Introduction

The irony is brutal: SME founders spend years building their business, yet on IPO day, they frequently hand a portion of that value to first-day buyers for free. This phenomenon—IPO underpricing—represents capital that could have funded expansion, R&D, or working capital, instead flowing to traders who flip shares within hours. While a "listing pop" generates headlines and excitement, it's a symptom of a deeper problem: weak corporate governance.

For SMEs especially, corporate governance quality acts as a credibility signal to underwriters, institutional investors, and retail buyers. When governance infrastructure is weak or poorly documented, underwriters apply a larger discount to offset information asymmetry—leaving founders with far less capital than they could have raised.

Weak governance is the single biggest contributor to excessive underpricing at listing. The fix doesn't start at filing. It starts 12–24 months before.

Key Takeaways

- Poor governance forces underwriters to widen the uncertainty discount, directly increasing underpricing for SMEs

- Four governance levers narrow underpricing: board independence, audit quality, financial disclosure, and related-party transaction transparency

- Building governance infrastructure 12–24 months before filing delivers tighter price bands and stronger post-listing stability

- SEBI's SME norms set the minimum — firms that exceed them early consistently achieve better price discovery at listing

What IPO Underpricing Really Costs an SME Founder

IPO underpricing is the gap between the IPO offer price and the closing price on listing day. While a first-day surge might look like validation, it represents capital the company permanently forfeited—money that went to first-day traders, not to the company's growth plan. In India's SME segment, this problem has become harder to ignore. Average listing gains fell from approximately 60% to 12.6% in FY2024-25, while 37% of 2025 SME IPOs closed below issue price on day one versus only 9% in 2024.

The scale is material. 268 SME IPOs raised ₹12,111.55 crore in 2025, up from ₹8,760.89 crore across 240 IPOs in 2024. Even a 5-10% reduction in underpricing would return hundreds of crores to issuer balance sheets.

Not All Underpricing Is Avoidable

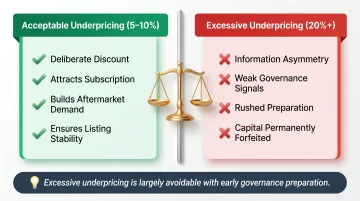

There's a distinction between acceptable and excessive underpricing:

- Acceptable underpricing is a deliberate, modest discount (5-10%) applied to attract subscription, build aftermarket demand, and ensure listing stability

- Excessive underpricing (20%+) is a symptom of information asymmetry, poor governance signalling, or rushed preparation—and it's largely avoidable

That distinction matters most for SMEs, where institutional investors have less independent data to work with. Without analyst coverage, earnings history, or peer comparables, investors rely on observable governance proxies to assess risk. Governance quality, as a result, becomes directly price-sensitive in ways that larger listed peers rarely experience.

Post-listing reality check: 65% of 2024 SME listings and 57% of 2025 listings are currently trading below their original issue price. Strong governance affects more than day-one pricing. It shapes 12-month performance and, for many SMEs, long-term survival in the public market.

How Corporate Governance Signals Directly Influence Pricing Decisions

The core mechanism is information asymmetry theory: investors and underwriters cannot fully verify an SME's true value before listing, so they use governance structure as a proxy for management quality, risk discipline, and earnings reliability. Weak governance signals higher uncertainty, which causes underwriters to widen the discount to protect investors.

Board Composition as a Pricing Signal

Board composition is the most visible governance signal. Independent directors reduce perceived risk of insider expropriation and earnings manipulation. Academic research consistently shows that director interlocking—where directors serve on multiple boards—significantly reduces underpricing across Indian IPOs. Well-connected directors act as reputational certification signals that reduce information asymmetry.

The Indian SME paradox: Contrary to large-cap markets, a 200-IPO study found that higher board independence actually increased underpricing in Indian SME IPOs. This suggests that in resource-constrained SMEs, independent directors may be perceived as costly overhead rather than investor protection. The lesson? For SMEs, director network quality and relevant industry experience matter more than independence ratios alone.

Audit Quality: The Underwriter vs. Auditor Hierarchy

Companies audited by credible firms are treated as having more reliable financials. For SMEs, upgrading from an unknown local auditor to a mid-tier or Big 4 firm ahead of the IPO should directly reduce the information discount applied to the offer price.

The data, however, complicates that assumption. In a 286-SME IPO study, auditor reputation lacked statistical significance on underpricing, while underwriter reputation had a significant positive relationship. The combined signal of both a reputable auditor and underwriter helps stabilize pricing through a negative interaction effect—but the underwriter's brand matters more than the auditor's.

Practical implication: Invest first in underwriter quality, then in audit firm selection. A strong merchant banker will require governance-clean documentation before accepting a mandate, which naturally filters for audit quality anyway.

