This guide covers how SEBI defines NIIs, the sNII/bNII split, how participation works step by step, and what NII subscription data actually signals about an IPO's health.

Key Takeaways

- NII = any IPO applicant bidding above ₹2 lakh who isn't a QIB (Qualified Institutional Buyer)

- Two sub-categories apply: sNII (₹2L–₹10L) and bNII (above ₹10L), each with its own allotment pool

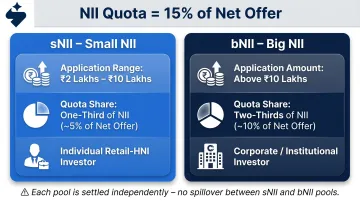

- SEBI mandates at least 15% NII quota: one-third goes to sNII, two-thirds to bNII

- Since April 2022, allotment runs on a draw of lots for the minimum bid lot — no longer purely proportionate

- NIIs cannot bid at cut-off price and cannot withdraw or reduce their bid once submitted

What Is a Non-Institutional Investor (NII) in an IPO?

Under Regulation 2(1)(nn) of the SEBI ICDR Regulations 2018, a Non-Institutional Investor is any applicant who is neither a Retail Individual Investor nor a Qualified Institutional Buyer. That covers anyone bidding above ₹2 lakh in an IPO who isn't a SEBI-registered institutional entity — resident individuals, HUFs, NRIs, private companies, trusts, and corporate bodies. The category exists so issuers can access high-value non-institutional capital without routing everything through QIBs or retail applicants.

NII vs HNI: Not the Same Thing

This distinction trips up a lot of people. HNI is a wealth classification describing a person's financial profile. NII is a regulatory category in IPOs, defined purely by application size and institutional status — the two measures operate on entirely different axes.

An HNI becomes an NII only when they apply for more than ₹2 lakh in a public issue. Below that threshold, even a wealthy individual is classified as a retail investor for IPO purposes. Treating them as interchangeable can cause real confusion when sizing an application or interpreting subscription data by category.

Types of NIIs: sNII and bNII Explained

Since April 2022, SEBI has divided the NII quota into two sub-categories. Each has its own reserved allocation within the 15% NII bucket, and each is treated as a separate allotment pool.

| Sub-Category | Application Size | Share of NII Quota | Approx. % of Net Offer |

|---|---|---|---|

| sNII (Small NII) | Above ₹2L up to ₹10L | One-third | ~5% |

| bNII (Big NII) | Above ₹10L | Two-thirds | ~10% |

Small NII (sNII)

sNII applicants bid above ₹2 lakh and up to ₹10 lakh. One-third of the NII reservation is set aside for this sub-category. sNII sits between retail and large-ticket HNI participation — a meaningful commitment, but within reach of individual investors and smaller family offices.

Big NII (bNII)

bNII applicants bid above ₹10 lakh, with roughly two-thirds of the NII reservation allocated here. This group typically includes HNIs, family offices, corporate bodies, and entities committing significant capital. Because bNII investors must name a specific price and cannot withdraw, their subscription figures are closely watched — high bNII oversubscription indicates that well-capitalised investors are comfortable with the issue's pricing.

Why the split matters for allotment:

- Oversubscription in one pool does not spill into the other — each sub-category is settled independently.

- Confirm which sub-category your bid falls into before applying, since allotment outcomes differ between pools.

How NII Participation Works in a Book-Built IPO

Once an IPO opens, NIIs submit applications through the ASBA system (Application Supported by Blocked Amount), specifying both the number of lots and a bid price within the declared price band. Funds are blocked — not debited — until allotment is finalised.

Step 1: Check Eligibility and Prepare

Before applying, an investor needs:

- An active demat account

- A linked bank account enrolled for ASBA

- A valid PAN with completed KYC

- An application value above ₹2 lakh

No SEBI registration is required. NIIs do not need to register the way QIBs do — any eligible investor bidding above the threshold automatically qualifies.

Step 2: Review the Red Herring Prospectus (RHP)

The RHP discloses the price band, lot size, NII reservation percentage, and category-specific terms. Reading it carefully matters for NIIs in particular, because:

- NIIs must specify a bid price — the cut-off option is not available

- Bids can only be revised upward before the issue closes

- Once submitted, a bid cannot be withdrawn or reduced

Understanding the price band isn't optional here. An invalid bid — typically one below the floor price — is rejected outright.

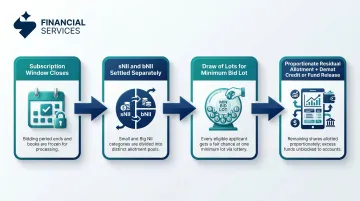

Step 3: Submit Application and Await Allotment

After submission, the application amount is blocked via ASBA. Once the subscription window closes:

- Allotment is calculated for sNII and bNII sub-categories separately

- In oversubscribed scenarios, a draw of lots determines which applicants receive the minimum bid lot

- Any remaining shares after the lottery are allotted proportionately

- The registrar publishes the basis of allotment; shares are credited to demat accounts or blocked funds are released

For issuers, NII demand — particularly from bNII — carries real weight because these bids are irrevocable and price-specific. Real-time category-wise tracking of sNII and bNII subscription patterns during the window matters: it's the difference between targeted pre-window engagement and reactive scrambling once bidding opens. S45's live Demand Map and 50,000+ mapped NII/HNI investor network (segmented by large ticket >₹10L and small ticket <₹10L) are built specifically for this visibility.

