This guide walks founders and promoters through what a merchant banker actually does at each stage of the IPO process, why SEBI mandates their involvement, and what separates a merchant banker who delivers a successful listing from one who just files paperwork.

Scope: This guide covers the SEBI-regulatory definition of merchant bankers, their end-to-end responsibilities across the IPO lifecycle, due diligence obligations, pricing and bookbuilding mechanics, intermediary coordination, and the criteria founders should use when evaluating and appointing one.

Key Takeaways

- SEBI mandates at least one registered merchant banker (BRLM) for every public issue, including SME IPOs

- Two categories exist post-2025 amendments: Category I (Main Board eligible, ₹50 crore net worth) and Category II (SME and advisory only, ₹10 crore net worth)

- The merchant banker is legally accountable for every DRHP disclosure; SEBI has penalised BRLMs for failing to independently verify facts

- For SME IPOs, the merchant banker must personally underwrite at least 15% of the issue size

- Pricing discipline, not aggressive valuation, drives successful subscription and healthy listing performance

What Is a Merchant Banker?

Statutory Definition

Under Regulation 2(cb) of the SEBI (Merchant Bankers) Regulations, 1992, a merchant banker is any entity engaged in issue management—through arranging the buying, selling, or subscribing to securities, or acting as manager, consultant, or adviser in relation to such issue management.

This is distinct from a commercial bank, which takes deposits and gives loans. In global usage, "investment bank" is a broader term. In India, merchant banker is a specific SEBI-registered category — and while the two terms are often used interchangeably, they are not legally identical.

In the IPO context, merchant bankers are referred to as Book Running Lead Managers (BRLMs). A single IPO may appoint one BRLM, a Co-Book Running Lead Manager, and multiple syndicate members depending on issue size. SEBI ICDR Regulations prescribe the maximum number of lead managers_2018.pdf) based on total issue size:

| Issue Size | Maximum Lead Managers |

|---|---|

| Below ₹50 crore | 1 |

| ₹50–100 crore | 2 |

| ₹100–250 crore | 3 |

| ₹250–500 crore | 4 |

| ₹500–1,000 crore | 5 |

| Above ₹1,000 crore | 5 + 1 per additional ₹1,000 crore |

Categories of Merchant Bankers Under SEBI

SEBI's December 2025 amendments (effective January 3, 2026) introduced a new two-tier framework, replacing the legacy single-category system:

- Category I — Permitted to handle Main Board public issues, including equity IPOs and underwriting. Minimum net worth: ₹25 crore by January 2027, rising to ₹50 crore by January 2028

- Category II — Restricted from Main Board equity issues. Permitted for advisory, consulting, and SME IPO management. Minimum net worth: ₹7.5 crore by January 2027, rising to ₹10 crore by January 2028

Category III and Category IV were abolished in the 1997 amendments and no longer exist.

That distinction matters practically. Founders must verify their chosen merchant banker's category before engagement — a Category II firm cannot manage a Main Board IPO, regardless of their experience or brand.

Role of a Merchant Banker Across the IPO Lifecycle

The merchant banker's mandate begins well before the DRHP is filed—and extends past listing day.

Pre-Filing: Readiness Assessment

The pre-filing phase determines whether an IPO runs clean or stalls mid-process. The merchant banker assesses:

- Whether the company meets eligibility criteria for Main Board (NSE/BSE) or SME platforms (NSE Emerge/BSE SME)

- Gaps in corporate governance, board composition, and audit committee constitution

- Financial restatement requirements (typically three years under Ind-AS)

- Related-party transaction hygiene, cap table structure, and ESOP dilution

Companies working with S45, which executes IPOs in partnership with Narnolia as Category-I SEBI-Registered Merchant Banker, typically begin this readiness work 12–18 months before the DRHP filing. S45's 30-minute AI-powered Readiness Scan screens financial track, free float, board independence, demat readiness, statutory dues, and material litigation. It delivers a route recommendation, indicative raise range, and a prioritised fix-list before any mandate is signed.

Active IPO Process: Filing and SEBI Observation

Once the company is ready to file, the merchant banker:

- Drafts and files the DRHP with SEBI (Main Board) or the relevant stock exchange (SME)

- Submits a due diligence certificate in the format prescribed under Schedule V of the ICDR Regulations

- Manages the SEBI observation process, coordinating responses to queries and required amendments

- Coordinates across all intermediaries—registrar, auditors, legal counsel, bankers to the issue, and syndicate members

SEBI typically issues its observation letter within 30 days of receiving satisfactory responses, and the letter remains valid for one year.

Timeline expectations vary by platform: SME IPOs run 3–6 months from DRHP filing to listing; Main Board IPOs typically take 6–12 months.

