For growth-stage Indian companies preparing for public markets, this matters more than ever. SEBI's BRSR framework has made ESG disclosure mandatory for the top listed entities, and institutional investors — including the QIBs who anchor IPO bookbuilding — are integrating ESG data into their evaluation process.

This article covers what ESG disclosure actually is, why it matters to investors and regulators, what the three pillars require, which frameworks apply in India and globally, and what best practices look like in practice.

Key Takeaways

- ESG disclosure is structured reporting on environmental, social, and governance performance — distinct from CSR narratives or general sustainability claims

- 88% of institutional investors increased their use of ESG information in 2024, per EY's global investor survey

- SEBI's BRSR is mandatory for India's top 1,000 listed companies, with BRSR Core assurance phasing to the top 1,000 by FY2026-27

- MSCI data shows top-quintile ESG performers carry a WACC of ~6.16% vs. 6.47% for the bottom quintile — a measurable cost-of-capital advantage

- For companies preparing for IPO, BRSR readiness belongs in pre-filing governance work — investors and SEBI reviewers will look for it

What is ESG Disclosure?

ESG disclosure is the formal process through which an organisation reports its performance, risks, and initiatives across three non-financial dimensions (Environmental, Social, and Governance) to stakeholders including investors, regulators, and customers.

How ESG Disclosure Differs from CSR and Sustainability Reporting

These terms are often used interchangeably, but they aren't the same:

- CSR reporting tends to be narrative and philanthropic — describing community investment, charitable giving, and social programmes

- Sustainability reporting focuses on ecological stewardship and a company's environmental footprint

- ESG disclosure is a structured, measurable, and increasingly standardised reporting mechanism used specifically by capital markets participants to evaluate risk and long-term value

The distinction matters. ESG disclosure is designed to be comparable across companies and periods, which is why it's driving investment decisions and regulatory requirements in ways that CSR reports never did.

Qualitative vs. Quantitative Disclosures

Complete ESG disclosure combines two types of information:

- Qualitative disclosures — narratives describing strategies, policies, and commitments (for example, a board's approach to climate risk oversight)

- Quantitative disclosures — concrete, comparable metrics such as Scope 1-2-3 emissions, gender pay ratios, and board independence percentages

Neither type alone is sufficient. Qualitative narrative without supporting data reads as aspiration. Metrics without context are hard to interpret.

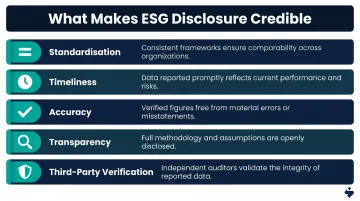

What Makes ESG Disclosure Credible

Credible disclosures share five characteristics:

- Standardisation — consistent methodology that allows comparison across companies and reporting periods

- Timeliness — disclosures published on a predictable cadence, not retrospectively

- Accuracy — data that can be traced back to underlying systems and source documents

- Transparency — clear explanation of what is included, excluded, and why

- Independent third-party verification — external assurance that the reported figures reflect operational reality

Disclosures that lack these qualities risk being dismissed as greenwashing, which carries real regulatory and reputational consequences. Global regulators have taken enforcement action on ESG misstatements: the SEC fined BNY Mellon USD 1.5 million in 2022 and DWS USD 19 million in 2023 for ESG claims not supported by underlying processes.

Why ESG Disclosure Matters

Investor Demand

According to EY's 2024 Global Institutional Investor Survey, 88% of investors increased their use of ESG information in the prior 12 months. PRI signatories — investors who commit to responsible investment principles — now number over 5,000, representing more than USD 121 trillion in assets under management.

For Indian IPO candidates, this translates directly to bookbuilding dynamics. S45's Demand Thesis process includes an explicit ESG Acceptance/Exclusion View that maps how different investor cohorts — domestic mutual funds, FPIs, insurance companies, pension funds — respond to a company's sector and ESG profile. Defence sector companies, for example, remain an exclusion category for some institutional investors based on ESG screens, which affects where demand comes from before a single share is priced.

Regulatory Pressure

ESG disclosure is shifting from voluntary to mandatory across major economies:

- EU CSRD — First cohort reported FY2024 data in 2025. Scope includes large EEA companies and listed entities; non-EU groups with over €150 million in EU turnover are also captured

- SEBI BRSR — Mandatory for India's top 1,000 listed companies, with BRSR Core assurance phasing from the top 150 (FY2023-24) to the top 1,000 (FY2026-27)

- California SB 253 — Companies with over $1 billion in revenue must disclose Scopes 1-3; first Scope 1-2 filings due August 2026

- ISSB/IFRS S1 and S2 — Effective for periods beginning January 2024; jurisdictions representing over half of global GDP have taken steps toward adoption

Voluntary reporting often becomes mandatory over time. Companies that treat ESG disclosure as a compliance minimum are perpetually catching up.

