Most founders and CFOs understand that an IPO raises capital. Far fewer can explain which specific line items change, which stay untouched, and why. That gap creates real problems: miscalculated post-IPO ratios, investor messaging that doesn't hold up under scrutiny, and capital deployment plans that conflict with what the DRHP actually committed.

This article walks through the mechanics precisely—covering every balance sheet account an IPO touches, the critical difference between fresh issues and OFS, and how the use of proceeds reshapes financial statements over the months that follow.

Key Takeaways

- An IPO increases cash (assets) and equity simultaneously — Share Capital rises by the face value of new shares, Securities Premium Reserve by the premium collected

- IPO issuance costs are charged against Securities Premium Reserve under Companies Act 2013, not the P&L. Net worth rises by gross proceeds minus issue expenses

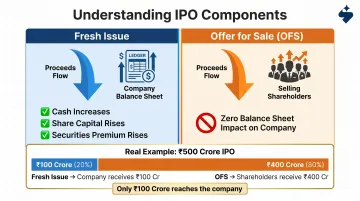

- Only a fresh issue puts money on the company's balance sheet; an OFS sends proceeds directly to selling shareholders, leaving the company's financials unchanged

- Post-IPO deployment of proceeds across capex, working capital, and debt repayment drives secondary balance sheet shifts over 12–24 months

What an IPO Actually Does to a Balance Sheet

A balance sheet is a snapshot of what a company owns (assets), owes (liabilities), and what belongs to shareholders (equity). An IPO is fundamentally a capital-raising event that alters at least two of these three pillars at once.

Not every IPO affects the balance sheet in the same way. Four variables determine both the magnitude and nature of the change:

- Issue type — a fresh issue brings in new capital; an OFS routes proceeds to selling shareholders, not the company

- Pricing — the offer price above par creates the share premium, which flows into reserves

- Use of proceeds — debt repayment, capex, and working capital each affect the balance sheet differently

- Pre-existing capital structure — existing debt, retained earnings, and equity base all shape how the change reads on paper

The assumption that "going public automatically strengthens the balance sheet" is only sometimes correct, and even then, only partially.

For Indian companies, the Companies Act 2013 governs how IPO proceeds and issuance costs are classified in financial statements. SEBI's ICDR Regulations also require specific disclosure of issue structure and objects. Relying solely on US GAAP or IFRS analogies will produce incorrect accounting treatment.

How an IPO Changes the Balance Sheet, Line by Line

An IPO doesn't rewrite every line of the balance sheet. It targets specific accounts in a predictable, mechanical sequence that follows the accounting entries made at allotment.

Assets: The Cash Impact

The most immediate change is in cash and cash equivalents. The company's bank account receives net IPO proceeds—gross subscription money minus underwriting fees, registrar charges, legal costs, SEBI filing fees, and marketing expenses. This inflow is recorded as an increase in current assets on day one.

If the offer document earmarks proceeds for capital expenditure, long-term assets (property, plant, and equipment or intangibles) will increase as funds are deployed. That happens after the IPO closes, not at listing. The day-one balance sheet shows only cash.

Equity: The Two-Part Entry

The equity section changes in two places simultaneously:

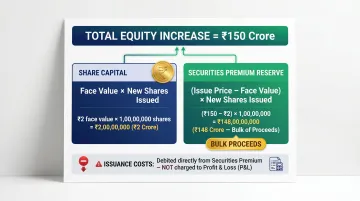

- Share Capital increases by face value × number of new shares issued. If 1 crore new shares are issued at ₹2 face value, Share Capital rises by ₹2 crore

- Securities Premium Reserve increases by the excess of issue price over face value × new shares—this is where the bulk of IPO proceeds sits

How issuance costs are treated is where most founders get it wrong.

Under Section 52(2)(c) of the Companies Act 2013, IPO issuance costs—underwriting commissions, legal fees, SEBI filing fees, printing, marketing—are debited against the Securities Premium Reserve, not charged to the profit and loss account. They reduce the premium reserve, not reported profits. Under Ind AS 32, directly attributable, incremental equity transaction costs are similarly deducted from equity rather than expensed.

Get this wrong and your IPO-year PAT looks artificially depressed—a red flag for analysts reviewing the first post-listing earnings.

