Introduction

The QIB route represents a critical yet poorly understood pathway to India's Mainboard IPO markets. Formally known as Regulation 6(2) of SEBI ICDR Regulations 2018, this alternative listing mechanism was designed specifically for companies that cannot satisfy the standard profitability criteria under Regulation 6(1). While the standard route requires an average operating profit of at least ₹15 crore across three preceding financial years, the QIB route allows pre-profit and marginally profitable companies to access public markets — provided they can secure at least 75% of the net offer from Qualified Institutional Buyers.

For founders of high-growth, asset-light companies — particularly in technology, SaaS, and new-age sectors — that three-year profitability requirement is the barrier. The QIB route exists specifically for them.

Yet confusion persists. Founders conflate "QIB participation" with the "QIB route." Investors mistake the allocation structure for a stamp of profitability. Commentators routinely misapply the label to standard Mainboard IPOs that simply attracted strong institutional interest.

That confusion has real consequences — for pricing, for investor expectations, and for listing outcomes. This guide cuts through it: regulatory structure, allocation mechanics, real-world examples, and the thresholds that determine whether the QIB route is viable or simply the wrong tool for the job.

Key Takeaways

- Regulation 6(2) lets companies that miss SEBI's profitability norms list on the Mainboard — if 75% of the net offer goes to QIBs

- QIBs include mutual funds, banks, insurance companies, FPIs (excluding individuals/family offices), and pension funds with ₹25 crore+ corpus

- Allocation split under QIB route: 75% QIBs / 15% NIIs / 10% retail, versus the standard 50/15/35 for eligible companies

- If QIB subscription falls below 75%, the IPO is cancelled and all application money is refunded

- Real examples: Tracxn, Awfis, Unicommerce, and RateGain all listed this way, pre-profit or marginally profitable

What Is the QIB Route in an IPO?

The QIB route is the mechanism under Regulation 6(2) of SEBI ICDR Regulations 2018 that permits a company to pursue a Mainboard IPO without satisfying the Regulation 6(1) profitability requirement. Instead of demonstrating an average operating profit of at least ₹15 crore over three preceding financial years, the company commits to allot a minimum of 75% of the net offer to Qualified Institutional Buyers through the book-building process.

One common point of confusion: QIBs participate in all book-built Mainboard IPOs. The "QIB route" specifically refers to the Reg 6(2) alternative pathway for companies ineligible under Reg 6(1). Conflating the two leads to misreading a company's financial health at listing. A high QIB subscription in a standard IPO does not make it a "QIB route IPO" — only a Reg 6(2) filing does.

SEBI's standard profitability norms protect retail investors but inadvertently shut out innovative, asset-light, high-growth companies that lacked a profit track record despite strong institutional backing. The QIB route resolves this tension by limiting retail exposure to 10% and placing the due diligence burden on institutional investors who conduct independent analysis before committing capital.

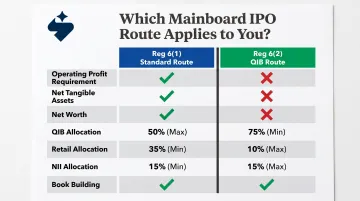

Regulation 6(1) vs Regulation 6(2): What Changes?

| Parameter | Reg 6(1) Standard Route | Reg 6(2) QIB Route |

|---|---|---|

| Operating Profit Requirement | ₹15 crore average over 3 years | Not required |

| Net Tangible Assets | ₹3 crore in each of 3 years | Not required |

| Net Worth | ₹1 crore in each of 3 years | Not required |

| QIB Allocation | Minimum 50% | Minimum 75% |

| Retail Allocation | Minimum 35% | Maximum 10% |

| NII Allocation | Minimum 15% | Maximum 15% |

| Book Building | Optional | Mandatory |

| Refund if QIB threshold unmet | N/A | Mandatory full refund |

A company that already satisfies Reg 6(1) has no reason to opt for the QIB route — doing so would needlessly reduce retail allocation and add institutional gatekeeping where none is required.

Who Qualifies as a QIB Under SEBI ICDR?

SEBI recognises 13 entity types as QIBs under Regulation 2(1)(ss):

- Mutual funds, AIFs, venture capital funds, and foreign VCFs registered with SEBI

- Foreign portfolio investors (excluding individuals, corporate bodies, and family offices)

- Public financial institutions

- Scheduled commercial banks

- Multilateral and bilateral development financial institutions

- State industrial development corporations

- IRDAI-registered insurance companies

- Provident funds with minimum corpus of ₹25 crore

- Pension funds with minimum corpus of ₹25 crore

- National Investment Fund

- Insurance funds managed by the Indian armed forces or Department of Posts

- Systemically important NBFCs

QIBs carry the financial depth and analytical infrastructure to assess risk without regulatory hand-holding. SEBI requires no minimum application amount from them but entrusts them with the majority allocation in a Reg 6(2) issue — a deliberate design choice that keeps retail investors shielded from companies that haven't yet proven profitability.

