This article covers what SEBI ICDR is, who must comply, its key provisions, and the material changes introduced in 2025 and 2026 — with the practical implications for companies planning an IPO or rights issue.

Key Takeaways

- SEBI ICDR 2018 replaced the 2009 regulations and governs all public capital issuances in India

- Main Board IPO eligibility requires either a profitability track record or at least 75% QIB subscription

- 2025 amendments require a 3-year promoter lock-in for capex-linked IPOs

- Rights issue timelines and procedures were streamlined under the same 2025 amendment cycle

- Disclosure requirements now cover KMP criminal proceedings and material civil litigations

- SME issuers must now demonstrate EBITDA of at least ₹1 crore in any 2 of the last 3 financial years

What Are the SEBI ICDR Regulations and Why Do They Matter?

The Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018, were notified on September 11, 2018, replacing the earlier 2009 regulations. The consolidated text, last amended on March 21, 2026, is available on SEBI's website.

These regulations determine how Indian companies raise capital from the public — what they must disclose, how pricing gets determined, what obligations promoters carry, and which companies are eligible to list at all.

Three objectives run through every provision:

- Mandatory disclosures give investors enough information to evaluate what they're buying

- Eligibility criteria, lock-in requirements, and allocation frameworks close the gaps that manipulation exploits

- Governance standards push Indian capital markets toward consistent, institutional-grade practices

Without SEBI ICDR, issuers could set arbitrary prices, withhold material information, and exit the moment trading begins. The regulations bind all parties — issuers, promoters, and intermediaries — to obligations that persist well beyond listing day.

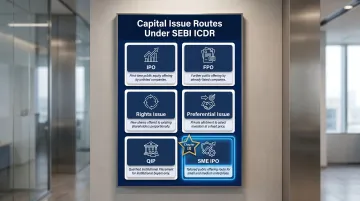

Who Must Comply: Types of Capital Issues Covered

The route a company takes to raise public capital determines which chapter of SEBI ICDR governs its filing — and each chapter carries distinct eligibility thresholds, disclosure obligations, and allocation rules. Six routes are covered:

| Capital Issue Type | Who Typically Uses It |

|---|---|

| Initial Public Offer (IPO) | Companies listing for the first time |

| Follow-on Public Offer (FPO) | Listed companies seeking additional public capital |

| Rights Issue | Listed companies offering shares to existing shareholders |

| Preferential Issue | Targeted allotments to specific investors |

| Qualified Institutional Placement (QIP) | Listed companies raising capital from QIBs |

| SME IPO (Chapter IX) | Companies listing on NSE Emerge or BSE SME |

Each route has its own chapter within ICDR, with different eligibility thresholds, allocation ratios, and disclosure requirements. SME IPOs under Chapter IX carry lower capital thresholds, but the 2025 amendments brought disclosure and governance expectations for SME issuers substantially in line with Main Board standards. Founders using Chapter IX need to plan accordingly.

Key Features of SEBI ICDR Regulations

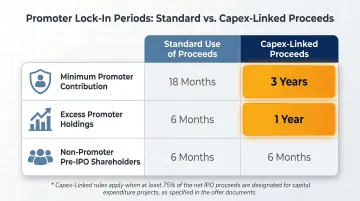

Minimum Promoter Contribution and Lock-in

Under Regulation 14, promoters must hold a minimum of 20% of the post-issue paid-up equity capital. If the promoter falls short, co-promoters may be brought in to complete this requirement.

Regulation 15 excludes certain securities from counting toward this minimum — including shares acquired through revaluation of assets or capitalisation of intangible assets. The 2025 amendment further clarified how ineligibility is calculated after corporate actions like bonus issues or stock splits.

Lock-in structure (post-2025):

| Category | Standard Use of Proceeds | Capex-Linked Proceeds |

|---|---|---|

| Minimum Promoter Contribution | 18 months | 3 years |

| Excess Promoter Holdings | 6 months | 1 year |

| Non-Promoter Pre-IPO Shareholders | 6 months | 6 months |

The capex-linked lock-in applies when the majority of fresh issue proceeds are designated for capital expenditure or repayment of loans taken for capital expenditure purposes.

Disclosure Requirements

The DRHP (Draft Red Herring Prospectus) is the primary disclosure vehicle. Under SEBI ICDR and related SEBI guidelines, it must contain:

- Audited financial statements for the preceding 5 financial years (restated and consolidated)

- Risk factors — both internal and external — with management's stated perception of each

- Promoter background, qualifications, and shareholding details

- Outstanding litigations, defaults, and pending statutory proceedings

- Use of proceeds with project cost breakdown and deployment schedule

- Management Discussion and Analysis (MD&A) covering significant financial changes and known uncertainties

SEBI makes the DRHP available for 21 days of public comment after filing. The consequences of inadequate disclosures are serious — in April 2026, approximately ₹18,000 crore of planned IPO fundraising was disrupted because DRHPs were returned by SEBI due to deficiencies. The companies weren't ineligible; their documents simply failed scrutiny.