NII vs Retail vs QIB: Key Differences

| Parameter | QIB | NII (sNII + bNII) | Retail |

|---|---|---|---|

| Application size | No upper limit | Above ₹2L (sNII: ₹2L–₹10L; bNII: above ₹10L) | Up to ₹2L |

| SEBI reservation | ≥50% | ≥15% | ≥35% |

| SEBI registration required | Yes | No | No |

| Cut-off price bidding | Not permitted | Not permitted | Permitted |

| Bid withdrawal | Not permitted after issue closure | Not permitted at any time after submission | Permitted during bidding period |

| Allotment method (oversubscribed) | Proportionate (non-anchor) | Draw of lots for minimum lot; balance proportionate | Draw of lots (min. one lot per applicant) |

Two differences matter most for NII applicants:

- Allotment uses a lottery, not pure proportionality — post-April 2022, an sNII applicant bidding ₹2.1 lakh and one bidding ₹9.9 lakh have the same probability of receiving the minimum lot in a heavily oversubscribed issue

- No cut-off option — NIIs must make a deliberate pricing decision, which demands greater familiarity with the company's valuation relative to peers

These mechanics also shape how the market reads demand. Retail oversubscription reflects applicant volume; NII oversubscription reflects the depth of committed, irrevocable capital — which is why bankers and analysts track the NII subscription ratio separately when assessing the true quality of an issue's book.

What Affects NII Allotment — and What Investors Often Get Wrong

How the Lottery System Works

Under the post-2022 framework, if the sNII or bNII sub-category is oversubscribed, allotment works like this:

- A draw of lots determines which applicants receive one minimum bid lot

- Any shares remaining after the lottery are distributed proportionately among successful applicants

- Applying for 1 lot versus 13 lots in the same sub-category gives you the same lottery probability

This is a fundamental shift from how most investors assume the system works.

The Multiple-Application Misconception

In retail IPOs, applying through multiple family members can improve lottery chances. NIIs have no equivalent workaround — one application per PAN per issue, no exceptions. Multiple NII applications under the same PAN are identified and rejected outright.

The only variable that legitimately affects NII outcomes is which issue you apply to and how you manage capital across concurrent opportunities.

What Drives Strong NII Demand

Historical data shows a strong correlation between NII subscription levels and listing performance. Vibhor Steel Tubes saw NII subscription of approximately 741x and listed at a ~193% gain. Paras Defence recorded approximately 928x NII subscription and a ~185% listing gain. Tata Technologies achieved 62x NII subscription and listed approximately 140% above issue price.

That said, high NII subscription is not a guarantee — the Hyundai Motor India IPO (2024) subscribed just 2.37x overall and listed at a discount.

On the issuer side, factors that consistently drive NII demand include:

- Pricing discipline — a price band set conservatively relative to listed peers signals credibility

- Grey market premium signals — NII investors monitor GMP as an informal pre-commitment indicator, given they cannot withdraw bids once placed

- Company fundamentals — revenue trajectory, margin profile, and sector tailwinds all affect how experienced non-institutional capital appraises an issue

Capital Risk: The Opportunity Cost Problem

Since funds are blocked rather than lost during the IPO window, many investors underestimate the real cost. In a heavily oversubscribed issue, the effective capital deployed for allotted shares may be a small fraction of the blocked amount — but the full blocked sum sits idle throughout the period. For investors applying to multiple concurrent IPOs simultaneously, this liquidity drag scales fast — three concurrent applications, each blocking ₹14 lakh, ties up ₹42 lakh regardless of allotment outcome.

Frequently Asked Questions

What is a non-institutional investor in an IPO?

A Non-Institutional Investor is any IPO applicant bidding for shares worth more than ₹2 lakh who does not fall under the QIB category. This includes resident individuals, HUFs, NRIs, companies, and trusts. No SEBI registration is required to participate.

What is the difference between retail and non-institutional investors in an IPO?

Retail and NII applicants differ on three fronts: application size (retail up to ₹2 lakh, NII above ₹2 lakh), cut-off price eligibility (retail can bid at cut-off, NII cannot), and allotment method. Retail allotment uses a minimum one-lot lottery guarantee; NII allotment uses a lottery for the minimum lot with proportionate residual, and all NII bids are irrevocable.

Can I apply for an IPO in the NII category?

Yes. Any resident Indian, NRI, HUF, company, or trust can apply in the NII category. Three conditions apply: the application must exceed ₹2 lakh, a valid demat account with completed KYC must be in place, and the bid must go through the ASBA system. No SEBI registration is needed.

Which category has more chances of IPO allotment?

It depends on subscription levels. In heavily oversubscribed issues, retail investors benefit from a minimum one-lot lottery guarantee. NII allotment also uses a lottery for the minimum lot post-2022, so the advantage of a larger bid size within NII has narrowed significantly since the 2022 SEBI amendments.

Is there any way to increase chances of IPO allotment as an NII?

Place your bid at or above the upper end of the price band — invalid bids are rejected automatically. The 2022 allotment reform reduced the advantage of larger bid sizes within a sub-category, and applying through multiple accounts under the same PAN is not permitted for NIIs.

What happens if the NII category is undersubscribed?

Full allotment is given to all valid applicants up to the bid quantity. Any unsubscribed NII portion may be carried over to other investor categories per the basis of allotment determined by the registrar and disclosed in the offer documents.