Introduction

When a founder shortlists banks for their IPO, the prospectus cover page can look deceptively simple — lead manager here, co-lead there, a row of co-managers below. The names are familiar. What each firm actually owns in the deal is rarely clear.

That ambiguity has consequences. Signing mandates without understanding the hierarchy means you may over-compensate banks for passive roles, under-leverage banks that could drive real distribution, or structure a syndicate that looks broad but delivers narrow reach.

That narrow reach often traces back to one role: the co-lead manager. It carries real execution weight — book-building responsibilities, investor outreach, pricing input — yet founders routinely treat it as a ceremonial credit. That's a structural mistake with direct distribution consequences.

This article explains what a co-lead manager is, how the role differs from a lead manager and a plain co-manager, and what the equivalent structure looks like in India under SEBI's BRLM framework — so you can build a syndicate around actual investor reach, not cover-page optics.

Key Takeaways

- A co-lead manager holds a senior syndicate position — below the lead bookrunner, above plain co-managers — with real distribution, research, and compliance responsibilities

- A co-lead doesn't control bookbuilding or set final pricing, but carries a meaningful share allocation and active execution duties — unlike plain co-managers who play a more passive role

- In India, this role is formally recognised as co-BRLM under SEBI's ICDR Regulations

- Issuers appoint co-lead managers to widen investor reach and distribute underwriting risk — not as a prestige signal

- Syndicate structure directly affects oversubscription quality, institutional demand, and post-listing price stability

What Is a Co-Lead Manager in an IPO?

A co-lead manager is an investment bank that holds a formally recognised, senior-tier position in the IPO underwriting syndicate. It sits directly below the lead bookrunner (called the Book Running Lead Manager, or BRLM, in India) and above the co-managers who make up the rest of the syndicate.

The "co-lead" designation signals shared lead-level responsibility for specific parts of the deal — not equal authority across the board, but meaningful ownership of defined functions: distribution targets, investor segment coverage, and sometimes research obligations.

Co-Lead vs. Joint Lead: An Important Distinction

Two different arrangements often get confused:

- Co-lead manager: One bank holds primary lead status; the co-lead sits in a senior-but-subordinate position with defined responsibilities

- Joint lead managers / joint bookrunners: Two or more banks share equal authority, economics, and league-table credit with no hierarchy between them

These are structurally different agreements. A founder who thinks they're appointing a joint bookrunner but signs a co-lead mandate ends up with an asymmetric arrangement that may not reflect what was negotiated.

Co-Lead Is Not the Same as Co-Manager

This is the most common source of confusion, and it matters for fee negotiations.

A co-lead manager takes on execution responsibilities : distribution targets, investor outreach, prospectus sign-off, and sometimes research coverage. A co-manager plays a largely passive role: distributing shares to their existing client base, excluded from bookbuilding, with smaller fee entitlement and no stabilisation duties.

Where the Co-Lead Appears on the Prospectus

The co-lead manager is listed on the cover page of the DRHP and RHP, typically in the second position after the lead bookrunner. In India, they appear under the designation "co-BRLM." Globally, the informal term "lead-right" is sometimes used.

That position isn't ceremonial. Tombstone placement reflects economics and accountability — which is why it's worth scrutinising carefully when comparing competing mandates.

The IPO Underwriting Syndicate: Where the Co-Lead Manager Fits

The IPO syndicate is a structured hierarchy, not a flat group of participating banks. Each tier carries different authority, fee entitlement, and distribution obligations.

| Syndicate Tier | Primary Role | Key Responsibilities |

|---|---|---|

| Lead Bookrunner / BRLM | Controls the book, sets pricing | Due diligence, DRHP, roadshow, stabilisation |

| Co-Lead Manager / Co-BRLM | Senior distribution role | Assigned investor segments, roadshow participation, prospectus sign-off |

| Co-Manager | Passive distribution | Shares placed with existing clients; no bookbuilding access |

| Syndicate Member | Selling group only | Distribution to client base; selling concession only |

The Lead Bookrunner's Position

The lead BRLM owns the book — the live record of investor demand across QIB, NII, and retail categories. They set the pricing recommendation in consultation with the issuer, coordinate the roadshow, oversee DRHP preparation, and bear primary regulatory accountability for disclosures. Their name appears first (upper-left) on the prospectus cover. In fee terms, they take the largest share.

The Co-Lead Manager's Position

The co-BRLM is assigned a defined slice of the distribution target. In practice, this often means leading investor outreach in a specific geography or investor segment where their relationships run deeper than the lead bank's — for example, stronger NII/HNI reach in certain regions, or deeper connections with sector-specific FPIs.

They participate in roadshow meetings with their own investor relationships, are signatories on the offer documents, and share due diligence liability with the lead.

Why the Syndicate Creates Value

Each layer of the syndicate earns its place through what it adds to the deal:

- Reaches investor segments the lead bank cannot cover alone

- Spreads underwriting risk so no single firm is overexposed to the issue

- Generates research coverage from multiple analyst teams, increasing institutional awareness before and after listing

Academic research by Hu and Ritter (2007) found that underpricing decreases by approximately 1% per additional bookrunner, as issuers gain improved bargaining power and better price discovery with multiple firms competing on execution.

