Introduction

Indian companies falter during their IPO journey not because their business performance is lacking, but because their governance structures simply aren't built for public scrutiny. The gap between being a good company and being a publicly listable one is wider than most founders expect — and it shows up in regulatory delays, investor skepticism, and valuation discounts that were entirely avoidable.

Corporate governance isn't just a compliance requirement to tick before filing your Draft Red Herring Prospectus (DRHP). It's a fundamental driver of IPO pricing, subscription demand, and long-term stock performance.

Board composition, audit trail transparency, related party disclosures, and risk governance maturity all send clear signals to institutional investors about whether your company is ready to operate under SEBI's ICDR and LODR requirements.

This article examines what corporate governance means in the IPO context, the specific pillars that institutional investors scrutinise, how governance directly shapes valuation and listing performance, and what founders need to do to prepare — ideally 2–3 years before filing, not in the final months before approaching SEBI.

Key Takeaways

- Corporate governance directly influences IPO pricing, subscription demand, and post-listing performance — treat it as core strategy, not compliance paperwork

- The critical pillars include board independence, audit committee quality, disclosure frameworks, and risk management policies

- QIBs and institutional investors scrutinize governance structures before committing capital, directly driving oversubscription rates

- Start building public-company-grade governance at least 2–3 years before filing — waiting until DRHP preparation is too late

- Unresolved RPTs, promoter-heavy boards, and undocumented disclosures consistently trigger SEBI observations and investor valuation discounts

What Is Corporate Governance and Why It Matters in an IPO

Corporate governance is the system of rules, practices, and processes by which a company is directed and controlled. For private companies, this system often develops informally around the founders and promoters. But when a company moves from private to public, the expectations shift dramatically. Going public means accepting accountability to shareholders, regulators, and the market — and that accountability is enforced through mandatory governance standards that aren't optional.

In India, corporate governance requirements for listed companies are defined primarily through SEBI's Listing Obligations and Disclosure Requirements (LODR) Regulations, which were first introduced in 2015 and have been amended multiple times since. These regulations specify board composition thresholds, committee structures, disclosure obligations, and compliance timelines that every listed company must meet. They're not guidelines — they're enforceable listing conditions that NSE and BSE monitor continuously post-IPO.

Governance vs. Compliance: Understanding the Difference

Compliance and governance quality are not the same thing. Compliance is the floor — meeting SEBI's minimum requirements for board independence, audit committee composition, and disclosure standards.

Governance quality determines how investors perceive and value your company. A company that merely clears SEBI's review will not command the same valuation premium as one where institutional investors trust the oversight structure, financial transparency, and leadership stability.

During bookbuilding, Qualified Institutional Buyers (QIBs) — who anchor IPO demand in India — conduct their own governance diligence, separate from SEBI's review. They evaluate:

- Whether independent directors are genuinely independent, not just nominally so

- Whether audit trails are complete and defensible

- Whether the company has a credible framework for managing conflicts of interest

Companies with weak governance may technically clear regulatory review but face muted institutional demand, pricing resistance, and weaker listing performance.

The Key Pillars of Corporate Governance That Drive IPO Success

Board Composition and Independence

Board independence is the foundational governance signal. SEBI's LODR Regulation 17 sets clear thresholds: at least one-third of the board must be independent directors when the chairperson is a non-executive non-promoter, rising to 50% independent directors when the chairperson is executive or promoter-related. Additionally, every listed company must have at least one woman director, and the top 1,000 entities by market capitalization must have at least one independent woman director.

But institutional investors look beyond these minimums. They evaluate:

- Whether independent directors are genuinely independent, not just nominally so

- The professional credentials and sector expertise of independent directors

- Whether independent directors are active in oversight or passive participants

- The size and diversity of the board relative to the company's complexity

Research supports this focus. A 2020 study by Columbia Law School and Sapienza University analyzing 1,270 European IPOs from 2000 to 2015 found that larger boards with a higher proportion of independent directors were positively associated with short-term IPO performance, as measured by Q-Tobin and Price-to-Book Value. Director quality also mattered: higher education credentials and stronger professional networks (measured by the number of other boards served) were described by the researchers as "vital" for improving IPO outcomes.

Audit Committee and Financial Transparency

The audit committee establishes investor confidence in the integrity of a company's financial statements. Under SEBI LODR Regulation 18, it must consist of a minimum of three directors, with two-thirds being independent directors.

