But here's the thing: the DRHP is not just a compliance exercise. How you prepare it determines how SEBI and institutional investors perceive your company before the IPO even opens. A clean, well-evidenced document moves faster through SEBI review. A vague, inconsistent one attracts observations that can delay your listing by months.

This guide covers everything issuers need to understand — the anatomy of NSE offer documents, the DRHP-to-RHP journey, how filing differs between NSE Main Board and NSE Emerge, and the pitfalls that most commonly derail IPO timelines.

Key Takeaways

- A DRHP is the preliminary offer document filed with SEBI/NSE — complete business, financial, and risk disclosures, but no final price or dates

- The RHP adds the price band, issue schedule, and allotment details; it's what investors actually subscribe against

- NSE Main Board filings go through SEBI review; NSE Emerge filings skip SEBI observations — the exchange reviews the document directly

- SEBI's observation letter is valid for 12 months under Regulation 44; miss that window and the process restarts

- Post-subscription listing timelines now follow SEBI's T+3 circular (August 2023), replacing the older T+6 norm

What Are NSE Corporate Filings and Offer Documents?

Most founders encounter two distinct categories of NSE filings — and mixing them up leads to wasted preparation time before the IPO process even starts.

Routine corporate filings are ongoing disclosure obligations for already-listed companies under SEBI LODR Regulations. These include quarterly financial results (Regulation 33), shareholding patterns (Regulation 31), and material event disclosures (Regulation 30). Every listed company files these continuously post-listing.

Offer documents are a separate category, created specifically for capital-raising events like an IPO.

The DRHP Defined

A Draft Red Herring Prospectus is the preliminary offer document submitted before a company launches its IPO. It discloses the business model, financials, management, risk factors, and IPO structure. Critically, it does not state the final issue price or listing date.

SEBI ICDR Regulations 2018, Regulation 245 sets the disclosure standard for all offer documents:

"All material disclosures which are true and adequate so as to enable the applicants to take an informed investment decision."

This standard applies to both Main Board and SME filings — which means the drafting burden is the same regardless of which exchange you list on.

The Main Board vs. Emerge Filing Distinction

This is where the two paths diverge sharply:

- NSE Main Board: The DRHP is filed with SEBI through a Book Running Lead Manager (BRLM). SEBI reviews it and may issue observations within 30 days under Regulation 25.

- NSE Emerge (SME): The draft offer document is filed directly with the exchange. Per Regulation 246(2): "The Board shall not issue any observation on the offer document." The exchange reviews; SEBI does not.

This distinction shapes your entire preparation strategy. For SME issuers, the absence of SEBI review means your lead manager's diligence is the primary quality gate — making the choice of banker more consequential, not less.

The Anatomy of a DRHP: Key Sections Every Issuer Must Understand

SEBI's Schedule VI prescribes the exact structure of a DRHP. Understanding what each section must contain — and where issuers most commonly fail — is essential before drafting begins.

Cover Page and Offer Structure

The front cover is fixed-format and non-negotiable. It must include:

- Issuer name, CIN, and registered office address

- Type of document (Draft Red Herring Prospectus) and date

- Offer type: fresh issue, offer for sale (OFS), or both

- Promoter names and lead manager details

- Risk clauses displayed in prescribed box format

Any inaccuracy here flags the entire document for closer scrutiny.

Business Overview and Financial Information

The business section is where the company tells its story — revenue model, market position, competitive advantages, and growth history. Vague or internally inconsistent narratives here generate more SEBI observations than almost any other section — and create lasting investor skepticism.

The financial information section requires restated audited financials for at least three preceding full financial years of 12 months each, prepared under Ind AS or Indian GAAP per Schedule VI, Item 11. Key ratios — ROE, EBITDA margins, debt-to-equity — must accompany the statements. If the most recent full-year data is older than six months from the issue opening date, a stub period must be included.

Start the restatement exercise at least 12 months before your planned DRHP filing.

Risk Factors and Objects of the Issue

Risk factors must be specific, material, and company-relevant. Generic boilerplate — "we operate in a competitive industry" — does not satisfy the adequacy standard and regularly triggers SEBI queries. Under-disclosed risks carry post-listing legal liability — which means the following categories demand honest, specific treatment:

- Regulatory and licensing risks

- Litigation exposure (pending and contingent)

- Customer concentration beyond 10-15% of revenue

- Key-person dependencies at the promoter or senior management level

The Objects of the Issue section (use of IPO proceeds) is under similar scrutiny. Regulation 7 imposes two hard rules:

- The amount allocated to "general corporate purposes" cannot exceed 25% of total proceeds

- The issuer must have firm finance arrangements for at least 75% of stated means of finance for specific projects

Utilization plans without project-level specificity — "general business expansion" being the most common offender — reliably extend your timeline and invite regulator pushback on the entire proceeds structure.

