Introduction

SME to Main Board migration is the process by which a company already listed on BSE SME or NSE Emerge formally transitions its listed securities to the mainboard exchange — a milestone that signals maturity, scale, and readiness for institutional scrutiny. Yet despite its strategic importance, this pathway remains widely misunderstood by the founders, promoters, and compliance officers it affects most directly.

Many companies approaching eligibility thresholds assume that meeting financial criteria automatically unlocks mainboard access. The data says otherwise: only 336 of 1,420 SME-listed companies (24%) successfully migrated between 2015 and 2025. In 2021, 65 companies completed the journey; by 2025, that number had collapsed to just three — a 95% decline in migration volume.

This guide is written for leadership teams of SME-listed Indian companies approaching migration eligibility who need clarity on why the process is harder than it looks.

It covers the dramatically tightened 2025 criteria from BSE and NSE, the operational reality of mainboard governance, and the hidden constraints — beyond the financial thresholds — that determine who actually gets through.

Key Takeaways

- Migration transfers already-listed SME shares to the mainboard — it's not a fresh IPO and requires no SEBI-approved DRHP

- BSE and NSE tightened eligibility in 2024-2025: market cap threshold rose from ₹25 crore to ₹100 crore, and minimum listing tenure increased to 3 years

- Public shareholder minimums now stand at 1,000 (BSE) and 500 (NSE) — both up from earlier benchmarks

- The process spans 3.5 to 6 months and includes shareholder approval via postal ballot, exchange application, compliance audits, and information memorandum filing

- Migration unlocks institutional investor access, eliminates ₹2 lakh lot-size barriers, removes mandatory market maker requirements, and typically improves valuation multiples

- Financial eligibility alone doesn't guarantee approval — SEBI SCORES records, trading history, surveillance cooling-off periods, and resolved audit qualifications are equally critical

What Is SME to Main Board Migration?

Migration is not a fresh IPO. It is the formal transfer of already-listed securities from BSE SME or NSE Emerge to the mainboard exchange of the same bourse, governed by SEBI (ICDR) Regulations 2018, Chapter IX.

No new capital is raised, existing shareholders retain their holdings, and the share structure carries forward intact.

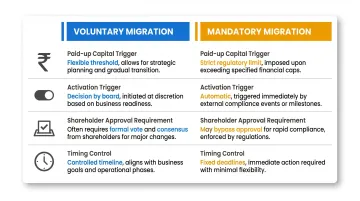

Two regulatory triggers govern when and how a company migrates:

| Voluntary Migration | Mandatory Migration | |

|---|---|---|

| Paid-up Capital | ₹10 crore – ₹25 crore | Crosses ₹25 crore |

| Trigger | Board decision | Automatic (rights issue, preferential allotment, bonus issue) |

| Shareholder Approval | Special resolution via postal ballot | Required |

| Timing Control | Promoter-driven | Regulated deadline |

SEBI has proposed letting companies above ₹25 crore remain on SME platforms if they voluntarily comply with full mainboard LODR obligations — but as of now, this proviso has not been notified.

Migration also differs from a fresh Main Board IPO in process. There is no book-building, no pricing discovery, and no new share issuance. Instead, the company files an information memorandum — signed by the MD or Company Secretary — demonstrating compliance with mainboard governance thresholds.

The exchange then reviews financials, liquidity metrics, compliance history, and shareholder distribution before approving or rejecting the application.

Why SME-Listed Companies Choose to Migrate

Capital Access and Investor Base Expansion

The SME platform imposes a minimum application size of ₹2 lakh per investor — a structural barrier that excludes most retail participants. Post-migration, shares trade in standard lots of one share, sharply lowering the entry point and opening the stock to a significantly larger retail and institutional investor base.

This shift improves price discovery, expands liquidity, and broadens the investor profile beyond high-net-worth individuals to include mutual funds, insurance companies, and foreign portfolio investors who typically avoid SME counters.

Valuation Uplift and Analyst Coverage

Mainboard-listed companies command higher valuation multiples due to perceived governance quality, transparency, and institutional participation. Research coverage by sell-side analysts becomes viable post-migration, as brokerage firms rarely dedicate resources to illiquid SME stocks. Enhanced visibility drives better price realization during secondary fundraising and strategic exits.

Post-migration return data illustrates the potential: Zota Health Care delivered 511% returns from its April 2017 listing through February 2026, while Manorama Industries delivered 295% returns from its September 2018 listing. While these figures reflect overall listing performance rather than exclusively post-migration gains, they demonstrate the trajectory available to well-governed, growth-oriented companies that successfully complete the transition.

Operational and Compliance Benefits

Migration delivers tangible operational improvements across three dimensions:

- Eliminates the mandatory market maker requirement, cutting ongoing compliance costs and removing artificial liquidity support

- Reduces margin requirements for traders by shifting to a lower stock group, making the stock more attractive for intraday and positional activity

- Improves float turnover through institutional participation, reducing volatility and stabilizing price discovery

Eligibility Criteria: BSE SME and NSE Emerge Requirements

Both BSE and NSE updated their migration criteria significantly in 2024-2025, raising the bar considerably and directly contributing to the sharp decline in successful migrations. The changes reflect a deliberate policy shift toward quality control, ensuring that only financially sound, mature, and well-governed companies transition to the mainboard.