The chairperson must be an independent director with accounting or related financial management expertise, and all members must be financially literate.

This committee's role goes beyond reviewing quarterly results. It oversees:

- Internal controls and the external audit process

- Related party transaction approvals

- Risk management frameworks

A strong audit committee signals to investors that the company's numbers can be trusted and that oversight sits clearly separate from management.

Audit firm selection carries real weight. Engaging a Big Four or reputable national audit firm before IPO filing sends a powerful credibility signal. Research across 33,500 IPOs in G20 nations found that Big 4 auditor involvement reduced IPO failure risk by up to 67% globally, with a 30% reduction in developing markets including India. Companies should transition to a top-tier audit firm well in advance of filing, not during DRHP preparation.

Disclosure Framework and Related Party Transactions

Clear, consistent, and complete disclosures are among the most scrutinized sections of any DRHP. Material contracts, promoter holdings, related party transactions (RPTs), litigation history, and risk factors all receive intense regulatory and investor attention. Undisclosed or inadequately explained RPTs are a leading cause of SEBI observations and investor concern.

SEBI's RPT disclosure framework has become more rigorous. Under SEBI Circular SEBI/HO/CFD/CMD1/CIR/P/2021/662, listed entities must submit RPT disclosures every six months, and as of April 2023, these disclosures must be filed simultaneously with financial results. SEBI has also introduced a tiered materiality framework effective November 2025, with specific thresholds based on a company's annual consolidated turnover. For SME-listed entities, the materiality threshold is ₹50 crore or 10% of turnover, whichever is lower.

SEBI has demonstrated it will enforce RPT compliance. In 2024, SEBI issued enforcement actions against Paytm for exceeding approved RPT limits during FY 2021-22 and against Linde India for failing to obtain shareholder approval for material RPTs. These actions make clear that RPT hygiene isn't optional.

What a strong disclosure framework looks like:

- A documented RPT policy with clear materiality thresholds

- Arm's-length transaction standards and board approval processes

- Evidence-backed financial reporting with audit trails

- Proactive disclosure of all material transactions, not reactive cleanup

- Records that were built in real time, not reconstructed before filing

Risk Management and Compliance Policies

RPT discipline is one component of a broader picture. Institutional investors assess the full governance stack — and they expect a suite of policies embedded in operations before IPO filing:

- Insider trading policy (mandatory under PIT regulations)

- Code of conduct and ethics for directors and senior management

- Whistleblower mechanism for reporting concerns

- Clawback policy for executive compensation

- Cybersecurity and data privacy risk oversight

Each policy should come with evidence of actual use: board minutes referencing the whistleblower mechanism, documented ethics reviews, periodic clawback policy assessments. Investors know the difference between policies that exist on paper and those that are operational. The former rarely survives due diligence.

How Governance Shapes IPO Outcomes: Valuation, Subscription, and Listing Performance

Governance Quality Directly Affects IPO Pricing

Corporate governance quality influences IPO pricing through the lens of investor perception. QIBs apply a governance premium or discount when assessing an offer price. A company with clean books, transparent related party disclosures, and an experienced independent board earns a tighter valuation band and faces less pricing resistance during bookbuilding.

Weak governance raises immediate red flags for institutional reviewers — reliability of financials, minority shareholder protection, and undisclosed risk all come into question.

This dynamic plays out during roadshows and pre-IPO soundings. Institutional investors scrutinize board composition, audit trails, and RPT disclosures before committing. When governance gaps surface, investors either pass or demand a pricing discount to compensate for perceived risk.

Governance Influences Subscription Demand

QIBs anchor IPO books in India, and their participation is critical to oversubscription. Because they conduct deep diligence before committing, governance quality directly shapes whether a book fills quickly or struggles — regardless of broader market conditions.

Recent market data illustrates this dynamic. During the second half of 2025, QIB subscription levels exceeded 40x for eight consecutive months. But by February-March 2026, subscription levels dropped to approximately 2x, and 66.6% of 2026 IPOs listed below their issue price. When market sentiment cools, governance quality becomes the differentiator between IPOs that attract institutional capital and those that struggle.

