Introduction

Many Indian founders treat IPO readiness as a paperwork exercise that begins once they decide to list. This misconception is one of the most expensive mistakes in India's public markets. IPO readiness is not a compliance checklist — it's a transformation of the company's financial systems, governance structures, and credibility that begins long before a DRHP reaches SEBI.

That transformation directly determines SEBI scrutiny intensity, institutional demand quality, subscription levels, and listing day performance. For founders, promoters, and management teams considering a Main Board or SME Exchange listing, getting it right is both a regulatory requirement and a commercial imperative — one that shapes everything from your first SEBI observation round to the quality of your QIB anchor book.

Key Takeaways

- IPO readiness means transforming finances, governance, disclosures, and equity story to meet SEBI's requirements and institutional investor expectations

- In India, this covers SEBI eligibility, Ind AS restatement, DRHP drafting, and demand mapping — not compliance checkboxes

- A well-prepared company takes 12–24 months; under-preparation means multiple SEBI observation rounds, delays, or weak post-listing performance

- Readiness gaps appear in predictable places: related party transactions, weak documentation, incomplete governance, and undisciplined pricing

- Companies that start early and treat readiness as an operational transformation consistently achieve better subscription and listing outcomes

What Is the IPO Readiness Process — and Why It Matters for Indian Companies

IPO readiness is the end-to-end process by which a private company transforms its financial statements, governance structures, disclosures, and investor narrative before listing on NSE, BSE, or the SME Exchange. The goal is a company that can withstand SEBI scrutiny, pass institutional due diligence, price its offering with discipline, and sustain post-listing compliance — without operational chaos.

Companies that skip this structured preparation pay for it in lost time, damaged credibility, and poor listing outcomes.

IPO readiness is not the same as meeting SEBI eligibility criteria. Meeting eligibility thresholds — such as the minimum 3-year track record, net tangible assets of at least ₹3 crore in each of the preceding three years, or average operating profit of ₹15 crore under SEBI ICDR Regulations 2018, Regulation 6(1) — qualifies a company to file. Readiness means the company is genuinely investable, not merely eligible.

When companies skip structured readiness, the same pattern plays out:

- Lost documentation surfaces mid-process, forcing rewrites under deadline

- Multiple SEBI observation rounds extend timelines by months

- Pricing misalignment damages promoter credibility at the worst possible moment

According to a joint study by Uniqus and the Indian Venture and Alternate Capital Association (IVCA), SEBI issues an average of approximately 100 observations per DRHP review — nearly half related to risk factor disclosures alone. Each observation round is time SEBI did not need to spend, and time your company cannot afford to lose.

How the IPO Readiness Process Works in India

IPO readiness in India moves through a defined sequence — internal assessment, financial and governance preparation, DRHP drafting and SEBI filing, and roadshow through to listing. The quality of each phase determines the pace and success of the next. For a well-prepared company, the typical timeline runs 12–18 months from readiness initiation to listing. Companies that begin with unresolved financial or governance issues routinely face 24+ months to listing and multiple SEBI observation rounds.

Before SEBI sees the first draft, the following must be in order:

- Audited financials under Ind AS

- Clean documentation of related party transactions

- Board restructuring and governance compliance

- Objects of issue articulation

- Merchant banker (BRLM) selection

- Investor demand mapping

Phase 1: IPO Readiness Assessment

The assessment phase evaluates SEBI eligibility, identifies governance gaps, and flags disclosure risks before DRHP drafting begins. Issues found here cost days to fix; the same issues found by SEBI cost months.

Key eligibility checkpoints include:

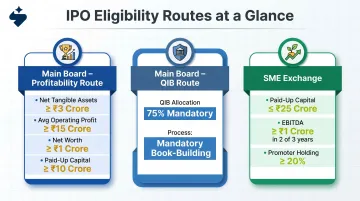

- Main Board profitability route: Net tangible assets of at least ₹3 crore in each of the preceding three years, average operating profit of ₹15 crore, net worth of at least ₹1 crore, and post-issue paid-up capital of at least ₹10 crore

- Main Board QIB route: At least 75% of the net offer allocated to Qualified Institutional Buyers (QIBs), mandatory book-building process

- SME Exchange eligibility: Post-issue paid-up capital not exceeding ₹25 crore, EBITDA of at least ₹1 crore in any 2 of the last 3 years, positive net worth, and promoter holding of at least 20% post-issue

Governance gaps assessed include:

- Board composition and presence of independent directors

- Audit committee readiness and compliance with Companies Act 2013

- Related party transaction disclosure quality

- MCA/RoC filing completeness

AI-led readiness diagnostics, such as the proprietary analytics S45 deploys, surface these gaps earlier than traditional advisor reviews — giving founders weeks to resolve financial and structural issues before they become mid-filing delays.

