Introduction

Most founders approaching a BSE listing don't know what their IPO price will be until the market tells them — and that's exactly how book building is designed to work. Rather than declaring a fixed price upfront, the company offers shares within a defined price band and collects investor bids over a three-day subscription window.

The Book Running Lead Manager (BRLM) then analyses actual demand at each price level and determines the final issue price once bidding closes.

This article breaks down the book building process for founders and promoters preparing to list on BSE — covering operational requirements, SEBI mandates, and the full timeline from DRHP filing through listing day.

Key Takeaways

- Book building determines IPO price through investor bidding within a SEBI-mandated price band

- Process governed by SEBI ICDR Regulations; applies to BSE Main Board and SME listings

- Key stages: DRHP filing → SEBI approval → 3-day bidding window → listing within T+3 days of IPO closure

- BRLM manages the order book, builds institutional demand, and determines the final cut-off price

- Book building is now standard for BSE IPOs; fixed price offerings are the exception

What Is Book Building in a BSE IPO?

SEBI defines book building as "a process of price discovery" in which the issuer discloses a price band and the Book Running Lead Manager (BRLM) determines the issue price based on bids received across price levels. The company and BRLM collect investor bids over a defined subscription window, then set the final price — called the cut-off price — at the level where demand fully covers the offer.

This market-driven mechanism aligns the issue price with genuine investor willingness to pay, reducing the risk of chronic overpricing or underpricing.

Book building differs from a fixed price issue in one fundamental way: who sets the price and when.

| Book Building | Fixed Price Issue | |

|---|---|---|

| Price determination | Emerges from investor bids | Declared by the company before opening |

| Investor role | Bid within a price band | Apply at the stated price |

| Best suited for | Most BSE listings today | Small, straightforward issues |

Because book building is the standard for most BSE listings, SEBI has formalized its structure under Regulation 43 of SEBI ICDR 2018, which mandates the bidding period remain open for a minimum of three working days.

How the BSE IPO Book Building Process Works

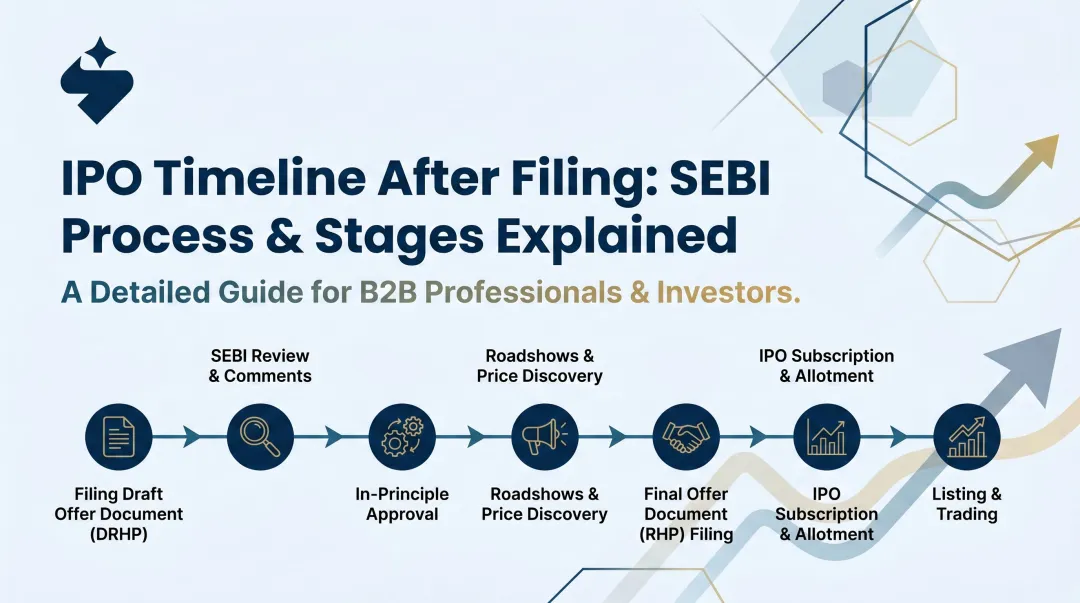

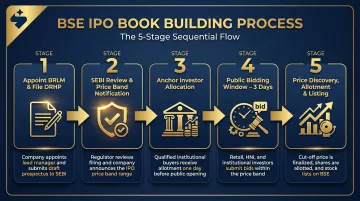

The process runs in a structured sequence:

- Appoint BRLM and file DRHP

- SEBI review and price band notification

- Anchor investor allocation

- Public bidding window (minimum 3 days)

- Price discovery, allotment, and listing

The BRLM manages a live order book throughout the subscription period, tracking real-time demand across investor categories (QIBs, NIIs, retail) at different price points. This real-time view lets the BRLM identify demand gaps early and adjust outreach before the window closes.

Step 1: Appointing the BRLM and Filing the DRHP

The company appoints a SEBI-registered Book Running Lead Manager who co-drafts the Draft Red Herring Prospectus (DRHP) — the core disclosure document filed with SEBI before the IPO opens. The DRHP does not contain the final price, only the price band, which is set based on:

- Company valuation using sector comparables

- Cash-flow and earnings multiples

- Market conditions and investor appetite

For example: S45, an AI-native BRLM operating with Narnolia as Category-I Merchant Banker, uses proprietary readiness scans to identify gaps in financials, governance, and compliance before DRHP filing. This ensures the document is evidence-backed and minimizes delays caused by incomplete disclosures.

DRHP drafting typically takes 30–45 days from a clean data room, issuer-dependent.

Step 2: SEBI Review and Price Band Notification

SEBI reviews the DRHP and issues observations, typically within 30 days for Main Board IPOs (per Regulation 25 of SEBI ICDR). For BSE SME, the exchange itself reviews the DRHP, not SEBI directly, which can compress the timeline.

After SEBI observations are addressed, the company files the Red Herring Prospectus (RHP) with the confirmed price band.

SEBI caps the price band spread: the upper price cannot exceed 120% of the floor, and the spread must fall between 5% and 20%.

Step 3: Anchor Investor Allocation (One Day Before IPO Opens)

For Main Board IPOs with QIB allocation, the BRLM allocates up to 60% of the QIB portion to anchor investors on the day before the public issue opens.

Anchor investor lock-in (current regulation, effective April 1, 2022):

- 50% of shares locked for 90 days from allotment

- Remaining 50% locked for 30 days from allotment

This phase signals institutional conviction and directly shapes retail and HNI sentiment. S45 identifies anchor investors through targeted outreach to domestic and global sector specialists, long-only funds, insurance companies, and AIFs, with diligence kits prepared under SEBI PIT (Prohibition of Insider Trading) regulations.

Step 4: The Bidding Window

The IPO opens for public subscription for a minimum of 3 working days. During this period:

- Retail investors, NIIs, and QIBs submit bids via ASBA or UPI through registered intermediaries

- Bids can be placed at any price within the band or at the cut-off price (available to retail and eligible employees only)

- The BRLM monitors live subscription data and can adjust outreach if demand is uneven across investor categories

Cut-off price bidding: Only retail individual investors (applying for up to ₹2,00,000) may bid at the cut-off price, accepting whatever final price is discovered. QIBs and NIIs must bid at specific prices within the band.

If needed, the BRLM may revise the price band during this window — requiring a mandatory 3-working-day extension and adequate public notice.

Step 5: Price Discovery, Allotment, and Listing

After bidding closes, the BRLM and issuer analyze cumulative demand at each price point across all categories. The BRLM and issuer finalize the cut-off price at the level where the issue is fully subscribed.

Current listing timeline (updated August 2023):

- T+1: Allotment finalized

- T+2: Refunds/unblocking of funds completed

- T+3: Listing and commencement of trading on BSE

This timeline was reduced from the earlier T+6 framework via SEBI Circular SEBI/HO/CFD/TPD1/CIR/P/2023/140, mandatory from December 1, 2023.

