Introduction

Incomplete disclosures are one of the most consistent reasons SEBI delays or rejects IPO filings in India. Yet promoters and founders routinely underestimate what they're signing up for — the disclosure obligations begin long before listing day and extend well beyond it.

The framework is comprehensive by design. SEBI, stock exchanges, and the investing public each have specific information rights, and the regulator enforces them rigorously.

This article covers the full disclosure framework: regulatory architecture, the DRHP as the central filing document, mandatory disclosure categories, financial reporting standards, Main Board versus SME differences, and post-listing obligations.

Key Takeaways

- SEBI's ICDR Regulations 2018 govern all IPO disclosure rules for Main Board and SME listings in India

- The DRHP must cover three years of restated financials, risk factors, promoter details, and use of proceeds

- Restated financials require Ind AS (or IGAAP) and a SEBI-registered auditor with valid ICAI peer review

- Non-compliance leads to SEBI withholding its observation letter — delaying or effectively blocking the listing

- After listing, LODR Regulations require timely disclosure of material events, quarterly results, and shareholding pattern updates

The Regulatory Framework Governing IPO Disclosures in India

IPO disclosures in India operate under the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018 (SEBI ICDR 2018), last amended May 17, 2024. These regulations replaced the 2009 ICDR framework and apply to both Main Board and SME IPOs, with calibrated differences for each segment.

SEBI's Role: Observations, Not Approvals

SEBI reviews every DRHP and issues an observation letter under Regulation 25 of ICDR 2018. SEBI does not approve an IPO — Regulation 25(10) clarifies that the observation letter does not constitute endorsement of the offer document's correctness or completeness. SEBI's mandate is disclosure review and investor protection, not validation of the issuer's business merits. The company, its directors, promoters, and lead manager bear primary liability for accuracy.

Stock Exchanges: Parallel Review

For Main Board IPOs, the DRHP is filed simultaneously with SEBI and the stock exchanges (NSE or BSE). Both entities conduct parallel reviews, with the exchange issuing in-principle listing approval. For SME IPOs on NSE Emerge or BSE SME, only stock exchange approval is required — SEBI review is not mandatory, which significantly shortens the approval timeline for smaller issuers.

The Companies Act 2013: Liability Framework

The Companies Act 2013 provides the legal backbone for prospectus liability. Two sections define exposure for misstatements:

- Section 34 (Criminal): Every person who authorizes the issue is liable under Section 447 — penalties include imprisonment of six months to 10 years and fines up to three times the fraud amount.

- Section 35 (Civil): The company, directors, named proposed directors, promoters, and experts must compensate investors who sustain losses from prospectus misstatements. Where intent to defraud is proven, liability under Section 35(3) is personal and unlimited.

That liability framework set the floor. SEBI has since raised the ceiling on what must be disclosed.

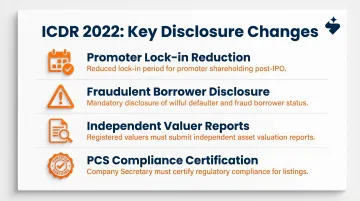

Recent Tightening: The ICDR Amendment of 2022

SEBI has steadily tightened disclosure norms. The ICDR (Amendment) Regulations, 2022, notified January 15, 2022, introduced several important changes:

- Reduced promoter lock-in from three years to 18 months for minimum contribution, and from one year to six months for excess holding

- Required explicit disclosure of "fraudulent borrowers" in addition to wilful defaulters

- Mandated independent valuer reports for allotments causing control changes or exceeding 5% to a single allottee

- Shifted compliance certification responsibility from statutory auditors to Practicing Company Secretaries

For companies preparing a DRHP today, these changes mean promoter history, control structures, and third-party valuations receive sharper regulatory scrutiny than they did under the 2009 framework — gaps that surface late in drafting are significantly harder to remedy.

The Draft Red Herring Prospectus (DRHP): Your Primary Disclosure Document

The DRHP is the detailed offer document filed with SEBI before an IPO. It contains all material information about the company except final pricing and issue size, which are disclosed later in the Red Herring Prospectus (RHP) and final Prospectus. The sequence is deliberate: DRHP for review and public comment, then the RHP with price band, and finally the Prospectus with final pricing post-close.

Mandated Structure

Schedule VI Part A of SEBI ICDR 2018 prescribes both the format and minimum content of the DRHP. Every DRHP must include:

- Cover page and risk factors: Company-specific risks cross-referenced throughout the document

- Business section: History, products, competitive positioning, customers, suppliers, capacity, order book

- Industry overview: Market size, growth drivers, regulatory environment

- Management Discussion and Analysis (MD&A): Performance commentary and outlook

- Financial statements: Restated financials with auditor's examination report

- Capital structure: Pre- and post-issue shareholding, promoter lock-in

- Objects of the issue: Quantified use of proceeds with supporting appraisals

- Key regulatory disclosures: Litigation, related party transactions, KMP remuneration

SEBI Review: The 30-Day Observation Timeline

Under Regulation 25(9), SEBI issues its observation letter within 30 days from the later of receiving a satisfactory reply to its queries or the exchange's in-principle approval. In practice, SEBI frequently raises clarifications. The issuer must respond point-by-point through the Book Running Lead Manager (BRLM), and multiple rounds of correspondence before observations are cleared is the norm rather than the exception.

