Introduction

For Indian SME founders eyeing the public markets, corporate governance is frequently treated as a formality to tick off before listing. That framing is expensive.

Governance is the foundation on which investors, SEBI, and exchanges evaluate whether your business is fit for public markets. SEBI's November 2024 consultation paper documented that 1 in 2 SME listed entities have related party transactions exceeding ₹10 crore — with fund diversion to shell companies and revenue inflation through circular transactions among the most serious concerns.

What follows covers what corporate governance actually requires from a listing SME, what SEBI and the exchanges specifically mandate, and where founders most often get it wrong.

Key Takeaways

- Corporate governance is mandatory for any SME listing on BSE SME or NSE Emerge—not optional

- Key pillars: board composition, independent directors, mandatory committees, and formal governance policies

- SEBI ICDR Regulations and exchange listing criteria set explicit governance benchmarks that must be met before DRHP filing

- Governance gaps cause IPO delays or outright rejections; weak boards, RPT irregularities, and inconsistent financials are the most common triggers

- Strong governance reduces due diligence friction and supports stronger IPO valuations

Why Corporate Governance Is the Real IPO Foundation

What Governance Actually Means

Corporate governance covers the systems, policies, and structures through which a company is directed and controlled. Public markets demand a higher standard than private ownership. For SME founders, this means transitioning from founder-controlled decision-making to a structured board-led model with accountability to public shareholders and regulators.

Governance Equals Investor Trust

Institutional investors—QIBs, NIIs—and retail participants evaluate governance quality as a proxy for management integrity and execution risk. A company with weak governance will struggle to attract quality anchor investors regardless of financial metrics.

S45's experience across 26 IPOs since July 2023 shows that companies with clean governance structures consistently achieve stronger subscription rates and listing pops. The average subscription reached 168x with a 43% listing pop, results directly tied to disciplined governance and clean disclosures.

Governance Affects Valuation and Pricing

Companies with transparent disclosures, clean books, and functional boards command better price discovery during bookbuilding. Research from LBSIM covering 235 IPOs from 2009 to 2018 found that board independence and non-executive director holdings significantly impact IPO subscription rates and underpricing. Governance quality is not abstract. It translates directly into how investors price and subscribe to your offering.

The Cost of Getting Governance Wrong

One of S45's founders lived this while scaling an SME to $60 million and attempting to list. Disorganised disclosures, lost communications, and opaque pricing directly threatened the listing — governance gaps that created repeated disclosure rewrites, unclear pricing frameworks, and compliance failures exhausting founders before they saw results.

That experience became S45's founding conviction: catch governance issues early, fix them systematically, and eliminate the chaos that derails listings.

SEBI Has Raised the Bar

SEBI has progressively tightened governance expectations for SME listings. The December 2024 amendments introduced operating profit requirements (₹1 crore EBITDA in 2 of 3 years), capped offer for sale at 20% of issue size, and banned IPO proceeds from repaying promoter loans. These changes respond to documented misuse of SME platforms and reflect a regulatory environment where the governance bar is higher than ever.

What Corporate Governance Actually Means for a Listing SME

The Governance Transformation

Private SMEs must undergo a fundamental shift before listing: from informal, founder-centric management to a structured board-led model with documented decision-making, formal policies, and external accountability. This transformation takes time—typically 12 to 18 months—and affects every operational aspect of the business.

Board Composition and Independent Directors

Companies Act 2013 Requirements:

Listed public companies must meet these board composition standards:

- Minimum 3 directors for public companies

- At least one-third independent directors (fractions rounded up)

- At least one woman director

- One director must reside in India for minimum 182 days per financial year

Who Qualifies as Independent:

Section 149(6) sets a strict independence bar. A director must meet all of the following:

- No promoter relationship

- No pecuniary relationship with the company in the preceding two years

- Neither the director nor their relatives hold securities exceeding ₹50 lakh or 2% of paid-up capital

- Maximum tenure of 5 consecutive years; one additional term permitted via special resolution

- 3-year cooling-off period required after two terms

Most SMEs have founder-heavy boards where independent directors are absent or only nominally appointed. SEBI scrutinises this closely. Genuine independence means no financial ties, no family connections, and no promoter relationships—not just adding a name to satisfy a checkbox.

