Introduction

Most founders don't think about lock-in compliance until after the DRHP is filed. By then, fixing structural gaps means SEBI objections, delayed timelines, and sometimes a complete restructuring of the cap table.

The pre-IPO lock-in period is a SEBI-mandated restriction that prevents certain shareholders—promoters, early investors, and employees—from selling their shares for a set period after listing. It sits at the core of India's IPO framework, yet remains one of the most misunderstood parts of the process.

This guide is for founders preparing for an IPO, pre-IPO investors (HNIs, AIF fund managers), ESOP holders, and SME/Main Board companies approaching listing. Misunderstanding lock-in obligations leads to regulatory non-compliance, failed exit strategies, and post-listing volatility that damages market credibility.

The scale of exposure is significant. 83 lock-in expiries worth approximately $55 billion occurred between May–August 2025 alone — yet studies on Indian IPOs consistently show lock-in expiry has produced little observable impact on share prices when managed correctly.

That outcome depends entirely on whether lock-in structuring was mapped correctly during the pre-filing phase. S45's IPO readiness process identifies compliance gaps before the DRHP is filed — keeping mandates on schedule and free from SEBI review objections.

Key Takeaways

- The pre-IPO lock-in period is a SEBI-mandated restriction on pre-IPO shareholders, not a voluntary arrangement

- Promoters face 18 months on up to 20% of post-issue capital; 6 months on excess shares

- Anchor investors exit in 30–90 days; all other non-promoters are locked in for 6 months from allotment

- Category I and II AIFs holding shares for 6+ months before RHP filing are generally exempt

- Lock-in expiry lifts the legal restriction — shareholders may then sell freely, but no regulation compels them to

What Is the Pre-IPO Lock-In Period?

The pre-IPO lock-in period is the regulatory restriction under SEBI's ICDR Regulations, 2018 that applies to shareholders who held equity in the company before the IPO. These provisions — codified under Regulations 14-17 for Main Board and Regulations 236-239 for SME IPOs — govern when pre-existing shareholders can sell their shares after listing.

Unlike post-IPO mechanisms, the lock-in applies exclusively to pre-existing shareholders and is disclosed upfront in the DRHP and prospectus.

Its core purpose: prevent a sudden flood of insider-held shares from entering the market at listing — a scenario that would suppress the stock price and erode public investor confidence.

Key distinctions:

- Pre-IPO lock-in (Regs. 16-17): Covers promoters and non-promoter pre-IPO shareholders; duration varies by acquisition timing

- Anchor investor lock-in (Reg. 288): A post-IPO mechanism with a 30-90 day split restriction on anchor allocations

- Insider trading blackout (SEBI PIT Regulations): Restricts trading on unpublished price-sensitive information — separate from lock-in rules and applies throughout the company's public life

Each mechanism addresses a different risk window. Understanding which rules apply to which shareholders — and from what date — is where the compliance complexity begins.

Why SEBI Mandates the Pre-IPO Lock-In Period

Market Stability Rationale

When a company lists, only a fraction of total shares are offered to the public. If promoters and early investors could immediately sell their entire holdings, the resulting supply imbalance could crash the stock price and erode retail investor wealth. The lock-in period creates a buffer for the market to establish a fair trading range.

In Main Board IPOs, only 10-25% of total capital typically enters the public float. Without lock-in restrictions, a promoter holding 60% pre-IPO could dump shares immediately. That supply surge would overwhelm demand and trigger panic selling among retail investors who participated in the IPO.

Investor Confidence Rationale

The lock-in period signals to public market investors that promoters and early backers remain committed to the company's long-term growth beyond the listing event. This is particularly important for Indian retail investors participating in SME and Main Board IPOs, who use promoter retention as a signal of conviction.

According to IndiaCorpLaw's analysis of SEBI's November 2025 consultation paper, SEBI views lock-ins as a "credible mechanism" to reinforce market integrity, provide predictability for institutional investors, and support share price stability at listing.

Regulatory Framework and 2021 Amendment

That rationale is backed by hard rules. The lock-in requirement is codified in Regulations 16 and 17 of the SEBI ICDR Regulations, 2018. Regulation 16 governs the lock-in of minimum promoters' contribution, while Regulation 17 governs the lock-in of pre-issue capital held by non-promoters.

