Introduction

Mainboard IPO listing is the regulated sequence that transforms a private company into a publicly traded entity. From the day the Draft Red Herring Prospectus (DRHP) lands on SEBI's desk to the moment shares begin trading on NSE or BSE, every step follows a strict, transparent framework designed to protect investors and ensure fair price discovery.

This article covers the end-to-end timeline — typically spanning 6 to 12 months from engagement to listing — and the specific trading mechanics that unfold on listing day itself. Two groups will find it most useful: founders and promoters who need clarity on what happens between subscription close and the opening bell, and investors who want to understand when they can trade their allotted shares and how the opening price is actually set.

Key Takeaways

- T+3 mandatory timeline: Listing happens within 3 working days after subscription closes — SEBI's current framework for all Mainboard IPOs

- Listing day opens with a pre-open session (9:00–9:45 AM) for price discovery, then shifts to normal continuous trading from 10:00 AM to 3:30 PM

- The listing price is discovered through live order matching in the pre-open session — it's rarely identical to the issue price

- QIB oversubscription levels, market sentiment, and sector conditions are the primary drivers of where a stock opens

What Is the Mainboard IPO Listing Process in India?

The Mainboard IPO listing process is the formal, SEBI-regulated sequence by which a company that has completed its public offer gets its shares admitted to trading on NSE or BSE. It governs price discovery, allotment fairness, and the structured handoff from the primary market to open secondary trading.

Mainboard vs. SME IPO: Key Differences

| Parameter | SME IPO | Mainboard IPO |

|---|---|---|

| Exchange | NSE Emerge / BSE SME | NSE / BSE |

| Post-issue paid-up capital | ₹1 crore – ₹25 crore | Minimum ₹10 crore |

| Minimum market capitalisation | Not specified | ₹25 crore |

| Underwriting requirement | 100% mandatory | Partial (as applicable) |

| Governance standard | SEBI ICDR (SME provisions) | SEBI ICDR Regulation 6 (higher thresholds) |

How the Mainboard IPO Listing Process Works: Step by Step

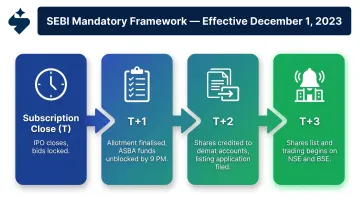

The full journey runs from regulatory filing and investor roadshow through to the opening bell on listing day. SEBI's T+3 framework — mandatory since December 1, 2023 — governs the post-subscription timeline, compressing what was once a six-day window into three working days.

Drafting and Filing the DRHP

The company appoints a SEBI-registered merchant banker (Book Running Lead Manager) to prepare and file the Draft Red Herring Prospectus with SEBI. This document must include:

- Audited financials for three complete years

- Risk factors and use of proceeds

- Promoter disclosures and capital structure

- Management's Discussion and Analysis

A well-prepared DRHP can be ready in 30 to 45 days from a clean data room. That window depends on how prepared the company is entering the process:

- Complete audited financials, legal opinions, facility lists, and KYC documents

- Board independence, audit committee structure, and internal controls in order

- Related-party transactions, promoter contribution sourcing, and Ind-AS restatements fully disclosed

Companies that lack these inputs face remediation cycles that can add weeks to the DRHP stage.

SEBI Review and Observations

SEBI reviews the DRHP within 30 days and may issue an observation letter with queries. The issuer and lead manager must respond before filing the final Red Herring Prospectus (RHP). SEBI approval confirms regulatory compliance — it is not an endorsement of investment merit.

The DRHP remains publicly available for at least 21 days for public comments. Once SEBI issues its observation letter and the company addresses all queries, the IPO must open within 12 months (extended to 18 months under the optional pre-filing mechanism).

IPO Subscription Period

The offer remains open for 3 to 10 working days across all investor categories:

- Qualified Institutional Buyers (QIBs)

- Non-Institutional Investors (NIIs)

- Retail Individual Investors (RIIs)

Key rules:

- The price band (floor to cap) must be announced at least 2 working days before the offer opens

- The cap price cannot exceed 120% of the floor price

- If the price band is revised, the bidding period must be extended by at least 3 working days (total cannot exceed 10)

- QIB bidding can close 1 working day prior to the official close date, if disclosed in the RHP

Strong QIB oversubscription signals institutional confidence and typically sets the tone for listing day pricing — which makes the allotment process that follows closely watched by all investor categories.

