Introduction

Many Indian founders underestimate the structural demands of going public. A 2025 report shows India's IPO market mobilized ₹1,71,507 crore in FY2024-25, yet approximately 65% of SME listings in CY2024 traded below issue price, signaling that market access has outpaced readiness.

IPO planning is the structured process a private company in India undertakes to prepare for, execute, and sustain a public listing on NSE or BSE. It covers regulatory readiness, documentation, pricing, and post-listing compliance. Without structured preparation, even fundamentally strong companies stumble through lost documentation, broken workflows, and unclear pricing.

This guide is for founders, promoters, and senior management preparing for a public listing in India. What you'll find here is a practical breakdown of every phase — from readiness assessment through post-listing compliance — so you can approach SEBI's DRHP review with 12–24 months of clean, disciplined preparation already behind you.

Key Takeaways

- IPO planning spans 12–18 months: readiness assessment, SEBI filings, bookbuilding, and post-listing compliance

- SEBI's ICDR Regulations govern eligibility, disclosure, and DRHP filing; gaps at any stage can delay or kill the listing

- Selecting the right investment bank early is one of the most consequential decisions in the IPO journey

- Most IPOs stumble on poor financial records and underestimated timelines

- SME and Main Board IPOs share the same planning arc but diverge sharply on eligibility thresholds and compliance obligations

What Is IPO Planning?

IPO planning is the end-to-end process of assessing readiness, assembling a qualified team, preparing statutory disclosures, managing investor demand, and building post-listing governance — all before the listing date is set. Done well, it produces a public listing that accurately reflects the company's value, attracts the right investors, and sets up compliant, well-governed post-listing operations.

The listing day is the outcome of this process, not the process itself. What makes a clean listing possible is 12–24 months of structured, disciplined work — not ad-hoc preparation that creates last-minute fire drills.

IPO planning covers five distinct phases:

- Readiness assessment — identifying financial, legal, and governance gaps before filing

- Team assembly — appointing merchant bankers, legal counsel, auditors, and registrars

- Statutory disclosure preparation — drafting the DRHP and RHP to SEBI ICDR standards

- Demand management — bookbuilding, anchor allocation, and investor roadshows

- Post-listing governance — investor relations, compliance calendars, and liquidity management

The IPO Planning Process in India: Step by Step

The IPO process in India typically spans 12–24 months from the readiness decision to listing day. It is governed at each stage by SEBI's ICDR Regulations, SEBI LODR, and NSE/BSE listing requirements.

Below is the structured roadmap every Indian company must follow.

Step 1: IPO Readiness Assessment

A readiness assessment covers:

- Financial audit readiness — typically 3 years of audited financials under Indian GAAP or Ind AS

- Corporate governance structure — board composition, audit committee formation, and independent director appointments

- Related party transaction cleanup — ensuring all RPTs are disclosed and defensible under SEBI scrutiny

- Promoter shareholding patterns — calculating minimum promoter contribution and verifying lock-in compliance

- Regulatory non-compliance identification — flagging and resolving any legal, tax, or regulatory gaps before filing

Why this step is the most underestimated:

Issues found here—such as missing segment disclosures, restatement requirements, or undocumented promoter loans—can add months to the timeline if caught late rather than early. According to a SEBI board memorandum reviewing 64 companies listed in 2021, 24 companies failed to disclose audited or limited reviewed financial results for one quarter due to regulatory gaps. Financial disclosure readiness is a material gap area.

Many companies work with their advisors for 12–18 months before filing to ensure thorough preparation.