Risk Management and Cost of Capital

MSCI's analysis shows the highest ESG-rated quintile carried a WACC of approximately 6.16% versus 6.47% for the lowest quintile across MSCI World companies from 2015-2019, with larger gaps in cost of equity. That spread compounds significantly over time for capital-intensive businesses.

Beyond financing costs, ESG disclosures help companies surface material non-financial risks before they become financial liabilities:

- Climate exposure and physical asset risk

- Supply chain labour practices and vendor conduct

- Governance gaps that affect board credibility with institutional investors

Competitive and Reputational Advantage

Peer-reviewed research on European IPOs finds that more extensive sustainability disclosure is associated with lower IPO underpricing — better disclosure reduces information asymmetry between issuers and investors, which supports tighter pricing. In India, NSE and BSE ESG thematic indices provide a direct signal; index eligibility increasingly depends on standardised ESG disclosures.

The Three Pillars of ESG

ESG disclosure is built on three distinct but interconnected pillars. Each requires its own data, metrics, and narrative.

Environmental

Environmental disclosure covers:

- GHG emissions — Scope 1 (direct), Scope 2 (purchased energy), and Scope 3 (value chain)

- Energy consumption and renewable sourcing

- Water usage and intensity

- Waste generation and management

- Biodiversity impact

- Physical and transition-related climate risk exposure

Environmental data is typically the most scrutinised pillar, particularly for capital-intensive industries. It's also the area with the biggest data gaps — only 53% of G250 companies disclose Scope 3 emissions, according to KPMG's 2024 Survey of Sustainability Reporting, despite near-universal reporting on Scopes 1 and 2.

Social disclosure, by contrast, is harder to standardise across companies and industries.

Social

Social disclosure covers:

- Workforce diversity, equity, and inclusion metrics

- Employee health and safety performance

- Pay equity across gender and grade

- Human rights due diligence in the supply chain

- Labour practices and worker welfare

- Community engagement and impact

Social metrics vary significantly by industry and business model. A manufacturing company faces different material social risks than a software company. Identifying which social issues are most material to your specific operations is the necessary first step — everything else follows from that determination.

Governance sits underneath both — and when it's weak, it undermines the credibility of everything above it.

Governance

Governance disclosure covers:

- Board composition and independence ratios

- Executive compensation structures and linkage to performance

- Anti-corruption and anti-bribery policies

- Shareholder rights and related-party transaction disclosures

- Internal ethics frameworks and whistleblower mechanisms

Weak governance — undisclosed related-party transactions, inadequate audit committee oversight, ESOP structures not reflected in cap tables — hollows out an ESG disclosure programme even when the environmental and social data is solid.

For growth-stage Indian companies preparing to list, these gaps are among the most common issues that surface during due diligence. S45's AI Risk Radar flags audit committee composition issues, undisclosed contingent liabilities, and ESOP dilution gaps as part of the IPO Readiness Scan, catching them before they become SEBI observations.

Key ESG Disclosure Frameworks and Standards

No single universal framework exists, but several have become de facto global standards:

| Framework | Focus | Key Feature |

|---|---|---|

| GRI | Broad impact, stakeholder-facing | Used by 14,000+ organisations in 100+ countries |

| SASB | Investor-focused, industry-specific | Now maintained by ISSB under IFRS Foundation |

| ISSB/IFRS S1 & S2 | Global baseline for sustainability-related financial disclosures | Effective from January 2024; absorbs TCFD recommendations |

| CSRD/ESRS | EU mandatory regime | Requires double materiality assessment |

| SEBI BRSR | India mandatory framework | Structured around nine NGRBC principles |

TCFD disbanded in October 2023 after ISSB folded its recommendations into IFRS S1 and S2. Many large companies report under multiple frameworks at once — GRI for broad stakeholder audiences, SASB for investor-specific metrics, and mandatory frameworks like BRSR or CSRD for regulatory compliance.

Mandatory vs. Voluntary

Mandatory frameworks like CSRD and BRSR carry legal obligations and penalties for non-compliance. Voluntary frameworks like GRI and SASB allow companies to signal leadership without regulatory compulsion — but voluntary reporting consistently becomes mandatory over time. For companies already building GRI reporting practices before regulation arrived, that early investment made the shift to mandatory frameworks significantly less disruptive.

Single vs. Double Materiality

Materiality is the organising principle behind what gets disclosed:

- Single materiality — how ESG issues affect the business financially (used by ISSB, SASB)

- Double materiality — how ESG issues affect the business AND how the business impacts society and the environment (required by CSRD)

CSRD's double materiality requirement is the more demanding standard — and for Indian companies with EU exposure or global investor bases, it sets the bar that disclosure programmes will increasingly need to meet.

ESG Disclosure in India: SEBI's BRSR Framework

India's primary mandatory ESG disclosure framework is the Business Responsibility and Sustainability Report (BRSR), introduced by SEBI in May 2021 and significantly strengthened by the July 2023 BRSR Core circular.