Phase 2: Financial and Operational Preparation

Financial preparation covers:

- Restating 3 years of audited financial statements under Ind AS

- Ensuring ICAI audit standards are met with valid Peer Review Board certification

- Cleaning up related party transactions and resolving revenue recognition inconsistencies

- Establishing segment reporting where applicable

- Preparing stub period financials under Ind AS 34 if the latest financial year is older than six months from filing date

Governance and operational preparation covers:

- Reconstituting the board to include independent directors and mandated committees (audit, stakeholder, nomination and remuneration) per the Companies Act 2013

- Establishing a quarterly close process to handle post-listing SEBI LODR obligations

- Building the management bandwidth to sustain ongoing regulatory filings without disruption

Phase 3: DRHP Drafting and SEBI Filing

The DRHP (Draft Red Herring Prospectus) is the central disclosure document for Indian IPOs — analogous to the S-1 in the US. It must include audited financials, business overview, risk factors, objects of the issue, management discussion and analysis, and capital structure. Quality of drafting directly determines how many SEBI observation rounds the company will face.

Mandatory DRHP sections include:

- General information (issuer, BRLMs, auditors, legal counsels)

- Risk factors categorised by importance and materiality

- Objects of the issue with specific use of proceeds

- Basis of issue price and dividend policy

- Capital structure and major shareholder disclosures

- Management and governance overview

- Restated financials for 3 years with management discussion and analysis

- Related party transaction disclosures

- Material outstanding litigations and defaults

- Government and regulatory approvals

The SEBI filing sequence works as follows:

- The DRHP is filed with SEBI and the relevant stock exchange simultaneously through a BRLM

- SEBI typically issues observations within 30 days for a complete and well-drafted filing

- The company must address all SEBI observations before proceeding to the RHP (Red Herring Prospectus)

- The observation letter is valid for 1 year, during which the issuer can tap the market by filing an updated DRHP

Incomplete disclosures and vague risk factors generate repeated clarification requests. The Uniqus-IVCA study found that **46% of all SEBI observations relate to risk factor disclosures**, with additional observations focused on compliance, related party transactions, and offer structure.

Phase 4: Roadshow, Bookbuilding, and Listing

Pre-IPO demand mapping and roadshow:

- Institutional investor outreach for QIB anchor allocation

- Non-institutional (NII) and retail investor communication

- Price band finalisation based on demand signal

The price band cap cannot exceed 20% of the floor price. Companies without a clear demand map before the roadshow either under-price (leaving capital on the table) or set an over-ambitious band that collapses subscription.

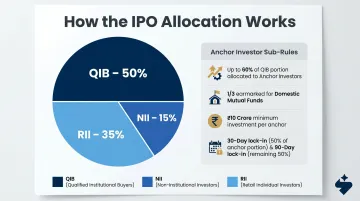

Anchor investor allocation rules:

- Up to 60% of the QIB portion may be allocated to anchor investors

- One-third of the anchor allocation is earmarked for domestic mutual funds

- Minimum investment: ₹10 crore (Main Board); ₹1 crore (SME)

- Lock-in: 50% of shares locked for 30 days; remaining 50% locked for 90 days from allotment date

Standard category allocation (book-built Main Board IPO):

- QIB: 50%

- NII: 15%

- RII: 35%

Listing is not the finish line — it's the start of a new compliance cycle. From the day trading begins on NSE/BSE Main Board or NSE Emerge/BSE SME, the company is subject to SEBI's LODR Regulations, including:

- Regulation 33: Quarterly financial results within 45 days; annual results within 60 days (in XBRL format)

- Regulation 29: Board meeting intimation at least 2 working days in advance (for financial results, dividends)

- Regulation 30: Material event disclosure within 30 minutes of board meeting closure; internal events within 12 hours

Key Factors That Affect IPO Readiness in India

Several readiness drivers determine the success and pace of IPO execution:

Financial Quality and Auditability

Institutional investors scrutinize the books before anything else. SEBI does too.

- Consistent revenue recognition, clean audit opinions, and a 3-year financial track record under Ind AS

- No material restatements — any auditor qualification or material weakness draws SEBI observations and erodes QIB confidence

Governance Structure and Compliance History

Regulators and anchor investors both review the governance track record early in diligence.

- Board composition with independent directors and mandated committees in place

- Clean MCA/RoC filings and a promoter record free of disclosed irregularities

- No pending regulatory or tax disputes that would require prominent risk factor disclosure

Market Timing and Sector Sentiment

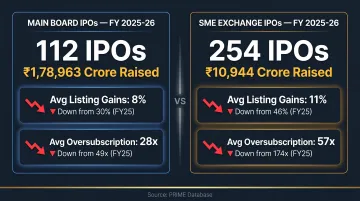

Even a fundamentally strong company can underperform if it lists at the wrong moment. According to PRIME Database, FY 2025-26 saw 112 Main Board IPOs raising ₹1,78,963 crore — an all-time high. Yet average listing gains dropped to 8% from 30% the prior year, and average oversubscription fell from 49x to 28x.