Co-Lead Manager vs. Lead Manager vs. Co-Manager: Key Differences

| Dimension | Lead Manager / BRLM | Co-Lead / Co-BRLM | Co-Manager |

|---|---|---|---|

| Bookbuilding authority | Full control — owns the book | Defined participation, no book control | Excluded entirely |

| Pricing decisions | Sets the price band recommendation | Participates in discussion, no final authority | No involvement |

| Distribution obligation | Largest share allocation | Meaningful defined allocation | Smaller residual allocation |

| Prospectus sign-off | Signatory — full liability | Signatory — full liability | Not a signatory |

| Roadshow role | Chairs and coordinates | Active participant with own investor meetings | Minimal or none |

| Research obligation | Yes (market convention) | Yes — expected, not SEBI-mandated | Primary reason for inclusion globally |

| Fee entitlement | Largest portion | Meaningful, below lead | Smaller formulaic share |

A Note on Fee Economics

In US markets, the gross underwriting spread typically runs 6–8%, structured across three components:

- Management fee: ~20% of gross spread

- Underwriting fee: ~20% of gross spread

- Selling concession: ~60% of gross spread

In joint bookrunner arrangements, each bookrunner typically receives 30–40% of total gross spread revenue, according to Hu and Ritter's 2007 research on US IPO underwriting economics.

Indian fee structures are privately negotiated. SEBI mandates disclosure but sets no caps, which creates information asymmetry for issuers. Understanding global benchmarks helps calibrate expectations even when Indian norms diverge significantly.

Joint BRLMs: When Two Banks Share Equal Status

The Hyundai Motor India IPO (DRHP filed June 2024) illustrates this directly. It appointed five BRLMs — Kotak Mahindra Capital, Citigroup, HSBC Securities, J.P. Morgan India, and Morgan Stanley India — all with equal designation and equal regulatory status. No informal hierarchy existed; a detailed inter-se allocation of responsibilities was documented in the DRHP.

In that structure, no single bank controlled pricing or held primary accountability. When one bank clearly leads and another plays a secondary role, those responsibilities are concentrated — which is precisely what separates a true joint BRLM arrangement from a lead-plus-co-lead structure.

What Does a Co-Lead Manager Do? Key Responsibilities

Distribution and Investor Outreach

The co-lead is assigned a specific share allocation and is responsible for identifying, engaging, and converting investors in their designated segments. This isn't passive. They bring their own investor relationships to roadshow meetings and are held to distribution targets, not just invited to observe.

In India, this often means a co-BRLM with stronger HNI or NII relationships covering that segment while the lead bank focuses on institutional QIB demand.

Research Coverage

In many IPOs, co-lead managers initiate research coverage after listing. Independent analyst coverage from multiple banks increases institutional awareness and supports post-listing liquidity.

SEBI's ICDR Regulations do not impose a formal obligation on BRLMs or co-BRLMs to initiate or maintain research coverage after listing. Neither the SEBI (Research Analysts) Regulations 2014 nor any identified SEBI circular creates this requirement.

Post-IPO research coverage remains a market convention and a negotiation point. Issuers who want it need to address it in their engagement letters — not rely on regulatory backing.

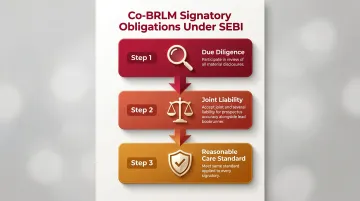

Documentation and Regulatory Accountability

Co-lead managers are signatories on both the DRHP and RHP. As signatories, they are required to:

- Participate in due diligence and review all material disclosures

- Accept joint and several liability for prospectus accuracy — alongside the lead bookrunner

- Meet the same reasonable care standard that applies to every signatory

This is a materially higher standard than co-managers face. SEBI enforcement precedent confirms this: in the Atherstone Capital Markets matter, SEBI held a merchant banker liable for information that should have been known through reasonable care. That standard applies to every signatory, including co-BRLMs.

When Should an Issuer Appoint a Co-Lead Manager?

Large or Complex Deals

When deal size makes it impractical for one bank to cover all investor segments credibly, adding a co-BRLM extends reach without fragmenting authority. For SME IPOs, a single BRLM often suffices. Main Board listings — particularly those targeting multiple investor categories simultaneously — more commonly involve a co-BRLM structure.

Strategic Investor Targeting

If your primary lead bank has deep QIB relationships but limited HNI distribution, appointing a co-BRLM with stronger NII reach is a deliberate distribution strategy — not a prestige move.

The question to ask: does this bank bring investor relationships we cannot access through our lead? If yes, the appointment adds value. "They're well-known" is not sufficient justification.

S45's Approach to Syndicate Decisions

That decision framework is only as reliable as the demand data behind it. S45 runs demand mapping before syndicate expansion decisions are made. The Demand Thesis (delivered within 24 hours of receiving inputs) provides cohort-level visibility into demand by investor category (QIB sub-segments, NII large/small, retail), geography, and sector-specific investor appetite. Only cohort-level signals are shared pre-mandate; specific investor identities are never disclosed at this stage.