DRHP vs RHP: Understanding the Difference and the Filing Timeline

The Core Distinction

| Document | Contents | Filed With |

|---|---|---|

| DRHP | All disclosures except price and dates | SEBI (Main Board) or Exchange (SME) |

| RHP | All DRHP content + price band, issue schedule, allotment details | Registrar of Companies |

The RHP is filed after SEBI clearance, incorporating all observation responses plus final pricing. It is the document against which investors actually bid during the subscription period.

Main Board Timeline

The full journey from DRHP filing to listing typically runs 8 months to 12 months for NSE Main Board IPOs:

- DRHP filed with SEBI through the BRLM

- 21-day public comment window (Regulation 26) — DRHP hosted on SEBI's website, stock exchange platforms, and lead manager's website; public announcement in English, Hindi, and regional language newspapers within two days of filing

- SEBI issues observations within 30 days of receipt (or satisfactory clarification responses) per Regulation 25

- Company addresses observations and updates disclosures

- RHP filed with Registrar of Companies

- IPO opens at least 3 working days after RHP filing

- Listing occurs within T+3 working days after subscription closes, per SEBI's August 2023 circular

The 12-Month Validity Clock

Regulation 44 limits the validity of a SEBI observation letter to 12 months from the date of issuance. If the IPO does not open within that window, the issuer must re-file a fresh DRHP with updated financials — incurring additional fees per Schedule III and restarting the timeline. In practice, issuers who miss this window lose their original valuation anchor and often face a changed market environment — meaning pricing discipline from Day 1 of filing matters more than most founders expect.

SME filings follow a different process. The 21-day public comment mechanism under Regulation 26 does not apply to SME IPOs. Regulation 247 requires hosting the offer document on relevant websites, but does not prescribe a structured public comment period — shortening the pre-filing runway but removing one layer of public scrutiny from the timeline.

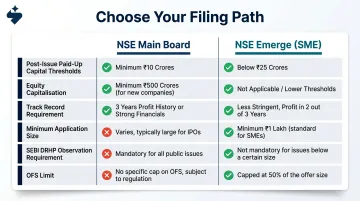

NSE Main Board vs NSE Emerge: Two Different Filing Paths

Eligibility at a Glance

| Criterion | NSE Main Board | NSE Emerge (SME) |

|---|---|---|

| Post-issue paid-up capital | Minimum ₹10 crore | Maximum ₹25 crore |

| Equity capitalisation | Minimum ₹25 crore | Not separately specified |

| Track record | 3 years (issuer or promoters) | 3 years |

| Minimum application size | Standard retail | ₹1,00,000 per application (Reg 267(2)) |

| SEBI DRHP observation | Required (Reg 25) | Not issued (Reg 246(2)) |

| OFS limit | Standard rules | Capped at 20% of total issue size |

The paid-up capital thresholds define which path is available. Companies with post-issue capital between ₹10 crore and ₹25 crore could technically qualify for either path — the operational and regulatory differences should drive the decision, not just the numbers.

The SME Filing Path in Practice

Since SEBI does not review SME DRHPs, the lead manager's due diligence certificate (Forms A and G of Schedule V) carries significant weight. The exchange conducts the primary review. This does not mean SME filings face lower standards — it means the lead manager bears heightened fiduciary responsibility, and the offer document must be complete and accurate before it reaches the exchange.

That accountability comes with a compressed timeline: 2–3 months from signed mandate to listing, compared to 6–12 months for Main Board.

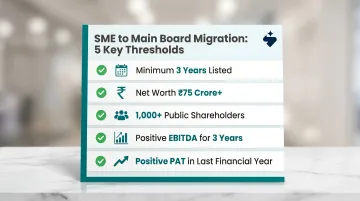

The Migration Pathway

SME-listed companies can migrate to the Main Board once they meet defined thresholds:

- Minimum 3 years of listing on the SME exchange

- Net worth of at least ₹75 crore

- At least 1,000 public shareholders in the preceding quarter

- Positive EBITDA for 3 preceding financial years

- Positive PAT in the immediately preceding financial year

Founders choosing the SME route should plan for this migration from day one. Capital structure, governance investments, and financial targets — particularly net worth trajectory and EBITDA consistency — should be set with Main Board thresholds in view.

