Introduction

Many Indian SME founders preparing for public listing underestimate a critical reality: governance standards determine IPO success more than financial eligibility. Companies routinely meet SEBI's paid-up capital and profitability thresholds, yet stall for months during DRHP review because their board minutes are incomplete, related-party transactions lack documentation, or auditors have issued qualified opinions.

For Indian SME founders, promoters, and senior management preparing to list on BSE SME or NSE Emerge, governance shapes three outcomes that determine your IPO's fate: whether SEBI approves your DRHP, how investors price your issue, and whether your listing holds up over time.

This guide covers the governance standards that apply under SEBI's framework, how they're enforced at each IPO stage, and what separates well-prepared companies from those that derail mid-process.

Key Takeaways

- SME IPOs operate under SEBI's ICDR Regulations with listing on BSE SME or NSE Emerge; governance obligations are real and enforceable despite lower financial thresholds than Main Board

- Governance readiness spans four pillars: board constitution, financial reporting standards, statutory disclosures, and post-listing compliance. All four are enforceable, not optional.

- SEBI review cycles begin with DRHP filing; disclosure quality directly determines observation rounds and approval timelines

- Most SME IPO delays originate internally, in audit gaps, related-party disclosures, and undocumented board decisions. The regulator is rarely the bottleneck.

- Companies treating governance as a pre-filing checklist rather than ongoing operating standard face the steepest post-listing compliance risk

What Is the SME IPO Governance Process?

The SME IPO governance process is the sequence of regulatory compliance and internal governance actions an SME must complete—from restructuring its board to filing audited disclosures—to satisfy SEBI, BSE SME, or NSE Emerge requirements for listing.

Its purpose is direct: give public investors enough verified, standardised information to make informed decisions, and give regulators confidence that operations and disclosures can withstand public scrutiny.

How SME Governance Differs from Main Board

SME platforms have lower financial thresholds and streamlined review processes, but the governance architecture follows the same SEBI ICDR framework with specific SME carve-outs—not a parallel relaxed track. Key distinctions:

- Exchange-led review: Unlike Main Board IPOs where SEBI issues observations within 30 days, SME DRHPs are reviewed by the stock exchange, including site inspections and Listing Advisory Committee interviews

- LODR exemptions: Under Regulation 15(2), SME-listed entities are exempt from SEBI LODR Regulations 17-27, covering audit committees, NRC, and corporate governance reporting—but not from Companies Act 2013 requirements

- Half-yearly reporting: SME issuers file financial results and shareholding patterns half-yearly rather than quarterly

The practical implication: a company can raise ₹20-25 crore from public markets without constituting an audit committee or filing quarterly results—obligations that kick in only on migration to the Main Board. Companies Act 2013 requirements, however, apply from day one regardless of which platform you list on.

SEBI's Governance and Eligibility Requirements for SME IPOs

Financial Eligibility Thresholds

Under Regulation 229 of SEBI ICDR 2018, issuers qualify for SME IPO if post-issue paid-up capital does not exceed ₹25 crore. Within this ceiling:

- Standard SME: Up to ₹10 crore post-issue capital

- Extended category: ₹10–25 crore post-issue capital

- Migration trigger: Exceeding ₹10 crore enables voluntary Main Board migration; exceeding ₹25 crore mandates it

Platform-specific requirements differ across exchanges:

| Criterion | BSE SME | NSE Emerge |

|---|---|---|

| Net tangible assets | ₹3 crore (last full FY) | Not specified |

| Net worth | ₹1 crore (2 preceding FYs) | Positive (all 3 FYs from Dec 2024) |

| Operating profit (EBITDA) | ₹1 crore in 2 of 3 FYs | ₹1 crore in 2 of 3 FYs |

| Free cash flow to equity | Not specified | Positive in 2 of 3 FYs |

| Leverage ratio | Max 3:1 | Not specified |

Sources: BSE SME Listing Criteria; NSE Emerge Eligibility

BSE SME imposes stricter quantitative thresholds overall. NSE Emerge offers greater flexibility through technology startup routes and QIB-based alternatives, but the FCFE requirement added from December 2024 narrows that advantage for capital-intensive businesses.

Board Constitution and Committee Requirements

Every listed public company must have at least one-third of directors as independent directors under Section 149(4) of the Companies Act 2013, plus at least one woman director.

Critical distinction: SME-listed entities are exempt from SEBI LODR Regulations 17-27, meaning audit committees, NRC, and risk management committees are not mandatory under LODR. However, if the Companies Act independently mandates these committees (Section 177 applies to all listed companies), compliance remains required.

Financial Reporting and Audit Standards

Issuers must present restated financial statements for three preceding years, audited by a qualified Chartered Accountant in accordance with Indian GAAP or Ind-AS.

