Introduction

Many founders approaching their first IPO assume that their audited financials are ready to file. They are not — at least not in the form SEBI requires.

Financial statement restatement means revising previously prepared financials to correct errors, align accounting policies, adopt Ind AS, and meet disclosure standards mandated for a public listing. It is not optional. SEBI ICDR Regulations require every issuer to include restated consolidated financial statements in both the DRHP and the RHP.

India recorded 326 IPO listings in 2024 — 243 SME and 83 Mainboard — with 276 DRHPs already filed for 2025. Every single one of those companies went through this process. Yet many founders still do not fully understand what restatement involves, how long it takes, or what it can uncover.

Miss it, misread it, or underestimate the timeline — and your IPO window closes before you reach the exchange.

Key Takeaways

- Restated financials covering three preceding financial years (plus stub period if applicable) are a mandatory SEBI requirement for every Indian IPO.

- Restatement covers Ind AS adoption, accounting policy alignment, audit qualification resolution, and prior period adjustments — not just error correction.

- Only a CA firm with a valid ICAI Peer Review Certificate can certify restated financials for DRHP submission.

- Issues caught after DRHP filing trigger SEBI comment letters; issues caught before filing can be resolved internally before they escalate.

- Starting restatement 12+ months before your target DRHP date is the single most reliable way to protect your IPO timeline.

What Is Financial Statement Restatement?

Restatement means revising one or more years of financial statements to correct errors in recognition, measurement, presentation, or disclosure — or to apply changed accounting policies consistently across all periods presented.

Big R vs Small r Restatement

Two types matter for IPO preparation:

- Big R restatement — covers material errors requiring reissuance and public disclosure; in a post-listing context, this involves a public announcement and amended filing with the stock exchange.

- Small r restatement — addresses immaterial period-specific errors corrected in the current period via footnote disclosure, without refiling prior statements.

The distinction depends on materiality, as governed by Ind AS 8 (Accounting Policies, Changes in Accounting Estimates and Errors). For IPO purposes, both types can surface during the restatement exercise — and both need to be handled correctly before the DRHP is filed.

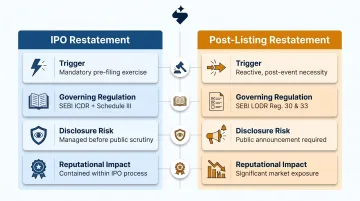

How IPO Restatement Differs from Post-Listing Restatement

This is a distinction founders frequently miss. IPO restatement is a proactive, mandatory preparation exercise — completed before the offer document is filed, not triggered by public scrutiny. It is governed by SEBI ICDR Regulations and Schedule III of the Companies Act, 2013.

Post-listing restatements are a different matter entirely. These are reactive events governed by SEBI LODR Regulations 30 and 33, and they carry significantly higher reputational cost.

| IPO Restatement | Post-Listing Restatement | |

|---|---|---|

| Trigger | Mandatory pre-filing exercise | Reactive correction post-listing |

| Governing regulation | SEBI ICDR + Schedule III | SEBI LODR Reg. 30 & 33 |

| Disclosure risk | Managed before public scrutiny | Public announcement required |

| Reputational impact | Contained within IPO process | Significant market exposure |

Why Restated Financials Are Mandatory for IPO in India

The Regulatory Basis

Regulation 24(1) and Regulation 26(1) of SEBI (ICDR) Regulations, 2018 mandate that the DRHP and the final offer document contain all disclosures specified in Schedule VI. Schedule VI requires restated consolidated financial information, including:

- Restated Statement of Assets and Liabilities

- Restated Statement of Profit and Loss

- Restated Cash Flow Statement

- Significant Accounting Policies and Notes

Without this, the filing is incomplete and SEBI will not accept it.

Mandatory Coverage Period

Restated statements must cover:

- Three full financial years immediately preceding the date of filing, presented per Schedule III of the Companies Act, 2013

- Plus a stub period (prepared under Ind AS 34) if the latest full-year financials are more than six months old at filing date

For example, Shanti Gold International Limited's restated statements covered September 30, 2024, March 31, 2024, March 31, 2023, and March 31, 2022 — three full years plus a stub period.

