Introduction

Many companies preparing to list on Main Board or SME exchanges face the same fundamental question: how will the market actually price our shares? The book building process is the mechanism by which an IPO price is discovered through structured investor demand, rather than being fixed in advance by the issuer.

For founders, CFOs, and investors alike, understanding how that price gets set — and why a poorly run book can cost both sides significantly — is not optional background knowledge. It's operational.

Book building is widely referenced in IPO conversations, but the mechanics — price bands, cut-off pricing, weighted averages, allotment logic — are rarely explained in full. This leaves issuers and investors navigating the process without a clear map, often discovering the specifics too late to act on them. This guide walks through every stage: how demand is gathered, how the issue price is determined, and what drives allotment decisions across investor categories.

Key Takeaways

- Book building is SEBI's mandated method for price discovery in most Indian IPOs, replacing the older fixed-price approach

- The issuer and BRLM set a price band; investors bid within that range over a defined subscription window

- Final issue price (cut-off) is determined by the level at which total demand equals or exceeds shares offered

- QIB, NII, and Retail categories receive separate allocation quotas; all bids at or above cut-off receive shares

- Book quality — not subscription multiples alone — drives listing stability and signals credibility to the market

What Is the Book Building Process in an IPO?

Book building is a systematic process of generating, capturing, and recording investor demand for shares during an IPO. The final issue price is determined after the bidding period closes, based on aggregated demand at various price points.

Regulatory Definition: Under Regulation 43 of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018, book building is defined as a "systematic mechanism for price discovery and allocation of securities." The issuer discloses a price band (floor and cap) in the Red Herring Prospectus, and investors bid within this band during the subscription window.

The mechanism was introduced in India in 1995 following recommendations by an expert committee under the chairmanship of Mr. Y.H. Malegam. The first book-built IPO was HCL Technologies in 1999, with SEBI introducing 100% book building later that year. That shift mattered: book building achieves price discovery that reflects real market appetite rather than promoter-set estimates, ensuring neither money is left on the table nor investor confidence eroded by overpricing.

Fixed Price vs. Book Building

In a fixed-price IPO, the price is declared upfront and investors apply at that price without input. In book building, the price emerges from the market itself through a structured bidding process.

SEBI mandates book building for companies that don't meet the profitability test under Regulation 6(1). Companies failing any of the following thresholds must use book building under Regulation 6(2):

- Net tangible assets of ₹3 crore

- Operating profit of ₹15 crore in 3 of the preceding 5 years

- Net worth of ₹1 crore

These issuers must also allocate at least 75% of the net offer to Qualified Institutional Buyers (QIBs).

Why Book Building Is the Preferred Method for IPO Pricing

Book building is SEBI's recommended approach because it aligns issue price with actual market demand, reduces post-listing price shocks, and creates a transparent audit trail of investor interest. In practice, it has become the de facto standard for any issuer targeting meaningful capital.

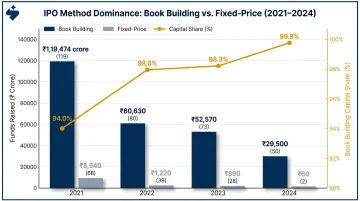

The numbers make the case clearly. In 2024, 178 of 248 IPOs used book building, raising ₹70,152 crore — 97% of total capital raised. Fixed-price issues raised only ₹2,145 crore across 70 offerings.

| Year | Book Building IPOs | BB Funds Raised (₹ Cr) | Fixed Price IPOs | FP Funds Raised (₹ Cr) | BB Share of Capital |

|---|---|---|---|---|---|

| 2024 | 178 | 70,152 | 70 | 2,145 | ~97% |

| 2023 | 165 | 49,437 | 77 | 3,165 | ~94% |

| 2022 | 91 | 58,154 | 58 | 1,142 | ~98% |

| 2021 | 105 | 1,19,882 | 17 | 264 | ~99.8% |

SEBI mandates book building because market-driven pricing consistently outperforms issuer-set pricing. The core rationale:

- Determines equity value based on actual investor demand, not promoter assumption

- Gives issuers real-time visibility into demand quality and credibility across investor categories

- Reduces post-listing volatility, supported by mechanisms like the 15% greenshoe option

- Cuts time and cost versus fixed-price processes

- Publishes live bid data on exchange websites, ensuring full transparency

That framework only holds when execution is disciplined. Poorly structured book building suffers from artificial demand inflation, price bands that are too wide or anchored incorrectly, and books that look subscribed on paper but are driven by short-term HNI leverage rather than genuine institutional conviction — all of which leads to weak listing performance.

