apply uniform policies retrospectively, adjust for accounting changes, and consolidate subsidiaries consistently. Common remediation issues include:

- Prior-period adjustments not properly reconciled

- Inconsistent revenue recognition policies across years

- Segment reporting that doesn't align with operational structure

- Related-party transactions that lack transparency

Interim Financial Statements

If the DRHP is filed more than six months after the last audited balance sheet date, the issuer must include audited or reviewed interim financials. This ensures that investors see recent financial performance, not outdated data.

Related Party Transaction Disclosures

All transactions with promoters, promoter group entities, and key managerial personnel must be disclosed with amounts, nature, and whether they are at arm's length. SEBI scrutinises:

- Large or recurring transactions that suggest fund diversion

- Below-market transactions (for example, rent-free premises provided to promoters)

- Loans to/from promoters or group entities

- Guarantees provided by the company for promoter borrowings

Post-March 2025, SME issuers are prohibited from using IPO proceeds to repay loans from promoters or related parties.

Use-of-Proceeds Schedule

Each object of the issue must have an independently appraised estimate (for amounts above prescribed thresholds) and a quarterly deployment schedule. Post-listing, companies must report actual deployment against this schedule under LODR Regulation 32, and deviations require audit committee approval.

Ongoing compliance requirements include:

- Explaining any variation between projected and actual utilisation in quarterly filings

- Submitting an annual statement of funds used for other purposes, certified by statutory auditors

- Placing that statement before the audit committee and reporting it to the stock exchange

Non-Financial Disclosures: Promoters, Governance, and Litigation

Promoter and Promoter Group Disclosures

The DRHP must include:

- Detailed profiles of all promoters (individuals and entities)

- Shareholding pre- and post-issue

- Criminal or civil proceedings against them

- Disqualifications under the Companies Act

- Details of entities they are associated with that have been debarred by SEBI or other regulators

- Confirmation that no promoter is a willful defaulter, fraudulent borrower, or fugitive economic offender

Corporate Governance Disclosures

Issuers must disclose:

- Board composition and compliance with independent director requirements (minimum one-third of the board under Companies Act Section 149)

- Committee composition (audit, nomination, remuneration, stakeholder relations)

- Related-party approvals obtained

- Lock-in arrangements for promoter shares

Lock-in rules differ by exchange and have been updated in recent years. Main Board requirements (post-2021 amendment) are as follows:

Promoter Lock-in Periods (Main Board, post-2021 amendment):

- 18 months for minimum promoter contribution (20% of post-issue capital)

- 6 months for excess promoter holdings above 20%

- 3 years where majority of proceeds are for capital expenditure

- 1 year for excess holdings where majority is for capex

SME listings operate under stricter lock-in terms introduced in March 2025:

- 3 years for minimum promoter contribution

- 1 year for excess holdings

Material Contracts and Agreements

Beyond governance structure, the DRHP must identify and disclose key contracts material to the business — agreements that give investors a clear picture of operational dependencies and financial exposure. These include:

- Long-term supply agreements

- Customer contracts

- IP licences

- Joint ventures

- Agreements that create contingent liabilities or affect future profitability

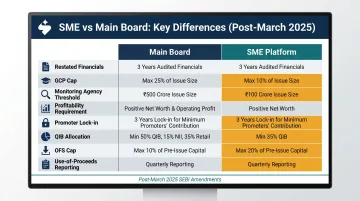

SME vs Main Board: How Disclosure Requirements Differ

The March 2025 SEBI amendments made sweeping changes to the SME IPO framework, narrowing the gap between SME and Main Board standards on financials, investor protections, and governance. The table below maps the key differences, followed by SME-specific disclosure additions and migration rules.

Key Differences (Post-March 2025)

| Parameter | Main Board | SME (NSE Emerge / BSE SME) |

|---|---|---|

| Restated financials | 3 years | 3 years (increased from 2) |

| Maximum post-issue capital | No upper limit | ₹25 crore |

| GCP cap | 25% of proceeds | 10% or ₹10 crore, whichever is lower |

| Monitoring agency threshold | ₹100 crore issue size | ₹20 crore issue size |

| Minimum issue size | No minimum | ₹10 crore |

| Minimum application size | ₹15,000 | ₹2 lakh (increased from ₹1 lakh) |

| Profitability requirement | ₹15 crore average operating profit | ₹3 crore in 2 of 3 years |

| Minimum allottees | - | 200 (increased from 50) |

| QIB allocation | Per ICDR categories | 25% mandatory |

| Use-of-proceeds reporting | Quarterly | Half-yearly |

| Promoter lock-in (MPC) | 18 months | 3 years |

| OFS cap | No specific cap | 10% of total issue size |

Beyond the comparative parameters above, the 2025 amendments also introduced a set of disclosures that apply exclusively to SME issuers.

