Getting it wrong isn't just a procedural problem. An underprepared anchor book, a poorly justified price band, or a list of unfamiliar institutions disclosed to the exchanges can undermine retail sentiment before a single public bid is placed. The timing is fixed. Everything else — investor selection, price band defensibility, disclosure readiness — has to be built around it.

Key Takeaways

- Anchor investors receive share allotment one working day (D-1) before the IPO subscription period opens

- Only SEBI-registered QIBs — mutual funds, FPIs, insurance companies, and pension funds — are eligible

- Up to 60% of the QIB portion can be allotted to anchor investors; SEBI's November 2025 amendment reserves 40% of that anchor allocation for domestic mutual funds (33.33%) and insurance/pension funds (6.67%)

- Allotted shares face a two-tier lock-in: 50% for 30 days, remaining 50% for 90 days from allotment

- A well-composed anchor book — with named mutual funds and insurers at the table — directly influences retail and HNI subscription behaviour in the days that follow

Why Anchor Allotment Timing Is Critical in an IPO

Anchor allotment is the first public signal of institutional conviction. Before retail investors place a single bid, the market already knows which institutions committed capital, at what price, and in what volume. That information shapes everything that follows.

The Signalling Effect Is Documented

Academic research confirms what practitioners already know. A study published in the IIMB Management Review examining 135 Indian IPOs (2009–2014) found that anchor investor participation creates measurable value for issuing firms — and that retail investors "overwhelmingly subscribe to the IPOs backed by anchor investors." A separate study in the International Review of Finance (2025) added that anchor investors "bring credibility to IPO firms, thereby enabling more firms to go public."

When anchor allotment details are disclosed to stock exchanges before the public subscription opens, retail and HNI investors read the list before placing bids. A strong anchor book from recognisable institutions drives higher subscription. A thin one, or one filled with unfamiliar names, can suppress it.

The Irrevocability Factor

Unlike public subscribers, anchor investors cannot withdraw their bids after allotment. Their capital commitment is locked in before the market reacts — which reduces pricing uncertainty for the issuer and signals to the broader market that sophisticated institutions have validated the valuation at or near the upper end of the price band.

That irrevocability cuts both ways. A full commitment at the upper end of the band is a vote of confidence. A book filled only at the lower end — or one that barely reaches the required threshold — tells the market the same story, just in the opposite direction. Which is why what happens when anchor quality is poor matters as much as when it goes well.

What Happens If Timing Is Misaligned

If anchor allotment is rushed without the right investor mix, the disclosed list can generate scepticism rather than confidence. A low-quality or incomplete anchor book doesn't just fail to signal conviction — it signals the absence of it. The downstream effects are predictable:

- Subscription multiples fall across QIB, NII, and retail categories before the window closes

- HNI and grey market participants reprice expectations downward

- The issuer loses negotiating leverage on final allocation decisions

Anchor quality isn't a formality. It sets the baseline from which every subsequent investor category makes their decision.

The Exact Timeline: When Are Shares Allotted to Anchor Investors?

The D-1 anchor allotment requirement is codified in Schedule XI of the SEBI (ICDR) Regulations, 2018, which states: "The bidding for Anchor Investors shall open one day before the issue opening date."

This single rule anchors (no pun intended) the entire pre-issue sequence. Here is how that plays out in practice:

The Full Sequence

The IPO timeline leading to anchor allotment follows this order:

- **DRHP filing and SEBI clearance** — no anchor process can begin without regulatory approval

- RHP filing and price band announcement — the price band must be formally disclosed before anchors are invited to bid

- Anchor bidding day (D-1) — the BRLM and issuer invite bids from eligible QIBs; the BRLM finalises allocations the same day

- Mandatory exchange disclosure — investor names, share quantities, and allotment price are disclosed to the stock exchanges before the next market session opens

- Public subscription opens (D) — retail, HNI, and QIB bidding begins the following working day

Both Main Board and SME IPOs follow this same D-1 structure under Schedule XI. The differences lie in thresholds, not timing.

