Introduction

In India's IPO process, the 24 hours before the public subscription window opens can decide whether an issue builds momentum or struggles to fill. That window belongs to anchor investors — institutions that collectively absorb up to 60% of the QIB portion before retail bids open. Their participation (or absence) sends a signal the rest of the market reads immediately.

Most founders encounter anchor investors in DRHP disclosures without fully grasping what they do, who qualifies, or why a weak anchor book can quietly sink an otherwise well-prepared issue. This article covers SEBI's eligibility and allocation rules, the lock-in structure, and why anchor quality — not just anchor count — shapes an IPO's outcome from day one.

Key Takeaways

- Anchor investors are Qualified Institutional Buyers (QIBs) allotted IPO shares one day before public subscription opens, under SEBI ICDR Regulations introduced in 2009

- They receive up to 60% of the QIB portion, with a minimum investment of ₹10 crore per investor on mainboard IPOs

- Key roles include building market credibility, enabling price discovery, generating early demand, and reducing post-listing volatility

- SEBI requires a staggered lock-in: half the shares held 90 days, half held 30 days — effective April 2022

- Anchor book quality signals institutional conviction to the broader market before retail bidding opens

What Is an Anchor Investor in an IPO

An anchor investor is a Qualified Institutional Buyer allotted shares in an IPO one day before the public subscription window opens — at a price at or above the lower end of the price band — under the SEBI ICDR Regulations 2018 framework. The concept was originally introduced in 2009 through SEBI's Issue of Capital and Disclosure Requirements Regulations.

Who qualifies as an anchor investor:

Only QIBs are eligible. Retail investors and High Net Worth Individuals (HNIs) are explicitly excluded regardless of net worth. Eligible entities include:

- Domestic mutual funds and Alternative Investment Funds (AIFs)

- Foreign Portfolio Investors (FPIs)

- Insurance companies registered with IRDAI

- Scheduled commercial banks

- Pension funds and provident funds with minimum corpus of ₹25 crore

- National Investment Fund

- Public financial institutions

- Multilateral and bilateral development financial institutions

That restriction on eligibility matters. Because anchor status is limited to research-driven institutions, the allocation itself carries weight — every anchor commitment is a public act of institutional validation before retail bids open.

Why Anchor Investors Matter

Anchor investors primarily function as a market signal mechanism. Their commitment appears in the prospectus before the public subscription window opens, giving retail investors and other QIBs a visible data point: a regulated institution reviewed the DRHP, assessed the valuation, and approved the pricing.

That signal has measurable consequences:

- Reduces retail hesitation — a named mutual fund or FPI on the anchor list lowers perceived risk for smaller investors

- Anchors the price band — institutional commitment at or above the floor price signals that the valuation is market-tested

- Accelerates QIB bookbuilding — other institutional investors often track anchor participation before submitting their own bids

- Strengthens the DRHP narrative — a strong anchor book gives the lead manager credible demand evidence when marketing the issue

Key Roles of Anchor Investors in an IPO

Anchor investors serve three functions in an IPO, each with measurable consequences for pricing, subscription rate, and post-listing stability.

Role 1: Building Credibility and Enabling Price Discovery

When a reputed institutional investor commits ₹10 crore or more at a fixed price one day before public bidding, it sends a powerful signal to the market. This commitment indicates that a research-driven institution has reviewed the DRHP, assessed the valuation, and found it defensible — diligence most retail investors cannot independently replicate.

How anchor participation affects pricing:

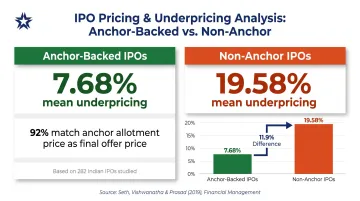

Anchor participation at or near the upper price band functions as a de facto endorsement of the issuer's stated valuation. Research by Seth, Vishwanatha, and Prasad (2019) in Financial Management analyzed 282 Indian IPOs and found that anchor-backed IPOs had mean underpricing of 7.68% versus 19.58% for non-anchor IPOs. In 92% of anchor-backed IPOs, the final offer price equaled the anchor allotment price, demonstrating that anchors effectively set the issue price.