Mandatory Board Committees

Three committees are mandatory under the Companies Act 2013. Note that while SEBI LODR Regulations 17–27 are exempt for SME-listed companies under Regulation 15(2), the Companies Act mandates apply in full.

| Committee | Minimum Size | Independence Rule | Chairperson Rule |

|---|---|---|---|

| Audit Committee | 3 directors | Independent majority | Financially literate |

| Nomination & Remuneration | 3 non-executive | One-half independent minimum | Cannot be company chairman |

| Stakeholders Relationship | 3 directors | At least one independent | Non-executive |

Mandatory Governance Policies and Committee Charters

Listing SMEs must formally adopt, document, and operationalise these policies:

- Insider trading policy – SEBI PIT Regulations apply in full to SME-listed companies with no exemption. Penalties range from ₹10 lakh to ₹25 crore

- Related party transactions policy – Critical for SME promoters who often have significant transactions with promoter-owned entities

- Whistleblower policy – Mandatory under Section 177(9)-(10) with direct access to Audit Committee Chairman

- Code of conduct – For directors and senior management

- Disclosure policy – Governs material event disclosure and continuous disclosure obligations

These must be formally adopted by the board, not just drafted and filed. SEBI scrutinises whether policies are operationalised—meaning systems, training, and monitoring are in place.

SEBI and Exchange Governance Requirements You Cannot Ignore

SEBI ICDR Chapter IX: The Primary Framework

SEBI's ICDR Regulations embed governance compliance throughout the SME IPO process—from eligibility to disclosure norms in the DRHP. Key provisions include:

- Regulation 228 (Ineligibility): Entities are ineligible if promoters, directors, or selling shareholders are debarred from capital markets, involved in IBC proceedings, or classified as wilful defaulters or fugitive economic offenders

- Regulation 229 (Paid-Up Capital): Post-issue capital up to ₹10 crore requires SME platform listing; ₹10-25 crore allows choice of SME or Main Board; above ₹25 crore requires Main Board listing

BSE SME Listing Criteria

BSE SME eligibility requirements include:

- Post-issue paid-up capital not exceeding ₹25 crore

- Net worth of at least ₹1 crore for 2 preceding full financial years

- Net tangible assets of ₹3 crore in last preceding full financial year

- Operating profit (EBITDA) of ₹1 crore in 2 of 3 preceding financial years

- Minimum 3-year track record

- No IBC proceedings or winding-up petitions admitted

- All promoter shareholding in demat form

- Active website with 3 years of audited financials disclosed

NSE Emerge Listing Criteria

NSE Emerge eligibility requirements include:

- Post-issue paid-up capital not exceeding ₹25 crore

- Operating profit of ₹1 crore in 2 of 3 preceding financial years

- Positive net worth

- Positive free cash flow to equity (FCFE) for 2 of 3 preceding years

- Minimum 20% promoter contribution post-issue

- Offer for sale capped at 20% of issue size

- IPO proceeds cannot repay loans from promoters, promoter group, or related parties

- No material regulatory action in past 3 years

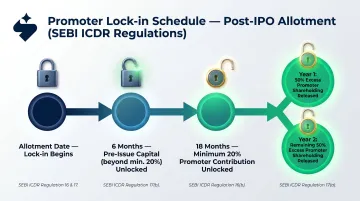

Promoter Lock-In Requirements

Per SEBI ICDR FAQs (May 2025):

- Minimum promoter contribution (20%): 18 months lock-in from allotment date

- Remaining pre-issue capital: 6 months lock-in from listing date

- Excess promoter shareholding: Phased release—50% after 1 year, 50% after 2 years (December 2024 amendment)

These lock-in periods demonstrate promoter commitment to public shareholders — investors treat them as a direct gauge of long-term conviction in the business.