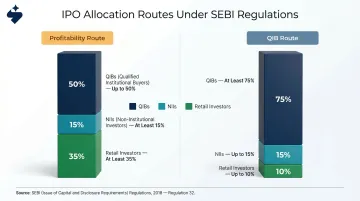

Pricing and Allocation Framework

Disclosure quality determines whether you can file. Pricing mechanics determine what you raise and who owns your company afterward.

Most Main Board IPOs use the book-building method: the issuer sets a price band (the cap cannot exceed 120% of the floor), investors bid within that range, and the final price is determined by demand. Retail investors may bid at the cut-off price without specifying a number.

Mandatory allocation ratios under Regulation 32:

| Investor Category | Profitability Route | QIB Route |

|---|---|---|

| QIBs | Up to 50% | At least 75% |

| Non-Institutional Investors | At least 15% | Up to 15% |

| Retail Individual Investors | At least 35% | Up to 10% |

The route an issuer takes has direct pricing consequences. A QIB route issue, with 75% allocated to institutional investors, attracts a different demand profile — and often a different price discovery outcome — than a profitability route issue. Tracking live subscription across QIB sub-categories (domestic mutual funds, FPIs, insurance companies, pension funds), NII, and retail gives issuers and their bankers real-time visibility into where demand is building and where it isn't.

IPO Eligibility Criteria Under SEBI ICDR

The Two Main Board Routes

Regulation 6(1) — Profitability Route:

| Criterion | Threshold |

|---|---|

| Net tangible assets | At least ₹3 crore in each of the preceding 3 years |

| Average operating profit | At least ₹15 crore across 3 of the preceding 5 years |

| Net worth | At least ₹1 crore in each of the preceding 3 years |

| Monetary asset cap | Not more than 50% of net tangible assets in monetary form |

Net worth is calculated as paid-up equity share capital plus free reserves and surplus, minus accumulated losses and deferred expenditure not yet written off. Confirm the precise definition with your legal counsel before filing — the calculation directly affects eligibility.

Regulation 6(2) — QIB Route:

Companies that don't meet the profitability criteria can still list, provided at least 75% of the net offer is allotted to QIBs. If this threshold isn't achieved, the issuer must refund all subscription amounts in full.

Pre-IPO Placements and Anchor Investors

Regulations 8 and 8A govern pre-IPO placements and anchor investor allocations. Anchor investors — a sub-category of QIBs receiving preferential allocation — now receive up to 40% of the QIB portion (increased from 33% via a late 2025 amendment). Their shares carry a staggered lock-in:

- 50% locked for 30 days from allotment

- 50% locked for 90 days from allotment

SME Eligibility Under Regulation 229

SME issuers qualify for the SME platform when post-issue paid-up capital does not exceed ₹10 crore. Companies with capital between ₹10 crore and ₹25 crore may still list on SME platforms under additional conditions. Post-2025, SME issuers must also demonstrate EBITDA of at least ₹1 crore in any 2 of the last 3 financial years.

Before approaching the market, it helps to know exactly where you stand against these criteria. S45's IPO Readiness Scan evaluates financial track record, free float, board independence, demat readiness, statutory dues, and material litigation. It produces a pass/fail assessment against SEBI ICDR thresholds in 30 minutes.

SEBI ICDR Amendments: What Changed in 2025 and 2026

Two rounds of amendments have reshaped ICDR's operational framework over the past year. The March 2025 amendment (Gazette: March 8, 2025; rights issue provisions effective April 4, 2025) addressed lock-in periods, rights issue procedures, and disclosure requirements. The 2026 amendment, notified March 16 and effective March 21, tightened lock-in rules and abridged prospectus standards.

Changes to Promoter Lock-in Periods

The most structurally significant change links lock-in duration to how proceeds are used. When the majority of fresh issue proceeds fund capex or related debt repayment, MPC lock-in extends to 3 years. For other uses of proceeds, the 18-month lock-in remains unchanged.

This creates a genuine strategic decision for issuers: classify proceeds differently to secure a shorter lock-in, but doing so constrains operational flexibility and signals lower long-term commitment to institutional investors.

Rights Issue Simplification

The 2025 amendment removed the ₹50 crore threshold — all rights issues by listed companies now fall under the ICDR framework. Key changes:

- Merchant banker appointment is no longer mandatory for qualifying issues

- Issuers file directly with stock exchanges rather than SEBI

- The entire rights issue process must be completed within 23 working days from board approval

- New Regulation 77B allows promoters to renounce entitlements in favour of specific named investors

Enhanced Disclosures and Transaction Reporting

From the date of DRHP filing through issue closure, all promoter and promoter group securities transactions must be reported to stock exchanges within 24 hours. Pre-IPO placements disclosed in draft documents must also be reported within 24 hours of execution.