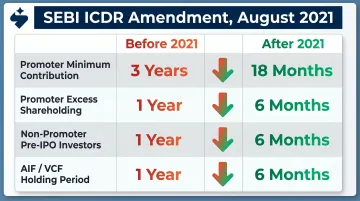

The SEBI ICDR (Second Amendment) Regulations, 2021, notified on August 13, 2021, significantly reduced lock-in durations:

- Promoter minimum contribution: reduced from 3 years to 18 months

- Promoter excess shareholding: reduced from 1 year to 6 months

- Non-promoter pre-IPO investors: reduced from 1 year to 6 months

- AIF/VCF holding period: reduced from 1 year to 6 months from acquisition date

According to the IBA's analysis, SEBI justified the reductions on three grounds:

- The shift from family-run enterprises to professionally managed companies with institutional investors

- The mature business profiles of IPO-bound companies coming to market

- The need to align lock-in norms with India's maturing capital markets

SEBI's Lock-In Guidelines: A Breakdown by Investor Category

Lock-in rules vary significantly depending on investor category, when shares were acquired, and what percentage of post-issue capital is held.

| Investor Category | Lock-In Duration | Regulatory Basis | Start Date |

|---|---|---|---|

| Promoters (up to 20% post-issue capital) | 18 months | Regulation 16, ICDR 2018 (amended 2021) | IPO allotment date |

| Promoters (excess over 20%) | 6 months | Regulation 16, ICDR 2018 (amended 2021) | IPO allotment date |

| Non-promoter pre-IPO shareholders | 6 months | Regulation 17, ICDR 2018 (amended 2021) | IPO allotment date |

| Category I/II AIFs (held 6+ months before RHP filing) | Exempt | Regulation 17, ICDR 2018 (amended 2021) | N/A |

| ESOP holders (SEBI-compliant schemes) | Exempt | Regulations 17(a) and 17(b), ICDR 2018 | N/A |

| Anchor investors (50% tranche) | 30 days | Regulation 288(4), ICDR 2018 (amended 2022) | IPO allotment date |

| Anchor investors (50% tranche) | 90 days | Regulation 288(4), ICDR 2018 (amended 2022) | IPO allotment date |

Promoters

Promoter lock-in follows a two-tier structure based on post-issue paid-up capital:

Tier 1 (Minimum Promoters' Contribution):

- Shares equivalent to up to 20% of post-issue paid-up capital are locked in for 18 months from IPO allotment date

- This was reduced from 3 years by the 2021 amendment

Tier 2 (Excess Shareholding):

- All promoter shareholding exceeding the 20% threshold is locked in for 6 months from IPO allotment date

- This was reduced from 1 year by the 2021 amendment

Critical exception: According to IBA's analysis, if the majority of issue proceeds (excluding offer for sale) are used for capital expenditure—civil work, purchase of land, plant, and machinery—the original 3-year lock-in for MPC shares continues to apply.

Both lock-in periods begin from the date of allotment in the IPO, not the listing date. The 20% calculation is based on post-issue paid-up capital (total equity capital after including IPO shares), not pre-issue capital.

Non-Promoter Pre-IPO Investors

Non-promoter shareholders who held shares before the IPO—including HNIs, angels, family offices, and any individual or entity holding shares in the unlisted market—are subject to a 6-month lock-in from the IPO allotment date under Regulation 17.

Before the August 2021 amendment, this lock-in was 1 year. The reduction to 6 months applies to all non-promoter pre-IPO shareholders equally—except for the AIF/VCF/FVCI and ESOP carve-outs described below.

Exception for Regulation 6(2) companies: Per Nishith Desai Associates' analysis, companies listing under Regulation 6(2) (those without a profitable track record meeting specified criteria) face stricter rules. Shareholders holding more than 20% of pre-IPO shareholding (individually or with persons acting in concert) are subject to a 1-year lock-in from allotment date.

AIF and PE Funds

Category I and Category II AIFs, Venture Capital Funds (VCFs), and Foreign Venture Capital Investors (FVCIs) qualify for a holding-period-based exemption under Regulation 17. If these funds held shares for at least 6 months prior to the date of filing the Red Herring Prospectus (RHP), they are exempt from the standard non-promoter lock-in at listing.

For shares acquired within 6 months of RHP filing:

- Lock-in runs for 6 months from the date of purchase (not from allotment or listing)

- Reduced from 1 year to 6 months by the 2021 amendment

Category III AIFs are excluded from this exemption and remain subject to the standard 6-month non-promoter lock-in.

Worked example:

- AIF acquires shares on January 1, 2026

- Company files RHP on May 1, 2026 (4 months later)

- IPO allotment occurs on July 1, 2026

- Lock-in expires on July 1, 2026 (6 months from January 1 acquisition date)—shares are free to trade immediately at listing

If the AIF had acquired shares on October 1, 2025 (7 months before RHP filing), shares would be completely free of lock-in at listing.

