The question this article addresses directly: after the Red Herring Prospectus is filed and the IPO closes, where does the Information Memorandum fit — and why does it matter?

The short answer is that the IM is not part of the standard IPO sequence at all. It belongs exclusively to the shelf prospectus framework under Section 31 of the Companies Act, 2013. Understanding this distinction — and the hard filing deadlines that come with it — is what separates compliant issuers from those who find out about the requirement a week before a tranche opens.

Key Takeaways

- Red Herring Prospectus (RHP): filed at least 3 days before subscription opens — full disclosures, no final issue price.

- Information Memorandum (IM): mandatory before each subsequent tranche under a shelf prospectus — not part of the standard DRHP → RHP → Final Prospectus sequence.

- Companies Act, 2013 discontinued pre-RHP IM circulation — a practice the 1956 Act permitted but the current law does not.

- The IM must be filed in Form PAS-2 at least one month before a second or subsequent tranche opens under Rule 10 of the PAS Rules, 2014.

- Missing this deadline can invalidate the tranche and expose directors to liability under Sections 34, 35, and 36 of the Companies Act.

The IPO Document Journey: From DRHP to Final Prospectus

Understanding where the IM sits requires a clear picture of the standard IPO document sequence first.

The Standard Sequence

| Step | Document | Governing Provision | Key Requirement |

|---|---|---|---|

| 1 | DRHP filed with SEBI | SEBI ICDR Reg. 25 | Filed through lead manager before public issue |

| 2 | Public availability | SEBI ICDR Reg. 26 | Minimum 21 days for public comments |

| 3 | SEBI observations | SEBI ICDR Reg. 28 | Issued within 30 days of receipt |

| 4 | RHP filed with ROC | Companies Act s.32(2) | At least 3 days before subscription opens |

| 5 | Subscription period | SEBI ICDR Reg. 266 | 3–10 working days (Main Board) |

| 6 | Final Prospectus | Companies Act s.32(4) | Total capital raised, closing price, residual disclosures |

Section 32(2) of the Companies Act, 2013 requires the RHP to be filed with the Registrar at least three days before the subscription list opens. The RHP is defined by the statute as a prospectus that does not include complete particulars of the quantum or price of the securities — those gaps are filled only after book-building closes.

What the RHP Omits (and Why)

The RHP carries all prescribed disclosures: company history, financial statements, risk factors, management details, objects of the issue, and a price band. What it excludes by statute is the final issue price and the exact quantum of securities since those figures are determined only after the book-building process closes.

After the offer closes, Section 32(4) requires the company to file a final prospectus stating total capital raised, the closing price, and any details not previously included.

Section 32(3) goes further: any variation between the RHP and the final prospectus must be explicitly highlighted — no quiet amendments.

The Information Memorandum plays no role in this standard sequence. It enters the picture only when a company uses a shelf prospectus — a separate instrument that allows multiple tranches of securities to be issued under a single filing. That distinction is what the next section covers.

What Is an Information Memorandum?

Legal Definition and Origin

The Information Memorandum concept was first introduced into Indian company law through Section 60B of the Companies Act, 1956, inserted by the Companies (Amendment) Act, 2000 (Act No. 53 of 2000, assented to on 13 December 2000). Under that regime, a public company could circulate an IM to the public before filing an RHP — the two documents together were deemed a prospectus.

The Companies Act, 2013 discontinued this entirely. There is no provision in the 2013 Act for a pre-RHP information memorandum in a standard IPO. The IM now exists only within the shelf prospectus framework under Section 31.

What the IM Is Under the 2013 Act

Under Section 31, the IM is a tranche-update document: a mandatory disclosure filed before each second or subsequent offer of securities under an existing shelf prospectus. Section 31(3) deems the IM together with the shelf prospectus to constitute a prospectus, which has direct consequences for liability.

It is not a standalone offering document. It must always be read alongside the shelf prospectus it updates — and cannot replace it.