BRSR Structure and Scope

BRSR is structured around nine NGRBC (National Guidelines on Responsible Business Conduct) principles covering:

- Environmental responsibility

- Stakeholder engagement and governance

- Human rights and labour practices

- Consumer responsibility

- Inclusive growth and community impact

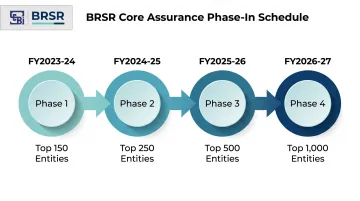

BRSR is mandatory for the top 1,000 listed entities by market capitalisation. BRSR Core — a defined subset of KPIs requiring reasonable assurance — phases in progressively:

| Phase | Entities | Financial Year |

|---|---|---|

| Phase 1 | Top 150 | FY2023-24 |

| Phase 2 | Top 250 | FY2024-25 |

| Phase 3 | Top 500 | FY2025-26 |

| Phase 4 | Top 1,000 | FY2026-27 |

BRSR and IPO Readiness

BRSR readiness starts well before a company files. Institutional investors (including the QIBs who anchor bookbuilding) increasingly use BRSR disclosures to evaluate governance quality and ESG risk exposure during price discovery — meaning weak disclosures can affect valuation before a single retail application comes in.

Pre-listing readiness work typically covers board independence, statutory dues, audit committee composition, and related-party transaction disclosure: the same governance foundations that BRSR Core assurance will scrutinise. Companies that close these gaps across a 12-18 month pre-filing window are materially better positioned than those who treat BRSR as a filing-day exercise.

SEBI is also aligning BRSR more closely with ISSB S1 and S2, so requirements will tighten over successive phases. Companies that build ESG disclosure infrastructure before listing carry a lighter compliance burden after the bell rings.

Best Practices and Common Challenges in ESG Disclosure

Three Practices That Actually Work

1. Adopt a framework and conduct a formal materiality assessment

Choose a framework — GRI, SASB, BRSR, or a combination — that matches your industry and investor base. Then conduct a structured materiality assessment to identify which ESG topics matter most to your business and stakeholders. The trap most companies fall into is reporting on everything superficially rather than disclosing the most material issues with depth and evidence.

2. Build data infrastructure and pursue third-party assurance

Data quality is the backbone of credible ESG disclosure. This means:

- Standardised data collection processes across business units

- Clear ownership of each ESG metric

- Documented data lineage and evidence chains

- Independent third-party assurance, particularly for BRSR Core KPIs

External assurance usage among G250 companies now stands at 75%, per KPMG's 2024 survey. That number signals how far credibility expectations have shifted — assurance is now table stakes for serious issuers.

3. Set SMART targets and track progress annually

ESG disclosure is an iterative process. Define specific, measurable targets, track progress against them in each reporting cycle, and update disclosures to reflect new data and evolving standards. A disclosure that shows directional progress on clearly defined targets is far more credible than aspirational language without milestones.

Three Challenges Companies Consistently Face

Getting the practices right is only half the equation. These are the obstacles that slow most companies down:

- Overlapping framework requirements make comparability difficult across GRI, SASB, and BRSR. Identify a primary framework first, then map to secondary standards — don't try to satisfy all simultaneously

- Scope 3 emissions and supply chain social metrics remain the hardest data to collect reliably. Early investment in data systems, supplier engagement programmes, and estimation methodologies closes this gap over time

- Regulatory timelines across jurisdictions are outpacing most internal compliance functions. Specialist advisory support reduces this risk — especially for companies navigating India's BRSR, the EU's CSRD, and US SEC requirements at the same time

Frequently Asked Questions

What are ESG disclosures?

ESG disclosures are structured reports in which companies communicate their environmental, social, and governance performance, risks, and strategies to investors, regulators, and other stakeholders. Unlike financial statements, they surface non-financial risks and long-term sustainability indicators that balance sheets don't capture.

What does ESG stand for?

ESG stands for Environmental, Social, and Governance: three non-financial dimensions used to evaluate a company's sustainability practices, ethical conduct, and quality of leadership. Investors use ESG data alongside traditional financial metrics to assess risk and long-term value.

What are the 4 types of ESG?

ESG has three core pillars: Environmental, Social, and Governance. Some frameworks and rating agencies add a fourth dimension, often called Economic or Business Conduct, to capture how companies manage their impact on communities, supply chains, and broader society.

Is ESG disclosure mandatory in India?

Yes. SEBI has made BRSR mandatory for the top 1,000 listed companies by market capitalisation. BRSR Core — covering high-assurance KPIs — is being phased in progressively through FY2026-27, making ESG disclosure a legal compliance requirement for a growing universe of Indian companies.

How does ESG disclosure affect a company's IPO prospects?

Strong ESG disclosure signals governance quality and long-term thinking to institutional investors who participate in IPO bookbuilding. Well-structured disclosures attract broader investor interest and support better price discovery. They also mean the company already has the compliance infrastructure BRSR obligations require post-listing.