Allotment and Listing

Once the subscription window closes, the merchant banker shifts from investor outreach to settlement and listing coordination:

- Oversees the basis of allotment in coordination with the registrar and stock exchange

- Ensures refunds are processed within SEBI-mandated timelines

- Manages the greenshoe or price stabilisation mechanism, if applicable

- Submits the final post-issue report and due diligence certificate within 7 days of allotment finalisation

SME IPO: Mandatory Underwriting

For SME IPOs, 100% of the issue must be underwritten, and the lead merchant banker must personally underwrite at least 15% of the total issue size. This obligation does not apply to Main Board IPOs, where underwriting is optional. The underwriting agreement must be executed before filing the RHP or Prospectus with the Registrar of Companies.

When evaluating merchant bankers for an SME IPO, founders should verify net worth, underwriting track record, and whether the banker has the balance sheet to absorb their mandatory 15% stake — not just the credentials to file the paperwork.

Due Diligence and DRHP: The Merchant Banker's Core Legal Responsibility

Due diligence is the most legally significant function a merchant banker performs. They are not merely helping prepare a document: they are certifying to SEBI and to investors that every material fact in the DRHP is accurate, complete, and not misleading.

What Due Diligence Covers

A thorough process includes:

- Independent verification of restated financial statements (three to five years)

- Examination of all pending litigation and contingent liabilities

- Verification of regulatory approvals, licences, and environmental compliance

- Scrutiny of related-party transactions cross-referenced with restated financials

- Assessment of the promoter's background, including any prior debarment or regulatory action

- Review of material contracts, key agreements, and intellectual property matters

The merchant banker must submit due diligence certificates at three stages: with the DRHP, with the RHP, and with the final Prospectus.

DRHP Drafting

The merchant banker leads preparation of the Draft Red Herring Prospectus, coordinating inputs from legal counsel, auditors, and the company secretary. The document must meet SEBI's disclosure norms under the ICDR Regulations, 2018, including:

- Restated consolidated financials for the preceding three financial years

- Internal and external risk factors prioritised by materiality

- Use of proceeds with specific allocation to identified objects

- Promoter background, shareholding pattern, and group company disclosures

Enforcement Is Not Theoretical

These drafting obligations carry direct legal consequences. In May 2025, SEBI imposed a penalty of ₹2,00,000 on Finshore Management Services Limited (FMSL), a Category I merchant banker, for failing to independently verify that a director of Presstonic Engineering had a prior criminal conviction. The offer document stated no past criminal cases existed.

SEBI's adjudication order was explicit: relying on the legal advisor's search report and the director's own undertaking does not absolve the merchant banker's independent verification obligation.

Beyond fines, SEBI may suspend a merchant banker's registration or debar them from undertaking fresh mandates.

Before appointing a BRLM, founders should check SEBI's enforcement orders database for any past actions against the prospective merchant banker.

IPO Pricing, Bookbuilding, and Investor Roadshows

Setting the Price Band

The merchant banker determines the price band through:

- Peer company valuation multiples (P/E, EV/EBITDA, P/S depending on sector)

- Assessment of the company's growth trajectory and profitability profile

- Current market conditions and sector sentiment

- Pre-IPO investor interactions with anchors and QIBs to gauge demand before the band is fixed

The price band must have a maximum spread of 20%—the cap price cannot exceed 120% of the floor price. Disciplined pricing drives stronger subscription and a healthier listing pop. An aggressively priced IPO frequently lists at a discount, damages investor confidence, and makes future capital raises harder.

Anchor Investors and Bookbuilding

Anchor investors bid one day before the public issue opens and can receive up to 60% of the QIB portion. Key parameters:

| Parameter | Requirement |

|---|---|

| Eligibility | QIBs only |

| Minimum application | ₹10 crore |

| Lock-in | 50% for 30 days; 50% for 90 days |

| Bidding timing | One working day before issue opens |

The merchant banker identifies and approaches eligible institutional investors for the anchor book. A strong anchor book is a visible signal of institutional confidence that directly influences retail and HNI demand during the main subscription window.

During the subscription period (minimum 3 working days, maximum 10), the merchant banker coordinates bid collection through syndicate members and the ASBA mechanism—the mandatory payment mechanism for all investor categories. ASBA ensures application money stays in the investor's account and is only debited upon allotment.

The quality of distribution — who you reach, and how well matched they are to the issue — determines how the book fills across all three categories. S45's investor network covers 50,000+ mapped investors across QIB, NII/HNI, and retail, each scored by mandate fit, peer holdings, roadshow attendance, win rates, and ticket size. Since July 2023, the S45 team has delivered 168x average subscription, a 43% average listing pop, and ₹1,83,000+ crore in cumulative bids across 26 IPOs.

How Merchant Bankers Coordinate Other Key Intermediaries

The merchant banker is the central coordinator of the entire IPO intermediary ecosystem. Their coordination responsibilities span:

Registrar to the Issue

The registrar handles operational processing—collecting applications, determining the basis of allotment with the stock exchange, crediting shares to demat accounts, and processing refunds. Critical rules:

- The registrar cannot be an associate of the issuing company

- A merchant banker acting as lead manager is strictly prohibited from simultaneously serving as registrar for the same issue

- The company appoints the registrar in consultation with the merchant banker

Syndicate Members and Bankers to the Issue

Syndicate members collect and upload bids into the electronic bidding system. Bankers to the issue (Self-Certified Syndicate Banks or SCSBs) handle ASBA applications—blocking funds in investor accounts and releasing them upon non-allotment.