What the IM Is Not

This distinction matters in practice. Founders and CFOs preparing for a public offer sometimes encounter terms like "Offering Memorandum" or "Private Placement Memorandum" in pre-IPO conversations — these are different instruments operating under a different legal regime. The table below sets out where the Section 31 IM sits relative to a private placement offer letter:

| Feature | Information Memorandum (Section 31) | Private Placement Offer Letter (Section 42) |

|---|---|---|

| Legal basis | Section 31, Companies Act, 2013 | Section 42, Companies Act, 2013 |

| Nature of offer | Public offer under shelf prospectus | Private placement to identified persons |

| Filed with | Registrar of Companies (Form PAS-2) | ROC (Form PAS-4); not filed with SEBI |

| Deemed prospectus | Yes, under Section 31(3) | No |

| SEBI regulation | Subject to SEBI ICDR framework | Not governed by SEBI ICDR |

An Offering Memorandum or Private Placement Memorandum used in private capital raises is a different instrument, not filed with SEBI and not subject to the same liability regime.

When Does the IM Come After the RHP?

Who Can Use the Shelf Prospectus Route

Section 31(1) of the Companies Act, 2013 is restrictive on eligibility. The shelf prospectus route is available to:

- Public financial institutions

- Public sector banks

- Scheduled banks whose main object is financing

- Any class of companies SEBI specifies by regulation

Most growth-stage companies preparing for a standard IPO on NSE or BSE are not eligible for the shelf prospectus route. This framework is primarily used by banks, financial institutions, and PSUs raising funds in multiple tranches over a defined period — most commonly in the debt securities space.

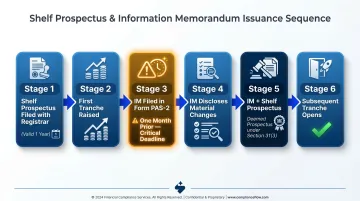

The Shelf Prospectus + IM Sequence

Once an eligible entity files a shelf prospectus, the process works like this:

- Entity files shelf prospectus with the Registrar (valid for up to one year from the date the first offer opens)

- First tranche raised under the shelf prospectus

- Before any second or subsequent tranche: IM filed in Form PAS-2 with the Registrar, at least one month prior to the issue date

- IM discloses all material changes since the previous offer

- IM + shelf prospectus together deemed a prospectus under Section 31(3)

- Subscription for the subsequent tranche opens

The one-month advance requirement comes from Rule 10 of the Companies (Prospectus and Allotment of Securities) Rules, 2014. Form PAS-2 was revised via MCA Notification dated 20 January 2023. This is a hard statutory deadline — not a target.

What This Means for Ongoing Documentation

A common assumption among founders is that once the RHP is filed and the IPO closes, the documentation work is done. For companies on the shelf route, that assumption is wrong. IPO documentation becomes an ongoing obligation tied to each new tranche window.

That obligation has teeth. Companies on the shelf route must maintain continuous records of material developments — financial results, new litigation, regulatory actions, management changes, new charges on assets — so the IM can be prepared accurately and filed within the one-month window.

This is precisely where source-linked disclosure tracking matters. S45's evidence-linked VDR and SEBI Query Board maintain a live, traceable record across the DRHP and RHP lifecycle — so that when the IM deadline arrives, there is no scramble to reconstruct what changed and when.

What an Information Memorandum Contains

Section 31(2) of the Companies Act, 2013 requires the IM to contain all material facts relating to:

- New charges created on company assets

- Changes in financial position since the first or previous offer

- Such other changes as may be prescribed

Form PAS-2 translates this into specific disclosure categories:

| Disclosure Category | Statutory Basis |

|---|---|

| New charges created on assets | Section 31(2) |

| Material changes in financial position | Section 31(2) |

| Changes in share capital | Section 31(2), "changes as may be prescribed" |

| Management changes (directors, KMPs) | Section 31(2), "changes as may be prescribed" |

| Litigation updates and regulatory actions | Section 31(2), "changes as may be prescribed" |

| Updated risk factors | Section 31(2), "changes as may be prescribed" |

| Other material changes | Section 31(2), catch-all |

The Delta Document Principle

The IM is not a re-statement of the full shelf prospectus. It captures only what has changed since the last offer — making it shorter than the original filing but carrying identical legal weight under Section 31(3). It must be read alongside the shelf prospectus to constitute a complete prospectus.

Materiality standard: Information is material if its omission or misstatement could influence the investment decision of a reasonable investor. The statute uses the phrase "all material facts" without prescribing quantitative thresholds — practitioners should apply SEBI's general disclosure guidance and the standards under Section 26 of the Companies Act, 2013.