The Ind AS Requirement

The accounting standard governs how those years are presented. All non-banking, non-insurance Mainboard issuers must present restated financials under Ind AS. Companies still on IGAAP must convert first, then apply SEBI's restatement adjustments on top.

One important exception: companies listing on the SME exchange are not required to adopt Ind AS per the MCA roadmap and may continue using IGAAP. However, any SME company planning a future Mainboard migration should consider early voluntary Ind AS adoption — a full conversion exercise mid-process adds months and cost at the worst possible time.

Who Can Certify Restated Financials

Only a Chartered Accountant firm holding a valid Peer Review Certificate issued by the Peer Review Board of ICAI is authorised to audit and certify restated financials for IPO. From April 1, 2024, this requirement applies to practice units rendering attestation services with four or more partners. Confirm your auditor's peer review status before engaging them for DRHP preparation — if they don't qualify, you're looking at re-tendering the audit, re-issuing work already done, and a filing delay that can run 60–90 days.

How the Financial Statement Restatement Process Works

Restatement for an IPO is not a single event. It is a structured, multi-step process that runs in parallel with legal due diligence, valuation, and DRHP drafting. Industry practice indicates companies typically begin IPO preparation 12 to 18 months in advance of listing — restatement must begin early in that window, not at the end of it.

That timeline explains the sequencing. S45's ≤30-day DRHP drafting timeline starts from a clean data room, which means restated, Ind AS-compliant financials must already be in place before the drafting clock begins. Restatement is a prerequisite to drafting, not something that runs alongside it.

Step 1: Readiness and Gap Assessment

The issuer, auditor, and lead manager jointly review the last three to five years of financial statements to identify:

- Accounting policy inconsistencies across periods

- Unresolved audit qualifications

- Ind AS transition gaps

- Prior period errors

S45's AI Risk Radar surfaces many of these issues during the initial 30-minute readiness scan, flagging inconsistent revenue recognition, unexplained working capital movements, undisclosed contingent liabilities, and tax disputes with material financial impact. Issues identified here can be resolved before SEBI ever sees the filing.

Step 2: Ind AS Conversion (Where Applicable)

For IGAAP companies seeking Mainboard listing, this step involves:

- Restating the opening balance sheet

- Reclassifying financial instruments

- Recognising previously off-balance-sheet items

- Revising revenue recognition policies under Ind AS 115

The shift from AS 9 (risks-and-rewards model) to Ind AS 115's five-step control-based model often causes material timing differences in revenue recognition. Businesses with milestone-based or subscription contracts should quantify this gap before the readiness scan.

Step 3: Applying Restatement Adjustments

The peer-reviewed CA firm applies all required adjustments under SEBI ICDR:

- Correct prior period errors and resolve outstanding audit qualifications

- Apply accounting policy changes retrospectively across all restated periods

- Regroup and reclassify line items to align with current presentation

- Revise accounting estimates where the original treatment reflects error, not a genuine change in judgement

The CA firm documents each adjustment with the period affected and the financial impact per line item, as required under Ind AS 8.

Step 4: Auditor Certification

Once adjustments are finalised, the peer-reviewed CA firm issues an examination report certifying that:

- Statements comply with SEBI ICDR Regulations

- Applicable accounting standards have been applied

- Adjustments have been properly disclosed

This certificate is a required annexure to the DRHP. S45 coordinates directly with auditors for this certification as part of the drafting and regulatory service — including due diligence certificate coordination and audit trail documentation.

Step 5: Integration into the DRHP

The restated financials are incorporated into the Financial Information section of the DRHP alongside a statement of restatement adjustments. That statement must disclose:

- Each adjustment made and the accounting basis for it

- The period(s) affected

- The financial impact per line item

The lead manager reviews all of this for internal consistency before the DRHP is filed with SEBI.

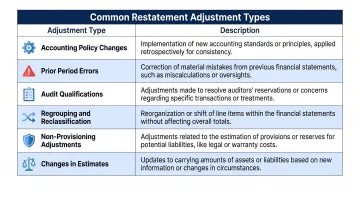

What Are the Common Restatement Adjustments?