Short-Term vs. Long-Term IPO Performance

The Columbia/Sapienza study found that good governance creates value in the short term through stronger listing performance, and protects value over the medium-to-long term by maintaining investor confidence. The study tracked IPOs at 12-, 24-, and 36-month intervals and found that companies with larger boards, higher proportions of independent directors, and stronger director credentials demonstrated more stable long-term performance.

A 2024 study by Harvard Law School and Diligent analyzing 1,026 companies from the 2021 IPO cohort confirmed two additional signals investors track:

- CEO tenure: Longer tenure showed a strong positive correlation with market cap growth post-IPO — leadership stability reads as a governance indicator

- Board independence: Companies with elevated board independence demonstrated positive average return on capital across the three-year study period

The India-Specific Regulatory Dimension

SEBI issues approximately 100 comments per DRHP during regulatory review, with 46% of observations relating to risk factors and 13% to regulatory compliance and governance. Common governance-related observations include:

- Disclosure of risks related to inexperienced directors

- Commercial rationale for promoter or related party transactions

- Materiality ranking of risk factors — SEBI requires issuers to explicitly highlight the top 5, top 10, and top 25 risks

SEBI observation letters are valid for only 12 months. Companies that enter DRHP review with unresolved governance issues consume that window responding to comments — and risk their approval expiring before they can list.

Building a Governance-Ready Company Before Your IPO

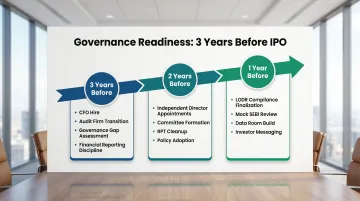

The Governance Readiness Timeline

Research by Stanford Graduate School of Business found that 42% of companies began serious governance work at least three years before their IPO — 29% more than three years before, and 13% exactly three years before. This timeline reflects the reality that building genuine governance capability takes time.

What governance-ready looks like at each stage:

3 Years Before IPO:

- Recruit CFO with public company or audit firm experience

- Begin discussions with potential independent directors

- Conduct governance gap assessment (board composition, policies, RPT hygiene)

- Select and transition to Big Four or reputable national audit firm

- Establish financial reporting discipline (quarterly close processes, internal controls)

2 Years Before IPO:

- Appoint independent directors to the board

- Establish audit, nomination, and compensation committees with proper composition

- Adopt governance policies (insider trading, code of conduct, whistleblower mechanism)

- Clean up and document all related party transactions with board approvals

- Implement disclosure controls and quarterly reporting cadence

1 Year Before IPO:

- Finalize board structure to meet SEBI LODR requirements

- Complete policy adoption and embed compliance into operations

- Conduct mock SEBI review of disclosures and DRHP content

- Build evidence-linked data room with audit trails and board minutes

- Prepare investor messaging on governance and leadership stability

Board Composition and Committee Setup

The timeline above makes one requirement unavoidable: independent directors must be recruited before filing, not scrambled for after. The ideal independent director brings:

- Sector-relevant expertise

- Financial literacy (especially for audit committee roles)

- Experience in taking companies public or serving on listed company boards

- Professional credibility and a strong network

Under SEBI LODR, listed companies must establish three mandatory committees:

| Committee | Minimum Members | Independence Requirement | Chairperson |

|---|---|---|---|

| Audit Committee | 3 directors | Two-thirds independent | Independent director with financial expertise |

| Nomination & Remuneration | 3 non-executive directors | At least 50% independent | Independent director |

| Stakeholders Relationship | 3 directors | At least 1 independent | Non-executive director |

For companies in the top 1,000 by market cap, a Risk Management Committee is also mandatory.

Documentation and Data Room Discipline

Chaotic documentation is one of the most common sources of SEBI observations and delays. Every financial record, contract, RPT approval, board minute, and compliance record needs to be well-organized, evidence-linked, and auditable. That means:

- Financial records tied to audit-confirmed entries

- RPT approvals with board resolution documentation

- Board minutes that are complete, dated, and signed

- Compliance records organized by policy and period

S45's AI-led readiness process builds a live data room with evidence-linked drafting, surfacing disclosure gaps before formal diligence begins. The system flags issues — undocumented RPTs, incomplete board minutes, missing policy approvals — early enough that teams can resolve them without triggering SEBI observations. DRHP preparation compresses to 30–45 days from a clean data room.