The scope of mandatory disclosures now includes:

- All agreements that directly or indirectly affect management or control of the issuer

- Criminal proceedings and regulatory actions against KMPs and Senior Management Personnel

- Material civil litigations exceeding the lower of 2% of turnover, 2% of net worth, or 5% of average absolute profit/loss after tax over the preceding 3 years

2026 Amendment: Lock-in Tightening and Abridged Prospectus Rules

The 2026 amendment addresses lock-in rules and abridged prospectus standards, responding directly to India's IPO market scale: 220 IPOs raised approximately ₹1.78 lakh crore in calendar 2025, with NSE crossing 12 crore registered investors. At that volume, disclosure quality and post-issue accountability demanded tighter structural guardrails.

For issuers managing the observation cycle that follows DRHP filing, S45's SEBI Query Board tracks observations across Financials, Governance, and Business categories, assigning specific owners (CFO for financials, Legal Counsel for governance, Lead Banker for business), due dates, and evidence closure requirements for each item.

What the New Rules Mean for SME IPOs

The SME framework under Chapter IX preserves lower capital thresholds but has moved decisively toward Main Board-level accountability. The 2025 changes that most directly affect SME issuers:

- Requires ₹1 crore operating profit in any 2 of the last 3 financial years as a hard eligibility gate (new EBITDA test)

- Extends 24-hour transaction reporting to SME IPOs, covering the full window from DRHP filing through closure

- Applies KMP criminal proceedings and material civil litigation disclosure thresholds to SME issuers, not just Main Board companies

The mandatory market-making requirement post-listing remains a distinguishing feature of the SME framework. Market makers must maintain quote obligations on spread and depth per exchange rules, providing liquidity for retail investors that the broader market doesn't automatically supply.

For SME founders, stricter disclosure norms make clean books a filing prerequisite, not a post-mandate cleanup. In practice, S45's AI Risk Radar routinely surfaces ESOP dilution not reflected in cap tables, audit committee composition gaps, undisclosed contingent liabilities, and inconsistent revenue recognition during SME readiness assessments. Catching these early is what makes the 30–45 day DRHP drafting timeline achievable.

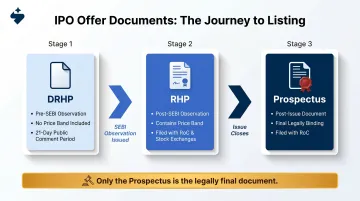

DRHP vs. RHP: Understanding the Offer Document Process

Three distinct documents exist in the IPO process, and they are not interchangeable:

| Document | Stage | Key Characteristics |

|---|---|---|

| DRHP | Pre-SEBI observation | Filed with SEBI; no price band; 21-day public comment period |

| RHP | Post-SEBI observation | Contains price band; filed with RoC and exchanges before subscription |

| Prospectus | Post-issue | Final legal document filed with RoC after issue closure |

One point the table above makes clear: neither the DRHP nor the RHP is the final document. The Prospectus filed with the Registrar of Companies after issue closure is the legally binding offer document.

For practical reference, key procedural requirements under the 2025 amendments include:

- RHP filing date is publicly accessible via the SEBI EFTS portal, BSE and NSE websites, and the registrar's website

- A single combined advertisement must be published at least 2 working days before the issue opens

- The public announcement after DRHP filing must be made within 2 working days of that filing

Frequently Asked Questions

What are SEBI ICDR Regulations?

SEBI ICDR (Issue of Capital and Disclosure Requirements) Regulations, 2018 are the primary rules governing how Indian companies raise capital from the public through IPOs, rights issues, FPOs, and other instruments. They mandate transparency standards, pricing safeguards, and investor protection measures across all public capital issuances.

What are the SEBI ICDR Amendment Regulations 2026?

The 2026 amendment, effective March 21, 2026, primarily modifies lock-in and abridged prospectus rules, responding to the scale of India's IPO market where 220 IPOs raised ₹1.78 lakh crore in 2025. It further strengthened eligibility norms and moved disclosure formats closer to global benchmarking standards.

What do Regulations 6, 8, 8A, 229, and 25(2A) cover?

Each regulation governs a distinct aspect of the IPO process:

- Regulation 6: Main Board IPO eligibility — profitability and QIB routes

- Regulations 8 & 8A: Pre-IPO and anchor investor placements, pricing and disclosure

- Regulation 229: SME IPO eligibility based on post-issue paid-up capital thresholds

- Regulation 25(2A): Promoter contribution rules for companies formed through conversion

How is net worth calculated under SEBI ICDR Regulations 2018?

Net worth is calculated as paid-up equity share capital plus free reserves and surplus, minus accumulated losses and deferred expenditure not yet written off. This definition applies directly to Regulation 6 eligibility assessments — cross-check against the latest consolidated SEBI ICDR gazette text before filing.

What are the new rules for SME IPOs?

The 2025 amendments introduced a minimum EBITDA test of ₹1 crore in any 2 of the last 3 financial years. Enhanced disclosure standards and 24-hour transaction reporting obligations now apply to SME IPOs. Mandatory market-making post-listing continues as a distinguishing requirement of the SME framework.

Is the RHP or DRHP the final document?

Neither. The DRHP is the preliminary filing subject to SEBI observations and public comment. The RHP includes the price band and governs the subscription period. The Prospectus filed with the Registrar of Companies after the issue closes is the legally final offer document.