December 2024 amendments added stricter requirements:

- Peer-reviewed auditor mandatory

- Converted entities (from proprietorships/partnerships/LLPs) must exist as companies for at least one full financial year before DRHP filing

- Financials must comply with Schedule III of the Companies Act, 2013

Clean audit opinions are critical—qualified statements consistently trigger multiple SEBI observation rounds.

Promoter Lock-In and Shareholding Disclosure

Under Regulation 236 and 238 of SEBI ICDR:

- Minimum promoter contribution: 20% of post-issue paid-up capital

- Lock-in structure:

- Minimum 20% contribution: 3 years from allotment

- Excess holdings above 20%: 1 year from allotment

- Non-promoter pre-IPO shareholders: 6 months from allotment

- Dematerialization: 100% of promoter shareholding must be in demat form at filing

Related-party transaction disclosure obligations receive the closest scrutiny during DRHP review.

December 2024 Amendments: Material Changes

SEBI Board Meeting PR No. 37/2024 (December 18, 2024) tightened SME IPO rules, effective April 1, 2025:

| Amendment | Before | After |

|---|---|---|

| Minimum application size | ₹1 lakh | ₹2 lakh |

| Minimum allottees | 50 | 200 |

| OFS cap | No specific cap | 20% of issue size |

| Monitoring agency | Not mandatory | Mandatory for issues > ₹20 crore |

| Auditor requirement | No peer review | Peer-reviewed auditor mandatory |

| Use of proceeds | Promoter loan repayment permitted | Prohibited |

Taken together, these amendments raise the practical bar for SME IPO readiness — issuers who haven't restructured governance, auditor arrangements, and proceeds deployment well before DRHP filing will face longer SEBI observation cycles.

How the SME IPO Governance Process Works

The process runs in three phases—pre-filing governance remediation (6-12 months), SEBI/exchange review (30-90 days), and post-listing compliance—with distinct governance deliverables gating progress between stages.

Phase 1: Pre-Filing Governance Remediation

This is where most timeline risk lives. Companies must:

- Reconstitute boards to meet independence requirements

- Close out or fully disclose related-party transactions

- Restate financials where revenue recognition or segment reporting doesn't align with Ind-AS

- Resolve outstanding ROC filings, director DINs, and statutory notices

AI-led readiness diagnostics—like the one S45 uses to prepare SME issuers—can surface these gaps early and map corrective actions against filing milestones, compressing what often takes months into structured sprints. Companies that clean books only at year-end face multiple clarification rounds extending timelines by months.

Phase 2: DRHP Preparation and Filing

The Draft Red Herring Prospectus is the primary governance disclosure document. It must contain:

- Risk factors

- Related-party transaction disclosures

- Litigation history

- Promoter background

- Use-of-proceeds rationale

- Audited financials in SEBI ICDR disclosure schedule format

First-filing quality directly determines how many observation rounds follow. Companies treating the DRHP as a finished product rather than an opening position consistently face more exchanges, longer timelines, and higher advisor costs.

Phase 3: SEBI Review, Observations, and Approval

Unlike Main Board IPOs, SME DRHPs are reviewed by the exchange, not SEBI directly. The exchange conducts:

- Detailed document review

- Physical site inspection of company facilities

- Promoter interview before Listing Advisory Committee

Exchanges typically issue observations within 30 days of filing. Responses are time-bound; inadequate or inconsistent disclosures restart review cycles. Governance-related observations—board structure, RPT disclosures, auditor qualifications—are among the most commonly cited causes of delayed approvals.

Phase 4: Post-Listing Governance Obligations

Clearing the exchange review marks the start of a new compliance cycle, not the finish line. Governance obligations continue after listing. Under SEBI LODR, SME issuers must:

- File financial results half-yearly (Main Board files quarterly)

- Submit shareholding pattern reports half-yearly within 21 days

- Hold Annual General Meetings

- Maintain investor grievance redressal systems

- Escalate to full Main Board governance requirements upon crossing the paid-up capital migration threshold

Non-compliance triggers penalties:

| Non-Compliance | Fine Per Day |

|---|---|

| Financial results delay (Reg 33) | ₹5,000 |

| Shareholding pattern delay (Reg 31) | ₹2,000 |

| Annual report delay (Reg 34) | ₹2,000 |

| Voting results delay (Reg 44) | ₹10,000 |

Continued non-compliance for two consecutive periods can trigger trading suspension.

Key Factors That Affect Governance Readiness

Financial Record Quality

The state of a company's financial records is the single biggest determinant. Companies with:

- Continuous audit-grade quarterly closes

- Clean segment reporting

- Reconciled subsidiary accounts

...move through SEBI review in weeks. Companies cleaning books only at year-end face multiple clarification rounds extending timelines by months.