Why this role matters:

- Price discovery backed by institutional commitment reduces the gap between issuer expectations and market acceptance

- This lowers the risk of a failed book or forced price cut at the last stage

- A weak anchor book or thin institutional participation often forces a downward price band revision, directly cutting capital raised

When this works most:

Price discovery via anchors is most critical for companies without well-established public profiles, for sectors where retail investors lack independent valuation benchmarks, and for IPOs where the price band is at a premium to listed peers.

Role 2: Generating Subscription Momentum and Retail Confidence

Because anchor allotments are disclosed before the public subscription window opens, a fully subscribed anchor book (especially one featuring marquee names like large domestic mutual funds or well-known FPIs) creates visible momentum that retail investors and HNIs observe before placing their own bids.

How this momentum effect operates:

Strong anchor books drive faster retail subscription in the first day of the public window, generating media coverage and compounding the initial institutional signal.

Real-world evidence:

Tata Technologies' November 2023 IPO raised ₹791 crore from anchor investors at the upper price band before the public window opened. The result: total subscription of 51.38x, with QIB at 203.4x, NII at 62.1x, and retail at 16.5x.

Similarly, Hyundai Motor India's October 2024 IPO — India's largest ever at ₹27,870 crore — secured ₹8,315.28 crore from anchor investors including BlackRock, Government of Singapore, and Fidelity, setting the stage for broad market participation.

Why this role matters:

- Retail investors typically cannot perform deep due diligence on an issuer's financials or growth projections

- They use anchor participation as a proxy for institutional confidence

- Weak anchors suppress retail participation even when underlying fundamentals are sound

- Strong anchor books drive faster full subscription, reducing pricing risk and improving listing outcomes

Where momentum matters most:

Momentum effects are most pronounced in uncertain market conditions, for lesser-known issuers, and for IPOs where institutional quality signals carry outsized weight relative to company brand recognition.

Role 3: Stabilizing Post-Listing Stock Price

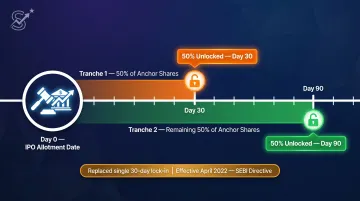

Anchor investors are required to hold their shares for a mandatory lock-in period following allotment, preventing large-block selling during the most volatile phase immediately after listing.

Current SEBI lock-in structure:

Per SEBI Notification No. SEBI/LAD-NRO/GN/2022/63 dated January 14, 2022:

- 50% of anchor shares locked for 90 days from allotment date

- 50% of anchor shares locked for 30 days from allotment date

- Effective April 1, 2022 for issues below ₹10,000 crore; July 1, 2022 for larger issues

This two-tranche structure replaced the previous single 30-day lock-in.

Why SEBI changed the lock-in rules:

Before April 2022, all anchor shares were locked for just 30 days. When lock-in periods expired simultaneously, several newly-listed stocks experienced sharp price crashes.

Zomato's anchor lock-in expiry in August 2021 triggered an 8% fall in a single session. Its pre-IPO lock-in expiry in July 2022 caused a 14% intraday crash to an all-time low.

Why this role matters:

- Staggered lock-in reduces the risk of concentrated selling events at a single expiry date

- It gives the stock time to build a wider shareholder base before large blocks can exit

- Post-listing price stability supports institutional and retail confidence beyond listing day, protecting the company's market reputation

Where stabilization matters most:

Stabilization is most critical in volatile market environments, for IPOs with high listing pops (where profit-taking pressure is strongest), and for companies needing stable share prices for future fundraises or ESOPs.

SEBI Regulatory Framework for Anchor Investors in India

SEBI's ICDR regulations set precise rules on who qualifies as an anchor investor, how much they must commit, and how many can participate in a single issue. These parameters were designed to ensure credible, concentrated pre-IPO demand rather than cosmetic sign-on.