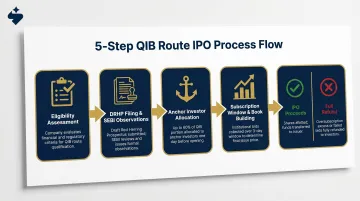

How the QIB Route Works: Step-by-Step

Unlike a fixed-price issue, shares in a QIB route IPO are not pre-priced — the final issue price emerges from demand within a declared price band. The entire process from eligibility assessment to listing typically takes 6–12 months and involves a licensed merchant banker or investment bank at every stage.

Step 1: Eligibility Assessment and Route Selection

Before filing, the company — working with its investment bank — conducts a formal eligibility review. If it cannot satisfy Reg 6(1) profit criteria but has strong institutional fundamentals (business model, growth trajectory, sector tailwinds), the QIB route becomes viable.

This is a strategic decision that requires honest demand mapping. Proceeding without genuine QIB interest is structurally risky — the refund clause creates real downside, and founders who proceed without a banker who can credibly map QIB demand before SEBI filing are taking on unnecessary execution risk.

Step 2: DRHP Filing and SEBI Observations

The Draft Red Herring Prospectus (DRHP) is filed with SEBI disclosing the Reg 6(2) route, issue structure, price band indicatives, and use of proceeds. SEBI reviews and typically issues observations within 30 days. QIBs independently scrutinise this document before bidding — any gap in disclosure will be caught and will hurt demand.

Step 3: Anchor Investor Allocation (One Day Before Opening)

Up to 60% of the QIB portion may be allotted to anchor investors — a defined sub-category of QIBs — one day before the IPO subscription opens to the public. Anchor investors are subject to a lock-in: 50% of their allotment is locked for 30 days and the remaining 50% for 90 days from the allotment date. Their participation is publicly disclosed and signals confidence to broader institutional and retail investors, drawing additional interest into the issue.

Step 4: Subscription Window and Book Building

During the three-day bidding period, QIBs, NIIs, and retail investors submit bids within the declared price band. The book builds based on price-quantity demand data, and the cut-off price is determined at close based on where sufficient demand exists. QIBs must account for at least 75% of the net offer — which makes institutional participation during these three days the single variable that determines whether the IPO succeeds.

Step 5: Finalisation, Allotment, or Mandatory Refund

This is a binary outcome: if QIBs have subscribed at least 75% of the net offer, allotment proceeds to all investor categories and listing follows. If the 75% threshold is not met, the IPO cannot proceed — the entire subscription amount across all categories must be refunded in full. There is no mechanism for partial listing or revised allocation. For founders, this means QIB conviction must be established well before the subscription window opens — not during it.

Share Allocation Rules Under the QIB Route

The allocation breakdown is:

- Minimum 75% to QIBs (of which a mandatory 5% is ring-fenced for mutual funds and up to 60% can be pre-allocated to anchor investors)

- Up to 15% to Non-Institutional Investors

- Up to 10% to Retail Individual Investors

Compare this with the standard Mainboard allocation of 50% QIBs, 15% NIIs, and 35% retail. The difference reflects a deliberate structural choice about which investor category absorbs primary demand under Reg 6(2).

NII Sub-Category Rule

Of the 15% reserved for NIIs:

- One-third is set aside for investors applying for shares worth ₹2 lakh to ₹10 lakh

- Two-thirds for applications above ₹10 lakh

If either sub-category remains undersubscribed, the unallotted shares can be transferred to the other sub-category.

Reallocation Mechanics for Undersubscribed Categories

When a category closes undersubscribed, SEBI's reallocation rules keep the issue on track:

- Unallocated retail shares transfer to the NII category, and vice versa

- Mutual funds can absorb remaining shares from the broader QIB pool

- Technical shortfalls in smaller categories do not derail an otherwise well-subscribed issue

Practical Implication for Retail Investors

The 10% retail cap means that in a heavily subscribed QIB route IPO, competition for retail allotment is far more intense than in a standard issue. Retail oversubscription of 50x or more is common in well-known QIB route listings, significantly reducing per-applicant allotment probability.