In Main Board IPOs

- Minimum bid size: ₹10 crore per anchor investor

- Allotment price equals the IPO price; if the final book-built price is higher, anchors pay the difference

- No refund is issued if the final price comes in lower than the anchor allocation price

- Anchor allotment day is a dedicated working day preceding the three-day public subscription window

In SME IPOs

- Minimum bid size: ₹1 crore per anchor investor — verify the current figure with your merchant banker, as the November 2025 amendment revised certain thresholds

- D-1 allotment and mandatory exchange disclosure rules apply identically to SME issues

- Smaller anchor books still drive retail confidence — a fully subscribed anchor tranche tells the market the issue has institutional backing before Day 1 bidding opens

What Must Be in Place Before Anchor Allotment Day

The anchor allotment day itself is a one-day window. The preparation for it takes weeks.

Regulatory Prerequisites

The RHP must be filed and SEBI must have cleared the IPO before anchor allotment can proceed. Any gap in disclosure, documentation, or compliance at this stage delays the entire process — and by extension, the public subscription opening.

The price band must also be formally announced before anchor investors are invited to bid. Issuers who arrive at anchor day without a defensible, well-researched band risk anchors bidding at the floor — or declining to participate altogether.

The BRLM's Role in Curating the Anchor Book

The quality of institutions in the anchor book matters as much as filling the quota. Factors that determine anchor book quality include:

- Reputation and AUM of the participating institutions

- Sector expertise — a sector-specialist fund anchoring an IPO carries more weight than a generalist

- Holding behaviour post-listing — long-only funds that hold through volatility send a different signal than opportunistic participants

- Diversity across QIB sub-categories — mutual funds, FPIs, insurance companies, and pension funds each bring different credibility signals to different investor audiences

Building this kind of book requires systematic coverage, not just warm contacts. S45 maps 50,000+ investors across QIB sub-categories — domestic mutual funds, FPIs, insurance companies, and pension funds — scored by mandate fit, sector relevance, recent roadshow behaviour, and ticket bands. Across 26 IPOs executed since July 2023, this approach has contributed to a 168x average subscription and ₹1,83,000+ crore in cumulative bids generated.

Internal Readiness

Anchor allotment day is effectively a compressed institutional roadshow. Management must be ready to answer diligence questions, engage with investors on fundamentals, and demonstrate confidence in the company's financials — all within a single working day.

That means structured investor memoranda prepared in advance, wall-crossing documentation per SEBI PIT regulations, and a management team briefed on likely questions from each anchor category — before the day begins.

What Can Go Wrong with Poor Anchor Allotment Timing

Weak Anchor Books Signal Weak Conviction

If anchor allotment is not fully subscribed — or if the disclosed list includes unfamiliar or low-credibility institutions — retail and HNI investors draw the obvious conclusion: large institutions don't believe in the valuation. That inference can suppress subscription across all categories, compressing demand precisely when the issuer needs it most.

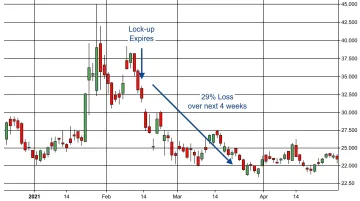

Lock-In Expiry Dates Are Predictable Sell-Off Triggers

If the IPO is overpriced at the anchor stage, the 30-day and 90-day lock-in expiry dates become predictable sell-off triggers. The evidence from recent Indian IPOs is consistent:

| Company | Lock-In Type | Expiry | Price Decline |

|---|---|---|---|

| Ola Electric | 30-day | Sep 6–9, 2024 | ~4% |

| Ola Electric | 90-day | Nov 5, 2024 | ~9% |

| Bajaj Housing Finance | 30-day | Oct 16, 2024 | ~4% |

| Bajaj Housing Finance | 90-day | Dec 12, 2024 | ~6.2% |

Forbes India reported that 66 companies faced lock-in expiries in early 2024, with a potential $21.1 billion withdrawal risk. CFOs and IR teams that anticipate these windows — with pre-prepared communication on business performance and valuation support — absorb the sell-off impact better than those caught flat-footed.