The holding period of original equity shares and resultant bonus shares are aggregated for the 6-month calculation, provided the bonus issue is made from free reserves and share premium (not from revaluation reserves or unrealized profits).

ESOP Holders and Anchor Investors

ESOP Holders: Equity shares allotted to employees under an Employee Stock Option Scheme (ESOP), Employee Stock Purchase Scheme (ESPS), or Stock Appreciation Rights (SARs) scheme are exempt from the standard non-promoter lock-in under Regulations 17(a) and 17(b).

The exemption requires that the ESOP/ESPS/SARs plan be compliant with the SEBI (Share Based Employee Benefits) Regulations, 2014. The March 8, 2025 ICDR amendments expanded this exemption to include bonus shares issued against ESOP/ESPS/SARs allotments.

That said, the company or its advisors may voluntarily impose restrictions on key managerial personnel. ESOP shares held by employee stock option trusts follow the SBEB Regulations regime rather than the ICDR regime.

Anchor Investors: Per Regulation 288(4) of the SEBI ICDR Regulations (amended January 14, 2022, effective for IPOs opening on or after April 1, 2022):

- 50% of anchor investor allocation: locked for 30 days from allotment date

- 50% of anchor investor allocation: locked for 90 days from allotment date

Prior to this amendment, the entire anchor investor allocation was locked for 30 days. The split lock-in provides institutional investors with staggered liquidity while maintaining initial market stability.

How the Pre-IPO Lock-In Period Works in Practice

End-to-End Sequence

Lock-in enforcement follows a structured process:

- Pre-filing phase: Lock-in obligations are established during IPO preparation and mapped against shareholder categories

- DRHP disclosure: All lock-in details—category-wise restrictions, timeframes, exact share counts, and exemptions—are documented in the DRHP

- Final prospectus: Lock-in provisions are confirmed in the final prospectus

- Depository enforcement: NSDL/CDSL place system-level "lock-in" markers on relevant demat accounts at allotment

- Automatic release: Depositories lift the lock-in automatically on the expiry date

Shareholders cannot bypass this mechanism unilaterally. Lock-in is enforced at the depository level by NSDL and CDSL, not by brokers or the issuer company.

Depository Enforcement Mechanism

Per the NSDL Master Circular NSDL/POLICY/2026/0022 (dated February 11, 2026), lock-in of pre-issue shares is implemented in line with the Standard Operating Procedure of Depositories dated August 8, 2023. The depository system automatically blocks any sell or transfer instructions for locked shares until the expiry date.

Lock-in categories in NSDL's system cover four standard durations: 6, 12, 18, and 36 months. Release is automatic upon expiry — shareholders do not need to file separate applications or take any affirmative action.

DRHP Disclosure Requirements

Lock-in details must be disclosed in the Draft Red Herring Prospectus and final prospectus, including:

- Category-wise restrictions (promoter, non-promoter, AIF, ESOP, anchor)

- Applicable timeframes for each category

- Exact share counts subject to lock-in

- Exemptions being claimed (with supporting rationale)

According to Lexology's analysis of the November 2025 consultation paper, "enhanced disclosures are required in the DRHP and RHP regarding how pledged non-promoter shares will be treated during the lock-in period."

Incomplete disclosures or incorrect category classifications are among the most common reasons SEBI flags companies during the review process. Getting these details right before filing avoids costly delays later.

Restricted Actions During Lock-In

Once lock-in is applied, shareholders face strict operational constraints. Locked-in shares cannot be:

- Sold on the open market

- Transferred to third parties (with limited exceptions)

- Pledged as collateral (with specific exceptions below)

- Hypothecated

Pledging Exception: Under Regulation 16/21 of the ICDR Regulations, promoters may pledge locked-in shares as collateral under the following conditions:

- The pledge must be a condition of the loan sanction

- The loan must be from a scheduled commercial bank, public financial institution, or systemically important NBFC

- The loan must be for the purpose of the company's objects as stated in the offer document

- If the pledge is invoked (lender takes possession), lock-in continues to apply to the transferee; the lender cannot sell until the expiry date

2026 Pledged Shares Mechanism

SEBI's notification dated March 21, 2026 amended the ICDR Regulations to allow shares on which a standard lock-in cannot be created (because they are under pledge) to be recorded as "non-transferable" by depositories for the lock-in duration.