Financial Disclosure Quality

Companies that produce clean, consistent, and forward-looking disclosures reduce investor uncertainty. Restated financials, qualified audit opinions, or thin DRHP disclosure force investors to price in the ambiguity. Three consecutive years of clean, audited financials with consistent accounting policies are the baseline—but what actually reduces underpricing is the quality and coherence of those financials.

Beyond the baseline, specific practices narrow the information discount further:

- Adopt Ind AS well before the filing year to eliminate last-minute restatement risk

- Establish an internal audit function to signal financial self-scrutiny, not just compliance

- Maintain consistent accounting policies across all three years of reported financials

- Ensure DRHP disclosures are forward-looking and internally coherent, not just regulatory boilerplate

Promoter Shareholding and Related-Party Transactions

Concentrated promoter holding with no independent checks, or high related-party transaction volumes, signal governance risk. Higher promoter retained ownership correlates with higher underpricing, interpreted as an entrenchment signal—investors demand a larger discount to compensate for the risk of promoter self-dealing.

Nearly 50% of listed SMEs report RPTs exceeding ₹10 crore, raising concerns about circular transactions and inflated financials. Unmanaged RPTs translate directly into a higher discount at pricing.

The Four Governance Levers That Reduce Underpricing

Board Structure and Independence

SMEs should aim to constitute a board that includes at least two independent directors with relevant industry or financial expertise before the DRHP is filed. Independent directors serve a dual purpose:

- They satisfy SEBI and exchange requirements

- They signal to QIBs and HNIs that management will not act unilaterally to disadvantage minority shareholders post-listing

SEBI requirements:

- At least 1/3 independent directors

- 1/2 if the Chairman is an executive director or related to the promoter

Director network effect: Firms with better-connected directors have higher IPO market valuations. Directors who serve on multiple boards bring networks that improve bookbuilding quality and investor roadshow engagement. Recruiting well-connected independent directors has direct pricing payoff.

Financial Reporting and Audit Trail

Three years of clean, audited financials with consistent accounting policies are the baseline. What separates good from great:

- No restatements or qualifications

- Clearly traceable audit trail

- Consistent accounting policies across all years

- Complete the shift to Ind AS well before the filing year

Internal audit functions signal financial self-scrutiny. Even lightweight internal controls tell investors that governance is built in, not bolted on — which matters when institutional allocators are sizing their bids.

Disclosure Quality and Risk Factor Precision

A well-drafted risk factor section in the DRHP that is specific rather than generic builds investor confidence. Investors and SEBI reviewers respond poorly to vague boilerplate risk disclosures—they increase perceived opacity.

What works:

- Specific, substantiated risk disclosures

- Clear identification of business, regulatory, and financial risks

- Commercial rationale for key operational decisions

Specificity here is a signal, not a concession — it tells the market that management understands its own business well enough to name the risks clearly.

Related-Party Transaction Governance

SMEs should conduct a structured review of all related-party transactions at least 18 months before the planned listing date. Steps include:

- Identifying all RPTs comprehensively

- Rationalizing any non-arm's-length arrangements

- Documenting commercial rationale for transactions that remain

Unexplained RPTs are among the most common reasons institutional investors discount an SME's offer price. SEBI's new materiality threshold—10% of annual consolidated turnover or ₹50 crore, whichever is lower—applies main-board standards to SMEs. SMEs that treat RPT governance as a pre-filing exercise rather than a disclosure afterthought will find institutional investors far more willing to anchor at the top of the price band.

Translating Governance Into Pricing Discipline Before Filing

Governance improvements take 12–24 months to show up credibly in disclosures and due diligence materials. A board change six weeks before filing looks cosmetic; a board reconstituted 18 months earlier with documented committee activity reads as genuine. Timing matters as much as the changes themselves.

What "Clean, Disciplined Books" Means in Pricing Terms

When the data room is organized, financials are traceable, and governance policies are documented and followed (not just printed), underwriters can narrow the price band because they carry less residual uncertainty. Chaotic documentation forces conservative pricing.

S45's AI-led readiness process catches governance gaps before they reach the data room. It builds evidence-linked drafting and a live data room that gives underwriters confidence in the issuer's numbers. Pre-validating every figure in the DRHP and anchoring projections to clear narratives reduces last-minute issues and supports disciplined pricing.

Bookbuilding Implications

QIBs who receive well-governed DRHP filings tend to anchor their bids closer to the upper end of the band, which tightens effective underpricing. A weak governance profile pushes HNIs and retail investors toward the lower end—or into waiting for the listing pop instead of bidding at issue price.