Core Parameters

Allocation and investment rules:

- Up to 60% of the QIB portion can be allocated to anchors

- Minimum one-third of anchor allocation reserved for domestic mutual funds

- Per November 2025 amendment: anchor reservation expanded to 40%, with 33% for mutual funds and 7% for insurance companies and pension funds

- Mainboard IPOs: Minimum ₹10 crore per anchor investor

- SME IPOs: Minimum ₹2 crore per anchor investor

The number of permitted anchor investors scales with issue size:

| Issue Size | Anchor Investor Limits |

|---|---|

| Up to ₹10 crore allocation | Maximum 2 investors |

| ₹10 crore to ₹250 crore | Minimum 2, maximum 15 investors |

| Above ₹250 crore | Minimum 5; up to 15 + 10 per additional ₹250 crore* |

*Subject to minimum allotment of ₹5 crore per investor.

Pricing Mechanics (Commonly Misunderstood)

Anchor investors do not receive a discount. They are allotted shares at a fixed price within the price band. Two pricing outcomes are possible:

- Final price exceeds anchor price: Anchors pay the difference within 2 days of issue closing

- Final price is lower than anchor price: No refund — anchors pay the higher price

Pre-IPO Disclosure Rules

Anchor allocation happens one day before the IPO opens for public subscription. Names, committed amounts, and allotment price are all disclosed in the Red Herring Prospectus (RHP) filed with SEBI and the stock exchanges — meaning retail investors can review this information before placing a single bid.

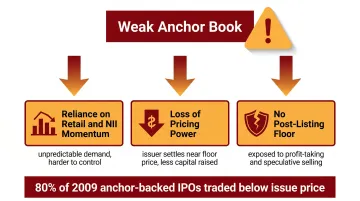

What a Weak Anchor Book Signals — and Why It Matters

A thin, poorly composed, or undersubscribed anchor book signals to the broader market that institutional due diligence either did not happen or produced no conviction. This creates hesitation among retail and non-institutional investors before the public window even opens.

When anchor quality is poor, the downstream effects are predictable:

- Lead managers are forced to rely entirely on retail and NII momentum, which is harder to predict and control

- Issuers lose pricing power at the upper end of the band, often settling near the floor

- The result: less capital raised than the offering could have supported

The data from India's own market underscores this. A 2009 Economic Times analysis found that of 5 anchor-backed IPOs that year, 4 (80%) traded below issue price — including Adani Power, Pipavav Shipyard, and Indiabulls Power, despite anchor participation from Nomura, Batterymarch, and Sundaram Mutual Fund.

As Brijesh Koshal, then Head of Investment Banking at Daiwa Securities, noted: "The presence of an anchor investor does not decide the success of an issue." What matters is the quality of anchor names, not just filling the anchor quota.

Beyond pricing, a weak anchor book creates a structural problem after listing. Without a lock-in-based institutional holding buffer, the stock has no floor during the sensitive early trading weeks — leaving it exposed to profit-taking and speculative selling from day one.

How Issuers Build a Quality Anchor Book

Building a strong anchor book starts well before the IPO opens — ideally during the DRHP preparation phase.

Early identification and engagement:

The issuer and its investment bankers identify and engage a targeted list of institutional investors whose sector expertise, investment philosophy, and AUM profile match the company's stage, size, and listing objectives. This includes:

- Long-only funds with sector-specific mandates

- Domestic mutual fund houses aligned with the issuer's growth story

- Foreign Portfolio Investors (FPIs) with India exposure

- Insurance companies and pension funds for stability-oriented allocations

- Alternative Investment Funds (AIFs) with relevant sector focus

The banker's role in institutional access:

The quality of the lead manager's institutional network directly determines which anchor investors can be approached, how pre-IPO presentations are structured, and whether the issuer gets access to the right long-term investors versus momentum-driven participants.

