Introduction

A market maker in an SME IPO is a SEBI-registered trading member who provides continuous two-way (buy and sell) quotes to ensure liquidity in listed SME shares. This role does not exist for large-cap listings — it exists precisely because SME stocks face structural liquidity challenges that larger exchanges don't.

Lower institutional participation, smaller free float, and thin trading volumes leave SME shares prone to illiquidity after listing. That can trap retail investors in positions they cannot exit and severely damage a company's post-listing credibility.

Between 2022 and 2024, SME IPOs in India surged from 109 listings raising ₹1,874.85 crore to 240 listings raising ₹8,760.89 crore — a 120%+ increase in just two years. The numbers are impressive. The underlying fragility is not.

Approximately 65% of 2024 SME listings currently trade below their issue price. Another 10–12% of SME-listed companies face trading suspensions due to non-compliance. Market makers are the regulatory mechanism designed to keep these problems from becoming worse — and for SME founders, understanding how that mechanism works is not optional.

This article breaks down what market makers actually do, why SEBI mandates them specifically for SME listings, and how the process works from pre-IPO setup through post-listing operations. It also covers what founders need to understand before appointing one.

Key Takeaways

- Market makers inject liquidity into SME shares by continuously quoting both buy and sell prices

- SEBI mandates market making for at least 3 years from listing on NSE Emerge and BSE SME

- Issuers must reserve 5% of the IPO size for the market maker as initial inventory

- Income comes from the bid-ask spread and an issuer-paid upfront fee — not from price performance

What Is a Market Maker in SME IPO?

A market maker is an individual or firm registered with SEBI and enrolled as a trading member on NSE or BSE's capital market segment. Their job is to continuously quote bid (buy) and ask (sell) prices for a specific SME security — so retail investors can always find a counterparty to trade, even when organic market activity is thin.

Key distinctions:

- Market Maker vs. Broker: A broker routes orders between parties. A market maker holds inventory and acts as the direct counterparty, buying from sellers and selling to buyers from their own stock.

- Market Maker vs. Underwriter: An underwriter guarantees the IPO subscription before listing. A market maker supports liquidity after listing.

In practice, the market maker absorbs one-sided order flow that would otherwise leave a retail investor stuck — unable to exit a position or enter one. That's what makes the role structurally critical for SME-listed companies, where trading volumes are naturally lower than on the Main Board.

Why SME IPOs Require a Market Maker

SME stocks face a core liquidity problem that mainboard listings rarely encounter. Unlike large-cap companies with deep institutional ownership and broad retail participation, SME stocks have a limited float, fewer institutional investors, and smaller trading communities. Left alone, many SME shares go days or weeks with zero trading volume after listing.

SEBI mandates market making under Regulation 106V of the SEBI ICDR Regulations (now Regulation 261 under the 2018 framework), making it a regulatory requirement for all SME listings on NSE Emerge and BSE SME. This obligation runs for a minimum of 3 years from the date of listing.

What goes wrong without market making:

- Investors who received allotments cannot exit their positions

- Prices become susceptible to extreme manipulation by any single large seller or buyer

- Post-listing credibility suffers, deterring future institutional interest

- Compliance failures and trading suspensions become more likely

These risks are what make market making structurally necessary for SMEs — not optional. Mainboard IPOs attract sufficient institutional and retail liquidity organically, so SEBI reserves this mandatory obligation for the SME segment where liquidity cannot be assumed.

How Market Making Works: From IPO to Post-Listing

The market-making lifecycle begins before listing. The issuer, merchant banker, and market maker sign a formal agreement upfront, with active daily quoting obligations running for at least 3 years post-listing.

Before Listing: The Setup Phase

The merchant banker leading the SME IPO is responsible for ensuring market-making arrangements are in place before the DRHP is filed. The market maker's identity and the terms of the agreement must be disclosed in the offer document.

At S45, this coordination begins before DRHP drafting starts. The team shortlists eligible market makers, aligns obligations with exchange rules, and integrates the market maker's role into the broader post-listing liquidity plan.

5% Share Reservation:

The issuer must allot at least 5% of the total IPO issue size to the designated market maker(s) at the time of allotment, providing them with the initial inventory needed to begin trading.

Example: If an SME IPO consists of 10,00,000 shares, at least 50,000 shares are reserved for the market maker.

After Listing: Day-to-Day Operations

Every trading day, the market maker must quote both a bid price and an ask price for at least 75% of the session. Quotes must cover a minimum depth of ₹1,00,000 worth of shares and at least one trading lot, with guaranteed execution at the quoted price and quantity.

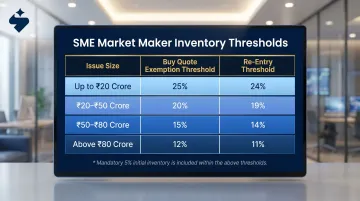

Inventory Management

Market makers hold the initial 5% stock allocation, adjusting positions throughout the session by buying from sellers and selling to buyers. If holdings cross SEBI-specified thresholds — which vary by issue size — the market maker is temporarily exempt from quoting buy prices until inventory normalizes.