How S45's AI-Led Process Catches Governance Gaps Early

Given how many of these requirements interact, governance gaps are among the most common issues surfacing during DRHP drafting. S45's readiness analytics run before engaging the full intermediary chain, flagging issues like:

- Board constitution gaps (missing independent directors, improperly constituted committees)

- Related party transaction anomalies (undisclosed or inadequately documented RPTs)

- Undocumented governance policies (missing insider trading codes, whistleblower policies)

- Disclosure control weaknesses

Catching these early means companies can resolve them before triggering SEBI observations or exchange rejections — not scrambling to fix them mid-filing.

S45's preliminary scan (5 business days) provides immediate governance gap visibility. The comprehensive scan (2-3 weeks) maps full compliance requirements against SEBI ICDR and Companies Act standards.

How Corporate Governance Transforms Your Company Pre-IPO

Operational Changes Required

Governance preparation introduces formal structures and documentation:

- Board minutes and resolutions become formal records of all decisions

- Financial reporting adopts SEBI-compliant formats and Ind-AS standards

- Company Secretary appointment becomes mandatory

- Management communication shifts from informal to documented board-level decision-making

Financial Clean-Up Runs in Parallel

Merchant Banker due diligence stalls immediately without the right financial foundations in place. Specifically, companies need:

- Three years of audited financial statements in Schedule III format, prepared by ICAI peer-reviewed auditors

- Established internal audit functions with clear, traceable audit trails

- Clean books that withstand scrutiny from the first due diligence session

The Timeline Reality

Governance restructuring for a promoter-run SME typically takes 12 to 18 months when done properly. This is why advisors recommend starting governance work at least 2 years before the intended IPO filing date. Companies that delay governance preparation compress timelines and increase rejection risk.

When governance is sorted ahead of time, execution can move fast. S45 moves from first call to signed mandate in 7 days and delivers DRHP-ready drafts in 30 to 45 days. That clock starts only when the data room is clean: governance structures in place, policies operationalised, and documentation complete.

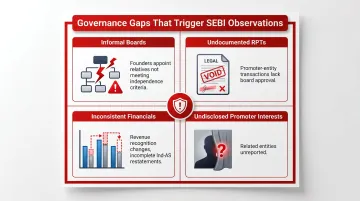

Common Governance Failures That Derail SME IPOs

Most Frequent Failure Patterns

From S45's experience across 26 IPOs, the most common governance failures include:

- Informal boards without proper independent directors – Founders appoint relatives or business associates who don't meet independence criteria

- Undocumented related party transactions – Transactions between the company and promoter-owned entities lack proper board approval or disclosure

- Inconsistent financials across years – Revenue recognition policies change, segment reporting is inconsistent, or Ind-AS restatements are incomplete

- Promoters with undisclosed interests – Other entities controlled by promoters go undisclosed or are incorrectly classified

The Data on Governance-Related Observations

DRHP rejections fell to 2 in FY26 from 17 in FY25, attributed to SEBI's consultative approach and improved issuer understanding of governance red flags. However, the Trafiksol ITS Technologies case in December 2024 demonstrates that governance failures still trigger severe enforcement: SEBI cancelled the IPO entirely and ordered ₹44.87 crore refunded after discovering IPO proceeds were intended to purchase software from a shell entity with fabricated credentials.

The Opaque Pricing Risk

When governance does not support a credible financial narrative, Merchant Bankers and investors struggle to validate pricing. This leads to two outcomes:

- Under-pricing – The company leaves money on the table to compensate for governance uncertainty

- Over-pricing – Subscription collapses and post-listing credibility is destroyed

Both outcomes are avoidable. Companies that proactively identify and fix governance issues before approaching a Merchant Banker move through DRHP drafting and exchange review faster and with fewer observations.