Step 2: Assembling the IPO Team

The key intermediaries a company must appoint:

| Intermediary | Role |

|---|---|

| Book Running Lead Manager (BRLM) | Drives documentation quality, pricing discipline, and investor demand mapping |

| Legal Counsel | Prepares due diligence certificates and ensures compliance with SEBI ICDR norms |

| Statutory Auditor | Audits financial statements and provides comfort letters |

| Registrar to the Issue | Handles application processing, allotment, and refunds |

| Market Maker (for SME IPOs) | Provides two-way quotes to ensure post-listing liquidity |

The investment bank is the most strategic appointment among these intermediaries. It drives documentation quality, pricing discipline, and investor demand mapping — and the quality of this choice shapes every subsequent step. Banks that pair sector expertise with structured analytics can move from first call to signed mandate in as few as 7 days and deliver DRHP-ready drafts in 30–45 days.

The BRLM must hold a Category-I Merchant Banker registration with SEBI, which authorizes issue management, underwriting, advisory, and portfolio management activities.

Step 3: Filing the Draft Red Herring Prospectus (DRHP) with SEBI

The DRHP contains:

- Business overview and competitive positioning

- Risk factors and material contracts

- Financial statements for 3 years (restated under Ind AS if applicable)

- Use of IPO proceeds

- Management background and promoter details

- Corporate governance disclosures

SEBI review cycle:

After filing, SEBI typically issues observations within 30 days for SME listings and 30–75 days for Main Board IPOs. Companies must respond to SEBI queries accurately and completely. Incomplete responses extend the review cycle.

Per a SEBI board memorandum from November 2022, SEBI issues its Observation Letter within 30 days of receipt of satisfactory reply from the Lead Manager.

Evidence-linked drafting reduces observation cycles:

Investment banks like S45 use versioned virtual data rooms where every disclosure in the DRHP is directly linked to its source document. This ensures that every statement is backed by verifiable evidence, minimizing back-and-forth with SEBI.

Step 4: Roadshow and Bookbuilding

The roadshow is a series of investor presentations lasting 1–2 weeks for Main Board IPOs. Management pitches to qualified institutional buyers (QIBs), non-institutional investors (NIIs), and high-net-worth individuals to build demand ahead of pricing.

The price band is set based on valuation models (sector comparables, cash-flow methods), demand signals from pre-IPO soundings, and peer multiples adjusted for current market conditions.

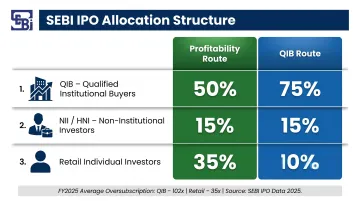

Bids are collected during the subscription window across QIB, NII, and retail categories. Per SEBI ICDR Regulations, the allocation structure is:

| Category | Profitability Route | QIB Route |

|---|---|---|

| QIB | Not more than 50% | At least 75% |

| NII (HNI) | Not less than 15% | Not more than 15% |

| Retail (RII) | Not less than 35% | Not more than 10% |

Subscription levels directly influence allotment and pricing decisions. FY2025 mainboard IPOs averaged 102x QIB oversubscription and 35x retail oversubscription, but companies must still demonstrate fundamentals—hype-driven pricing leads to poor post-listing outcomes.

Step 5: Listing Day and Post-IPO Compliance

What happens on listing day:

- Shares are allotted to investors

- Refunds are processed

- Trading begins on NSE or BSE

The listing price reflects opening demand and often diverges from the issue price depending on subscription quality and market conditions.

T+3 listing timeline:

Effective December 1, 2023, SEBI mandated listing within T+3 days of issue closure (previously T+6). Allotment, refund, and share credit processes are compressed; issuers must ensure intermediary coordination is airtight.

Post-IPO obligations that are frequently underplanned:

- Quarterly financial disclosures within 45 days of quarter-end (Regulation 33(3)(a))

- Annual results within 60 days of year-end

- Board composition requirements — at least one-third independent directors (one-half if chair is executive or promoter-related), at least one woman director

- Related party transaction approvals — all RPTs require prior audit committee approval; material RPTs (exceeding ₹1,000 crore or 10% of consolidated turnover, whichever is lower) require shareholder approval

These obligations begin the moment a company is listed and require dedicated internal resources or external support. S45 integrates post-IPO investor relations directly into its end-to-end mandate — not as an afterthought — so listed companies have continuity from day one of trading.