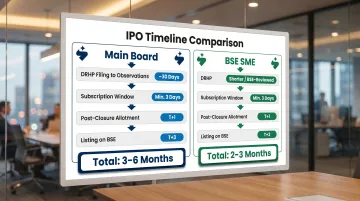

BSE Book Building Timeline: From DRHP Filing to Listing

End-to-end timeline:

| Stage | Main Board | BSE SME |

|---|---|---|

| DRHP filing to SEBI observations | ~30 days | Shorter (BSE-reviewed) |

| RHP filing and subscription window | Minimum 3 days | Minimum 3 days |

| Post-closure allotment | T+1 | T+1 |

| Listing on BSE | T+3 | T+3 |

| Total elapsed time (DRHP to listing) | 3–6 months | 2–3 months |

BSE SME-specific features:

- Minimum application size: ₹2,00,000 (doubled from ₹1 lakh in December 2024)

- Minimum allottees: 200 (increased from 50)

- Market maker requirement: Mandatory for 3 years from listing; market maker must hold at least 5% of post-issue capital

- DRHP reviewed by BSE, not SEBI

The timeline above reflects the regulated stages. The biggest variable is what happens before DRHP filing — financial restatement per Ind-AS, legal due diligence, auditor certificates, and readiness assessments. Companies that arrive with clean documentation compress every subsequent stage. Those that don't often stall at SEBI observations.

Once the subscription window opens, oversubscription dynamics take over. If aggregate demand across all categories exceeds the shares offered, the issue is oversubscribed. QIB allotment is proportionate to bids; retail allotment follows a lottery. The BRLM's job is to generate demand from investors who intend to hold — not speculative churn that inflates subscription figures but collapses on listing day.

Price band revisions are permitted by SEBI under specific conditions, but they carry a cost. Any revision requires adequate public notice and a mandatory 3-working-day extension to the subscription window. Issuers who revise mid-window signal that initial pricing missed market demand — which institutional investors notice. A revision handled transparently with clear rationale is manageable; one that looks reactive erodes the book's quality heading into allotment.

SEBI Guidelines and Key Rules Governing BSE Book Building

Three core SEBI ICDR rules shape how every book-built IPO on BSE is structured and priced:

- 100% underwriting — The issue must be fully underwritten before opening (Regulation 40).

- Price band cap — The cap price cannot exceed 120% of the floor price, capping the spread at 20% (SEBI ICDR Regulations).

- Minimum subscription threshold — If subscriptions fall below 90% of the issue size by close, the issuer must refund all application money (Schedule VIII, Part A of SEBI ICDR 2018).

Anchor investor lock-in rules:

- 50% locked for 90 days, 50% for 30 days

- Mandatory 1-day gap between anchor allocation and public issue opening

- Governed by Schedule XIII and Regulation 44 of SEBI ICDR

The 2021 amendment also revised promoter lock-in periods, cutting what was previously a blanket 3-year requirement:

Promoter lock-in requirements (post-2021 amendment):

| Promoter Lock-In Category | Non-Capex Issues | Capex-Majority Issues |

|---|---|---|

| Minimum Promoters' Contribution (20%) | 18 months | 3 years |

| Excess over MPC | 6 months | 1 year |

These changes came into effect via the SEBI (Issue of Capital and Disclosure Requirements) (Third Amendment) Regulations, 2021.

Investor Categories, Allocation Norms, and the BRLM's Role

Three statutory investor categories:

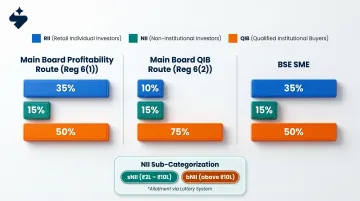

Main Board (Profitability Route – Regulation 6(1)):

- Retail Individual Investors (RII): Not less than 35% of net offer

- Non-Institutional Investors (NII): Not less than 15% of net offer

- Qualified Institutional Buyers (QIB): Not more than 50% of net offer

Main Board (QIB Route – Regulation 6(2)):

- QIB: At least 75% of net offer

- NII: Not more than 15% of net offer

- RII: Not more than 10% of net offer

BSE SME allocation norms:

- Retail: At least 10%

- Non-Institutional: At least 15%

NII sub-categorization (post-April 2022 amendment):