For example, Hyundai Motor India's IPO engaged six Book Running Lead Managers — Kotak Mahindra Capital, Citigroup, HSBC, J.P. Morgan, Morgan Stanley, and BofA Securities. This premium BRLM consortium delivered India's largest-ever anchor allocation of ₹8,315.28 crore.

What issuers must prepare for anchor due diligence:

Anchors scrutinize the DRHP carefully. Their feedback during pre-IPO management presentations often surfaces:

- Disclosure gaps

- Pricing concerns

- Use-of-proceeds questions

- Governance and compliance issues

- Operational metrics and growth drivers

Addressing these issues before filing improves the overall quality of the prospectus and reduces the risk of regulatory or investor pushback during the public subscription phase.

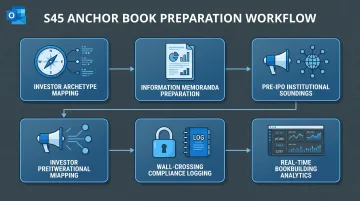

S45's approach to building anchor books:

Choosing the right lead manager shapes what that preparation actually looks like in practice. S45's AI-led readiness scans evaluate whether a company's financials, governance, and sector profile are likely to appeal to the QIBs who participate as anchors — catching gaps before they surface in front of investors.

From there, S45's anchor book work includes:

- Preparing anchor investor information memoranda tailored to each investor archetype

- Conducting pre-IPO soundings with targeted domestic and FPI institutions

- Maintaining wall-crossing logs in compliance with SEBI's Prohibition of Insider Trading (PIT) regulations

- Running real-time bookbuilding analytics to map demand and price with discipline before the anchor window opens

This structured process — from investor archetype mapping to compliant soundings — is what converts an institutional network into a disciplined anchor book rather than a list of names.

Conclusion

Anchor investors are not simply early buyers. They are institutional validators whose participation, disclosed publicly before retail bidding begins, sets the tone for pricing, subscription momentum, and post-listing stability. SEBI's 2024 study of 144 mainboard IPOs_are_sold_within_a_week.pdf) found that 54% of shares allotted to investors (excluding anchors) were sold within one week of listing — highlighting that anchor investors, constrained by lock-in periods, are structurally different from the flipping behavior prevalent among other investor categories.

The quality of the anchor book is often more consequential than its size alone. For companies preparing to list, the anchor process is one of the few variables that disciplined execution can actually control. Working with advisors who carry the right institutional relationships — and the bookbuilding rigor to assemble a credible anchor book — determines how that window is used. At S45, anchor allocation is built into the pricing and distribution mandate, not treated as an afterthought.

Frequently Asked Questions

What is an anchor book in IPO?

The anchor book is the record of institutional commitments made by anchor investors one day before the public IPO opens. It documents investor names, amounts allocated, and the allotment price — and is publicly disclosed before retail bidding begins.

Who is eligible for anchor investor?

Only Qualified Institutional Buyers (QIBs) are eligible — including domestic mutual funds, FPIs, insurance companies, scheduled commercial banks, pension funds, and AIFs. Retail investors and HNIs are explicitly excluded regardless of net worth.

What is the minimum amount for anchor investor?

The minimum investment is ₹10 crore per anchor investor for mainboard IPOs and ₹2 crore for SME IPOs, as mandated by SEBI's ICDR Regulations.

Do anchor investors get shares at a discount?

No. Shares are allotted at a price within the price band — not at a discount. If the final book-building price exceeds the anchor allotment price, the anchor investor pays the difference. No refund applies if the final price is lower.

What is the lock-in date for anchor investors?

SEBI mandates a two-tranche lock-in: 50% of anchor shares are locked for 90 days from the date of allotment, and the remaining 50% are locked for 30 days. This structure was introduced in April 2022 to prevent concentrated selling at a single expiry date.

How to check anchor book of IPO?

The anchor book is available on the NSE and BSE exchange websites and the issuer's IPO page before the public subscription window opens. Look for the Red Herring Prospectus (RHP) filing — it carries the full disclosure.