For Indian founders and promoters, this is one of the most consequential decisions you will make — yet most approach it with generic information that doesn't account for India's specific regulatory framework, market dynamics, or the real operational demands of becoming a listed company.

This article explains what going public means, why companies choose this path, how the IPO process works step by step under SEBI's regulatory framework, and — critically — when it may not be the right move at all.

Key Takeaways

- Going public means selling shares through an IPO and listing on BSE or NSE (Main Board or SME platforms)

- Companies go public to raise equity without debt, give founders and investors an exit path, and build credibility that compounds future fundraising

- The process takes six to twelve months: merchant banker appointment, DRHP filing, SEBI review, roadshow, then listing

- Real costs cover SEBI fees, banker commissions, legal, audit, and registrar — plus ongoing annual compliance after listing

- Most listings that stumble do so on timing, financial gaps, or a weak execution team — not the business itself

What Does Going Public Mean?

Going public is the moment a private company first sells ownership shares to the general public — converting from a privately held entity to one listed and traded on a stock exchange. In India, this happens on the Bombay Stock Exchange (BSE) or the National Stock Exchange (NSE), with the SME segment served by BSE SME and NSE Emerge platforms.

How It Differs from Private Capital Raising

Most founders have raised capital before going public — from angels, venture capitalists, or private equity. The difference is structural:

- Private rounds are negotiated with a small, defined group of investors

- That scale of participation is what creates genuine price discovery — and it's why listed companies carry a different weight in the market than privately held ones of similar size.

Which route applies to your company depends on size and stage. The SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 defines two distinct pathways.

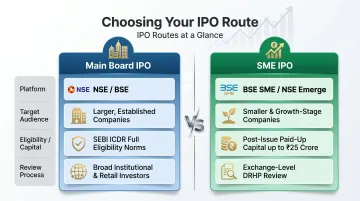

Two IPO Routes in India

The SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 — last amended March 8, 2025 — governs both pathways:

| Route | Platform | Who It's For |

|---|---|---|

| Main Board IPO | NSE / BSE | Larger companies meeting full SEBI ICDR eligibility criteria |

| SME IPO | BSE SME / NSE Emerge | Smaller companies with post-issue paid-up capital up to ₹25 crore |

For SME IPOs, the DRHP is reviewed by the stock exchange rather than SEBI directly — a distinction that affects both the timeline and the depth of regulatory scrutiny involved.

Why Companies Choose to Go Public

Access to Large-Scale Equity Capital

The most direct reason: public markets give companies access to capital that private rounds rarely match. In calendar year 2024, Indian companies collectively raised approximately ₹1,71,051 crore across 326 IPOs — 83 on the Main Board and 243 on SME platforms. The SME segment alone raised ₹8,760 crore in 2024, up 87% from the previous year.

That is equity capital raised without taking on debt or servicing obligations.

Founder and Investor Liquidity

Early-stage investors — venture capitalists, angel investors, PE funds — hold stakes that are illiquid in private markets. An IPO creates a structured exit path. Founders can also monetise partial ownership without diluting the company's fresh capital raise.

This happens through an Offer for Sale (OFS) component, where existing shareholders sell their stakes rather than the company issuing new shares. In FY2024, OFS accounted for 53% of Main Board IPO proceeds.

Credibility and Brand Compounding

Listing on NSE or BSE signals institutional maturity to customers, suppliers, talent, and partners in ways that private funding rounds do not. A well-subscribed IPO — particularly one with strong listing performance — opens doors to partnerships, acquisitions, and relationships with institutional counterparties who require listed-company status as a baseline.

Access to Future Capital

Once listed, companies can raise follow-on capital through QIPs, rights issues, or FPOs far more efficiently than returning to private funding rounds. That repeat-access advantage compounds over time — each successful raise builds the credibility needed for the next one.

The Cost Reality

Going public is expensive. Key cost components include:

- SEBI filing fees: 0.1% of issue size for issues between ₹10 crore and ₹5,000 crore (flat ₹1 lakh for issues up to ₹10 crore)

- NSE annual listing fees: ₹3,00,000 for companies with paid-up capital up to ₹100 crore, scaling to ₹12,20,000+ above ₹1,000 crore

- Merchant banker fees: accounted for more than 4% of issue size for certain IPOs in May 2024

- Additional costs: legal counsel, auditor, registrar, advertising, and printing

These are one-time costs. The ongoing compliance burden — quarterly disclosures, secretarial audits, exchange reporting, investor relations — adds recurring cost that does not end at the listing bell.