Share Allotment and Basis of Allotment

The registrar finalises allotment within T+1 (1 working day after subscription closes):

- Retail investors receive allotment by lottery when the category is oversubscribed

- QIBs and NIIs receive proportional allotment based on their subscription levels

- SEBI mandates public announcement of the allotment basis

- Non-allotted funds are unblocked from ASBA accounts by 9:00 PM on T+1

Share Credit, Refunds, and Listing Date Announcement

T+2: Allotted shares appear in demat accounts. The company files the listing application with stock exchanges.

T+3: Shares list and commence trading on NSE and BSE.

This timeline is mandatory for all equity public issues opening on or after December 1, 2023, under SEBI Circular No. SEBI/HO/CFD/TPD1/CIR/P/2023/140.

IPO Listing Day: Trading Sessions and Timings Explained

Listing day splits into two distinct phases: a Special Pre-Open Session designed for newly listed securities, followed by normal continuous trading. This pre-open session is separate from the regular daily pre-open that applies to all listed stocks.

Special Pre-Open Session (9:00 AM to 10:00 AM)

| Phase | Timing | Details |

|---|---|---|

| Order Entry Period | 9:00 AM to 9:45 AM | Investors can place, modify, or cancel limit orders only. System-driven random closure occurs between 9:35 AM and 9:45 AM. |

| Order Matching & Trade Confirmation | 9:45 AM to 9:55 AM | Exchange determines equilibrium (opening) price and matches orders. No modification or cancellation permitted. |

| Buffer Period | 9:55 AM to 10:00 AM | Transition from pre-open to normal market. No orders accepted. |

Key rules during pre-open:

- Only limit orders are accepted (market orders are not permitted)

- The base price for IPOs is the issue price

- Unmatched limit orders within the applicable price range carry forward to normal trading at their limit price

Continuous Trading (10:00 AM to 3:30 PM)

At 10:00 AM, the stock enters continuous trading. Unmatched orders from the pre-open session are carried over at the discovered opening price. Freshly listed stocks are subject to circuit limits of 20% above or below the discovered opening price — not the issue price — during this session.

The IPO issue price and the listing (opening) price are not the same thing. The opening price is discovered through live order matching in the pre-open session and reflects actual demand at that moment — which is why listing pops and discounts both happen at the open, not at allotment.

How the Listing Price Is Determined for a Mainboard IPO

The listing price emerges from a call auction mechanism in the Special Pre-Open Session. Buy and sell orders placed between 9:00 AM and 9:45 AM are matched to find the equilibrium price at which the maximum number of shares can be traded.

Price Discovery Hierarchy

- Maximum volume: The price at which the maximum executable volume (number of shares) can be traded

- Minimum imbalance: If multiple prices yield the same volume, the price with the smallest unmatched quantity is chosen

- Closest to base price: If imbalance is equal, the price closest to the issue price is selected

Demand-Side Factors

QIB oversubscription as institutional confidence indicator:

An academic study by Suresh A.S. (2012, PES University) found a correlation of 0.8233 between QIB subscription levels and IPO returns, significantly higher than the correlation with IPO grading (0.5035). High QIB oversubscription serves as a reliable proxy for institutional confidence.

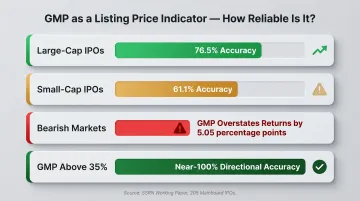

Grey Market Premium (GMP):

GMP operates in informal, unregulated markets and is not recognised by SEBI. A recent SSRN working paper analysing 205 mainboard IPOs found an overall correlation of r = 0.913 between GMP and listing-day underpricing, but reliability varies sharply:

- Large-cap IPOs: 76.5% accuracy

- Small-cap IPOs: 61.1% accuracy (near coin-flip)

- In bearish markets: GMP systematically overestimates returns by 5.05 percentage points

- GMP above 35% threshold: near-100% directional accuracy

GMP data comes from informal sources. Use it as a directional indicator — not a forecast.