Governance Failures Are Often Unintentional

Understanding why pricing risk exists in the first place starts with recognising where most failures originate: not from intent, but from habit.

Many governance failures arise from years of informal operations that worked fine as a private company. Handshake agreements, undocumented decisions, and family-controlled boards are common in successful SMEs — and rarely caused problems before a listing attempt. Public markets require a different standard. Companies that recognise this early move into DRHP drafting with a cleaner data room, fewer regulator observations, and a stronger pricing narrative.

Post-Listing Governance: What Changes After You Ring the Bell

Governance Obligations Increase Significantly

Post-listing compliance includes:

- Half-yearly financial disclosures – SME-listed companies are exempt from quarterly reporting under LODR Regulation 15(2) but must file half-yearly results within 21 days

- Continuous disclosure for material events – LODR Regulation 30 requires immediate disclosure of material events; determining materiality requires a formal framework

- Annual General Meeting obligations – Notice, quorum, resolutions, and filings must meet statutory timelines

- Related party transaction rules – SEBI LODR Regulations 17-27 are exempt for SME companies, but RPT disclosure requirements apply from April 1, 2025 for companies with paid-up capital above ₹10 crore or net worth above ₹25 crore

- SEBI PIT Regulations – Full compliance applies with no SME exemption; companies must log all UPSI in a Structured Digital Database within 2 calendar days

The Ongoing Investor Relations Burden

Many SME founders underestimate the ongoing burden of investor communication:

- Quarterly earnings preparation and analyst Q&A

- Non-deal roadshows and investor conferences

- IR website maintenance with disclosure materials

- Compliance calendar management for filings and board meetings

- Market maker coordination for SME liquidity programs

S45's post-listing support covers this entire operational layer — IR toolkit preparation, PIT code implementation, compliance calendar management, and market maker coordination. The companies that navigate this well are the ones that build these systems before listing day, not after.

Frequently Asked Questions

What is the new SME rule for IPO?

SEBI's December 2024 amendments require minimum operating profit (EBITDA) of ₹1 crore in at least 2 of the last 3 financial years, cap offer for sale at 20% of issue size, and prohibit using IPO proceeds to repay promoter loans. A 21-day public DRHP review period was also introduced.

Can I sell SME IPO easily?

Liquidity is limited. SME IPO shares carry minimum lot sizes (typically 10,000+ shares per lot), making secondary market exits harder for retail investors than on the Main Board. Promoters face lock-in periods post-listing, and selling shareholders in the IPO are capped at 50% of their pre-issue shareholding.

What is the minimum paid-up capital required for an SME IPO in India?

Post-issue paid-up capital must not exceed ₹25 crore to qualify as an SME IPO under SEBI ICDR Regulations. Issuers in the ₹10–₹25 crore range may choose between SME and Main Board; above ₹25 crore, Main Board listing is mandatory.

How many independent directors are required for a listed SME company?

Listed companies under the Companies Act 2013 must have at least one-third of the board as independent directors, with the Audit Committee requiring a majority of independent directors. This requirement must be met before IPO listing, not after.

What is the difference between BSE SME and NSE Emerge for governance requirements?

The key difference is financial thresholds: NSE Emerge requires positive net worth and positive FCFE for 2 of 3 years, while BSE SME requires net worth of ₹1 crore for 2 preceding years and net tangible assets of ₹3 crore. Board constitution and compliance standards are identical across both platforms under SEBI ICDR and Companies Act 2013.

How long does it take to prepare for an SME IPO in India?

The full preparation cycle typically takes 2 to 3 years, with governance restructuring and financial clean-up beginning in Year 1, SEBI compliance alignment in Year 2, and Merchant Banker appointment and DRHP drafting in Year 3. Companies that start governance and financial clean-up 12–18 months ahead of their target listing date can often compress the full cycle to under 2 years.