Introduction

The Nifty 50 is India's benchmark index — 50 of the country's most investable listed companies, tracked by roughly ₹4.9 trillion in passive funds and ETFs. When a stock enters the index, passive funds are required to buy it mechanically, often moving ₹800–1,000+ crore in a matter of days. Removal triggers the same dynamic in reverse.

Yet most investors — and most founders of listed companies — don't fully understand how stocks earn or lose a spot on it.

That gap is worth closing. This guide covers the governing body, the five eligibility criteria, the review calendar, common removal triggers, what index changes signal for stock returns, and how the NIFTY Next 50 feeds into the main index.

Key Takeaways

- NSE Indices Limited governs the Nifty 50; all inclusion/exclusion decisions go through the Index Maintenance Sub-Committee

- All five criteria must be met together: F&O eligibility, ≤0.50% impact cost, 100% trading frequency, 1.5× free-float market cap threshold, and 6-month listing history

- Reviews happen twice yearly using data to January 31 and July 31; changes take effect end-March and end-September

- Most price movement happens before formal inclusion or exclusion — not after

- Graduating through NIFTY Next 50 (ranks 51–100) is the mandatory staging ground for any Nifty 50 candidacy

What Is the Nifty 50 Index?

The Nifty 50 is a free-float market capitalisation-weighted index of 50 large-cap companies listed on the National Stock Exchange. Launched on April 22, 1996, with a base value of 1,000 (base date: November 3, 1995), it is the primary benchmark for Indian ETFs, index mutual funds, and F&O contracts.

How the Index Is Calculated

The index uses a single formula:

NIFTY = (Current Market Value ÷ Base Market Capital) × 1,000

The index switched from full market cap to free-float methodology in June 2009, which means only publicly tradeable shares — not promoter-held shares — count toward each company's weight. This better reflects the shares actually available to investors.

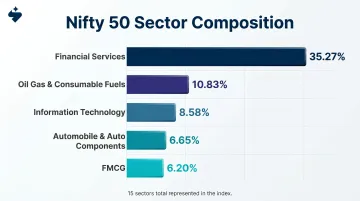

Scale and Sector Composition

That methodology shapes how much weight each company carries — and at scale, the numbers are significant. As of March 2026, the Nifty 50 represents approximately 53.73% of NSE's free-float market capitalisation, with a total market cap of roughly ₹209 lakh crore.

The index spans 15 sectors, with concentration heavily skewed toward a few:

| Sector | Index Weight |

|---|---|

| Financial Services | 35.27% |

| Oil, Gas & Consumable Fuels | 10.83% |

| Information Technology | 8.58% |

| Automobile & Auto Components | 6.65% |

| FMCG | 6.20% |

The top five constituents by weight — HDFC Bank, Reliance Industries, ICICI Bank, Bharti Airtel, and Larsen & Toubro — together account for over 37% of the index.

Who Governs the Nifty 50?

The Nifty 50 is owned and managed by NSE Indices Limited, a wholly owned subsidiary of NSE. Governance operates through a three-tier structure:

- Board of Directors of NSE Indices Limited

- Index Advisory Committee (Equity)

- Index Maintenance Sub-Committee, or IMSC (Equity)

The IMSC is the decision-making body for all inclusions and exclusions. It applies published criteria without subjective discretion — decisions follow a defined rules-based methodology.

Outside its standard review cycle, the IMSC can act on several triggers:

- Quarterly screenings of existing constituents for compliance with SEBI's portfolio concentration norms

- Mergers and delistings that require a replacement constituent

- Regulatory reconstruction schemes that necessitate off-cycle reconstitutions overriding the standard calendar

The 5 Criteria a Stock Must Meet to Enter the Nifty 50

All five criteria must be satisfied simultaneously — clearing four of five is not enough to qualify.

Here's what each criterion demands at a glance:

| Criterion | Threshold |

|---|---|

| F&O Segment Eligibility | Must be listed on NSE F&O + Nifty 100 constituent |

| Impact Cost | ≤ 0.50% for 90% of observations (₹10 Cr basket, last 6 months) |

| Trading Frequency | 100% — traded on every market session over 6 months |

| Free-Float Market Cap | ≥ 1.5× the smallest existing Nifty 50 constituent |

| Listing History | Minimum 6 months (1 month exception for large IPOs) |

Criterion 1: F&O Segment Eligibility

The stock must be actively traded in NSE's Futures & Options segment. F&O eligibility itself requires SEBI's approval, based on minimum market cap, liquidity, and investor base. This is a hard pre-filter: a stock cannot be considered for Nifty 50 inclusion if it isn't already in the F&O segment. A company must also be a Nifty 100 constituent to qualify.