Inventory Thresholds by Issue Size:

| Issue Size | Buy Quote Exemption Threshold | Re-Entry Threshold |

|---|---|---|

| Up to ₹20 crore | 25% | 24% |

| ₹20 to ₹50 crore | 20% | 19% |

| ₹50 to ₹80 crore | 15% | 14% |

| Above ₹80 crore | 12% | 11% |

These thresholds include the mandatory 5% initial inventory. When inventory crosses the exemption threshold, market makers can pause buy quotes; when it falls below the re-entry threshold, two-way quoting must resume.

How Market Makers Earn Revenue

Market makers earn income from two primary sources:

1. The Bid-Ask Spread:

The market maker profits from the difference between the price they buy at and the price they sell at. SEBI caps the spread at no more than 10% of the sale price, with tiered limits by price band specified by NSE Emerge:

| Share Price Band (₹) | Maximum Permissible Spread |

|---|---|

| Up to ₹10 | 10% |

| Above ₹10 to ₹20 | 8% |

| Above ₹20 to ₹50 | 6% |

| Above ₹50 to ₹100 | 5% |

| Above ₹100 | 4% |

2. Upfront Market-Making Fee:

The issuer pays a fee to the market maker covering the mandatory 3-year period.

Key risk: If the stock price falls below the market maker's acquisition cost, the market maker can incur losses. Market makers provide liquidity — they do not carry guaranteed returns.

Key SEBI Rules and Obligations for SME Market Makers

Eligibility Criteria

Per SEBI Circular CIR/MRD/DP/14/2010, any entity seeking to act as a market maker must meet all of the following conditions:

- Must be a registered trading member of the capital market segment of NSE or BSE

- Must hold a minimum net worth of ₹1 crore (tiered upward for market makers managing multiple companies)

- Must complete a one-time registration with the exchange before commencing market-making activity

Operational Obligations

- Maintain two-way quotes for 75% of trading hours

- Quote for a minimum depth of ₹1,00,000

- Purchase the entire shareholding of a shareholder in one lot if that holding is worth less than ₹1 lakh (to protect small investors who cannot sell partial lots)

Restrictions

- Cannot purchase shares from promoters or promoter group members during the 3-year compulsory market-making period — and promoters are equally prohibited from selling to market makers (Regulations 106V(6) and 106V(7))

- Cannot re-enter the buy side once inventory exceeds the exchange-defined threshold; must wait until holdings fall back within limits

Scale and Appointment

These rules also govern how many market makers a company can engage and what happens when one exits.

- A company may appoint between 1 and 5 market makers

- Voluntary withdrawal after the 3-year period requires at least one month's advance notice to the exchange

- The merchant banker must appoint a replacement within one month of any withdrawal to ensure continuity

Common Misconceptions About Market Makers in SME IPOs

Misconception #1: "Appointing a market maker protects my stock price"

Market makers are not price guarantors. Their obligation is to provide liquidity — meaning there is always a buyer and seller available — not to prevent the share price from falling. If the company underperforms, the stock can decline sharply regardless of the market maker's presence. Price protection is simply not part of the mandate.

Misconception #2: "The market maker will stabilize my stock post-listing"

Market makers provide the mechanism to trade — not a floor price. What actually drives post-listing price performance is strong fundamentals, transparent communication, and consistent investor relations. The market maker ensures your stock can be bought or sold; it cannot ensure the price holds.

Misconception #3: "Once I have a market maker, liquidity is sorted"

Market maker obligations are time-bound — typically three years under SEBI's SME framework. Once that period ends, the company must attract organic trading interest on its own.

Founders who rely solely on market-making without building a post-listing IR strategy often see sharp liquidity drops after year three. The smarter approach is to use the mandatory period to:

- Build a consistent investor communication cadence

- Optimize lot sizes to attract broader retail participation

- Develop relationships with analysts and institutional investors who can sustain long-term trading interest

Frequently Asked Questions

Who is the market maker in SME IPO?

A market maker in an SME IPO is a SEBI-registered trading member with a minimum net worth of ₹1 crore — typically a brokerage firm. The issuer company appoints them in consultation with the merchant banker, and their name is disclosed in the offer document before listing.

What is the role of a market maker?

A market maker provides continuous two-way quotes for SME shares during at least 75% of every trading session. This ensures retail investors can always execute trades and that the stock maintains orderly price discovery through active supply and demand.

What is the minimum percentage reserved for market maker?

SEBI mandates a minimum reservation of 5% of the total IPO issue size for the designated market maker(s) at the time of allotment. This allocation forms their initial inventory for post-listing trading activity.

Is market making mandatory for SME IPOs?

Yes, it is mandatory under Regulation 106V (now Regulation 261) of SEBI's ICDR Regulations for all SME listings on NSE Emerge and BSE SME, for a minimum period of 3 years from the date of listing.

How do market makers earn profit in an SME IPO?

Market makers earn income through the bid-ask spread — the difference between their buy price and sell price — and through an upfront fee paid by the issuer company for the 3-year market-making service.

What is the market-making agreement in an SME IPO?

The market-making agreement is a formal contract signed before listing between the issuer company, the merchant banker, and the market maker. It covers quote obligations, spread limits, inventory thresholds, and other terms of the arrangement. A copy must be attached to the offer document filed with the SME exchange.