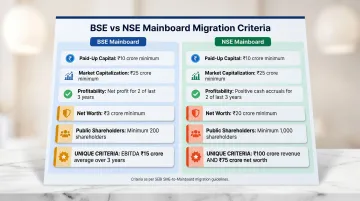

BSE SME to BSE Mainboard Criteria

BSE revised its eligibility framework in August 2025, implementing the most significant tightening in migration history. The core thresholds are:

Financial Metrics:

- Minimum paid-up capital: ₹10 crore

- Average market capitalisation: ₹100 crore over the last 6 months (up from ₹25 crore)

- Average EBITDA: ₹15 crore over 3 years with minimum ₹10 crore in each year

- Net worth: ₹1 crore per year for 3 consecutive years

- Net tangible assets: ₹3 crore per year for 3 consecutive years

- Public shareholders: Minimum 1,000 (up from 250)

Market Liquidity Requirements — a frequently overlooked hard filter:

- Trading on at least 80% of market days in the preceding 6 months

- Minimum 5% of listed shares traded in the preceding 6 months

- Average daily turnover: ₹10 lakh

- Minimum daily turnover: ₹5 lakh

- Average daily trades: Minimum 50

This liquidity gate catches companies with technically compliant financials but illiquid stocks. A company meeting the ₹100 crore market cap threshold but failing to sustain ₹10 lakh daily turnover will not qualify, regardless of profitability or net worth.

NSE Emerge to NSE Mainboard Criteria

NSE updated its criteria in May 2025, introducing net worth and revenue thresholds that diverge significantly from BSE's approach:

Financial Metrics:

- Minimum paid-up capital: ₹10 crore

- Average market capitalisation: ₹100 crore (3-month average of weekly high/low closing prices)

- Revenue from operations: Greater than ₹100 crore in the last financial year

- Net worth: At least ₹75 crore

- EBITDA: Positive operating profit in at least 2 of the last 3 financial years

- Public shareholders: Minimum 500

Promoter Retention Requirement:

- Promoters must hold at least 50% of their listing-day shareholding at the time of application

NSE's ₹100 crore revenue threshold doesn't appear in BSE's criteria at all — it screens for top-line scale, not just profitability. The ₹75 crore net worth requirement is 75× higher than BSE's ₹1 crore annual standard, making balance-sheet strength a genuine filter rather than a formality.

These financial divergences matter when choosing which exchange to target. Companies with strong revenue but modest net worth may find BSE's path more viable; those with clean balance sheets but thinner top lines may prefer BSE's approach.

Compliance and Governance Gatekeepers

Both exchanges enforce compliance thresholds that frequently stall applications:

- Minimum 3 years listed on the SME platform (extended from 2 years before January 2024)

- Zero pending investor complaints on SEBI's SCORES platform at the time of application

- 2-month cooling-off period after removal from ESM, ASM, GSM, or T2T surveillance categories

- 100% promoter shareholding held in demat form

- No SEBI debarment orders, no NCLT winding-up petitions, no wilful defaulter or fugitive economic offender classification

- No defaults on interest or principal debt payments

Compliance failures derail more applications than financial shortfalls. A SCORES complaint filed three months before submission — or a T2T surveillance exit without the required cooling-off — will block approval even for a company that clears every financial threshold. Resolving these issues before filing, not during the process, is what determines whether the timeline stays on track.

The Migration Process: From Assessment to Listing

Step 1: Eligibility and Readiness Assessment

The first step is conducting a detailed gap analysis against both financial and compliance criteria. Companies often discover they are financially eligible but have clean-up work to do on investor complaints, surveillance history, or documentation gaps.

For SME-listed companies considering migration, S45 conducts structured readiness diagnostics through AI-led document auditing. The preliminary scan delivers a readiness score and fix list within 48 hours, flagging immediate gaps in contracts, consents, and order book disclosures.

The comprehensive scan extends this to governance structures, board and committee formation, ICDR eligibility, export/offset and security clearances, milestone revenue policies, and IND-AS restatements — catching issues before they surface at the exchange review stage.

Step 2: Board Resolution and Shareholder Approval

Voluntary migration requires a special resolution passed through postal ballot, with non-promoter votes in favor at least 2 times (2x) the votes cast against. The voting period spans 30 days from the date of dispatching the notice, which must be advertised in one English and one vernacular daily. A scrutinizer oversees the voting process, and Form MGT-14 must be filed with the Registrar of Companies within 30 days of result declaration.

Step 3: Documentation and Information Memorandum Preparation

The key documents required include:

- Information memorandum (signed by MD or Company Secretary)

- Three years of audited financial statements (restated to IND-AS if applicable)

- Market capitalisation and liquidity certificates from the exchange

- Credit rating agency certificate on IPO proceeds utilization

- Corporate governance compliance report

- SEBI SCORES confirmation of no pending complaints

- Promoter demat certificates

- Evidence of surveillance cooling-off compliance

S45's AI-native approach adds specific value at this stage through:

- Evidence-linked drafting within a live data room, so every disclosure has a verifiable source

- Versioned virtual data rooms (VDRs) with audit trails and responsibility matrices

- Regulatory checklist automation aligned with SEBI and exchange requirements

Step 4: Exchange Application and Review

The application with all supporting documents is filed with the exchange, which conducts its own due diligence, may seek clarifications, and retains the right to reject applications where criteria are unmet or information is incomplete.