The compounding effect: Governance quality doesn't just affect day-one pricing—it affects 12-month post-listing stock performance and the ability to avoid delisting. Research shows that Indian SME IPOs exhibit long-run overperformance up to 12 months, but the pattern reverses over longer horizons for poorly-governed companies. Well-governed SMEs retain institutional interest after listing; poorly-governed ones see institutional exit and price erosion.

India's SME IPO Regulatory Context: What SEBI Expects

SEBI's governance-related eligibility and disclosure requirements for BSE SME and NSE Emerge set the floor, not the ceiling. Meeting just the minimum does not protect against underpricing.

BSE SME Eligibility Criteria

- Post-issue paid-up capital: Max ₹25 crore

- Net worth: Min ₹1 crore for 2 preceding full financial years

- Net tangible assets: Min ₹3 crore in last preceding financial year

- Operating profit: Min ₹1 crore from operations for 2 out of 3 latest financial years

- Leverage ratio: Max 3:1

NSE Emerge Eligibility Criteria

- Post-issue paid-up capital: Max ₹25 crore

- Operating profit: Min ₹1 crore for 2 out of 3 latest financial years

- Cash flow: Positive free cash flow for min 2 out of 3 previous financial years

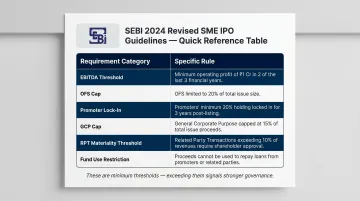

SEBI's Revised Guidelines (Effective 2024)

| Aspect | Requirement |

|---|---|

| EBITDA threshold | Min ₹1 crore in any 2 of last 3 FYs for DRHP filing |

| Offer for Sale (OFS) | Capped at 20% of issue size |

| Promoter lock-in (minimum 20% contribution) | 3 years |

| General Corporate Purposes (GCP) | Capped at 15% of issue size or ₹10 crore (whichever lower) |

| RPT materiality threshold | 10% of annual consolidated turnover or ₹50 crore (whichever lower) |

| Fund use restriction | IPO proceeds cannot repay loans to promoters/related parties |

Enhanced Scrutiny and Timeline Risk

SEBI's review process can delay or return a DRHP when governance disclosures are incomplete or inconsistent. IPO rejections dropped from 17 in FY25 to just 2 in FY26, according to a Business Standard report on SEBI's consultative approach — but common red flags still trigger scrutiny:

- Use of funds directed toward marketing expenses

- Undisclosed or irregular prior allotments

- Debt issuances with related-party linkages

- Ambiguous promoter classification

Timeline delays carry a direct valuation cost. If the market window shifts during a prolonged review, the price band set at filing may no longer reflect demand — compressing the final listing outcome.

Merchant Banker Accountability

Under SEBI regulations, the merchant banker is legally accountable for disclosures in the DRHP. A credible merchant banker will require clean governance documentation before accepting a mandate. This makes pre-IPO governance investment a prerequisite for accessing quality merchant banking relationships, not a box to check after the mandate is signed.

Frequently Asked Questions

What exactly is IPO underpricing, and is it always bad for an SME?

IPO underpricing is the gap between the offer price and listing price. Moderate underpricing (5–10%) is deliberate and helps ensure subscription success, but excessive underpricing reflects unresolved information asymmetry. That gap represents capital permanently left on the table — capital that could have funded growth instead.

How does board independence specifically affect an SME's IPO offer price?

Independent directors reduce investor-perceived risk of insider self-dealing, which allows underwriters to apply a smaller uncertainty discount when setting the price band. However, in Indian SME IPOs, director network quality and relevant experience matter more than independence ratios alone.

What is the minimum governance structure SEBI requires for an SME IPO in India?

SEBI requires a mandatory Audit Committee, at least one-third independent directors (one-half if the Chairman is an executive or promoter-related), and compliance with ICDR and LODR regulations. Sector-specific or size-specific disclosures are common — confirm requirements with your merchant banker early in the process.

How far in advance should an SME start building governance infrastructure for an IPO?

Start 18–24 months before the planned filing date, so governance changes are reflected in at least one full financial year of audited results and are clearly visible in the DRHP rather than appearing cosmetic or rushed.

Can strong governance compensate for modest financials when pricing an SME IPO?

Strong governance cannot replace revenue growth or profitability, but it meaningfully reduces the risk premium investors apply. A company with good governance and moderate financials will typically price better than one with strong financials but opaque governance.

What role does the merchant banker play in governance-linked pricing decisions?

The merchant banker conducts due diligence and is legally responsible for DRHP disclosures. Where governance documentation is incomplete, they will price conservatively or decline the mandate altogether. Arriving at due diligence with clean, organized governance records directly affects both access to quality bookbuilding and final pricing.