Introduction

Most IPO coverage mentions QIB subscription numbers prominently — "oversubscribed 105x by QIBs" — without explaining what actually happens behind those figures. Who gets shares? How are they allocated? And what does it mean when a company files under the "QIB route"?

QIB share allotment is how Qualified Institutional Buyers receive shares in a book-built IPO — allocated proportionately based on their bids within the declared price band. It governs how the majority of every mainboard IPO is distributed and shapes the final issue price.

In one specific regulatory pathway, QIB demand doesn't just influence the outcome — it determines whether the offering can proceed at all.

This guide is for founders, CFOs, and investment professionals who want to move beyond headline subscription numbers and understand how allocation actually works.

Key Takeaways

- QIBs are large institutions (mutual funds, banks, FPIs, insurance companies, pension funds) allocated at least 50% of a book-built IPO under Reg 6(1), rising to 75% under Reg 6(2)

- QIB allotment is proportionate: at 10x oversubscription, each eligible bidder receives roughly one-tenth of their bid

- Anchor investors are allotted shares one day before the IPO opens under a mandatory 30/90-day split lock-in; non-anchor QIBs face no lock-in

- Under Reg 6(2), if QIBs don't subscribe 75% of the net offer, the entire IPO is cancelled and all proceeds are refunded

- High QIB subscription signals institutional conviction — KPMG data shows average QIB subscription of ~105.6x in FY25, strongly correlated with listing-day returns

What Is QIB Share Allotment in IPO Bookbuilding?

QIB share allotment refers to the distribution of shares to Qualified Institutional Buyers after the bookbuilding window closes and the cut-off price is finalised.

Unlike the retail category (where oversubscribed issues use a computerised lottery), the QIB category uses proportionate allotment: each QIB receives shares in proportion to their bid quantity relative to total QIB demand at or above the cut-off price.

Bookbuilding vs. Fixed Price Method

Bookbuilding is a price discovery mechanism where investors bid within a declared price band, and the final issue price is set where total demand meets total supply. The fixed price method uses a single pre-announced price with no bidding.

QIB allotment exclusively occurs in book-built issues. That is the only method where QIBs formally participate as a distinct investor category under SEBI ICDR Regulations — which also makes the following distinction worth understanding before reading further.

"QIB Participation" vs. "The QIB Route" — A Critical Distinction

These two terms are frequently conflated, and the confusion can mischaracterise a company's financial standing in investor communications:

- QIB participation occurs in every book-built mainboard IPO regardless of regulatory route — strong institutional demand simply means institutions found the offering attractive

- The QIB route refers specifically to Regulation 6(2) filings, applicable only to companies that cannot meet SEBI's profitability norms under Reg 6(1)

Calling a standard IPO with strong institutional interest a "QIB route IPO" falsely equates companies with very different financial profiles.

Who Qualifies as a QIB Under SEBI ICDR?

SEBI Regulation 2(1)(ss) of the ICDR Regulations 2018 defines exactly 13 QIB categories:

| # | QIB Category | Key Criteria |

|---|---|---|

| 1 | SEBI-registered mutual fund | SEBI registration |

| 2 | SEBI-registered venture capital fund | SEBI registration |

| 3 | SEBI-registered alternative investment fund | SEBI registration |

| 4 | SEBI-registered foreign venture capital investor | SEBI registration |

| 5 | Foreign portfolio investor (excluding individuals, corporate bodies, family offices) | SEBI registration |

| 6 | Public financial institution | As defined under Companies Act |

| 7 | Scheduled commercial bank | RBI scheduled status |

| 8 | Multilateral/bilateral development financial institution | Institutional status |

| 9 | State industrial development corporation | State government entity |

| 10 | IRDAI-registered insurance company | IRDAI registration |

| 11 | Provident fund | Minimum corpus of ₹25 crore |

| 12 | Pension fund | Minimum corpus of ₹25 crore |

| 13 | Systemically important NBFC | Net worth ≥ ₹500 crore |

Additional eligible entities include the National Investment Fund and insurance funds managed by the armed forces or Department of Posts.

QIB status flows from institutional structure, regulatory registration, and financial scale. SEBI allocates the majority of a book-built issue to this category because these entities are expected to conduct independent due diligence — and are accountable for it.

