Introduction

Picture this: you're scrolling through financial news and see a much-hyped IPO making headlines. You want to apply, but the application form is filled with confusing terms: RII, NII, HNI, sHNI, lot sizes, and ASBA. Which category do you fall into? How much can you invest? Will you actually get shares?

The answer starts with understanding where you fit. India's IPO market operates under a SEBI-mandated framework that divides all applicants into distinct investor categories — and retail investors have a clearly defined, protected place in that system, with guaranteed reservations and allotment rules designed to level the playing field.

By the time you finish reading, you'll know exactly which category applies to you, how allotment works when an issue is oversubscribed, and what to watch for before you apply.

Key Takeaways

- Retail Individual Investors (RII) apply for IPO shares worth up to ₹2 lakh and receive 35% reservation in every mainboard IPO

- India divides IPO investors into RII, NII (including sHNI and bHNI), and QIB categories with different rules for each

- Retail allotment uses a computerised lottery when oversubscribed, giving every applicant equal odds regardless of bid size

- Benefits include reserved allocation and equal lottery probability in oversubscribed issues

- Risks include nil allotment in high-demand IPOs and potential listing-day losses

Who Is a Retail Investor in an IPO?

A Retail Individual Investor (RII) in India is any individual—resident or NRI—who applies for IPO shares with a total application value of up to ₹2 lakh. This classification is purely based on the size of your application, not your income, net worth, or investment experience.

Concrete example: If you're a salaried professional applying for 10 shares at ₹180 each (total bid: ₹1,800), you qualify as a retail investor regardless of your total wealth. The ₹2 lakh threshold applies per IPO application, not across multiple IPOs.

What Retail Investors Are NOT

Retail investors are distinct from:

- QIBs (Qualified Institutional Buyers): Mutual funds, insurance companies, FIIs, and banks that invest institutional capital

- NIIs (Non-Institutional Investors): Individuals, HUFs, or entities bidding above ₹2 lakh

The RII classification is application-based, not investor-profile-based. The same person can apply as RII in one IPO (₹1.5 lakh bid) and NII in another (₹5 lakh bid).

Why SEBI Created the Retail Category

That application-based flexibility is intentional. SEBI established this protected bucket to ensure smaller investors aren't crowded out by institutional capital. By ring-fencing 35% of every mainboard issue for retail investors, the regulator gives ordinary individuals a dedicated pool — you're not competing directly against mutual funds or high-net-worth investors for the same allocation.

Two groups often overlooked also qualify under the retail category:

- Hindu Undivided Families (HUFs) can apply under the retail category, subject to the same ₹2 lakh cap

- NRIs with NRE/NRO bank accounts can participate as retail investors without requiring PIS permission

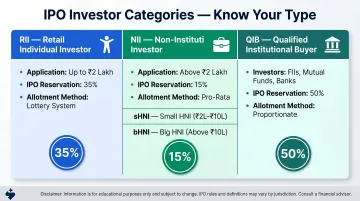

IPO Investor Categories in India: RII, NII, HNI, sHNI, and QIB

SEBI mandates three primary investor buckets for mainboard book-built IPOs, each with defined share reservations:

| Category | Application Size | Reservation | Allotment Method |

|---|---|---|---|

| RII (Retail) | Up to ₹2 lakh | 35% minimum | Lottery (draw of lots) |

| NII (Non-Institutional) | Above ₹2 lakh | 15% minimum | Min lot via lottery, then pro-rata |

| QIB (Institutional) | Institutional investors | 50% maximum | Proportionate/discretionary |

Note: For loss-making companies following the QIB route (Regulation 6(2)), the split changes to QIB ≥75%, NII ≤15%, RII ≤10%.

QIBs (Qualified Institutional Buyers)

QIBs include mutual funds, foreign institutional investors, insurance companies, and scheduled commercial banks. These investors:

- Receive the largest allocation (up to 50% of the issue)

- Don't apply through ASBA like retail investors

- Get discretionary allotment, with anchor investors receiving shares before the issue opens

- Drive market perception — heavy QIB participation is widely read as a vote of confidence in the issuer's pricing

NIIs (Non-Institutional Investors)

NIIs are individuals, companies, HUFs, or trusts applying for more than ₹2 lakh. Effective April 1, 2022, SEBI subdivided this category to improve fairness:

| Sub-Category | Application Range | NII Bucket Share | Notes |

|---|---|---|---|

| sHNI (Small HNI) | ₹2 lakh – ₹10 lakh | 1/3 (~5% of net offer) | Shielded from being crowded out by larger bids |

| bHNI (Big HNI) | Above ₹10 lakh | 2/3 (~10% of net offer) | Often uses NBFC financing to maximise bid size |

If either sub-category is undersubscribed, leftover shares flow to the other.