Criterion 2: Impact Cost ≤ 0.50%

Impact cost measures the price slippage when executing a large trade. If the mid-price of a stock is ₹100 but a ₹10 crore buy order can only be filled at ₹100.60 on average, the impact cost is 0.60%, which exceeds the threshold.

The rule: 0.50% or less for 90% of observations over the past six months, measured on a ₹10 crore basket size. Stocks that look large on paper but can't absorb institutional-sized trades without moving the price don't pass this test.

Criterion 3: 100% Trading Frequency

The stock must have traded on every single market session over the prior six months. Zero tolerance. This rule eliminates thinly traded companies that may carry significant market caps on paper but cannot sustain continuous price discovery — a prerequisite for an index that passive vehicles must track daily.

Criterion 4: Free-Float Market Cap Threshold

A candidate's average free-float market cap must be at least 1.5 times the average free-float market cap of the smallest existing Nifty 50 constituent.

This threshold is dynamic. As existing constituents grow or contract, the bar shifts with them. There is no fixed rupee figure — the index recalibrates around its own composition.

Criterion 5: Listing History

A stock needs a minimum 6-month listing history on NSE. For recently listed companies (large IPOs in particular), an exception allows consideration after just 1 month.

Two additional rules apply across all candidates:

- Companies with Differential Voting Rights (DVR) shares are eligible

- A maximum of 5 new stocks (10% of the index) can be added in any calendar year

The Semi-Annual Review Process: When and How Changes Are Made

The Review Calendar

| Step | Timing |

|---|---|

| Data compiled for | Six months ending January 31 and July 31 |

| Changes announced with | Minimum 4-week advance notice |

| Changes effective from | Last trading day of March and September |

The 4-week notice period is not incidental — it exists specifically so ETFs, index funds, and institutional portfolios can rebalance without triggering disruptive price swings.

Selection Mechanics

NSE Indices evaluates all Nifty 100 constituents against the five criteria. Qualifying companies are ranked by average free-float market cap. The largest eligible candidate replaces the smallest existing constituent that no longer clears the eligibility bar.

Off-Cycle Reconstitutions

The standard calendar can be bypassed when extraordinary events demand it:

- HDFC–HDFC Bank merger (July 2023): HDFC Ltd. ceased to exist as an independent entity upon merger with HDFC Bank on July 1, 2023. LTIMindtree was added as an off-cycle replacement.

- Yes Bank (March 2020): After the RBI's gazette notification on the Reconstruction Scheme, the IMSC accelerated removal to March 19, ten days ahead of the originally scheduled March 27 date.

- Satyam (January 2009): Removed on January 12, 2009, after the accounting fraud admission made continued inclusion untenable.

Recent Changes

March 2025: Zomato (now Eternal) and Jio Financial Services replaced BPCL and Britannia Industries. Both entrants had six-month average free-float market caps exceeding 1.5 times those of the departing constituents.

September 2025: InterGlobe Aviation (IndiGo) and Max Healthcare replaced IndusInd Bank and Hero MotoCorp. Max Healthcare alone was estimated to attract approximately $400 million in passive inflows upon inclusion. That figure illustrates the scale of forced buying that index entry triggers across the passive ecosystem.

The 5-stock annual cap keeps turnover low by design. For companies approaching Nifty 50 eligibility, that discipline means the window opens infrequently — but the demand impact when it does is substantial.

Why Stocks Get Removed from the Nifty 50

Inadequate Free-Float Market Capitalisation

The most common removal trigger. During semi-annual reviews, the smallest constituent is replaced when a larger eligible candidate qualifies. A stock that significantly underperforms its peers — as BPCL and Britannia did before their March 2025 exit, and IndusInd Bank and Hero MotoCorp before September 2025 — will eventually fall below the 1.5× threshold relative to eligible outside candidates.

Corporate Actions

Mergers and restructurings can force exits when a company ceases to exist as an independent listed entity. HDFC's 2023 exit was not a failure — it was a consequence of a successful merger. That's a different outcome entirely from exits driven by operating distress.