The Liability Stakes

That deeming provision has teeth. Because the IM is treated as a prospectus under Section 31(3), the full liability framework under Sections 34, 35, and 36 of the Companies Act applies:

- Section 34 (Criminal): Misstatements or misleading omissions → liability under Section 447 (imprisonment of 6 months to 10 years; fine up to 3x the fraud amount)

- Section 35 (Civil): Compensation to subscribers who suffer loss from misleading disclosures; unlimited personal liability where fraud is proved

- Section 36 (Criminal): Fraudulent inducement to invest → liability under Section 447

Directors, promoters, and anyone who authorised the IM's issue face the same personal exposure as they would with any full prospectus. An IM signed off without careful review is not a procedural shortcut — it is a personal liability event for every signatory.

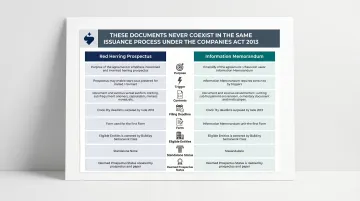

Information Memorandum vs Red Herring Prospectus: Key Differences

These two documents never coexist in the same issuance process under the Companies Act, 2013. Their roles are entirely separate.

| Parameter | Red Herring Prospectus | Information Memorandum |

|---|---|---|

| Purpose | Originating offer document for IPO book-building | Tranche-update disclosure under shelf prospectus |

| Trigger | Standard IPO; filed before subscription opens | Second or subsequent tranche under shelf prospectus |

| Contents | Full disclosures (all SEBI ICDR prescribed items); omits final price | Material changes since last filing only (delta document) |

| Filing deadline | At least 3 days before subscription opens | At least 1 month before subsequent tranche |

| Form | No specific prescribed form (governed by SEBI ICDR format) | Form PAS-2 |

| Eligible entities | All companies making public offers | Public financial institutions, public sector banks, scheduled banks, SEBI-specified classes |

| Standalone document? | Yes — self-contained | No — read alongside shelf prospectus |

| Deemed prospectus? | Yes, under Section 32(3) | Yes, together with shelf prospectus under Section 31(3) |

| Liability | Sections 34, 35, 36 apply | Sections 34, 35, 36 apply |

The historical source of confusion is Section 60B of the 1956 Act, where an IM was circulated before the RHP and both together formed a prospectus. That framework has been abolished. Under the 2013 Act, a company filing a standard IPO will never encounter Form PAS-2 — and a public financial institution using a shelf prospectus will never file an RHP. Knowing which pathway applies upfront prevents misfiled documents and wasted SEBI review cycles.

Frequently Asked Questions

What is an information memorandum in a prospectus?

In the Indian regulatory context, an IM is a document filed before each new tranche of securities under a shelf prospectus. It discloses all material changes since the original shelf prospectus was filed — covering new charges, financial changes, management updates, and litigation — and must be submitted to the Registrar in Form PAS-2 at least one month before the tranche subscription opens.

What is the next step after filing the DRHP?

After filing the DRHP, SEBI typically issues observations within 30 days. The company incorporates required changes and files the RHP at least 3 days before the subscription list opens. Once the offer closes and allotment is complete, a final prospectus is filed with ROC and SEBI disclosing total capital raised, closing price, and any details omitted from the RHP.

What is the difference between an information memorandum and a red herring prospectus?

The RHP is a standalone document used in the IPO book-building process — full disclosures, but no final issue price. The IM is a supplemental update filed only under the shelf prospectus framework, disclosing material changes before each subsequent tranche and read alongside the original shelf prospectus.

Is an information memorandum mandatory under SEBI regulations?

Yes. Filing an IM is mandatory before each new tranche under a shelf prospectus, as required by Section 31 of the Companies Act, 2013 and Rule 10 of the PAS Rules, 2014. Skipping this step can invalidate the tranche and expose the issuer and its directors to both regulatory action and personal liability under Sections 34–36.

Who is responsible for filing the information memorandum?

The issuing company — through its lead manager or merchant banker — prepares and files the IM with the Registrar. Directors bear ultimate legal responsibility for accuracy and completeness, with the same personal liability that applies to any prospectus attaching in full to the IM.

What happens if material changes occur between the RHP and the final prospectus?

Under Section 32(3) of the Companies Act, 2013, any variation between the RHP and the final prospectus must be explicitly highlighted. Section 32(4) then requires the final prospectus to be filed with the Registrar and SEBI, confirming total capital raised, closing price, and any details not included in the RHP.