SME-Specific Additional Disclosures (2025 Amendments)

SME issuers must now disclose:

- Details of heads of departments and their experience

- ESIC and EPF compliance details (number of employees, payment history, delays for past 3 years)

- Merchant banker site visit report as a material document

- All merchant banker fees

- DRHP made public for 21 days for comments (aligning with Main Board)

These disclosure additions align SME listings more closely with Main Board standards — a shift that also affects when and how companies must transition between the two platforms.

Migration from SME to Main Board

Companies listed on the SME platform must migrate to the Main Board when market capitalisation reaches ₹50 crore — up from the previous ₹25 crore paid-up capital threshold.

Upon migration, the company moves into full Main Board compliance: quarterly financial reporting, complete audit committee composition, and enhanced related-party transaction norms apply from that point forward.

Common Disclosure Gaps That Delay or Derail Indian IPOs

Most Frequent SEBI Observation Categories

MD&A Inconsistencies: The most common gap is misalignment between the Management Discussion and Analysis narrative and the restated financials. For example, describing "operational efficiency improvements" when gross margins declined, or highlighting "diversification" when revenue concentration increased.

Vague Risk Factors: Generic risk factors that could apply to any company in the sector are insufficient. SEBI requires company-specific risks with materiality ordering. A chemical manufacturer must disclose specific environmental compliance risks, not just "regulatory changes may affect operations."

Incomplete Related Party Transactions: Under-disclosed transactions, off-market pricing, or transactions that lack board approvals are red flags. SEBI frequently queries transactions where the basis for pricing is not explained.

Insufficient Objects of the Issue: General corporate purposes line items that exceed prescribed caps, or capex estimates without independent appraisals, trigger observations. Each object must have a clear basis, timeline, and deployment schedule.

Documentation Gaps

Lost board resolutions, missing statutory approvals, or unaudited related-party transactions surfacing during due diligence force issuers to refile or seek extensions, adding months to the timeline. Common documentation issues include:

- Incomplete title for operational facilities

- Missing environmental clearances

- Outdated material contracts

- Promoter KYC gaps

- Missing audit committee approvals for related-party transactions

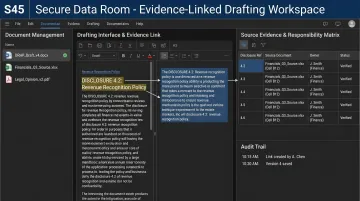

S45's Evidence-Linked Drafting Approach

S45 runs an evidence-linked drafting process inside a live data room, where every disclosure in the DRHP is linked to a source document before filing. Each element of the process is built to catch issues during drafting — not in the SEBI observation cycle:

- Version-controlled data room with audit trails and a clear responsibility matrix

- Every claim traced to its source: audited financials, legal opinions, contracts, compliance records

- Real-time gap identification flagged before SEBI filing, not after

When the issuer has restated financials, complete promoter and director documentation, and proactive management involvement, this workflow produces a DRHP-ready draft in 30 to 45 days — without last-minute rewrites.

Frequently Asked Questions

Who is eligible to apply for an IPO in India?

Eligibility covers two sides. Issuers must meet SEBI ICDR's profitability, net tangible assets, or net worth criteria — or qualify via the QIB route with 75% mandatory institutional allotment. On the investor side, resident Indians, NRIs, QIBs, HNIs, and FPIs can all apply through ASBA during the subscription window.

How do I check IPO eligibility for my company?

Cross-check your restated financials against SEBI ICDR Schedule XVI across the three eligibility routes — profitability, net tangible assets, and net worth. Also confirm that no promoter or group entity has been debarred or is ineligible under SEBI regulations.

What is the difference between a DRHP and an RHP in India?

The DRHP (Draft Red Herring Prospectus) is filed with SEBI for review and does not include the price band. The RHP (Red Herring Prospectus) is filed with SEBI and stock exchanges after receiving SEBI's observation letter and includes the price band. The Final Prospectus is filed after the issue closes and pricing is confirmed.

What are the minimum financial requirements for a Main Board IPO in India?

Three routes qualify a company for a Main Board IPO:

- Net tangible assets of ₹3 crore in each of 3 years (max 50% in monetary assets)

- Average pre-tax operating profit of ₹15 crore in 3 of the last 5 years

- Net worth of ₹1 crore in each of 3 years

Companies that don't meet these thresholds can use the QIB route, which requires 75% mandatory institutional allotment.

How long does SEBI take to review a DRHP?

SEBI typically issues its observation letter within 30 days of receiving a complete DRHP filing. However, if SEBI raises queries, each query-response cycle resets the review period. In practice, the full process from DRHP filing to SEBI observations often takes 60-90 days, depending on the completeness of the initial submission.

What are the key disclosure requirements in a DRHP?

A DRHP must cover:

- Risk factors ranked by materiality

- 3-year restated financials and MD&A

- Promoter details, related-party transactions, and litigation

- Objects of the issue with fund deployment schedules

- KPIs benchmarked against listed peers

- Corporate governance structure and material contracts

Every disclosure must be anchored to verified source documents.