Key implication: Each clarification round resets the clock, so the quality of initial disclosures directly affects total filing-to-observation time.

Public Availability Requirement

Once SEBI issues its observation letter, the DRHP must be made available to the public on the websites of the company, BRLM, SEBI, and the stock exchanges, at least 21 days before the issue opens (Regulation 25(4)). This mandatory window exposes disclosures to scrutiny from investors, media, and competitors before pricing and launch.

Preparing a Clean DRHP

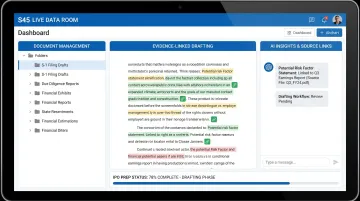

Preparing a DRHP that minimises SEBI queries requires every disclosure to be tied to a verifiable source document before drafting begins. S45's AI-enabled live data room uses evidence-linked drafting, where each claim in the document traces back to a source file in the data room, allowing the team to produce a DRHP-ready draft in 30 to 45 days while reducing observation queries driven by unsupported claims.

Key Categories of Mandatory IPO Disclosures Under SEBI

Promoter and Promoter Group Disclosures

SEBI mandates detailed disclosure on all promoters and promoter group entities:

- Identity (name, PAN, DIN)

- Educational qualifications and business background

- Other directorships and business interests

- Shareholding pattern before and after the issue

- Pledging or encumbrance on shares

Lock-in requirements (post-2022 amendment):

- Minimum promoter contribution of 20% of post-issue capital: locked in for 18 months

- Excess promoter holding above 20%: locked in for six months

- Non-promoter pre-IPO shareholders: six months lock-in

These lock-in schedules must be explicitly disclosed in the DRHP. Any deviation triggers SEBI observations and can stall the listing process.

Objects of the Issue and Use of Proceeds

SEBI requires specific, quantified disclosure of how IPO proceeds will be deployed. Under Regulations 7(2) and 141(2), general corporate purposes cannot exceed 25% of gross proceeds. Every other object must be supported by:

- Appraisal reports or certified cost estimates

- Clear rationale for the amount allocated

- Timeline for deployment

Vague or insufficiently justified use of proceeds is a leading cause of SEBI queries. Post-listing, companies must disclose actual deployment against stated objects in every quarterly and annual report. The same scrutiny that applies to proceeds extends to how companies characterize the risks surrounding their business.

Risk Factors and Business Disclosures

Risk factors must be company-specific and material — boilerplate language is flagged in SEBI observation letters. SEBI expects issuers to disclose:

- Internal risks: dependence on key customers or suppliers, pending litigation, regulatory dependencies

- Industry and macro risks: competition, cyclicality, policy changes

- Each risk factor cross-referenced to relevant sections in the document

Each risk factor — even sector-wide ones — must be tied explicitly to the issuer's business model, geography, or offering structure.

Business disclosures must cover:

- Company history and incorporation details

- Products, services, and production processes

- Competitive positioning and market share

- Key customers and suppliers (without compromising confidentiality where justified)

- Capacity utilisation and order book status

- Operational metrics relevant to the sector

Financial Disclosure Requirements for Indian IPOs

Restated Financial Statements: Quantity and Standards

Main Board IPOs require three years of audited restated financial statements. SME IPOs require two years. Financials must be prepared under Indian Accounting Standards (Ind AS) or IGAAP (for eligible companies) and audited by a statutory auditor holding a valid Peer Review certificate from the ICAI Peer Review Board.

Restated financial statements differ from standard audited accounts. They incorporate four specific adjustments:

- Accounting policy changes — earlier years recomputed as if the uniform policy had always applied

- Prior period errors — adjusted retrospectively in the year the error occurred

- Audit qualifications — items subject to qualified, adverse, or disclaimer opinions are restated

- Accounting estimate changes — recognised prospectively unless they affect carrying amounts

The restated financials must be accompanied by an Independent Auditor's Examination Report on the Restated Financial Information, confirming compliance with SEBI ICDR requirements. This report is a mandatory attachment — without it, SEBI will not process the filing.

Stub Period Financials

If the filing date falls more than six months after the last audited year-end, the issuer must include limited review financial statements for the intervening period. This stub period requirement applies to both Main Board and SME issuers.

The practical implication: issuers filing in October with a March 31 year-end must furnish reviewed financials through at least September 30. Planning the filing calendar around this threshold — rather than scrambling to compile stub period data at the last minute — is one of the cleaner ways to keep a DRHP timeline on track.

Main Board vs SME IPO: How Disclosure Requirements Differ

Main Board IPOs are governed by Chapters II–IV of SEBI ICDR 2018 and require full prospectus-level disclosure. SME IPOs follow Chapter IX, which offers a lighter-touch framework designed for smaller issuers.