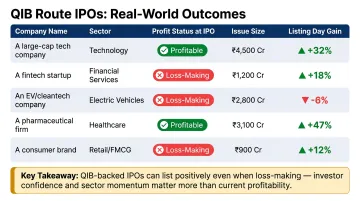

Real-World Examples: Companies That Took the QIB Route

The QIB route has attracted a range of growth-oriented businesses in India — pre-profit or marginally profitable at listing, but with credible institutional backing and scalable business models.

| Company | Sector | Profit Status at IPO | Issue Size (₹ Cr) | Listing Day Gain |

|---|---|---|---|---|

| RateGain Travel Technologies | SaaS / Travel Tech | Loss-making (₹-28.58 Cr FY21) | 1,335.74 | -15.29% |

| Tracxn Technologies | Marketplace Intelligence | Loss-making (₹-4.85 Cr FY22) | 309.38 | +16.69% |

| Awfis Space Solutions | Flexible Workspace | Loss-making (₹-18.94 Cr Dec 2023) | 598.93 | +13.58% |

| Unicommerce eSolutions | E-commerce Enablement | Profitable (₹13.08 Cr FY24) | 276.57 | +117.59% |

| Quadrant Future Tek | Railway Technology | Mixed (₹-12.11 Cr H1 FY25) | 290.00 | +28.97% |

What the data shows:

- Strong institutional demand drove solid listing gains even for companies that were loss-making at filing — RateGain being the notable exception

- The QIB route does not guarantee listing gains — outcomes depend on sector sentiment, pricing discipline, and the quality of bookbuilding

- SEBI's Reg 6(2) pathway applies across sectors — SaaS, workspace, e-commerce, and railway technology all qualify, provided the business model and institutional interest are present

Common Misconceptions and When the QIB Route Doesn't Apply

"QIB Route" Is Routinely Conflated with "An IPO That Has Strong QIB Subscription"

These are different things. A high QIB subscription in a regular book-built IPO (under Reg 6(1)) does not make it a "QIB route IPO." The QIB route label only applies to Reg 6(2) issues where the company has explicitly opted for the alternative pathway because it cannot satisfy profitability norms. Applying the label incorrectly creates false equivalence between companies with different financial profiles.

The Lock-In Misconception

QIBs (other than anchor investors) are not subject to any lock-in period and can sell their allotted shares from the first day of listing. Only anchor investors carry a mandatory split lock-in (30/90 days from allotment date).

Institutional exits can begin on listing day, which can create price pressure. Founders should not assume QIB participation implies long-term holding.

When the QIB Route Is Unnecessary or Unsuitable

These misconceptions point to a broader pattern: the QIB route is neither universal nor always advantageous. Two situations call it into question:

- Unnecessary: The company already meets Reg 6(1) profitability criteria — opting for this route only reduces retail allocation without benefit

- Unsuitable: The company's sector, scale, or institutional relationships make 75% QIB demand unlikely — the refund risk makes this route structurally dangerous, and BSE SME or NSE Emerge is the more appropriate path

Frequently Asked Questions

What is the QIB route in an IPO and what is the role and eligibility of QIBs?

The QIB route is the Regulation 6(2) pathway for Mainboard IPOs where companies skipping profitability criteria commit at least 75% of the net offer to QIBs. QIBs include mutual funds, banks, insurance companies, AIFs, FPIs (excluding individuals and family offices), and pension/provident funds with ₹25 crore corpus.

Can QIBs sell their IPO shares on listing day or is there a lock-in period?

QIBs (excluding anchor investors) face no lock-in and can sell allotted shares from listing day. Only anchor investors — a defined sub-category of QIBs — are subject to a split lock-in: 50% for 30 days and 50% for 90 days from the date of allotment under SEBI rules.

What are the IPO allocation categories (QIB, HNI/NII, Retail) and what are the limits for each?

Under the QIB route (Reg 6(2)), the split is 75% QIBs, 15% NIIs, and 10% retail. In contrast, a standard Mainboard book-built IPO under Reg 6(1) allocates 50% QIBs, 15% NIIs, and 35% retail.

What happens if the QIB portion in an IPO is not fully subscribed?

If QIBs do not subscribe at least 75% of the net offer in a Reg 6(2) IPO, the issue cannot proceed and all application money across all investor categories must be refunded in full. Partial listing or adjusted allocation is not permitted under SEBI rules.

How does QIB participation affect IPO pricing and post-listing stock performance?

Strong QIB subscription signals institutional confidence and supports price discovery, generating positive market sentiment that typically drives broader oversubscription. Since QIBs have no lock-in, however, early institutional selling post-listing can suppress prices.

Is there a 15×15×30 rule for retail IPO allotment?

No SEBI regulation or exchange rule defines a "15×15×30 rule" for IPO allotment. In oversubscribed IPOs, retail allotment runs through a computerized lottery where each valid single-lot application has an equal chance of selection. Under the QIB route, with only 10% allocated to retail (versus 35% in a standard IPO), the smaller retail pool means allotment odds are proportionally lower.