Company Secretary and CFO

A full-time Company Secretary and CFO must be in place before the DRHP is filed. This is not optional — it is a SEBI eligibility requirement. A well-organised merchant banker flags this during the readiness phase and tracks resolution before filing begins.

This governance check typically covers board composition for independent directors, audit committee compliance under ICDR and LODR, and CS/CFO appointment status — all resolved before the DRHP clock starts.

The 2025 SEBI amendments add further restrictions: merchant bankers are prohibited from managing issues where key personnel hold significant shareholding, and from undertaking valuation activities without specific SEBI registration.

How to Choose the Right Merchant Banker for Your IPO

Choosing a merchant banker is a business decision with direct consequences for subscription quality, listing performance, and the company's long-term standing in capital markets.

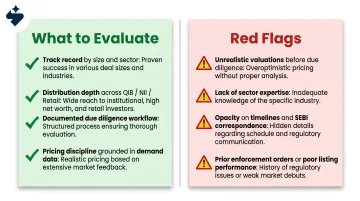

What to Evaluate

- Track record: Look at issues similar in size and sector to yours — SME-focused bankers dominate that segment; Main Board mandates concentrate among institutional names

- Distribution depth: QIB, NII, and retail participation in their previous issues reflects the strength of their actual investor network

- Due diligence process: Do they handle SEBI observations with a documented, evidence-linked workflow — or is it ad-hoc? Ask to see a sample query response

- Pricing discipline: A banker who pitches the highest valuation to win the mandate is not serving your interests

Red Flags to Watch For

- Committing to unrealistic valuations before completing due diligence

- Lack of sector-specific knowledge (a banker who doesn't understand EPC working capital cycles or cold-chain unit economics will produce a weak risk factors section)

- Opacity on documentation timelines, SEBI correspondence, or demand signals

- Prior SEBI enforcement orders or a pattern of poor listing performance

What the Landscape Looks Like

Knowing who operates in this space sharpens your shortlist. In 2025, 51 merchant bankers managed Main Board IPOs in India, with Kotak Mahindra Capital and Axis Capital among the most active by funds raised. The SME segment is dominated by specialised smaller firms — Hem Securities Limited averaged 245.41x subscription across 26 SME IPOs in 2024.

The landscape is also shifting. Platforms like S45 pair sector bankers with live AI analytics — covering demand mapping, SEBI query tracking, and post-listing IR — operating through Narnolia as Category-I SEBI-registered Lead Manager. The practical implication: SEBI registration is the floor, not the ceiling. What separates adequate from excellent is sector depth, real-time demand visibility, and execution discipline that holds from mandate signing through listing day.

Frequently Asked Questions

What are the merchant banker fees for an SME IPO?

Merchant banker fees for SME IPOs typically range from 2–5% of total funds raised, negotiated case-by-case. Total all-in costs (registrar, legal, advertising, printing) generally run 8–15% of issue size. Main Board fees run lower as a percentage — typically 1–3% — given larger issue sizes.

Is a merchant banker required for an SME IPO?

Yes. SEBI mandates at least one registered merchant banker as Book Running Lead Manager for every public issue, including SME IPOs. SME IPOs go further: the merchant banker must underwrite 100% of the issue, with the lead manager personally covering at least 15%. Main Board IPOs do not carry this underwriting requirement.

What are the key qualities of a successful merchant banker?

Strong merchant bankers bring:

- Deep sector expertise and understanding of your specific business model

- A broad institutional distribution network across QIBs, NIIs, and retail

- Disciplined due diligence with transparent documentation

- Honest pricing judgment grounded in real demand data

- Ability to manage SEBI correspondence and timelines without disrupting the promoter team

Who is the registrar in an IPO?

The registrar is a SEBI-registered entity (appointed with the merchant banker's input) who handles IPO operations: processing applications, determining allotment with the stock exchange, crediting shares to demat accounts, and processing refunds. This is a distinct role — a merchant banker cannot simultaneously serve as registrar.

What is a Category 4 merchant banker?

Category IV existed under the original 1992 classification, which divided merchant bankers into four categories. Following the 1997 amendments, Categories II, III, and IV were abolished, consolidating all registered merchant bankers into a single category. The 2025 amendments then introduced the current two-tier system (Category I and Category II). Category IV no longer exists as a regulatory category in India.

Can a company have more than one merchant banker for its IPO?

Yes. An IPO can appoint multiple merchant bankers — a BRLM and one or more Co-Book Running Lead Managers — with SEBI prescribing the maximum number based on issue size. In large IPOs, multiple BRLMs are common to expand distribution reach. The inter-se allocation of responsibilities must be clearly defined and disclosed in the offer document.