Introduction

Get this section wrong in your DRHP and SEBI will find it. Material litigation disclosure requires an issuing company to accurately report all legal proceedings — civil, criminal, tax, and regulatory — that could materially affect its business or finances.

For founders, promoters, CFOs, and company secretaries preparing to go public in India, it is one of the highest-risk sections in the entire offer document. According to market research cited by 5paisa, SEBI raises approximately 100 observations per DRHP on average, with nearly half tied to risk disclosures.

Litigation omissions have caused IPO delays, triggered re-filings, and in serious cases, resulted in market bans and mandated investor refunds.

This guide breaks down what qualifies as "material" litigation, how to structure disclosures across the DRHP, which categories SEBI expects covered, and where companies most commonly go wrong during the review process.

Key Takeaways

- Material litigation disclosure is mandatory under Schedule VI, Part A of SEBI ICDR Regulations 2018, covering the issuer, subsidiaries, promoters, and directors

- A case is "material" if an adverse outcome could influence an investor's decision — regardless of how confident the company is about winning

- Litigation disclosures must align consistently across the Outstanding Litigations chapter, Risk Factors, and Financial Information sections of the DRHP

- SEBI has imposed three-year market bans (DLF, 2014) for promoter-level concealment — omissions at that entity layer carry the most severe consequences

- Catching litigation gaps before filing is far less costly than addressing SEBI observations after the DRHP is submitted

What Is Material Litigation Disclosure in an IPO?

Material litigation disclosure is a statutory requirement under Regulation 28 read with Schedule VI, Part A of the SEBI (ICDR) Regulations, 2018. It mandates issuer companies to report all outstanding legal proceedings involving the company, its subsidiaries, promoters, and directors that cross a defined materiality threshold — giving investors a complete, factual picture of legal exposure before they commit capital.

How It Differs from the Risk Factors Chapter

These two sections are related but serve different functions:

- Outstanding Litigations provides factual case-level detail: case name, court or tribunal, amount at stake, current procedural status

- Risk Factors frames those same litigations as forward-looking narratives — what could happen to the business if outcomes are adverse

Both sections must be internally consistent. A risk mentioned in Risk Factors must correspond to a disclosed case in Outstanding Litigations. Discrepancies between the two are among the most common triggers for SEBI observation letters.

The Materiality Policy Requirement

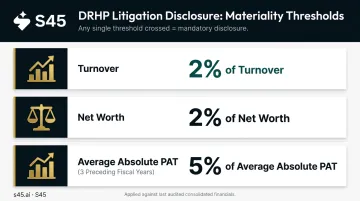

Schedule VI does not prescribe fixed percentage thresholds. Instead, each issuer's board must adopt and disclose a materiality policy within the DRHP itself. In practice, companies benchmark against the SEBI LODR Regulation 30(4)(i)(c) framework, which uses three independent tests:

All thresholds are applied against the last audited consolidated financials.

| Threshold | Trigger |

|---|---|

| Turnover | 2% |

| Net worth | 2% |

| Average absolute PAT (3 preceding fiscal years) | 5% |

Exceeding any single threshold triggers mandatory disclosure. The policy must be board-approved by resolution before DRHP filing.

Why Litigation Disclosures Matter in India's IPO Process

SEBI's review process scrutinises the litigation section in detail. Observation letters routinely flag incomplete case descriptions, missing financial quantum, and omissions at the promoter level — any of which can trigger a re-filing requirement and delay the entire IPO timeline.

The DLF Enforcement Precedent

SEBI's order dated October 10, 2014 (Order No. WTM/PS/124/IVD/OCT/2014) remains the most consequential enforcement action in this area. DLF had filed its DRHP in January 2007 for an IPO to raise ₹9,187.5 crore.

SEBI found that DLF concealed its continued association with three entities — Sudipti Estates, Shalika Estate Developers, and Felicite Builders — by engineering sham share transfers to the wives of Key Managerial Personnel, with purchase funds provided by the KMPs themselves. DLF also failed to disclose an outstanding FIR involving Sudipti Estates. SEBI restrained DLF, five directors, and its CFO from accessing the securities market for three years, which was described at the time as the regulator's harshest penalty.

The DLF case established a clear principle: promoter-level concealment through structural transactions is treated as active fraud, not a borderline disclosure judgment.

That penalty reflects what the underlying regulations actually demand — not disclosure as a best effort, but as a non-negotiable floor.