That mapping determines whether a co-BRLM appointment genuinely adds distribution coverage or simply adds coordination overhead. Knowing when to expand the syndicate — and when to keep it lean — is what shapes subscription quality, not syndicate size.

S45's 26 executed IPOs have averaged 168x subscription and a 43% listing pop. For issuers evaluating syndicate structure, that record reflects what disciplined demand-driven decisions produce.

Co-Lead Managers in India: SEBI Regulations & the BRLM Framework

What SEBI Actually Requires

Under Regulation 23(1) of SEBI's ICDR Regulations 2018 (last amended March 8, 2025), issuers must appoint one or more SEBI-registered merchant bankers as lead managers. In book-built issues, these appointees act as BRLMs per Regulation 2(1)(cc).

When multiple BRLMs are appointed, Regulation 23(2) mandates that the rights, obligations, and responsibilities of each lead manager be predetermined and disclosed in the offer document per Schedule I. This inter-se allocation must cover:

When multiple BRLMs are appointed, Regulation 23(2) mandates that the rights, obligations, and responsibilities of each lead manager be predetermined and disclosed in the offer document per Schedule I. This inter-se allocation must cover:

- Capital structuring and offer document drafting

- Intermediary selection and marketing coordination

- Post-issue activities and compliance obligations

Is "Co-BRLM" a Formal SEBI Term?

The SEBI ICDR Regulations 2018 do not formally define "co-BRLM." That said, Schedule XIII (Format of Advertisements for Public Issue) explicitly uses the heading "LEAD MERCHANT BANKERS / BOOK RUNNING LEAD MERCHANT BANKERS / COBOOK RUNNING LEAD MERCHANT BANKERS" — confirming regulatory recognition of the designation in prescribed formats.

The practical implication: all appointed BRLMs carry equal regulatory liability regardless of informal market designations. Appointing a co-BRLM does not reduce that firm's liability exposure.

One Common Misconception on BRLM Caps

The commonly cited thresholds capping the number of BRLMs by issue size (e.g., 2 BRLMs for issues up to ₹50 Cr) originate from the SEBI (Merchant Bankers) Regulations, 1992 — not the 2018 ICDR Regulations. The 2018 ICDR framework does not contain issue-size-linked BRLM caps. Issuers should verify current operative provisions under both regulatory frameworks when structuring their syndicate.

India vs. Global Terminology

| Aspect | India (SEBI Framework) | Global Convention |

|---|---|---|

| Designation | Co-BRLM (Schedule XIII recognised) | Co-lead manager / lead-right |

| Regulatory basis | SEBI ICDR Regulations 2018 | Informal market convention |

| Liability | Equal to lead BRLM — joint and several | Varies by jurisdiction |

| Documentation | Must appear in DRHP/RHP inter-se allocation | Deal-specific agreement |

For Indian issuers working with global banks in a syndicate, the terminology gap has real consequences. A global bank using "co-lead" informally still carries full SEBI regulatory obligations once appointed as a BRLM — the cover page label does not limit liability. Confirm each bank's inter-se allocation in the DRHP before the offer document is filed.

Frequently Asked Questions

What is a co-lead manager in an IPO?

A co-lead manager is an investment bank holding a senior position in the underwriting syndicate — below the lead bookrunner, above plain co-managers — with meaningful distribution, research, and compliance responsibilities. In India, this role is formally designated as co-BRLM and carries joint liability for prospectus disclosures alongside the lead manager.

What does a lead manager do in an IPO?

The lead manager manages the IPO book (tracking live investor demand across all categories), sets the price band in consultation with the issuer, coordinates the roadshow, oversees all syndicate members, and bears primary regulatory responsibility for the accuracy of offer documents filed with SEBI.

What is the difference between a co-manager and a lead manager in an IPO?

The lead manager controls bookbuilding and pricing decisions and is a signatory on the offer documents. A co-manager plays a distribution-only role — placing shares with their existing client base — with no bookbuilding authority, no prospectus sign-off responsibility, and a smaller formulaic fee.

What is a Book Running Lead Manager (BRLM) in an IPO?

The BRLM is the primary investment bank responsible for managing the IPO book, coordinating investor demand, recommending the offer price, and signing the DRHP. It is the most senior and accountable role in the Indian IPO syndicate, formally defined under Regulation 2(1)(cc) of SEBI's ICDR Regulations 2018.

What is the role of a lead underwriter in an IPO?

Beyond execution, the lead underwriter carries underwriting liability for unsubscribed shares and manages post-listing price stabilisation through the greenshoe mechanism when applicable. This financial exposure is what distinguishes the lead underwriter from advisors or co-managers who face no such capital commitment.

Who is the lead manager in an IPO?

In India, the lead manager is a SEBI-registered Category-I Merchant Banker, appointed by the issuer and named first on the prospectus cover page. The appointment is documented in the Merchant Banker agreement filed as part of the DRHP with SEBI.