Compliance Risk Can Derail the Entire Issue

Financial risk isn't the only exposure. Process failures carry their own consequences:

- Non-disclosure before opening: Anchor allotment details must be published before the IPO subscription window opens — any gap triggers SEBI review

- Timeline deviations: Allotment on any day other than T-1 (one day before the issue opens) violates SEBI ICDR Regulations and can draw formal observations

- Serious breaches: Repeated or material non-compliance can delay or cancel the offering entirely

Key SEBI Rules Governing Anchor Allotment

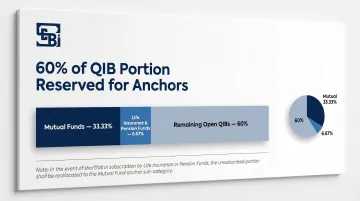

Allocation Limits

Up to 60% of the QIB portion can be reserved for anchor investors. SEBI's November 2025 amendment (effective November 30, 2025) restructured the sub-allocation framework:

| Category | Reservation (of Anchor Portion) |

|---|---|

| Mutual Funds | 33.33% |

| Life Insurance + Pension Funds | 6.67% |

| Total Reserved Block | 40% |

| Remaining Open | 60% |

If the insurance/pension allocation (6.67%) is not fully subscribed, the shortfall is redirected to mutual funds. The remaining 60% of the anchor portion is available for other eligible QIBs.

Investor Count Rules

Following the November 2025 amendment:

- Up to ₹250 crore anchor portion: Minimum 2, maximum 15 anchor investors

- Above ₹250 crore: 15 additional investors permitted per subsequent ₹250 crore tranche

- Minimum allotment per anchor investor: ₹5 crore

Category I and Category II FPIs have been consolidated into a single FPI category, simplifying participation for global fund managers running multiple investment vehicles under one structure.

These count rules directly shape the lock-in schedule that follows — because each investor's allotment ties to a specific tranche date.

Two-Tier Lock-In Structure

- First 50%: Locked in for 30 days from the allotment date

- Remaining 50%: Locked in for 90 days from the allotment date

No anchor shares enter the secondary market before the 30-day window closes. After that, tranches unlock on separate dates — which is why post-listing anchor exit dates appear on institutional calendars as discrete events, not a single sell-off risk.

Conclusion

Anchor allotment is fixed at one working day before the IPO opens. But the real work — selecting the right investors, finalising a defensible price band, completing every disclosure and regulatory requirement — happens in the weeks before that date.

Timing is only one variable. The quality of the anchor book, the credibility of the institutions on it, and the discipline of the pricing together determine whether anchor allotment strengthens or complicates the IPO's market entry.

A strong anchor book from recognisable, sector-relevant institutions sets a positive tone that carries through the retail subscription window. A weak one signals hesitation to the market — dampening QIB demand and putting pressure on the listing price before retail bidding even opens.

Frequently Asked Questions

What is anchor allocation in an IPO?

Anchor allocation refers to the reservation of up to 60% of the QIB portion of an IPO for large institutional investors, who receive shares one working day before public subscription opens. In exchange for this confirmed allotment, they commit capital at a fixed price and are subject to mandatory lock-in periods.

When exactly are shares allotted to anchor investors in India?

Shares are allotted on D-1 — the one working day immediately before the IPO subscription period opens to the public. Allotment details, including investor names, share quantities, and allotment price, must be disclosed to stock exchanges before the next market session begins.

What is the lock-in period for anchor investors after allotment?

50% of allotted shares are locked in for 30 days from the allotment date; the remaining 50% are locked in for 90 days. Anchor investors cannot sell any shares until the 30-day period expires.

Can anchor investors cancel or withdraw their bids after allotment?

No. Unlike public subscribers, anchor investors cannot withdraw bids or cancel allotments once shares have been allocated. Their commitment is binding from the moment allotment is finalised on D-1.

How does anchor investor allotment affect retail investor sentiment?

Because allotment details are publicly disclosed before the IPO opens, retail and HNI investors treat the anchor book as an early read on institutional conviction. When marquee domestic funds and FPIs anchor at the full price, retail subscription tends to follow. A thin or unknown anchor list tends to suppress demand before the subscription window even opens.

What is the difference between anchor investors and regular QIBs in an IPO?

| Anchor Investors | Regular QIBs | |

|---|---|---|

| Bidding window | One day before IPO opens (D-1) | During normal subscription period |

| Allotment basis | Confirmed at the time of bidding | Proportionate, based on total QIB demand |

| Lock-in requirement | Mandatory (30 days / 90 days split) | None |