How the QIB Allotment Process Works

The end-to-end process follows a defined sequence:

- Company files DRHP with SEBI

- SEBI issues observations

- Roadshows build institutional interest

- Anchor investors are allocated shares one business day before the public window

- Three-day subscription window opens for all categories

- Book is analysed and cut-off price finalised

- Proportionate allotment is calculated for QIBs

- Shares credited to demat accounts by T+2; trading commences T+3 (mandatory under SEBI Circular SEBI/HO/CFD/TPD1/CIR/P/2023/140 from December 1, 2023)

The Book Running Lead Manager (BRLM) is responsible for mapping institutional demand before the DRHP is filed, conducting roadshows, and managing bid collection. An investment bank with deep institutional relationships and real-time book visibility reduces the risk of QIB subscription falling short of SEBI thresholds.

S45's pre-mandate Demand Thesis Report — delivered within 24 hours — maps cohort-level QIB demand across domestic mutual funds, FPIs, insurance companies, and pension funds before any engagement letter is signed. Founders see which cohorts are likely to participate and at what scale before deciding whether to proceed.

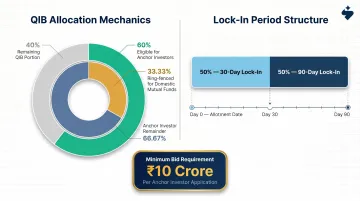

Step 1: Anchor Investor Allocation

Up to 60% of the QIB portion may be allotted to anchor investors — large, reputable QIBs — one business day before the subscription window opens.

Key rules:

- Minimum bid size: ₹10 crore per anchor investor

- One-third of the anchor portion is ring-fenced for domestic mutual funds

- Mandatory split lock-in: 50% of anchor allotment locked for 30 days, remaining 50% locked for 90 days from allotment date (revised effective April 2022, replacing the earlier uniform 30-day lock-in)

- Anchor allocations must be publicly disclosed, setting a credibility benchmark for the broader market

Step 2: Subscription Window and Bid Collection

The three-day bidding window is when QIBs submit bids specifying quantity and price within the declared band. A few important mechanics:

- Live subscription data for each category (QIB, NII, retail) is published on BSE and NSE throughout the window

- QIBs may revise bids upward within the band but cannot withdraw or lower bids — this asymmetric rule ensures QIB bids provide a reliable floor for price discovery

- Only bids at or above the eventual cut-off price qualify for allotment

During this window, S45's Demand Map provides real-time subscription multiples by QIB sub-category — Domestic Mutual Funds, FPI/Global, Insurance Companies, Pension Funds — alongside NII and retail participation, giving issuers and the Lead Manager live visibility into book composition.

Step 3: Cut-Off Price Finalisation and Proportionate Allotment

After the window closes, the BRLM analyses the collected book to determine the cut-off price — the price at which total valid bids equal or exceed the total issue size.

For the QIB category specifically:

- Allotment is proportionate, not a lottery

- Example: If the QIB portion is 1 crore shares and total valid QIB bids are for 5 crore shares, each bidder receives one-fifth of their bid quantity

- A separate 5% ring-fence within the non-anchor QIB portion is reserved for domestic mutual funds

QIB Quota and Allocation Rules Under SEBI ICDR

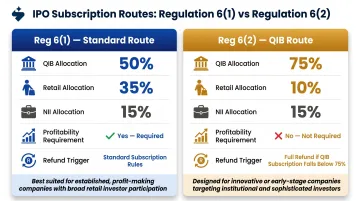

The regulatory framework divides into two distinct routes:

| Parameter | Regulation 6(1) — Standard Route | Regulation 6(2) — QIB Route |

|---|---|---|

| QIB allocation | Minimum 50% of net offer | Minimum 75% of net offer |

| Retail (RII) | Minimum 35% | Maximum 10% |

| NII allocation | Minimum 15% | Maximum 15% |

| Profitability required? | Yes — track record criteria | No — for companies that cannot meet Reg 6(1) |

| Refund trigger | Standard minimum subscription rules | Full refund if QIB subscription < 75% |

NII Sub-Category Rules

Of the 15% reserved for Non-Institutional Investors (under both routes):

- One-third goes to applicants applying for shares worth ₹2 lakh to ₹10 lakh

- Two-thirds goes to applicants applying above ₹10 lakh

- Allotment within NII sub-categories is by draw of lots (not proportionate), mirroring the retail process

- If either sub-category is undersubscribed, unallotted shares transfer to the other

Reallocation Mechanics

SEBI's reallocation rules are designed to keep a well-subscribed issue from failing on technicalities:

- Undersubscribed retail portions transfer to NII (and vice versa) under Reg 48

- Within the QIB pool, mutual funds absorb remaining shares if their ring-fenced 5% sub-tranche goes unfilled

- Cross-category reallocation only flows between retail and NII — the QIB pool stays separate

Under Reg 6(2), however, the QIB portion cannot be diluted through reallocation — the 75% threshold is an absolute gate.