Conducting a Governance Gap Assessment

Before starting the formal IPO process, conduct a structured review of:

- Board composition — verify it meets SEBI LODR independence thresholds, with directors who are credible and active

- Governance policies — confirm they are documented, formally adopted, and embedded in operations (not just on paper)

- Related party transactions — confirm all RPTs are documented, board-approved, and disclosed; formalize any informal arrangements

- Disclosure readiness — confirm financial records, contracts, and board minutes are audit-ready

Issues caught at this stage cost weeks to resolve. The same issues surfacing during DRHP review can cost months — and in some cases, trigger an observation letter that stalls the filing entirely.

Common Governance Pitfalls That Can Derail an IPO

Promoter-Dominated Boards with No Functional Independence

The most common governance red flag in Indian pre-IPO companies is a board dominated by promoters and their associates, with independent directors who exist on paper but play no real role in oversight. This creates immediate investor skepticism: Will minority shareholder interests be protected post-listing? Is there credible oversight separate from management?

Institutional investors recognize cosmetic independence. They look for evidence that independent directors are engaged — through committee meeting minutes, board resolutions on key decisions, and audit committee approval of material transactions. If independent directors have been appointed only to meet minimum requirements but don't participate meaningfully, investors will discount the offer.

Undocumented or Poorly Structured Related Party Transactions

Many SMEs and growth-stage companies operate with informal arrangements between the promoter entity and the company — loans, leases, contracts with related entities — that were never formally documented or board-approved. These become expensive to unwind or disclose when DRHP preparation begins.

NISM's analysis of India's SME IPO market found that nearly 50% of listed SMEs report related party transactions exceeding ₹10 crore. Additionally, 65% of 2024 SME listings and 57% of 2025 SME listings currently trade below their issue price, driven in part by governance failures including undisclosed pre-IPO arrangements, inflated revenues, and use of shell entities to divert funds. Approximately 10–12% of SME-listed companies face trading suspensions for non-compliance.

Those numbers carry regulatory consequences. SEBI's enforcement actions treat RPT disclosure as non-negotiable — companies must document all arrangements, obtain board and shareholder approvals where required, and disclose them transparently in the DRHP.

Reactive Compliance Mindset

Companies that treat governance as a checklist to complete just before filing — rather than a system built over time — produce disclosures that are inconsistent, policies that aren't embedded in operations, and boards that have no institutional memory of the company. This kind of governance cosmetics is visible to sophisticated investors and regulatory reviewers.

Governance cannot be retrofitted convincingly in the final months before filing. Credibility requires time — and evidence that was created in real time, not reconstructed retrospectively:

- Consistent board meeting cadence with documented minutes

- Committee-level decision-making on material matters

- Policies embedded in operations, not drafted for the DRHP

- Audit trails that show continuous compliance, not a pre-filing sprint

Frequently Asked Questions

How does corporate governance affect performance?

Corporate governance improves performance by aligning leadership incentives with shareholder interests, ensuring transparent financial reporting, and enabling better decision-making through independent oversight. Well-governed companies consistently show stronger post-IPO valuation metrics and lower long-term stock decay.

What are the factors affecting the IPO market?

The IPO market is shaped by macro factors — interest rates, market liquidity, investor sentiment — and company-specific factors: governance quality, financial track record, promoter credibility, pricing discipline, and disclosure clarity. Governance stands out as one of the few company-controlled variables that directly influences investor perception and subscription demand.

What are the key pillars of corporate governance?

The core pillars are board independence and composition, audit and financial transparency, disclosure and related party transaction management, risk management frameworks, and ethics and compliance policies. Each pillar signals to investors whether the company is genuinely ready for public market accountability.

What does IPO stand for in corporate governance?

IPO (Initial Public Offering) marks the point at which a private company becomes accountable to public shareholders, regulators, and the market. At listing, governance structures face their first formal test — and the quality of oversight, disclosure, and risk management becomes directly visible to institutional investors and SEBI.

How early should a company start building governance for an IPO?

Companies should begin serious governance work 2–3 years before IPO, covering audit firm selection, board structuring, policy frameworks, and RPT cleanup. Companies that start earlier move through filing with fewer SEBI observations and cleaner data rooms.

How does board independence affect IPO valuation?

Independent directors signal to investors that the company has credible oversight separate from promoter influence, reducing perceived risk and building trust in financial disclosures. Boards with higher proportions of genuinely independent directors consistently achieve better short-term IPO valuations and stronger institutional subscription.