How the Book Building Process Works, Step by Step

The book building process converts investor interest into a final issue price through five structured phases. Each phase has defined regulatory requirements, specific participants, and clear outputs — understanding them helps founders and CFOs anticipate what's ahead and prepare accordingly.

Step 1: Appointing the BRLM and Filing the DRHP

The issuer appoints a Book Running Lead Manager (BRLM) — typically a SEBI-registered investment bank — which advises on issue structure, drafts the Draft Red Herring Prospectus (DRHP), and files it with SEBI for review. The BRLM sets the preliminary price band based on financial benchmarking and comparable company analysis.

S45's Approach: S45 delivers a DRHP-ready draft in 30–45 days from a clean data room. A well-prepared data room includes:

- Audited financials (3 years, Ind-AS compliant)

- Legal opinions on title and compliance

- Promoter and director KYC documents

- Key contracts and licenses

- A clean cap table

The drafting environment links evidence directly from the data room, so financial and operational metrics stay consistent with pricing benchmarks throughout.

Step 2: Roadshow and Investor Education

Before the subscription window opens, the BRLM conducts a roadshow where the issuer's management presents to institutional investors, funds, and anchor investors. The goal is building informed demand and validating the price band before public bidding begins.

S45's Execution: S45 structures the roadshow with management training, an investor grid, and a meeting schedule that complies with SEBI's ICDR publicity guidelines, ensuring all communications meet fair disclosure standards. Pre-IPO soundings and demand mapping refine the valuation range and gauge institutional conviction before the window opens.

Step 3: Anchor Investor Allocation

One day before the IPO opens to the public, up to 60% of the QIB quota can be allocated to anchor investors at the upper end of the price band. This creates a price signal and public confidence. Anchor investors face a lock-in period: 50% of shares for 30 days and 50% for 90 days from allotment date.

Anchor Framework: Minimum allotment per anchor is ₹5 crore for Main Board IPOs (₹2 crore for SME). Investor count limits by allocation size:

| Allocation Size | Minimum Anchors | Maximum Anchors |

|---|---|---|

| Up to ₹250 crore | 2 | 15 |

| Above ₹250 crore (first ₹250 crore) | 5 | 15 |

| Each additional ₹250 crore beyond that | — | +15 |

Institutional Reservation: SEBI's November 2025 amendment expanded total reservation to 40%: 33% for mutual funds and 7% for life insurance companies and pension funds.

Step 4: Public Bidding Period

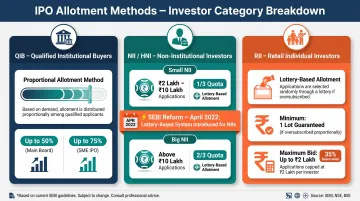

The IPO remains open for subscription (typically 3 working days under SEBI rules), during which QIBs, NIIs (Non-Institutional Investors / HNIs), and Retail Individual Investors place bids within the price band. All applications use ASBA (Application Supported by Blocked Amount), which became mandatory for all investor categories from January 1, 2016. Retail investors can bid at cut-off price, meaning they agree to receive shares at whatever final price is determined.

UPI-ASBA: Introduced in 2019, individual investors can use UPI for applications up to ₹5 lakh. Applications above ₹2 lakh via UPI are categorized as NII.

S45's Real-Time Tracking: S45's platform provides daily bidding reports, book updates, bid quality analysis, and investor classification reviews throughout the subscription window, ensuring transparency and precision.