Market-Context Factors

- Broader Nifty/Sensex direction on listing day

- Sector-specific news or sentiment in the preceding week

- Global market conditions

Each of these factors can shift sentiment quickly. Even a well-subscribed IPO can list flat or at a discount if the macro environment deteriorates sharply between subscription close and listing date.

Green Shoe Option (Price Stabilisation Mechanism)

Because listing prices can fall below issue price when market conditions turn, SEBI provides a formal stabilisation mechanism. Governed by Regulation 45 of SEBI ICDR Regulations 2018:

- Maximum over-allotment: 15% of issue size

- Stabilisation period: not exceeding 30 days from trading permission

- The stabilising agent (typically a merchant banker or book runner) borrows shares from promoters, over-allots to investors, and buys from the market if the post-listing price falls below issue price

- Excess funds are transferred to the SEBI Investor Protection and Education Fund (IPEF)

What Founders and Investors Often Get Wrong About the Mainboard IPO Listing Process

Founder Misconception: The Process Ends on Listing Day

Many founders believe listing day marks the finish line. The 30 to 90 days after listing — covering investor relations, analyst engagement, and price stabilisation — often determine whether that opening pop becomes lasting value or fades quietly.

Experienced investment banks like S45 build post-listing IR support into the engagement, including:

- Earnings call preparation and quarterly results materials

- Analyst education and coverage coordination

- Liquidity monitoring and market maker coordination (for SME listings)

- Investor access programs and non-deal roadshows (investor meetings not tied to a capital raise)

Investor Misconception: Active Trading During Pre-Open

Many retail investors believe they can actively trade during the 9:00–9:45 AM window the way they would in normal sessions. They cannot. Order matching does not occur until 9:45 AM, and no new orders are accepted during the buffer period (9:55 AM to 10:00 AM).

Placing a sell limit order during the pre-open session is technically possible, but execution depends on whether a matching buy order exists at that price. Unmatched orders carry over to continuous trading at the discovered opening price — not the price the seller specified.

Timeline Misconception: Stock Lists in 2–3 Days

Many founders expect listing within 2–3 days of subscription close and are caught off-guard by the allotment, demat credit, and refund steps that precede listing. The current T+3 framework sets realistic expectations. Delays are usually caused by:

- Incomplete documentation (missing audit opinions, facility lists, KYC)

- Registrar bottlenecks during allotment

- Unresolved SEBI observations

Most of these delays are preventable with early diagnosis. S45's AI-led readiness scans surface financial restatement needs, promoter disclosure gaps, and governance issues within 5 business days (preliminary) or 2 to 3 weeks (comprehensive) — before they become last-minute blockers.

Frequently Asked Questions

What time do IPO stocks open in the pre-open market?

The Special Pre-Open Session for newly listed IPO stocks begins at 9:00 AM. Investors can place limit orders from 9:00 AM to 9:45 AM. The opening price is determined through order matching between 9:45 AM and 9:55 AM, with normal continuous trading commencing at 10:00 AM.

Can I sell IPO shares during the pre-open market?

Yes, allotted shareholders can place a sell limit order during the pre-open session (9:00 AM to 9:45 AM). However, execution depends on whether a matching buy order exists at that price. If unmatched, the order carries over to the continuous session at the discovered opening price.

How many days after the subscription close does a Mainboard IPO list?

Under SEBI's current T+3 framework (mandatory since December 1, 2023), a Mainboard IPO lists within 3 working days of the subscription close date. This window covers allotment finalisation, ASBA unblocking, and demat credit of shares before trading commences.

How is the listing price of a Mainboard IPO determined?

The listing price is discovered through a call auction mechanism in the Special Pre-Open Session on listing day. Buy and sell orders placed from 9:00 AM to 9:45 AM are matched to find the equilibrium price at which the maximum number of orders can be executed.

Is there a circuit limit on a stock's price on its listing day?

Yes. During continuous trading (10:00 AM to 3:30 PM), exchanges apply 20% circuit limits above or below the discovered opening price. In the pre-open session, "dummy circuit filters" set an operating range of 25%–75% of the issue price, expandable in 10% increments.

What is the difference between the IPO issue price and the listing price?

The issue price is the fixed price at which the company offered shares during the subscription period. The listing price is the market-discovered opening price on listing day, set through live order matching in the pre-open session. A stock lists at a premium when demand exceeds supply, and at a discount when it falls short.