RIIs (Retail Individual Investors)

RIIs are individual investors applying within the ₹2 lakh ceiling — the category this guide covers in depth. Key characteristics:

- Apply up to ₹2 lakh per IPO

- Receive 35% reservation on mainboard issues

- Must pay full application amount upfront via ASBA/UPI

- Get allotment through computerised lottery if oversubscribed

- Can bid at cut-off price (unlike NIIs)

How IPO Allotment Works for Retail Investors

Retail allotment operates on two-scenario logic:

Scenario 1: Undersubscribed Retail Portion Every retail applicant receives their full applied quantity. Simple and straightforward.

Scenario 2: Oversubscribed Retail Portion SEBI mandates a computerised lottery where:

- Each valid applicant receives maximum one lot

- Applying for 10 lots gives you the same lottery odds as applying for 1 lot

- Lots are distributed randomly until reserved shares are exhausted

- No preference for larger bids within the retail category

Understanding "One Lot" Maximum

When the retail portion is oversubscribed, SEBI requires that as many unique investors as possible receive at least one lot. A "lot" is the minimum tradeable unit set by the company in the prospectus.

Bidding for multiple lots does NOT increase your allotment chances in an oversubscribed IPO. You still receive only one lottery entry for one lot maximum.

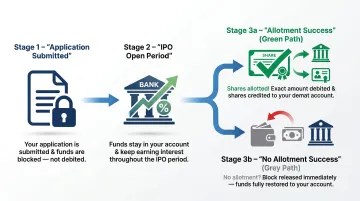

The ASBA Process

Application Supported by Blocked Amount (ASBA) is mandatory for all IPO applications:

- Your bid amount is blocked in your bank account, not debited

- Funds remain in your account earning interest until allotment

- If you don't receive shares, the block is released immediately

- If allotted, funds are debited and shares credited to your demat account before listing

This mechanism protects investors from float risk — your capital is never transferred to the issuer unless you actually receive shares.

After Allotment: Listing Day Dynamics

Once allotment is finalized (typically within T+3 days of issue close):

- Successful applicants receive shares in their demat account before listing

- Unsuccessful applicants get their blocked funds released

- Listing day performance depends on pricing discipline and market conditions

Pricing discipline at the issuer level directly shapes what retail investors realize on Day 1. S45's 43% average listing pop across 26 IPOs reflects how accurate demand mapping — rather than aggressive pricing — tends to deliver better outcomes for lottery winners.

Investment Limits and Eligibility for Retail Investors

The ₹2 Lakh Ceiling

The maximum application value for retail category is ₹2,00,000 per IPO, calculated as:

(Number of shares applied) × (Issue price or upper end of price band)

This limit applies per PAN. Only one application per PAN is permitted in any given IPO—multiple applications are treated as duplicates and rejected.

Spouses, children, and other family members with separate PANs can each apply independently as retail investors up to ₹2 lakh, effectively multiplying household participation.

Note: Applications above ₹2 lakh but up to ₹5 lakh submitted via UPI are automatically categorized under NII, not retail.

Minimum Investment

The minimum investment is one lot. Lot sizes vary by company and are specified in the prospectus.

| IPO Type | Typical Minimum Investment |

|---|---|

| Mainboard IPO | ₹14,000 – ₹15,000 |

| SME IPO | Up to ₹1,00,000 |

Eligibility Requirements

To apply for an IPO as a retail investor, you need:

For Resident Indians:

- Valid PAN card

- Demat account with a depository participant

- ASBA-enabled bank account or UPI-linked account (UPI limit: ₹5 lakh per transaction)

For NRIs:

- Valid PAN card

- NRI demat account

- NRE or NRO bank account (no PIS permission required for IPO applications)

- Compliance with FEMA regulations as prescribed by RBI

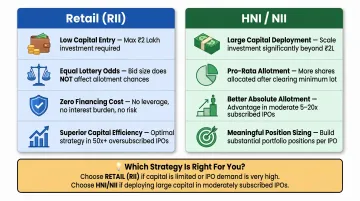

Retail vs HNI in an IPO: Key Differences

The core trade-off between retail and HNI categories comes down to capital commitment vs. allotment probability:

Retail Advantages

- Entry requires ₹2 lakh or less, so you can participate without deploying large capital

- Every retail applicant draws from the same lottery in heavily oversubscribed IPOs — a ₹15,000 bid has identical allotment odds as a ₹2 lakh bid

- Applying with your own funds eliminates financing costs and interest risk

- In IPOs oversubscribed 100x or more, the retail lottery can deliver better risk-adjusted returns per rupee than proportionate HNI allotment

HNI/NII Advantages

- HNIs can deploy ₹10 lakh, ₹50 lakh, or more in a single IPO for meaningful exposure

- After the minimum lot lottery, remaining shares distribute pro-rata — larger bids receive proportionately more shares

- In moderately subscribed IPOs (5–10x, not 100x+), HNI category typically yields better absolute allotment than retail's one-lot ceiling

The Financing Dynamic

Larger deployment is why many HNIs use IPO financing (borrowed funds from NBFCs or banks) to maximize application size and allotment chances. The risks, however, are real:

- RBI caps IPO-related lending at ₹25 lakh per individual borrower

- This leverage amplifies both potential gains and costs (interest on borrowed capital)

- If listing is flat or negative, leveraged HNIs face losses on both principal and interest

Retail investors, limited to ₹2 lakh and typically using their own funds, avoid this leverage risk entirely.