Common Pitfalls in DRHP Preparation That Delay IPOs

The most common documentation failures that trigger SEBI observations follow a recognisable pattern:

- Vague use-of-proceeds disclosures — failing Regulation 7's specificity requirements

- Inconsistent financial restatements — figures in the business narrative that don't match the restated financials

- Incomplete risk factors — especially regulatory exposure and pending litigation

- Promoter background gaps — incomplete disclosures on prior directorships, group entities, or legal proceedings

- Undisclosed contingent liabilities — tax disputes and statutory defaults discovered mid-diligence

Each of these can add weeks or months to the timeline when SEBI issues observations.

The Lost Documentation Problem

Companies frequently discover during DRHP drafting that key contracts, board resolutions, or compliance records are missing or internally inconsistent. This triggers last-minute rewrites of disclosures — which introduce new errors — which invite more observations. Each round of rewrites widens the observation surface and compresses the filing window further.

The EbixCash enforcement case (SEBI Order dated December 19, 2024) illustrates what's at stake when documentation discipline breaks down. SEBI found violations including failure to disclose material information about IPO proceed utilisation, a press release that mischaracterised a 64–75% revenue restatement, and public communications issued without mandatory lead manager approval. The penalty was ₹6 lakh — but the reputational and timeline damage was far larger.

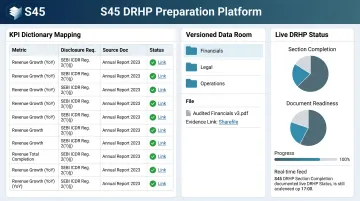

How S45 Addresses This Structurally

The pattern above — missing documents, last-minute rewrites, cascading observations — is structural. S45's approach to DRHP preparation is built around eliminating it before drafting begins, not after SEBI flags it.

The process starts with an AI-led Readiness Scan that surfaces specific disclosure gaps: ESOP dilution not reflected in the cap table, audit committee composition issues, undisclosed contingent liabilities, inconsistent revenue recognition, and unexplained working capital movements.

Every disclosure in the DRHP is then tied to a verified source document through a versioned data room with evidence links. The KPI Dictionary maps each disclosed metric to its underlying evidence, so nothing in the DRHP is unsupported at the time of writing. From clean data room handoff, S45 delivers a DRHP-ready draft in 30 to 45 days.

The Live DRHP Status and SEBI Query Board replaces the fragmented email-and-inbox workflow that traditional banks run — tracking observations with assigned owners (CFO for financials, legal counsel for governance, lead banker for business matters), due dates, and evidence closure in one connected dashboard.

When companies arrive with a DRHP problem — version sprawl across inboxes, no audit trail — the chaos usually traces back to this structural absence.

Frequently Asked Questions

How long is a DRHP valid?

Under Regulation 44 of SEBI ICDR 2018, SEBI's observation letter is valid for 12 months from issuance. If the IPO does not open within this window, the issuer must re-file a fresh DRHP with updated restated financials — and material company or market developments may trigger an early update even within that period.

What is the listing timeline on NSE after an IPO closes?

Per SEBI's August 2023 circular on listing timelines, listing occurs within T+3 working days of the issue closing date — reduced from the prior T+6 norm — with allotment, refund, and registrar processes all required to meet the same T+3 deadline.

How do I find a DRHP on BSE or SEBI's website?

Main Board DRHPs are available on SEBI's public issues filings page, the lead manager's website, and the issuer's own site; NSE hosts RHPs and offer documents at its corporate filings section. SME DRHPs are filed directly on NSE Emerge and BSE SME.

Does an SME IPO need SEBI approval?

No. Under Regulation 246(2) of SEBI ICDR 2018, SEBI explicitly does not issue observations on SME offer documents. The draft is filed directly with the exchange, which conducts the review. However, all ICDR disclosure requirements still apply — the exchange, not SEBI, enforces them.

What is the RHP in an IPO?

The Red Herring Prospectus is the final offer document filed with the Registrar of Companies after SEBI clearance. It incorporates the price band, issue opening and closing dates, and allotment details that are absent from the DRHP. Investors bid during the subscription period against the RHP — it is the operative document from pricing through listing.