BSE processing fee: ₹2 lakh or 0.05% of market capitalisation, whichever is higher.

Step 5: Migration Approval and Commencement of Trading

Upon approval, the company's shares are transferred to the mainboard segment, and full SEBI LODR 2015 compliance obligations take effect immediately. These include:

- Quarterly financial reporting (versus half-yearly for SME)

- Mandatory board committees: Audit, Nomination & Remuneration, Stakeholders Relationship, and Risk Management

- Appointment of independent directors

- Secretarial audits

- BRSR reporting for applicable entities

- Expanded website and newspaper disclosure requirements

Total timeline from application to trading: 3.5 to 6 months, depending on company readiness and exchange review timelines.

Common Pitfalls, Misconceptions, and When Not to Migrate

Misconception 1: Financial Threshold Compliance Guarantees Approval

The most common error is assuming that meeting financial thresholds alone ensures approval. In practice, many applications are stalled or rejected because of:

- Unresolved investor complaints on SEBI SCORES

- Recent surveillance category history (ESM, ASM, T2T, GSM) without completing the 2-month cooling-off period

- Pending litigation disclosure gaps or incomplete evidence trails

- Audit qualifications related to financial reporting or internal controls

Companies should treat compliance hygiene as a continuous pre-migration investment, not a last-minute cleanup.

Misconception 2: Market Capitalisation Calculation Is Uniform

BSE uses a 6-month weighted average of daily market cap on all traded days, while NSE uses a 3-month average of weekly high/low closing prices. A company that meets the threshold under one method may not qualify under the other. Fluctuating share prices close to the ₹100 crore threshold make timing the application critical — submitting during a price dip can result in rejection.

When Migration May Not Be the Right Move

Eligibility thresholds are only part of the picture. Several operational and structural factors can disqualify an otherwise financially ready company — or make migration inadvisable even when eligibility is technically met:

- Trading activity below BSE's liquidity norms: Your stock must trade on at least 80% of market days and sustain ₹10 lakh in daily turnover — failing either gate rules out BSE migration regardless of market cap

- Less than 3 years of listing history: Both exchanges enforce a strict 3-year minimum tenure

- Recent name changes without revenue continuity: If the company changed its name in the last year, 50% of revenue must come from the business activity reflected in the new name

- Promoter dilution below NSE's retention floor: NSE requires promoters to retain at least 50% of their listing-day shareholding; companies that have diluted below this threshold will not qualify

Companies that migrate before building governance infrastructure often spend more on compliance than they save in capital-raising costs. Moving from half-yearly to quarterly reporting, standing up mandatory board committees, and meeting BRSR disclosure requirements are not administrative formalities — they require dedicated capacity.

Ensure your organisation can absorb these obligations before initiating migration, not after.

Frequently Asked Questions

What are the criteria for SME to main board migration?

Both BSE and NSE require a minimum 3-year listing history, paid-up capital of at least ₹10 crore, average market cap of ₹100 crore, profitability thresholds, clean regulatory record, and minimum public shareholders. BSE mandates ₹15 crore average EBITDA over 3 years and 1,000 public shareholders, while NSE requires ₹100 crore revenue from operations, ₹75 crore net worth, and 500 public shareholders.

What is the difference between an SME listing and a main board listing?

SME listings operate under lighter regulations with market maker requirements, higher lot sizes (minimum ₹2 lakh), and relaxed governance norms. Mainboard listings remove lot-size restrictions, attract institutional investors and analyst coverage, require full SEBI LODR compliance, and typically command higher valuation multiples.

How many shareholders must a company have to migrate from NSE SME to the NSE main board?

As per NSE's May 2025 criteria, a minimum of 500 public shareholders is required at the time of application. BSE requires 1,000 public shareholders as of its August 2025 update, up from the earlier requirement of 250.

How long does the SME to main board migration process take?

The process typically takes 3.5 to 6 months from initial assessment to trading commencement on the mainboard, depending on company readiness, documentation completeness, and exchange review timelines. Unresolved compliance gaps or illiquid trading history can extend this significantly — or result in rejection.

What is the difference between voluntary and mandatory migration to the main board?

Voluntary migration applies when post-issue paid-up capital is above ₹10 crore but below ₹25 crore — the company chooses to migrate by passing a special resolution through postal ballot. Mandatory migration is triggered when paid-up capital exceeds ₹25 crore, at which point the company must compulsorily migrate to the mainboard.

What happens to existing shareholders when a company migrates from SME to mainboard?

Existing shareholders retain their shares without dilution, and no new allotment occurs unless the company runs a concurrent fundraise. The minimum trading lot shifts from the SME's lot-based structure (minimum ₹2 lakh) to single-share trading on the mainboard, which generally improves liquidity.