When to Choose Retail vs HNI

Choose Retail when:

- The IPO is expected to be heavily oversubscribed (50x+ demand)

- You have limited capital to deploy (under ₹2 lakh available)

- You want to avoid financing costs and leverage risk

- You're comfortable with lottery odds and potential nil allotment

Choose HNI/NII when:

- You have larger capital to deploy (₹5 lakh+)

- The IPO shows moderate demand (10-20x oversubscription)

- You want proportionate allotment for larger exposure

- You're willing to accept financing costs for potentially higher absolute allocation

Benefits and Risks for Retail Investors in IPOs

Key Benefits

- 35% reservation is ring-fenced exclusively for retail investors on every mainboard IPO — institutions and HNIs cannot touch this portion.

- The lottery system gives every applicant identical odds regardless of wealth. A first-time investor with ₹15,000 competes on the same terms as someone bidding ₹2 lakh.

- One lot (₹14,000–₹15,000 on mainboard) keeps the entry barrier low, without requiring significant capital upfront.

- Buying at the issue price means you get early access before secondary market trading begins, capturing potential listing gains.

- The ASBA mechanism keeps your application money in your own account until allotment — earning interest and fully available if you don't receive shares.

These protections are built into SEBI's framework specifically to level the playing field. That said, the risks are real and worth understanding before applying.

Primary Risks

- Zero allotment in oversubscribed issues: The retail category now averages 24x oversubscription, with some issues hitting 375x. Most applicants walk away empty-handed, with capital blocked for 3–4 days.

- Listing-day losses: About 58.2% of the 115 IPOs launched between January 2025 and March 2026 were trading below their offer price by April 30, 2026. Issuer overpricing hits retail investors hardest, since they lack the research resources institutions bring.

- Limited research access: Retail investors rely primarily on the Red Herring Prospectus (RHP) and public disclosures, while QIBs have direct management access and dedicated analyst coverage.

- Post-listing sell pressure: Retail investors face no lock-in, but selling from other categories — particularly QIBs exiting after anchor lock-up periods — can push prices sharply lower in the first few weeks.

Knowing these risks doesn't mean avoiding IPOs. It means applying with a clear-eyed approach — which is where the following habits make a difference.

Mitigating the Risks

Read the RHP before applying. The Red Herring Prospectus contains audited financials, risk factors, and use of proceeds. SEBI requires it to be available at least 21 days before the issue opens — on SEBI's website, NSE/BSE portals, and lead manager websites.

Look past Grey Market Premium (GMP). GMP reflects unofficial pre-listing sentiment but has no binding relationship to listing performance. Focus on fundamentals: revenue growth, profitability, sector tailwinds, and valuation relative to listed peers.

Check where the money goes. Funds directed toward business expansion signal growth intent. Heavy promoter exit through an Offer for Sale (OFS) warrants more scrutiny. SEBI caps unidentified acquisitions and general corporate purposes at 35% of the fresh issue amount.

Spread applications across multiple IPOs. Concentrating capital in one issue increases the cost of a zero-allotment outcome. Applying across several issues over time improves your probability of consistent allotments.

Frequently Asked Questions

Who is considered a retail investor in an IPO?

Any individual (resident Indian or NRI) applying for IPO shares worth up to ₹2 lakh in a single application qualifies as a Retail Individual Investor (RII) under SEBI's ICDR regulations, regardless of their overall net worth or investment experience.

What is the maximum investment limit for retail investors in an IPO?

The maximum is ₹2,00,000 per application per IPO, calculated at the upper end of the price band. Applying above this limit automatically moves you into the NII/HNI category with different allotment rules and no ability to bid at cut-off price.

How is an IPO allotted to retail investors?

If the retail portion is oversubscribed, SEBI mandates a computerised lottery where each valid applicant receives one entry, capped at one lot, regardless of how many lots they applied for. If undersubscribed, full allotment is made to all applicants.

What are the IPO investor categories (RII, NII, HNI, sHNI, bHNI)?

SEBI divides investors into three main buckets: RII (up to ₹2 lakh, 35% reservation), NII — which includes sHNI (₹2–10 lakh) and bHNI (above ₹10 lakh) with 15% reservation combined — and QIB (institutional buyers) with the remaining 50%.

Which is better, retail or HNI in an IPO?

It depends on expected demand. In heavily oversubscribed IPOs (50x+), retail's lottery system can be more capital-efficient per rupee invested. In moderately subscribed issues (10-20x), HNI's proportionate allotment may yield better results for larger capital deployment.

Can retail investors participate in IPOs?

Yes—SEBI mandates that 35% of every mainboard IPO is reserved exclusively for retail investors. Any individual with a PAN card, demat account, and ASBA/UPI-linked bank account can apply as long as their application doesn't exceed ₹2 lakh.