Key Differences

| Category | Main Board | SME (NSE Emerge / BSE SME) |

|---|---|---|

| Restated financials | 3 years | 2 years |

| Regulatory review | SEBI + Exchange | Exchange only (no SEBI) |

| Quarterly results | Mandatory | Not required (semi-annual only) |

| Corporate governance (LODR Reg 17-27) | Fully applicable | Exempt |

| Minimum shareholders | 1,000 | 50–200 |

| Underwriting | Not mandatory | 100% mandatory (15% by merchant banker) |

| Market making | N/A | Mandatory for 3 years |

These relaxations are structural, not substantive. Qualitative disclosures on promoters, risk factors, objects of the issue, and related party transactions carry the same rigour for SME IPOs as they do on the Main Board.

Migration to Main Board

Once an SME-listed company's post-issue paid-up capital exceeds ₹25 crore due to a further capital raise, it must migrate to Main Board (Regulation 280 of SEBI ICDR). Migration requires:

- Passing a special resolution by postal ballot

- Securing approval from the Main Board exchange

- Meeting Main Board eligibility criteria

From that point, the company is subject to full quarterly reporting and the corporate governance requirements under LODR Regulations 17–27 — the same obligations that apply to any other Main Board-listed issuer.

Post-Listing Disclosure Obligations Every Issuer Must Know

Post-listing, companies become subject to SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (LODR), last amended January 22, 2026. LODR governs continuous and periodic disclosures across four main categories.

Quarterly Financial Results (Regulation 33)

Listed companies must file:

- Quarterly results (Q1, Q2, Q3) within 45 days of quarter-end

- Annual results (Q4) within 60 days if audited

SME-listed companies are exempt from quarterly filings and file semi-annual results instead.

Shareholding Pattern and Corporate Governance

- Shareholding pattern (Regulation 31): Within 21 days of quarter-end

- Corporate governance report (Regulation 27): Within 15 days of quarter-end

- Annual report (Regulation 34): Filed at commencement of AGM notice dispatch (at least 21 clear days before AGM)

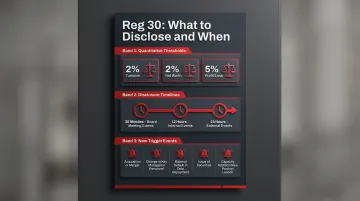

Material Event Disclosure (Regulation 30)

Regulation 30 requires companies to disclose price-sensitive information to stock exchanges promptly and before disclosing it elsewhere. The LODR (Second Amendment) Regulations, 2023 (notified June 14, 2023) significantly expanded Regulation 30:

- Quantitative thresholds introduced: 2% of turnover, 2% of net worth, or 5% of average absolute profit/loss after tax (last three audited years)

- Strict timelines: 30 minutes from board meeting closure; 12 hours for internal events; 24 hours for external events

- New events added: shareholder settlement agreements impacting control; KMP/senior management resignations with detailed reasons; cybersecurity incidents; regulatory searches or seizures; voluntary revision of financials

For the top 100 listed entities (effective October 1, 2023) and top 250 entities (effective April 1, 2024), SEBI introduced a rumour verification framework: companies must confirm, deny, or clarify market rumours within 24 hours.

Post-Listing Transition Support

Many newly listed companies miss their first LODR deadlines — not because the rules are unclear, but because compliance calendars, filing workflows, and board reporting cadences weren't built before listing day. S45's post-IPO investor relations support helps management put those systems in place before the first quarterly filing is due, reducing the risk of exchange notices or SEBI queries in the months immediately after listing.

Frequently Asked Questions

What legal disclosures are required when a company has an IPO?

Indian IPO issuers must disclose business operations, restated financials, promoter details and shareholding, risk factors, objects of the issue, litigation history, related party transactions, and management remuneration in the DRHP, as governed by SEBI ICDR Regulations 2018 and the Companies Act 2013.

What is the SEBI requirement for company disclosure?

SEBI requires all IPO-bound companies to file a DRHP with prescribed disclosures, then reviews it and issues observations that must be addressed before the IPO can proceed. Post-listing, companies must meet ongoing disclosure obligations under LODR.

What is a DRHP and what information does it contain?

A Draft Red Herring Prospectus is the primary offer document filed with SEBI before an IPO. It contains the company's business overview, audited restated financials, risk factors, promoter disclosures, objects of the issue, and capital structure — everything except final pricing, which is added in the Red Herring Prospectus.

What are the differences in disclosure requirements between Main Board and SME IPOs in India?

SME IPOs require only two years of restated financials versus three for Main Board, have a shorter approval process (exchange only, no SEBI review), and are exempt from quarterly financial filings and certain corporate governance provisions until they migrate to Main Board. However, qualitative disclosures on promoters, risks, and fund use are equally rigorous.

What are the consequences of making false or incomplete disclosures in an Indian IPO?

False or misleading statements in a prospectus attract civil liability under Section 35 of the Companies Act 2013 and criminal prosecution under Section 34, with imprisonment of six months to 10 years and fines up to three times the fraud amount. SEBI can also enforce disgorgement of gains and debarment, with liability extending to directors, promoters, and the lead manager who verified the disclosures.