Step 5: Price Discovery, Allotment, and Listing

After the bidding window closes, the BRLM and issuer analyze the demand curve and set the final cut-off price — the lowest price at which the issue is fully subscribed. All eligible bidders at or above that price receive shares. Shares are allotted, blocked funds are released, and shares list on the exchange within T+3 working days (reduced from T+6 in August 2023 via SEBI Circular SEBI/HO/CFD/TPD1/CIR/P/2023/140).

How the IPO Price Is Determined Through Book Building

Price Band Mechanics

SEBI caps the spread between floor price and cap price at 20% — the cap cannot exceed 120% of the floor. Additionally, a minimum spread of 5% was introduced in December 2021, meaning the cap must be at least 105% of the floor. This prevents artificially narrow bands that negate price discovery.

The issuer and BRLM set this range based on valuation analysis, peer multiples, and pre-IPO investor feedback. The band signals the issuer's acceptable valuation range — not a guaranteed price.

On timing: the price band must be announced at least 2 working days before the issue opens. If revised during the subscription period, the bidding window must be extended by at least 3 additional working days.

Cut-Off Price and Demand Quality

The BRLM aggregates all bids by price point, builds a demand curve, and identifies the lowest price at which cumulative demand equals or exceeds 100% of the issue size. That becomes the cut-off price — the single clearing price at which all successful bidders receive shares, regardless of what they bid above it.

The cut-off alone doesn't tell the full story. BRLMs also analyze weighted average bid data to assess demand quality and distribution. A book where most demand clusters near the floor is a warning signal; strong demand at or near the cap indicates institutional conviction. That distinction shapes how oversubscribed shares get allocated.

Oversubscription and Allotment

When the book is subscribed multiple times over, shares are allotted proportionally within each investor category:

| Category | Allotment Method | Notes |

|---|---|---|

| QIB | Proportional | Allotment on proportionate basis among all QIB applicants |

| NII - Small (₹2L to ₹10L) | Draw of lots (lottery) | Minimum one lot per successful applicant; 1/3 of NII quota |

| NII - Big (above ₹10L) | Draw of lots (lottery) | Minimum one lot per successful applicant; 2/3 of NII quota |

| Retail Individual Investors | Draw of lots (lottery) | Minimum one bid lot per successful applicant |

NII Reform: SEBI shifted from proportional to lottery-based allotment for NIIs in April 2022. This structural change means leveraged mega-bids no longer improve allotment odds, reducing the incentive for artificial demand inflation.

HNI Leverage Curbed: From April 2022, the Reserve Bank of India imposed a cap of ₹1 crore per borrower for IPO financing by NBFCs, down from previously unlimited lending (sometimes exceeding ₹100 crore per individual). The practical effect: NII oversubscription figures in subsequent IPOs dropped sharply, as the economics of leveraged bidding no longer held.

Subscription Multiple vs. Book Quality

A 168x subscription indicates demand volume, but composition matters more. A book built on genuine QIB and long-term institutional interest produces more stable post-listing performance than one inflated by leveraged HNI bidding driven by grey market premium speculation.

Evidence of Weak Correlation:

| IPO | Year | Subscription Multiple | Listing Performance |

|---|---|---|---|

| Paytm | 2021 | 1.89x | -27% (opened ₹1,955, fell to ₹1,564) |

| LIC | 2022 | 2.45x | ~-8.1% (listed at ₹872 vs. ₹949 issue price) |

| Hyundai Motor India | 2024 | 2.37x | -6% (closed at ₹1,882 vs. ₹1,960) |

| CarTrade Tech | 2021 | 20.3x overall (NII 41x) | -7.3% (closed at ₹1,500 vs. ₹1,618) |

S45's Track Record: Across 26 IPOs executed since July 2023, S45 achieved an average listing pop of 43% against an average subscription of 168x — a data point that sits on the opposite end of the spectrum from the examples above.