The Regulatory Framework Behind the Obligation

Two regulations define that floor:

- Regulation 28 of SEBI ICDR Regulations 2018 mandates that the offer document contain all disclosures specified in Schedule VI, including the Outstanding Litigations chapter

- Regulation 30 of SEBI LODR requires listed entities to disclose any material event — including litigation, regulatory orders, and penalties — within 24 hours

For companies preparing to list, Regulation 30 effectively sets the pre-listing standard too: the DRHP's litigation section must meet at least the same threshold that will apply once the company is listed. Building your disclosure framework around both regulations from the outset avoids the common failure mode of retrofitting disclosures after SEBI flags gaps — by which point the timeline cost is already locked in.

How the Litigation Disclosure Process Works

Litigation disclosure is a multi-stage data-gathering, classification, and drafting exercise — it begins during IPO readiness assessment and runs through DRHP filing, SEBI review, and RHP conversion.

Companies that treat it as a last-minute task consistently find themselves rewriting disclosures under pressure once SEBI observations arrive.

Step 1: Litigation Identification and Data Collection

Legal counsel maps every outstanding proceeding across all relevant entities: the issuer, all subsidiaries, all promoters individually, and key directors, organised by entity and jurisdiction.

The output is a master litigation register capturing:

- Case name and parties

- Court, tribunal, or statutory authority

- Nature of claim

- Amount in dispute

- Current procedural status and next scheduled event

This step must be completed before DRHP drafting begins, not alongside it. Missing any entity layer — particularly promoter-level cases — is the most common trigger for SEBI observations.

Catching these gaps early is where the cost is lowest. S45's AI Risk Radar surfaces material litigation gaps during the IPO readiness phase, before formal diligence begins.

Step 2: Materiality Assessment and Classification

With the register complete, each case is assessed against the company's board-approved materiality policy and categorised as follows:

- Criminal proceedings — no monetary threshold; all must be disclosed

- Regulatory and statutory actions — no threshold; all must be disclosed

- Tax claims — consolidated disclosure with aggregate count and amount

- Other civil and commercial litigation — disclosed if above the quantitative threshold

Cases that fall below the materiality threshold are still reviewed for qualitative factors: reputational risk, regulatory nature, and precedent-setting implications. The SAT, in its ruling on the Credit Analysis and Research Limited (CARE Ratings) case, established that the "nature" of information determines materiality, not its monetary value alone. When in doubt, the safer position is disclosure.

Step 3: Drafting, Internal Review, and DRHP Integration

Approved disclosures are drafted to capture case identity, current stage, financial quantum, and potential impact on the business. Each disclosure is cross-referenced with the Risk Factors chapter and Financial Information section to ensure consistency across the document.

The draft is then reviewed by legal counsel and the lead manager (BRLM), who must certify due diligence under Schedule V of SEBI ICDR Regulations 2018 before the DRHP is filed.

S45's platform manages this stage through a versioned virtual data room with source links, audit trails, and a SEBI Query Board with assigned owners, due dates, and evidence closure tracking. DRHP version control scattered across email inboxes makes SEBI observation responses genuinely difficult to manage; organised source documentation removes that friction entirely.

Categories of Litigation That Must Be Disclosed in the DRHP

Schedule VI establishes five mandatory sub-categories for each entity grouping (issuer, subsidiaries, directors, promoters, group companies):

Criminal Proceedings

All outstanding criminal cases require disclosure regardless of financial quantum. SEBI treats criminal proceedings against promoters and directors as reputational and regulatory risks that investors can't evaluate without the full picture. Pending investigations and FIRs must be assessed for materiality — not assumed immaterial simply because no charge sheet has been filed.

The DLF case demonstrated what happens when an undisclosed FIR against an associate entity surfaces post-filing. That single omission became the foundation for the entire enforcement action.

Actions by Statutory and Regulatory Authorities

Show-cause notices, penalties, and enforcement actions from the following regulators all require disclosure: MCA, RBI, SEBI, IRDAI, environmental authorities, and sector-specific bodies. These carry dual risk — financial penalty and licence or approval jeopardy. Full factual context is required for each:

- Nature of the default or non-compliance

- Corrective action taken (if any)

- Current status of the proceeding

Tax Disputes

Income tax, GST, customs, and excise disputes before CIT(A), ITAT, High Courts, or other tax tribunals must be disclosed in consolidated form: total number of cases and aggregate amount in dispute. For mid-sized companies, this is often the most voluminous category.

Common error to avoid: Netting tax provisions against demands understates the disclosed amount and creates inconsistencies with the contingent liabilities note in the financials — a pattern SEBI flags consistently.