Governance and Regulatory Failures

A deteriorating governance profile can cause a stock to lose F&O eligibility, which automatically disqualifies it from Nifty 50 membership. The Satyam (2009) and Yes Bank (2020) cases are the clearest examples — both stocks experienced catastrophic price declines before formal removal, not after.

Declining Liquidity

A stock that fails the impact cost or trading frequency test will be excluded even if its market cap remains large. Prolonged regulatory probes can scare off market makers, triggering this outcome.

The Counter-Intuitive Truth About Exclusion

The same research found that excluded companies sometimes delivered better returns post-exit. Freed from the constant institutional scrutiny that index membership brings, management teams often refocus on fundamentals.

Academic research published in Global Business Review reinforces this: "deleted stocks outperform the market in the long run." In practice, by the time formal removal is announced, the price damage is largely done — investors who wait for the official date are reacting to yesterday's news.

A 2024 Economic Times study by Kumar Shankar Roy covering 48 stocks (25 entries, 23 exits since 2015) found that "a large part of value destruction happens before formal exclusion" — the market front-runs removals well in advance of the announcement.

The NIFTY Next 50: India's Waiting Room for Index Inclusion

NIFTY Next 50 (also called NIFTY Junior) tracks companies ranked 51st to 100th by free-float market cap on NSE. It uses the same methodology and draws from the same Nifty 100 universe as the Nifty 50 — which means it functions as the mandatory staging ground for future Nifty 50 candidates.

Every recent Nifty 50 entrant — Zomato, Jio Financial Services, Max Healthcare, InterGlobe Aviation — graduated directly from NIFTY Next 50. This pathway is not incidental; the methodology requires Nifty 100 membership as a prerequisite for Nifty 50 consideration.

Why NIFTY Next 50 Membership Matters

- ICICI Prudential's Nifty Next 50 Index Fund alone holds approximately ₹8,900 crore in AUM — passive buying pressure that begins before Nifty 50 entry

- Analyst coverage and institutional ownership typically expand with NIFTY Next 50 membership, compounding over time

- For many stocks, the most significant price appreciation happens during this phase — not after Nifty 50 inclusion, but before it

For companies that have recently completed an IPO, the trajectory toward NIFTY Next 50 and eventually Nifty 50 candidacy depends on sustained free-float market cap growth through strong operating performance and disciplined investor relations.

Building that market cap doesn't happen passively. S45's post-listing IR services cover index inclusion tracking, free-float calculations, institutional investor targeting, analyst coverage coordination, and quarterly earnings cadence management — structured specifically to keep newly listed companies on this trajectory.

DSM Fresh Foods founder Deepanshu Manchanda put it directly after listing: "When I see our stock trade with stability and gradual compounding, I know it is the outcome of a disciplined process." Stable institutional ownership, built methodically in the months after listing, is what separates index candidates from companies that plateau.

Frequently Asked Questions

What are the criteria for stocks to be included in the Nifty 50 index?

Five criteria must all be met: active F&O trading on NSE, average impact cost ≤0.50% on a ₹10 crore basket (90% of observations over six months), 100% trading frequency over the prior six months, free-float market cap at least 1.5× the smallest existing constituent, and a minimum 6-month NSE listing history.

Which stocks are included in the Nifty 50?

The index holds exactly 50 stocks across 15 sectors; visit niftyindices.com for the current list, which changes semi-annually. Prominent current constituents include HDFC Bank, Reliance Industries, ICICI Bank, Infosys, TCS, and Bharti Airtel.

How many stocks are in the Nifty 50 index?

Always exactly 50. Every new inclusion is matched by a corresponding exclusion, and a maximum of 5 new stocks can be added in any calendar year to limit index churn.

Can you explain the Nifty 50 index simply?

The Nifty 50 tracks India's 50 largest and most liquid listed companies across the economy's major sectors. Because it spans financials, energy, tech, consumer goods, and more, it moves broadly in line with India's corporate health — which is why it anchors the country's entire equity derivatives market.

How often is the Nifty 50 index rebalanced?

Semi-annually, using data from six-month periods ending January 31 and July 31 each year. Resulting changes take effect in late March and late September with at least 4 weeks of advance notice. Off-cycle changes can occur for extraordinary events like mergers or regulatory actions.

Does Nifty 50 inclusion always lead to better stock returns?

Not necessarily. Research shows that most price appreciation is front-loaded before formal inclusion, as markets anticipate the event. Similarly, most price decline occurs before exclusion — stocks removed from the index have sometimes delivered stronger returns post-exit as companies refocus on fundamentals.