Key Factors That Shape IPO Readiness in India

Financial Record Quality

Three years of clean, audited financials—restated if necessary to comply with SEBI's disclosure norms—is non-negotiable. Per SEBI ICDR Regulations, companies must provide financial data for the "preceding three full years" to calculate net tangible assets, net worth, and operating profits for eligibility.

Ind AS is mandatory for all listed companies and for unlisted companies with net worth of Rs 250 crore or more. Companies listing on the SME exchange are exempt from Ind AS requirements.

Corporate Governance and Promoter Structure

SEBI scrutinizes promoter group composition, related party transactions, and board independence. Companies with complex holding structures or undisclosed related-party dealings often face extended SEBI review cycles.

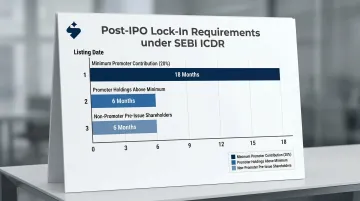

Promoter lock-in requirements (post SEBI ICDR Third Amendment 2021):

| Lock-in Category | Duration |

|---|---|

| Minimum promoter contribution (20%) | 18 months |

| Promoter holdings above minimum | 6 months |

| Non-promoter pre-issue shareholders | 6 months |

Minimum public shareholding is 25% for listed companies, with new tiered slabs introduced in March 2026 for large issuers.

Internal Systems and Process Scalability

Weak ERP systems, manual close processes, and missing internal controls go beyond audit findings. They tell institutional investors the company cannot operate at scale under public scrutiny — and that judgment alone is enough for many funds to pass on an otherwise strong business.

Common internal readiness gaps that flag during due diligence:

- Fragmented financial reporting with no single source of truth

- Manual month-end close processes lasting more than 10 days

- Absent or untested internal audit function

- No documented SOPs for revenue recognition or expense approvals

Market Conditions and IPO Timing

External factors—secondary market performance, sector sentiment, liquidity cycles, and macroeconomic conditions—affect whether an IPO is likely to be well-received. The right window must be matched with genuine readiness, not used as a reason to rush.

Getting these four factors right simultaneously is what separates a clean listing from a delayed or withdrawn one.

Common IPO Planning Mistakes Indian Companies Make

Underestimating the Timeline

Many founders believe IPO preparation takes 3–6 months. In practice, cleaning up financials, resolving corporate governance issues, appointing and coordinating all intermediaries, and navigating SEBI observations typically takes 12–24 months. Rushing creates documentation gaps that regulators and investors notice.

Treating DRHP Drafting as a Passive Exercise

Founders who delegate the DRHP entirely to their banker or legal counsel often end up with a disclosure document that misrepresents competitive positioning or understates key risks. SEBI expects management to own the narrative. Investors can tell when founders don't know their own prospectus.

The Oversubscription Trap

High subscription multiples feel like validation — but they're not the sole measure of a well-planned IPO. What matters equally is investor quality: did long-only institutional funds and sector-focused QIBs participate? And is the company positioned for sustained post-listing performance, or just a listing pop followed by price decay?

Ignoring Post-Listing Obligations During the Planning Phase

Most companies plan intensively for the listing event but fail to build internal capacity for what comes after. The obligations that catch companies off guard include:

- SEBI LODR compliance — ongoing disclosure requirements with strict timelines

- Quarterly financial disclosures — formatted and filed to exchange standards

- Investor relations management — maintaining institutional confidence post-listing

This gap typically becomes visible within the first two quarters and, left unaddressed, erodes the institutional confidence built during the IPO itself. S45 builds post-IPO IR into every engagement from the start — not as an add-on, but as a core part of the mandate.

When an IPO May Not Be the Right Move

Situations Where IPO Timing Is Premature

A company is not ready if:

- Unresolved promoter disputes exist

- Pending regulatory actions are outstanding

- The company has less than 3 years of consistent profitability or auditable revenue (for Main Board)

- The business model has not yet demonstrated scalability at public market valuations

Alternatives Worth Evaluating

Two routes are worth serious consideration when a Main Board IPO isn't the right fit yet.