- SEBI's prevailing market window and sector-specific valuation multiples on Indian exchanges

- Performance of comparable listed peers sets the pricing ceiling the market will accept

A company that is financially ready but lists into a cold sector or adverse market window will see lower subscription and listing pop regardless of fundamentals.

Quality of the Equity Story and Banker Selection

Beyond the numbers, QIBs invest in a narrative — one that maps growth to a quantifiable market opportunity.

- A compelling, data-backed equity story is the difference between strong anchor demand and a sluggish book

- The choice of BRLM/merchant banker directly affects institutional placement quality, pricing discipline, and the rigour of the DRHP

Operational Readiness for Post-IPO Life

Listing day is not the finish line. The first year as a public company exposes gaps that pre-IPO preparation should have closed.

- Quarterly close capability, an investor relations function, and Board-level awareness of SEBI LODR obligations

- Companies that treat post-IPO readiness as an afterthought typically miss earnings guidance or delay disclosures in their first year as a listed entity

Common Misconceptions About the IPO Readiness Process

Misconception: Meeting SEBI's minimum eligibility thresholds means a company is IPO-ready

Eligibility is the floor, not the standard. Many companies that technically qualify lack the institutional-grade financial documentation, governance structures, and investor narrative needed to attract QIB anchor participation or price at a premium multiple.

Misconception: DRHP drafting can be delegated entirely to intermediaries

The primary causes of SEBI observation rounds are internal — not legal or secretarial failures:

- Poor data organisation and missing board resolutions

- Undocumented related party rationale

- Internally inconsistent financial notes

Management ownership of the drafting process is what separates one-round filings from multi-round delays.

Misconception: Pricing is determined by the market on listing day

Pricing discipline begins in the demand mapping phase, before the roadshow. Setting a price band without a clear read on institutional appetite leads either to under-subscription at an inflated band or to a suppressed issue price that disappoints promoters and early investors. S45's pre-IPO demand mapping and AI-driven bookbuilding analytics are built to remove this guesswork from India's IPO execution process.

Misconception: SME Exchange listings are a lower-stakes alternative to Main Board IPOs

NSE Emerge and BSE SME have lower eligibility thresholds, but they require a distinct investor base strategy, carry different post-listing liquidity dynamics, and impose the same governance and disclosure obligations after listing.

The market data confirms the risk. PRIME Database reports that while 254 SME IPOs raised ₹10,944 crore in FY 2025-26, average listing gains dropped from 46% to 11% and average oversubscription fell from 174x to 57x. Under-prepared SME IPOs carry the same reputational consequences as poorly executed Main Board listings.

When a Company Is Not Ready for an IPO

Financial signals that indicate a company should delay:

- Material inconsistencies in financial statements across reported periods

- Pending auditor qualifications or material weaknesses

- Unresolved related party transactions that cannot be disclosed cleanly

- Significant dependence on a single customer or promoter-linked contract that creates disclosure risk under SEBI ICDR norms

Governance and structural signals:

- Absence of independent directors and mandated board committees

- MCA filings with significant lapses

- Ongoing regulatory or tax disputes without legal clarity

- Promoter group structures requiring extensive reorganisation before a clean holding structure can be presented in the DRHP

Strategic and market signals:

- IPO driven primarily by promoter or investor liquidity rather than genuine capital requirements — institutional investors and SEBI both recognise the difference

- Use of proceeds that cannot be justified with specific, verifiable business plans in the DRHP

- Timing dictated by market sentiment rather than company readiness

- Absence of a credible growth narrative that withstands QIB scrutiny during bookbuilding

In March 2024, SEBI returned the DRHP of Diffusion Engineers, a reminder that meeting eligibility thresholds is not enough — SEBI can reject filings where the stated objects of the issue don't hold up.

Frequently Asked Questions

What is IPO readiness?

IPO readiness is the process by which a company prepares its financials, governance, disclosures, and equity story to meet SEBI's listing requirements and attract institutional investor confidence. It covers both regulatory compliance and the commercial preparation required for a successful Indian IPO.

What does a company need to be IPO ready?

Four essentials define IPO readiness:

- Three years of Ind AS-compliant audited financials

- A clean governance structure with independent directors and mandated committees

- Documented disclosures covering related party transactions and risk factors

- A well-articulated equity story supported by credible demand mapping

What is the pre-IPO process?

The pre-IPO process covers readiness assessment, financial and governance preparation, DRHP drafting, SEBI filing, and pre-roadshow demand mapping. In India, this phase typically spans 12–18 months for a well-prepared company.

How long does IPO readiness take?

For a well-organised Indian company, the IPO readiness process from initial assessment to SEBI filing typically takes 6–12 months, with the full journey from readiness initiation to listing running 12–18 months. Companies with unresolved financial or governance gaps should budget 18–24 months.

When should a company go for an IPO?

A company is ready for an IPO when it has a demonstrable growth track record, a funded use of proceeds, governance that can withstand public scrutiny, and a market window where sector sentiment supports a premium multiple. All four conditions need to align — missing any one typically delays the process by 6–12 months.