Most companies encounter several of these adjustments during the restatement exercise:

| Adjustment Type | What It Involves |

|---|---|

| Accounting policy changes | Standardising policies (revenue, depreciation, inventory) across all periods; applied retrospectively |

| Prior period errors | Correcting mathematical mistakes, misapplied standards, or factual errors; material errors require line-item disclosure per Ind AS 8 |

| Audit qualifications | Resolving qualifications by making required adjustments, or disclosing and explaining those that remain unresolved |

| Regrouping and reclassification | Correcting items presented under wrong line items; particularly common when transitioning from statutory audit format to Schedule III |

| Non-provisioning adjustments | Adequately provisioning doubtful debts, contingent liabilities, and slow-moving inventory that were previously under-provisioned |

| Changes in estimates | Applied prospectively if a genuine change; retrospectively as a prior period error if the original estimate reflected a mistake |

The estimate vs. error distinction is frequently misunderstood. If the company used a conservative depreciation rate due to a calculation error rather than a genuine policy choice, that must be treated as a prior period error — not a prospective change. The auditor's rationale for that classification must be documented in writing — SEBI reviewers and DRHP scrutiny panels will probe exactly this point if the treatment is challenged.

Common Mistakes Companies Make During Restatement

Starting Too Late

The restatement process typically takes three to five months depending on the quality of underlying books. For companies requiring Ind AS conversion, the timeline is longer. Starting only after engaging the lead manager — rather than 12 months before target filing — compresses every subsequent workstream and puts the SEBI observation letter's 12-month validity at risk.

SEBI typically issues its observation letter within 30 days to three months of a complete DRHP filing. If restatement delays push the DRHP past the planned filing date, that 12-month clock shortens accordingly. Miss the window, and the company must refile from scratch.

Treating Restatement as Only an Accounting Exercise

Restatement surfaces issues that affect the entire IPO narrative — related-party transactions, segment reporting, internal control assessments, and revenue recognition. Companies that silo restatement within the finance team miss the chance to resolve these issues coherently before SEBI review. The founding team, legal counsel, and bankers need to align on the narrative early — not after a comment letter arrives.

This is where early AI flagging changes the dynamic. When S45's AI Risk Radar surfaces inconsistent revenue recognition or unexplained working capital movements at the diagnostic stage, all three workstreams can address the issue together — before it hardens into a SEBI observation.

Ignoring Internal Control Implications

A prior period error is not just an accounting adjustment — it is evidence of a gap in internal controls. SEBI and investors treat restated financials as a window into governance quality. Companies should:

- Conduct a root-cause assessment for each restatement adjustment

- Implement corrective controls before the IPO

- Reflect that improvement clearly in the offer document

SEBI and investors want to see that the gap has been identified, fixed, and documented — not explained away. S45's SEBI Query Board tracks each observation to closure with documented evidence, assigning ownership by category: financials to the CFO, governance to legal counsel, and business disclosures to the lead banker. Nothing falls through after filing.

Frequently Asked Questions

What is the process of restatement of financial statements?

Restatement involves reviewing prior-year financials, identifying errors or policy inconsistencies, and making the required adjustments under Ind AS 8. A peer-reviewed Chartered Accountant firm certifies the revised statements and issues an examination report, which is a mandatory annexure to the DRHP.

What requires restatement of financial statements?

The main triggers are SEBI ICDR's mandatory requirement, correction of prior period errors, retrospective accounting policy changes, resolution of audit qualifications, and Ind AS transition adjustments for companies previously reporting under IGAAP.

What does it mean to restate financial statements?

Restating means revising previously prepared financials to present a corrected and standardised view of a company's financial position and performance across multiple periods. For IPO purposes, this must comply with Ind AS and SEBI ICDR disclosure requirements, giving investors a consistent, comparable basis for evaluation.

What are restated financials for IPO?

Restated financials for an IPO are the audited and certified financial statements for the three preceding financial years (plus stub period if applicable), prepared under Ind AS and adjusted per SEBI ICDR Regulations, included in the DRHP and RHP as part of the mandatory financial information section under Schedule VI.

How do you disclose a restatement of financial statements?

Disclosures must include a restatement adjustments statement covering each adjustment, the period affected, and line-item financial impact — with material errors explained in notes to accounts. The auditor's examination report must reference the restatement. Post-listing Big R restatements require a public announcement and amended exchange filing under SEBI LODR Regulations 30 and 33.