Introduction

Picture this: you open your trading app and see an IPO with a price band of ₹480–₹500. Three options stare at you — bid at ₹480, bid at ₹500, or select "cut-off price." Most retail investors stall here. Bid too low and your application gets rejected. Bid at the cap and you worry about overpaying — or choose cut-off without knowing exactly what price you're committing to.

That confusion costs investors allotments every IPO season — and with the market moving at this pace, the stakes are rising. India witnessed 80 mainboard IPOs in FY2025, raising ₹1,630 billion — nearly three times the prior year's total, according to KPMG's FY2025 IPO report. With average oversubscription hitting 29x across all categories, understanding how price bands work isn't optional anymore.

This guide covers what a price band actually is, how it gets set, what SEBI mandates, and how to bid smart.

TLDR: Key Takeaways on IPO Price Band

- A price band is the bid range (floor to cap) within which investors must apply in a book-built IPO

- SEBI caps the spread: the cap price cannot exceed 120% of the floor price

- Cut-off price is set after the bidding window closes, based on total demand across all investor categories

- Retail investors can bid at cut-off price, which guarantees allocation at whatever the final price is set

- Bids below the cut-off price are rejected outright

- All successful bidders pay the same cut-off price, regardless of what they bid

What is a Price Band in an IPO?

A price band is the officially declared range within which investors must place bids during a book-built IPO. It has two boundaries:

- Floor price — the minimum permissible bid; no bid below this is accepted

- Cap price — the maximum permissible bid; the upper limit of the range

Any bid outside this range is rejected outright. If the floor is ₹450 and the cap is ₹500, bids at ₹450, ₹470, or ₹500 are all valid. A bid at ₹420 is automatically invalid.

The Cut-Off Price Explained

The cut-off price is the single final issue price discovered after evaluating all bids submitted during the subscription window. It always falls within the price band — at or between the floor and cap.

Retail investors who select "cut-off price" agree to pay whatever final price is discovered. Their bank account is blocked at the cap price; if the cut-off lands lower, the difference is refunded via ASBA.

Per SEBI's September 2024 investor behaviour study, approximately 90% of retail applications are placed at the cut-off price — which makes it the practical default for most applicants.

Once pricing is finalised, the shares move to exchange listing — where an entirely different price discovery begins.

Price Band vs. Listing Price

These two are frequently confused, but they govern entirely different phases:

| Term | Phase | Determined By |

|---|---|---|

| Price Band | IPO subscription (pre-listing) | Company + BRLM, regulated by SEBI |

| Issue / Cut-off Price | End of subscription window | Book-building demand |

| Listing Price | First day of trading | Open market supply and demand |

The average listing-day gain for mainboard IPOs in FY2025 was 29% over the issue price — the market, on day one, often prices shares sharply above what was set in the price band weeks earlier.

How Does the IPO Price Band Work? The Book-Building Process

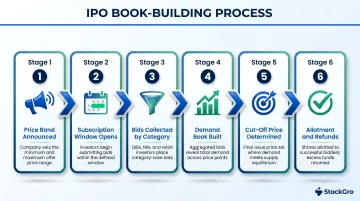

Step-by-Step: From Band Announcement to Allotment

- Price band announced — Published at least two working days before the IPO opens, in the same newspapers as the pre-issue advertisement

- Subscription window opens — Typically runs for 3 working days (10 AM to 5 PM daily)

- Bids collected — Retail investors (RIIs), Non-Institutional Investors (NIIs), and Qualified Institutional Buyers (QIBs) submit bids specifying price and number of lots

- Demand book built — The Book Running Lead Manager aggregates all bids to see demand at each price point

- Cut-off determined — After the window closes, the BRLM and company review the demand book and set the final price where the issue is fully subscribed

- Allotment and refunds — Successful bids receive shares at the cut-off price; rejected bids have funds unblocked via ASBA

Illustrative Demand Book Example

Here's how cut-off price discovery works in practice — the figures below are illustrative:

| Bid Price | Shares Demanded | Cumulative Demand | Issue Size |

|---|---|---|---|

| ₹500 (cap) | 40,00,000 | 40,00,000 | 30,00,000 |

| ₹490 | 25,00,000 | 65,00,000 | 30,00,000 |

| ₹480 | 18,00,000 | 83,00,000 | 30,00,000 |

| ₹470 (floor) | 12,00,000 | 95,00,000 | 30,00,000 |

In this scenario, the issue is fully subscribed even at ₹500 — so the cut-off is set at ₹500. All bids at ₹490, ₹480, and ₹470 are rejected. Everyone who bid ₹500 (or chose cut-off) pays ₹500.

Price discovery doesn't happen in isolation — who gets allocated shares at that cut-off price is equally regulated. SEBI mandates specific allocation percentages in mainboard book-built IPOs:

Investor Category Reservations

- QIBs — up to 50% of the net offer

- NIIs — minimum 15% of the net offer

- Retail Individual Investors (RIIs) — minimum 35% of the net offer

QIBs and NIIs must bid at a specific price within the band. Only RIIs can bid at the cut-off price — meaning they'll pay whatever the final price is, up to the cap.

Book-Building vs. Fixed Price Issues

In a fixed price IPO, the company sets one price upfront — no bidding range, no price discovery. The company only learns actual demand after the issue closes. Most mainboard IPOs in India use the book-building route; some SME IPOs may use fixed pricing under SEBI ICDR provisions that permit either method. For a growth-stage company deciding which path to take, the book-building route gives management far more pricing control — and far more information about who actually wants to own the stock.

Who Decides the IPO Price Band and How Is It Calculated?