SEBI Regulations and India-Specific Book Building Rules

Key SEBI Rules

- Mandatory ASBA for all categories

- 20% cap on price band spread (cap ≤ 120% of floor)

- 5% minimum spread (cap ≥ 105% of floor)

- Issue must be fully underwritten

- 3-day extension rule if price band is revised during subscription window

- T+3 working days timeline for listing post-closure (Main Board IPOs)

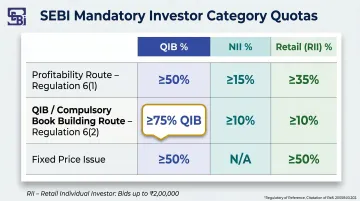

Mandatory Investor Category Quotas

| Eligibility Route | QIB | NII | Retail (RII) |

|---|---|---|---|

| Profitability Route - Regulation 6(1) | ≤50% | ≥15% | ≥35% |

| QIB Route / Compulsory Book Building - Regulation 6(2) | ≥75% | ≤15% | ≤10% |

| Fixed Price Issue | -- | Balance 50% | ≥50% |

RII (Retail Individual Investor): Applies or bids for specified securities up to ₹2,00,000 (₹2 lakh).

Within the QIB quota, SEBI carves out a separate anchor investor framework that operates before the public subscription window opens.

Anchor Investor Framework

SEBI permits anchor allocation of up to 60% of the QIB quota, subject to the following conditions:

- Entity cap: Up to 15 anchor investors for issues ≤₹250 crore; up to 25 for issues above ₹250 crore

- Minimum allotment: ₹5 crore per anchor investor

- Application process: Not open for public application — allocations are at the BRLM's and issuer's discretion

- Lock-in: Anchors are subject to a mandatory lock-in period post-listing

Common Misconceptions About Book Building

Higher Subscription ≠ Better IPO

Oversubscription reflects demand volume but not demand quality. A book dominated by HNI bidding funded by borrowings can result in sharp sell-offs on listing day as leveraged positions unwind. What matters is depth of genuine institutional interest at cut-off or near-cap levels.

Issuers Don't Control Final Price

While the issuer and BRLM set the price band and have discretion in finalizing the cut-off within the band, the cut-off must reflect actual market demand. Artificially setting a price above where demand clears violates the principle of fair price discovery and creates post-listing risk. Disciplined bankers prioritize a defensible price over a headline valuation — stable listing performance follows from getting that call right.

Book Building ≠ Underwriting

Underwriting is the commitment by the investment bank to purchase unsold shares if the issue fails to attract sufficient subscriptions. Book building is the price discovery mechanism. They are distinct functions, though the BRLM often acts in both capacities in Indian IPOs.

Frequently Asked Questions

What are the steps in the book building process?

The five key steps are:

- Appoint the BRLM and file the DRHP

- Conduct the roadshow and complete anchor allocation

- Open the public bidding window for 3 working days

- Determine the cut-off price from the demand curve after closure

- Complete allotment and listing within T+3 working days

How is the price determined in the book building process?

After the subscription window closes, the BRLM aggregates all bids by price point and identifies the lowest price at which cumulative demand equals the full issue size — this is the cut-off price. That price becomes the final issue price for all successful bidders.

Who carries out the book building process in an IPO?

The Book Running Lead Manager (BRLM), a SEBI-registered investment bank, executes the book building process in coordination with the issuer. The BRLM manages everything from price band setting and roadshow through to bid aggregation and allotment.

What is the difference between a fixed price IPO and a book building IPO?

In a fixed-price IPO, the issue price is declared before the subscription window opens and investors apply at that price without input. In a book building IPO, the price emerges from actual investor bids within a declared price band, so the final price reflects real demand.

What is a price band and who decides it in the book building process?

A price band is the floor-to-cap price range within which investors submit bids, set by the issuer and BRLM based on valuation benchmarking. SEBI mandates the cap cannot exceed 20% above the floor price, and the minimum spread is 5%.

What is 100% book building?

100% book building means the entire issue — across all investor categories — is priced and allocated through the book building mechanism, with no portion sold at a pre-determined fixed price. This is the standard approach for most Indian Main Board IPOs under SEBI guidelines.