How the IPO Process Works in India

The IPO process is a multi-stage, multi-party exercise governed by SEBI's ICDR Regulations. From internal readiness to listing, it typically spans six to twelve months and involves the company, a SEBI-registered merchant banker, legal counsel, auditors, registrars, and stock exchanges operating simultaneously.

Step 1: Appoint an Investment Banker and Assess IPO Readiness

The first decision shapes everything that follows: selecting a SEBI-registered merchant banker (also called a Book Running Lead Manager or BRLM).

The BRLM assesses IPO readiness — audited financials, legal structure, corporate governance, debt profile, regulatory compliance — and determines whether the company should pursue the Main Board or SME route. The quality of this partnership directly affects pricing discipline, SEBI observation outcomes, and subscription results.

S45 moves from first call to signed mandate in seven days and delivers a DRHP-ready draft in 30 to 45 days from data room handoff — roughly a third of the 90+ day conventional timeline. S45 executes alongside Narnolia, a Category-I SEBI-Registered Merchant Banker.

Step 2: File the Draft Red Herring Prospectus (DRHP)

The DRHP is the foundational disclosure document of any Indian IPO. It contains:

- Financial history (three years of audited statements)

- Business description and risk factors

- Use of proceeds

- Promoter details and shareholding structure

- Valuation rationale

The merchant banker drafts this document with legal counsel and auditors, then files it with SEBI and the stock exchanges. SEBI provides observations within 30 days of receipt. Any weakness — incomplete disclosures, inconsistent financials, unclear promoter structure — can delay approval or stall the process entirely.

Step 3: Conduct the Roadshow and Build the Book

Once SEBI issues its observations, the company and its merchant banker conduct a roadshow — presentations to QIBs, NIIs, and retail investor networks. The goals are demand awareness, price band refinement, and order book construction.

Bookbuilding collects bids at different price points within the announced price band during the subscription window (minimum 3 working days, maximum 10 working days under SEBI ICDR). The quality of institutional relationships and the precision of demand mapping before the roadshow determine whether the book builds with depth or fragments across weak demand.

Step 4: Allotment, Listing, and Post-IPO Obligations

After the subscription window closes:

- Shares are allotted per SEBI's pro-rata and lottery rules across investor categories

- The company lists on the exchange on the scheduled date

- The listing price — determined by market demand — becomes the first public signal of investor sentiment

Listing is not the finish line. From this point forward, the company operates under a permanent compliance regime with SEBI and the exchanges:

- Quarterly financial results filed within 45 days of quarter end

- Annual audited results within 60 days of financial year end

- Shareholding patterns within 21 days of quarter end

- Minimum 4 board meetings per year, with no more than a 120-day gap between them

- Continuous disclosure of material events under SEBI LODR Regulation 30

Going public does not end at the listing bell. It marks the beginning of these obligations.

What Makes a Company IPO-Ready in India

SEBI Eligibility Thresholds

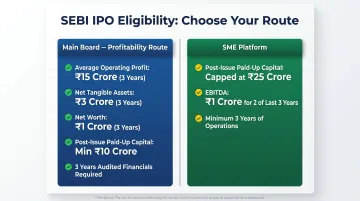

Main Board (Regulation 6(1) — Profitability Route):

- Average operating profit of at least ₹15 crore over the preceding 3 financial years

- Net tangible assets of at least ₹3 crore in each of the preceding 3 years

- Net worth of at least ₹1 crore in each of the preceding 3 years

- Post-issue paid-up capital of at least ₹10 crore

- Three years of audited financial statements

Companies that don't meet the profitability track record can still list via the QIB Route (Regulation 6(2)), provided at least 75% of the net offer is allotted to Qualified Institutional Buyers.