Civil and Commercial Litigation

Civil and commercial cases — contract disputes, property claims, consumer complaints, and labour matters — are assessed primarily on financial quantum relative to net worth or revenue. A large commercial arbitration against a key customer or supplier can be material even when the outcome is uncertain. Quantum alone does not determine materiality; counterparty significance does too.

Contingent Liabilities

Not every material litigation surfaces as a named disclosed case. Contingent liabilities under Ind AS 37 that arise from legal proceedings must be cross-referenced with the Financial Statements section of the DRHP.

Discrepancies between the contingent liabilities note and the Outstanding Litigations section are one of the most consistent triggers for SEBI observations. Reconciling these two disclosures before filing is non-negotiable.

Common Errors in Litigation Disclosures

Incorrect Assumption About Entity Scope

Many companies disclose only the issuer's own litigation and omit promoter-level cases, subsidiary disputes, or group company proceedings. SEBI's ICDR framework requires disclosure across all promoters, directors, subsidiaries, and group companies. Promoter-level omissions have triggered the most severe enforcement actions — the DLF case is the clearest example.

Vague or Incomplete Case Descriptions

Describing litigation in generic terms — "a commercial dispute is pending" — without naming the forum, the financial quantum, or the current procedural stage fails SEBI's precision standard. Each case disclosure must be specific enough for an investor to independently assess exposure: the amount in dispute, the court or tribunal, and the next scheduled hearing date.

Conflating Materiality with Likelihood of Loss

A case the company expects to win still requires disclosure if losing would materially affect revenue or net worth. Materiality is tested by potential adverse impact — not probability of winning. A large contract dispute with strong legal defences remains disclosable if the adverse outcome would affect a significant portion of financials.

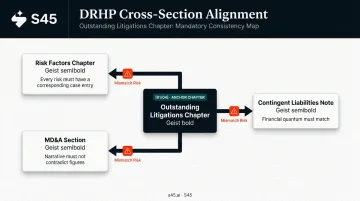

Inconsistency Between Sections

The Outstanding Litigations chapter must align precisely with three other sections of the prospectus:

- Risk Factors chapter — every risk mentioned must have a corresponding case entry

- Contingent liabilities note in the financial statements — quantum must match

- MD&A section — narrative discussion must not contradict disclosed figures

SEBI's observation letters routinely flag discrepancies where a risk appears in Risk Factors but the underlying case is absent from Outstanding Litigations, or where financial quantum differs across sections. These inconsistencies signal poor due diligence and invite deeper regulatory scrutiny.

Frequently Asked Questions

What information is typically excluded from a DRHP?

The DRHP excludes the final issue price and the exact number of shares to be offered — these appear in the RHP and Prospectus. All material information about the company, including litigation, must be disclosed. Omission of any item that could affect an investor's decision is grounds for SEBI objection.

What litigation disclosures are required for promoters and directors in a DRHP?

Promoters and directors must individually disclose all pending criminal proceedings, regulatory actions, tax demands, and civil disputes above the materiality threshold. This applies to each named individual, not just the company entity. SEBI's ICDR Regulations require this at both the individual and group-entity level, covering the past ten years of litigation history.

What disclosures are required under Regulation 30 of SEBI LODR?

Regulation 30 requires listed entities to disclose any material event or information — including initiation of litigation, regulatory orders, or penalties — to stock exchanges within 24 hours. For companies preparing to list, Regulation 30 sets the disclosure standard that the DRHP's litigation section must meet and maintain post-listing.

Which section of the DRHP discloses outstanding dues to creditors?

Outstanding dues to creditors are disclosed in the "Outstanding Litigations and Material Developments" chapter, cross-referenced with the Financial Information section. MSME and other creditors are disclosed separately. Where creditor disputes have escalated to legal proceedings, they must appear in the litigation disclosure with forum, quantum, and current status.

How does SEBI define "material" litigation for IPO disclosure?

SEBI does not prescribe a single fixed threshold. Each company must adopt a board-approved materiality policy covering both quantitative factors (amount in dispute as a percentage of net worth or revenue) and qualitative factors (reputational risk, regulatory nature, precedent impact). This policy must be documented and consistently applied across all entities covered in the DRHP.

What are the consequences of omitting material litigation from a DRHP?

Consequences range from SEBI observation letters requiring re-disclosure and re-filing (which can push listing timelines back by months) to enforcement actions including financial penalties, market bans, and mandated investor refunds. SEBI has imposed all of these outcomes in past cases, with the DLF three-year market ban representing the most severe end of the enforcement spectrum.