The Key Parties

The price band is jointly determined by the issuer (the company going public) and its Book Running Lead Manager (BRLM) — the investment banker mandated to manage the IPO. SEBI doesn't prescribe the exact price, but regulates the process and the maximum permissible spread.

Per Regulation 28 of SEBI ICDR 2018: "The issuer may determine the price of equity shares...in consultation with the lead manager(s) or through the book building process."

Valuation Inputs BRLMs Use

Setting a price band requires judgment, not just formulas. BRLMs draw on several financial inputs:

- P/E comparison — The company's earnings per share (EPS) is benchmarked against listed peer companies' price-to-earnings multiples to derive an implied value range

- EV/EBITDA — Enterprise value relative to operating cash flow, useful for capital-intensive businesses

- Price-to-Book (P/B) — Common in financial services and asset-heavy sectors

- DCF analysis — Projects free cash flows and discounts them to estimate intrinsic value; most useful when earnings visibility is strong

- Peer transaction analysis — Recent IPO pricing in the same sector provides a real-time market reference

The DRHP's "Basis for Issue Price" section discloses the financial ratios computed at both the floor and cap price — a SEBI requirement under Regulation 29(5).

The Role of Roadshows and Pre-IPO Soundings

Before finalising the band, BRLMs conduct pre-IPO roadshows with institutional investors. Their feedback on valuation — which cohorts are interested, at what price, and at what ticket size — directly shapes where the band lands. Too high a band risks under-subscription; too conservative and the company leaves money on the table.

Some banks start this demand intelligence work before mandate signing. S45, for instance, runs a pre-mandate Demand Thesis that maps cohort-level signals across 50,000+ investors — scored by mandate fit, peer holdings, and historical participation. By the time the band is formally set, it reflects actual investor appetite across sub-categories. S45's Live Pricing Band dashboard then tracks floor price, cap, and indicated price in real time as bids update during the bookbuild — rather than relying on a static spreadsheet updated manually.

Market Conditions as a Real Factor

Overall market sentiment matters. In a strong bull phase with active peer IPOs, issuers can often price more aggressively. In volatile conditions, BRLMs typically set a more conservative band — or use the full 20% spread — to build in a buffer for demand uncertainty.

SEBI Rules That Govern the IPO Price Band

Regulation Mapping: Mainboard vs. SME

A common error in financial content is citing Regulations 248–251 for all IPOs. These apply only to SME IPOs under Chapter IX of SEBI ICDR 2018. Mainboard IPOs are governed by Regulations 27–30 under Chapter II, Part VII. The provisions are substantively identical, but precision matters.

| Provision | Mainboard | SME | What It Covers |

|---|---|---|---|

| Face value disclosure | Reg 27 | Reg 248 | Face value in all documents, identical font size |

| Price determination | Reg 28 | Reg 249 | Issuer + lead manager, per Schedule XIII |

| Price band rules | Reg 29 | Reg 250 | 20% cap, 2-day advance notice, financial ratios |

| Differential pricing | Reg 30 | Reg 251 | Up to 10% discount for retail/employees |

The 20% Cap Rule

Per Regulation 29(2): "The cap on the price band...shall be less than or equal to one hundred and twenty per cent. of the floor price."

In practice: a floor at ₹100 means the cap cannot exceed ₹120. The 20% ceiling keeps the band tight enough for investors to assess fair value without guessing across too wide a range.

The 2-Working-Day Announcement Rule

If the price band isn't included in the Red Herring Prospectus, it must be announced at least two working days before the IPO opens — published in the same newspapers as the pre-issue advertisement. The announcement must also include relevant financial ratios at both ends of the band.

This rule connects directly to the 20% cap: SEBI requires both the range and the supporting ratios to be public before bidding opens, so investors can make an informed call at any point within the band.

Differential Pricing for Retail and Employees

SEBI permits issuers to offer shares to retail individual investors and employees at a discount of up to 10% on the final issue price. For example, if the cut-off price is ₹500, retail investors and employees may receive shares at as low as ₹450. This provision is at the issuer's discretion and must be disclosed in the offer documents.

What the Price Band Means for You as an Investor: Bidding Smart

The Cut-Off Price Option — Use It

SEBI allows retail investors (those applying for up to ₹2 lakh worth of shares) to bid at "cut-off price" rather than a specific number within the band. This is the safest strategy in oversubscribed IPOs.

Here's why it matters: In a ₹480–₹500 band, if you bid ₹480 and the cut-off is set at ₹500, your application is rejected. You don't get a "cheaper" entry — you get no entry at all. Bidding at cut-off eliminates this risk entirely.

The mechanics are straightforward: when you select cut-off, your ASBA-linked account is blocked at the cap price. If the final issue price is lower, the difference is unblocked after allotment.

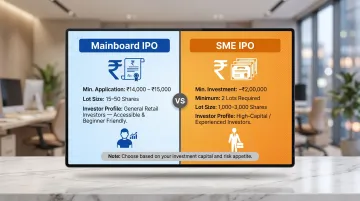

Understanding Lot Sizes

IPOs don't allow you to buy any arbitrary number of shares. You must apply in whole multiples of the minimum lot size, which is set by the company and BRLM and disclosed in the RHP.

- Mainboard IPOs — Minimum application is ₹14,000–₹15,000 (commonly 15–50 shares per lot, depending on issue price)

- SME IPOs — Minimum investment is typically around ₹2,00,000 (minimum 2 lots), with lot sizes ranging from 1,000 to 3,000 shares per lot depending on the issue price. Because SME lot sizes are larger, these IPOs are geared toward investors with higher capital allocation capacity than a typical retail Mainboard application.