SEBI's Proposed Changes for Large IPOs

In July 2025, SEBI issued a consultation paper proposing to increase QIB allocation from 50% to 60% (in a graded manner) for IPOs exceeding ₹5,000 crore, while reducing the retail portion from 35% to 25% and raising the domestic mutual fund ring-fence from 5% to 15%. The SEBI Board approved the framework in September 2025. Founders planning large mainboard IPOs above ₹5,000 crore need to account for this shift in category sizing — specifically the tighter retail window and the expanded MF ring-fence — when modelling their distribution strategy ahead of filing.

Common Misconceptions About QIB Allotment

Misconception 1: "High QIB subscription = QIB route IPO"

Every book-built mainboard IPO features QIB participation and can attract heavy institutional demand. The "QIB route" label applies exclusively to Regulation 6(2) filings — companies that explicitly cannot satisfy Reg 6(1) profitability norms. Applying the label to standard IPOs with strong institutional interest creates a false equivalence between companies with very different financial profiles.

Misconception 2: "QIBs are locked in post-listing"

Only anchor investors carry a mandatory lock-in — 50% for 30 days, 50% for 90 days. Non-anchor QIBs face no lock-in whatsoever and can sell their allotted shares from the first day of trading. Founders should plan for potential institutional selling pressure from listing day rather than assuming QIB allotment guarantees long-term holding.

Misconception 3: "The QIB route is always the superior path for high-growth companies"

The Reg 6(2) path only works if genuine, mappable QIB demand exists before the DRHP is filed. The mandatory refund clause is binary: if QIBs don't subscribe 75% of the net offer, the entire IPO is cancelled. For companies whose sector, scale, or institutional relationships cannot support this threshold, the SME IPO route (BSE SME or NSE Emerge) is typically the more appropriate and less risky path, with a 2–3 month execution timeline and materially lower institutional demand requirements.

Misconception 4: "QIB allotment signals profitability"

Under Reg 6(2), several well-known companies listed while loss-making. Delhivery reported restated losses of ₹1,011 crore in FY2021; Nykaa's prospectus explicitly confirms the offer was made under Reg 6(2). QIB allotment signals institutional conviction and the depth of due diligence behind the subscription — not that the company is profitable.

Using QIB subscription levels as a proxy for financial health, without reading the DRHP, is a reasoning error the regulatory framework itself cautions against.

Frequently Asked Questions

What does QIB mean in IPO?

QIB stands for Qualified Institutional Buyer — a category of large, SEBI-recognised institutional investors including mutual funds, banks, insurance companies, and FPIs. They receive the majority allocation in every book-built IPO, making them better placed to assess investment risk independently.

What is the QIB quota for IPO?

Under the standard Regulation 6(1) route, a minimum of 50% of the net offer is reserved for QIBs. Under Regulation 6(2) — for companies that cannot meet SEBI's profitability norms — this rises to at least 75%, with the retail portion capped at 10%.

What is book-building in a prospectus?

The Red Herring Prospectus (filed before the subscription window opens) discloses the price band, investor category allocation percentages, issue size, and bookbuilding mechanics. The final issue price is not in the RHP — it is discovered through bidding and confirmed only in the final prospectus filed after allotment.

When can QIBs sell IPO shares?

Non-anchor QIBs have no lock-in and can sell from listing day. Anchor investors — allotted shares one day before the IPO opens — are subject to a mandatory split lock-in: 50% locked for 30 days and 50% locked for 90 days from the date of allotment.

Can I apply for an IPO in the QIB category?

Individual retail investors cannot apply under the QIB category. QIB eligibility is restricted to specific institutional entities defined under Regulation 2(1)(ss). Individuals invest under the Retail Individual Investor (RII) category, or the Non-Institutional Investor (NII) category if applying above ₹2 lakh.

What is the difference between RHP and DRHP?

The DRHP is filed with SEBI for review and contains financials, risk factors, and proposed issue structure — but no final price. The RHP is filed after SEBI observations and opens the subscription window with the price band disclosed. The final prospectus, filed post-allotment, confirms the cut-off price.