The operational framework was issued via SEBI Circular dated April 8, 2026, requiring issuers to:

- Incorporate suitable provisions in Articles of Association

- Issue intimations to lenders/pledgees

- Make suitable disclosures in offer documents

In practice, issuers now carry direct contractual obligations — not just depository system compliance — to enforce lock-in where pledged shares are involved. The depository marks shares as non-transferable; the issuer ensures lenders are notified and Articles of Association reflect the restriction.

Common Misconceptions and What Happens at Lock-In Expiry

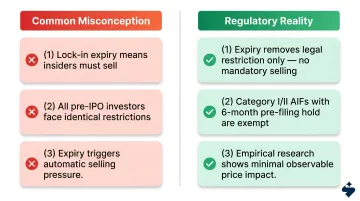

Lock-In Expiry Does Not Equal Mandatory Selling

The most common misconception is that lock-in expiry means insiders will or must sell. Lock-in expiry only removes the legal restriction—it does not trigger mandatory selling. Promoters and investors may choose to retain their shares indefinitely.

The Economic Times notes that lock-in expiry means shares "become eligible for trade" but "doesn't imply that they will necessarily be sold." Nuvama research cited in the same piece confirms that a "sizable portion" of these shares are held by promoters who may choose not to sell.

The empirical record backs this up. Research published on ResearchGate found that "the event of lock-in period expiration has not produced much impact on Indian stock market"—suggesting the fear of automatic selling pressure is largely overstated.

AIF/PE Funds Are Not Always Locked In

The 6-month pre-filing holding exemption for Category I and II AIFs is frequently misunderstood or overlooked. Many founders and advisors assume all pre-IPO investors face the same restriction—which leads to redundant lock-in provisions being included in the DRHP, adding unnecessary friction to the filing process and creating confusion among investors.

Planning for Lock-In Expiry

Both misconceptions point to the same root issue: a communication gap. The lock-in expiry window is best navigated with a clear investor communication strategy rather than reactive damage control. Companies should consider:

- Whether any block deals, secondary market transactions, or structured sell-downs are appropriate

- Coordination with their investment banker or IR team to manage market expectations

- Proactive disclosure of promoter intentions (if they plan to retain shares)

- Messaging to retail investors to prevent unwarranted volatility

S45's post-listing IR support includes preparing earnings call scripts, coordinating investor Q&A sessions, and maintaining an updated IR website—tools that can be used to address potential concerns during lock-in expiry windows. Done well, this keeps the narrative in front of retail investors before headlines do.

Frequently Asked Questions

How long is the pre-IPO lock-in period?

The duration varies by category: 18 months for promoter shares up to 20% of post-issue capital, 6 months for excess promoter shares and non-promoter pre-IPO investors, and 30–90 days (a split lock-in structure) for anchor investors. Category I and II AIFs meeting the 6-month pre-filing holding condition are exempt from post-listing lock-in.

Who is subject to the pre-IPO lock-in period under SEBI regulations?

Promoters, non-promoter pre-IPO shareholders (HNIs, angels, family offices, and unlisted market buyers), and anchor investors fall under lock-in requirements. ESOP holders with SEBI-compliant SBEB schemes are generally exempt, though companies may impose voluntary restrictions on key managerial personnel.

Does the lock-in period apply if I bought shares of a company in the unlisted market before its IPO?

Yes, unlisted market buyers classified as non-promoter pre-IPO investors are subject to a 6-month lock-in from the IPO allotment date under Regulation 17, regardless of when within the pre-IPO window the shares were purchased.

Can the lock-in period be waived or released early?

SEBI-mandated lock-in periods cannot be unilaterally waived. Limited exceptions include inter-se transfers among promoters (where lock-in passes to the transferee), death of the promoter, court orders, and NCLT-approved schemes of reconstruction. All such exemptions must be disclosed in the IPO prospectus.

What is the difference between the promoter lock-in and non-promoter lock-in period?

Promoter shares up to 20% of post-issue capital are locked in for 18 months, while excess promoter shares are locked in for 6 months. All non-promoter pre-IPO investor shares (excluding exempt AIFs and ESOP holders) are locked in for 6 months—both periods commencing from the IPO allotment date.

Can locked-in shares be pledged as collateral?

Promoters may pledge locked-in shares to scheduled commercial banks, public financial institutions, or systemically important NBFCs for loans tied to the company's stated objects, per Regulation 16/21. If the pledge is invoked, the lock-in transfers to the lender — who cannot sell until expiry. SEBI's March 2026 amendment added a "non-transferable" depository marking mechanism to enforce this during lock-in.