Organizational and Structural Factors

Critical readiness factors include:

- Undisclosed holding structures within the promoter group

- Related-party transactions that lack arm's-length documentation

- Inconsistent disclosure of litigation or tax demands across filings

- Boards that are structurally compliant but operationally promoter-controlled

Exchange-Specific Requirements

BSE SME and NSE Emerge each have their own vetting processes and may request additional disclosures beyond SEBI's minimum ICDR requirements. BSE SME applies stricter net tangible asset and leverage thresholds, making it a more conservative filter. NSE Emerge only requires positive net worth, giving it a wider entry point for early-stage companies. Knowing which exchange suits your financial profile before filing saves weeks of rework.

Common Governance Mistakes and Misconceptions

Eligibility ≠ Readiness

The most common misconception: meeting SEBI's financial eligibility thresholds means the company is governance-ready. In practice, eligibility thresholds are necessary but not sufficient. A company can exceed net worth requirements and still fail DRHP review because board minutes are incomplete, promoter transactions are undisclosed, or auditors issued qualified opinions.

Structural vs. Operational Compliance

Teams consistently oversimplify by treating governance remediation as a legal exercise rather than operational one:

- Appointing independent directors on paper without constituting functioning committees

- Disclosing related-party transactions in financial notes without addressing them in DRHP risk factors the way SEBI expects

- Treating auditor appointment as an annual formality rather than evaluating actual independence from promoter relationships

The SEBI Review Is a Dialogue, Not a Gate

The SEBI review is not a one-shot approval gate—it's a dialogue. The correct approach is to file a governance-complete document that anticipates SEBI's standard queries and addresses them proactively.

Case Study: DroneAcharya Aerial Innovations

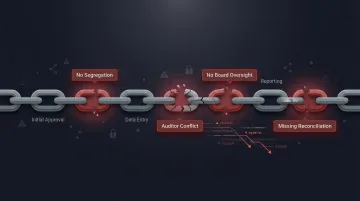

SEBI's interim order against DroneAcharya Aerial Innovations, a BSE SME-listed drone services company, marks the first major enforcement action against financial fraud at an SME-listed company. SEBI found that the company allegedly fabricated 35% of FY24 revenue.

Governance failures identified:

- Same individuals generating and recording revenue — no segregation of duties in the finance function

- Longstanding auditor-promoter relationships that compromised independence

- Board failed to examine contracts underlying major revenue lines

- No reconciliation linking contracts, delivery confirmations, and bank receipts

When governance is ceremonial, fraud has room to compound. SEBI's action here signals that SME listings face the same scrutiny — and the same consequences — as Main Board filings.

Frequently Asked Questions

What are the requirements for SME IPO?

Under SEBI ICDR Regulation 229, issuers must have post-issue paid-up capital up to ₹25 crore and meet platform-specific financial thresholds (BSE SME: ₹3 crore NTA, ₹1 crore net worth; NSE Emerge: positive net worth and positive FCFE). Promoters must contribute a minimum 20% with a 3-year lock-in, and the company must list on BSE SME or NSE Emerge rather than the Main Board.

What is the process of SME IPO?

The SME IPO process runs from pre-filing governance preparation (board restructuring, financial restatements, RPT cleanup) through merchant banker appointment, DRHP filing, and exchange-led review including site inspection and promoter interview. After that comes marketing, price discovery, bidding, allotment, listing, and ongoing half-yearly LODR compliance.

What governance changes must an SME make before filing a DRHP?

Companies must reconstitute their boards to meet Companies Act independence requirements (minimum one-third independent directors) and form mandatory committees where applicable. Related-party transactions must be closed out or fully disclosed with arm's-length documentation, and three years of audited financials must be in Ind-AS compliant format with clean audit opinions.

What is the difference between BSE SME and NSE Emerge listing requirements?

Both operate under SEBI's ICDR framework but diverge on financial thresholds. BSE SME requires ₹3 crore net tangible assets, ₹1 crore net worth, and a 3:1 leverage cap; NSE Emerge requires only positive net worth but adds positive FCFE in 2 of 3 years. NSE also offers technology startup routes and QIB-based alternatives unavailable on BSE.

How long does SEBI take to review an SME IPO application?

Exchanges (not SEBI directly) typically issue observations within 30 days of DRHP filing, but total approval timeline depends on the number of observation rounds triggered. High-quality governance disclosures in the initial DRHP result in faster approval; incomplete disclosures restart review cycles. Typical SME IPO timelines run 3-6 months from DRHP filing to listing.

What happens if an SME fails to meet post-listing governance requirements?

SEBI LODR non-compliance triggers daily fines — ₹5,000/day for delayed financial results, ₹2,000/day for shareholding pattern lapses — along with exchange notices and, in serious cases, trading suspension or delisting. SMEs crossing the ₹25 crore paid-up capital threshold must migrate to Main Board standards, which carry significantly higher obligations including quarterly reporting and full LODR Regulations 17-27 applicability.