SME IPO lists on BSE SME or NSE Emerge, with shorter timelines (12–18 months) and lower eligibility thresholds than the Main Board. Companies can later migrate once they meet:

- Paid-up capital ≥ ₹10 crore

- Market cap ≥ ₹100 crore

- 3+ years listed (migration takes 3–5 months)

Speed is the appeal. The risk is real, though: 65% of CY2024 SME listings trade below issue price, and roughly 10–12% face trading suspensions for non-compliance.

Qualified Institutional Placement (QIP) is available only to companies already listed. It lets them raise capital from QIBs via private placement — no pre-issue SEBI filings required. FY2024-25 saw 91 QIP issues raising ₹1,35,597 crore, reflecting strong institutional appetite.

If a Main Board IPO isn't feasible yet, the SME route or a QIP can bridge the gap — but each comes with distinct trade-offs in visibility, compliance burden, and post-listing performance that founders should weigh carefully before committing.

Conclusion

IPO planning is not a pre-listing checklist—it is a structured, multi-stage process that requires operational discipline, clean financials, the right intermediaries, and a clear equity story built well before SEBI ever sees the DRHP.

The quality of the planning process directly determines the quality of the listing outcome. Three outcomes consistently separate well-prepared companies from last-minute ones:

- Better pricing, anchored by a defensible valuation and clean financials

- Stronger investor quality, driven by targeted pre-marketing and clear demand mapping

- More resilient post-listing performance, built on a shareholder base that understood the story before listing day

Companies that treat IPO planning as a structured discipline — not an event to manage under pressure — tend to list on their terms. If your company is evaluating a public listing on NSE or BSE, S45's advisory process starts with an AI-powered readiness assessment that identifies gaps before they become filing problems.

Frequently Asked Questions

What is an IPO plan?

An IPO plan is the structured roadmap a company creates before going public, covering readiness assessment, regulatory documentation, intermediary appointments, investor outreach, pricing strategy, and post-listing compliance—typically developed 12–24 months before the intended listing date.

How long does the IPO process take in India?

The end-to-end timeline depends on the route: Main Board engagements typically run 6–12 months from mandate to listing; SME listings can close in 2–3 months. SEBI's DRHP review takes 30–75 days for Main Board and around 30 days for SME, with roadshow and subscription periods adding further time after observations are received.

What is the difference between an SME IPO and a Main Board IPO in India?

SME IPOs list on BSE SME or NSE Emerge with lower eligibility thresholds and higher minimum lot sizes. Main Board IPOs list on BSE or NSE and carry stricter financial, governance, and disclosure requirements. Both require a SEBI-registered BRLM and DRHP filing, but post-listing compliance intensity is substantially higher on the Main Board.

What documents are required to file an IPO in India?

The core filing requires:

- Draft Red Herring Prospectus (DRHP)

- Three years of audited financial statements

- Due diligence certificates from the BRLM and legal counsel

- Promoter disclosures and in-principle listing approval from the exchange

- SEBI-mandated certificates and declarations

Who are the key intermediaries in an Indian IPO?

The mandatory intermediaries are the Book Running Lead Manager (investment bank), statutory auditor, registrar to the issue, legal counsel, bankers to the issue, and—for SME IPOs—a market maker. The BRLM coordinates all intermediaries and is accountable to SEBI for the accuracy of the DRHP.

What are the SEBI eligibility criteria to file for a Main Board IPO?

Two routes apply. Under the profitability route, the company needs net tangible assets of at least ₹3 crore in each of the preceding 3 years and average pre-tax operating profit of at least ₹15 crore in any 3 of the last 5 years. If those thresholds aren't met, the QIB route requires allocating at least 75% of the issue to qualified institutional buyers—and carries higher scrutiny from the market.