SME Platform:

- Post-issue paid-up capital capped at ₹25 crore

- Operating profit of at least ₹1 crore (EBITDA) for 2 of the 3 preceding financial years

- Minimum 3 years of operations

Operational Readiness Beyond the Checklist

Many companies meet SEBI's eligibility thresholds on paper but aren't ready to sustain investor confidence once listed. The gaps that most commonly surface during pre-filing reviews of growth-stage companies include:

- ESOP dilution not reflected in the cap table

- Audit committee composition issues (SEBI LODR requires at least two-thirds independent directors)

- Undisclosed contingent liabilities or tax disputes

- Inconsistent revenue recognition practices

- Unexplained working capital movements

These gaps often compound each other. Board composition issues, for instance, are rarely a quick fix: if the chairperson is an executive director or promoter, at least half the board must be independent directors. Many founders underestimate how much restructuring this requires — and how long it takes.

Market Timing Matters Too

A company that is technically eligible but listing during unfavourable conditions — high volatility, sector-specific sentiment problems, post-budget uncertainty — may achieve a technically successful IPO but a poor listing and sustained weak aftermarket performance. In 2025, 64% of IPOs were trading below issue price as listing gains faded — the worst performance since 2017, according to PRIME Database data reported by Financial Express. IPO readiness means assessing external market windows, not just internal financial metrics.

The Real Tradeoffs of Going Public

The Accountability Structure Changes Permanently

Founders often believe going public means raising money while retaining control. In practice, public company status introduces a permanent accountability structure that does not switch off:

- SEBI compliance and quarterly disclosure obligations

- Insider trading regulations that apply from the moment the DRHP is filed — not after listing

- A live share price that reflects investor sentiment — not just business fundamentals

- Shareholder pressure on short-term earnings delivery

Some founders mistake high oversubscription for operational success. In CY2024, 80% of mainboard IPOs delivered positive listing-day gains — but only 70% were still trading above issue price weeks later. Subscription is a moment; sustained performance is the actual measure.

When an IPO May Not Be the Right Move

An IPO is a strategic choice, not a default milestone. Consider alternatives when:

- The company lacks predictable, auditable revenue across three financial years

- Founders are not prepared for full public disclosure of financial and business information

- The capital need could be met through private equity, venture debt, or strategic investment at lower cost

- Market conditions make institutional demand shallow for the company's sector

- Governance gaps — missing independent directors, incomplete audit committee, cap table issues — would require 12 to 18 months of remediation before filing

If the capital and liquidity objectives can be met another way, a public listing is the wrong tool for the job. An IPO makes sense when the scale of capital required, the liquidity need, or the strategic signaling of a public market presence cannot be replicated by any private structure — not as a default next step.

Frequently Asked Questions

Why would a company want to go public?

Companies go public primarily to raise large-scale equity capital without taking on debt, provide liquidity to early investors and founders, and gain the credibility that comes with listed status. These advantages compound over time — listed companies can access follow-on capital through QIPs and rights issues far more efficiently than private rounds.

What happens when a company goes public?

Once listed, the company's shares become tradeable on BSE or NSE, and it becomes subject to SEBI's ongoing disclosure and governance requirements under SEBI LODR. Valuation is now determined in real time by market demand, meaning both performance and perception drive the company's standing.

How much does it cost to go public in India?

SEBI filing fees run at 0.1% of issue size; merchant banker fees can exceed 4%. Add legal counsel, auditor, registrar, and advertising costs, and the total one-time outlay runs into crores. Annual recurring costs — exchange listing fees (₹3 lakh to ₹12+ lakh), audit, secretarial, and investor relations — continue every year post-listing.

Can a public company issue another IPO?

A company can only have one IPO — its first public offering. After listing, additional capital can be raised through Follow-on Public Offers (FPOs), Qualified Institutional Placements (QIPs), or rights issues. These are distinct instruments available only to already-listed entities.

What is the difference between an SME IPO and a Main Board IPO?

SME IPOs (BSE SME or NSE Emerge) require a lower financial bar — operating profit of ₹1 crore for 2 of 3 years versus ₹15 crore average for Main Board — and include a mandatory market maker for post-listing liquidity. Main Board IPOs meet SEBI's full ICDR requirements and attract a broader institutional investor base.

How long does it take for a company to go public in India?

From readiness assessment to exchange listing, Main Board IPOs typically take 6–12 months; SME listings run 2–3 months, faster with clean documentation and governance. Many growth-stage companies engage a banker 12–18 months before filing to close readiness gaps first.