- Small NII (sNII): Applications between ₹2 lakh and ₹10 lakh — at least 1/3 of NII quota

- Big NII (bNII): Applications above ₹10 lakh — remaining 2/3 of NII quota

- Allotment method: Draw of lots (lottery), replacing proportionate allotment

The BRLM's operational role during book building:

The BRLM carries active execution responsibility throughout the bookbuilding window. Core duties include:

- Managing the order book in real time and monitoring category-wise subscription levels

- Coordinating with syndicate members and sub-brokers to sustain application flow

- Ensuring ASBA and UPI application processing runs without breaks

- Advising the issuer on cut-off price based on demand data

- Managing ongoing communication with BSE and SEBI

The calibre of a BRLM's institutional relationships and demand-mapping rigour shapes the quality of the book — not just its size. A firm like S45 uses proprietary analytics to track bid composition across QIB, NII, and retail categories in real time, running pre-IPO soundings and anchor investor mapping before the subscription window opens. The focus is on clean, disciplined books rather than inflated headline subscription numbers.

Cut-off price explained:

The BRLM's price advisory role connects directly to how the cut-off price works for each investor category:

- Retail investors can bid at the cut-off price without specifying an exact figure, accepting whatever price the book discovers

- QIBs and NIIs must bid at specific prices within the price band

- Investors who bid below the final cut-off price do not receive allotment and are refunded in full

Book Building vs. Fixed Price Issue: What BSE Issuers Should Know

| Feature | Book Building | Fixed Price |

|---|---|---|

| Price determination | Demand-based price discovery within band | Issuer-set fixed price |

| Demand visibility | Real-time during subscription window | Unknown until subscription closes |

| Cut-off price mechanism | Yes (retail investors can bid at cut-off) | No |

| Pricing accuracy | Aligns with market willingness to pay | Risk of overpricing or underpricing |

| Main Board usage | Default/mandatory for Regulation 6(2) route | Available for Regulation 6(1) route |

| SME trend | Increasing adoption | Traditional method, declining |

Many founders assume a lower fixed price guarantees higher subscription, while book building "risks" under-subscription. In practice, a well-executed book building IPO — backed by proper demand mapping and institutional anchoring — produces stronger listing outcomes than a mispriced fixed price issue. What drives results is the quality of preparation before the subscription window opens, not the method itself.

Most BSE Main Board IPOs today use book building by default. Among SME IPOs, the trend is shifting in the same direction — though very small issues occasionally retain fixed price for simplicity. For most issuers serious about price discovery and institutional participation, book building is the relevant framework to understand.

Frequently Asked Questions

What is book building in an IPO?

Book building is the price discovery mechanism in which the company offers shares within a price band (floor to cap) and investors bid over a defined window. The final issue price is set at the level where demand fully covers the offer.

Who manages the book building process in an IPO?

A SEBI-registered Book Running Lead Manager (BRLM), an investment bank appointed by the issuer, manages the entire process. This includes setting the price band, building the order book, determining the cut-off price, and coordinating allotment with BSE.

What is the difference between fixed price IPOs and book building IPOs?

A fixed price issue sets a single price before the IPO opens with no bidding. Book building uses a price band and lets investors bid, with the final price emerging from actual demand. SEBI regulations favor book building for Main Board listings, and it now accounts for the overwhelming majority of BSE IPOs.

How long does the BSE book building process take?

The subscription window is a minimum of 3 working days. Allotment is processed by T+1, and listing on BSE occurs by T+3. Total time from DRHP filing to listing ranges from 3 to 6 months, depending on SEBI review timelines and issuer readiness.

What is the price band in a BSE book building IPO?

The price band is the range (floor to cap) within which investors can bid, set by the issuer and BRLM based on company valuation. SEBI mandates that the cap price cannot exceed 120% of the floor price (maximum 20% spread).

What happens if a BSE IPO is oversubscribed during book building?

If demand exceeds the shares offered, QIBs receive proportionate allotment while retail investors are allotted shares via a lottery system. Investors who bid at or above the cut-off price but miss allotment receive a full refund of their blocked funds.