Beyond issuance costs, pre-IPO convertible instruments—CCPS, convertible notes, or SAFEs from venture rounds—typically convert to ordinary equity at or before listing. This eliminates a hybrid liability and further boosts the equity section, while removing associated interest or dividend obligations.

Liabilities: What Disappears

While equity expands, the liability side often shrinks. The IPO itself doesn't create new liabilities. If the offer document commits fresh issue proceeds to repaying term loans or working capital borrowings, those debt line items retire at or shortly after listing—improving the debt-to-equity ratio and reducing finance costs on the income statement going forward.

Fresh Issue vs. Offer for Sale: The Distinction That Changes Everything

Fresh Issue vs. Offer for Sale: What Each Component Does to the Balance Sheet

Every Indian IPO can contain one or both components:

| Component | Who Receives Proceeds | Balance Sheet Impact |

|---|---|---|

| Fresh Issue | The company | Cash increases; Share Capital and Securities Premium rise |

| Offer for Sale (OFS) | Selling shareholders | Zero impact on company's balance sheet |

In an OFS, no new shares are created, no cash enters the company, and no accounting entries are made in the company's books. The register of shareholders changes—not the financial statements. A company that runs a pure OFS IPO will show the exact same balance sheet the day after listing as the day before.

The LIC IPO is the most visible example of this. LIC's issue was structured as an OFS of approximately 22.13 crore shares, with proceeds flowing to the Government of India as selling shareholder—not to LIC's balance sheet.

Always check the "Objects of the Issue" section in the prospectus to find the fresh issue size. That figure (minus issuance costs) is what actually strengthens the company's financial position. A large OFS component with a small fresh issue means limited incremental capital reaches the company itself.

A concrete example: a ₹500 crore IPO with ₹100 crore fresh issue and ₹400 crore OFS delivers only ₹100 crore (minus costs) to the company's cash account. Not ₹500 crore. Modelling post-IPO ratios without accounting for that split produces materially wrong outputs.

How the Use of Proceeds Reshapes the Balance Sheet Over Time

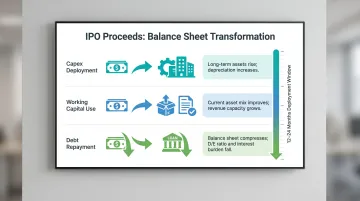

The "Objects of the Issue" disclosed in the DRHP and final prospectus commit the company to specific uses of IPO funds. Each category produces a predictable second-order balance sheet shift as funds deploy over the 12–24 months following listing.

The three most common transformation patterns:

- Capex deployment — Cash converts into fixed assets, increasing long-term assets. Depreciation charges on the income statement rise as assets are capitalised and placed in service

- Working capital use — Cash converts into receivables, inventory, or operating capacity. Current asset composition improves, supporting higher revenue capacity

- Debt repayment — Cash and long-term borrowings both decrease simultaneously. The balance sheet compresses, but solvency ratios improve and interest burden on the income statement reduces

None of these deployment paths are discretionary once they appear in the prospectus. LODR Regulation 32 mandates quarterly Statements of Deviation/Variation until proceeds are fully deployed, filed with exchanges and tabled to the Audit Committee. Any deviation from the stated objects requires shareholder approval and regulatory disclosure.

SEBI's adjudication order in the Taksheel Solutions case imposed monetary penalties for diversion and misuse of IPO proceeds, confirming that the Objects of the Issue are binding commitments. CFOs building post-IPO deployment plans should treat the prospectus as the governing document — revisions require formal disclosure, not internal reallocation.

Post-IPO Balance Sheet: What Changes on an Ongoing Basis

After listing, the balance sheet becomes a public document scrutinised every quarter. Under LODR Regulation 33, companies must file quarterly standalone results within 45 days of quarter-end, board-approved and accompanied by auditor or limited review reports. SEBI's T+3 listing timeline (mandatory from December 2023) compresses the operational window around issue close further.

Two ongoing equity movements founders often underestimate:

- ESOPs dilute equity over time: Under Ind AS 102, share-based compensation expense hits the P&L each quarter over the vesting period, with Share Capital and Securities Premium credited on exercise — a steady equity expansion that analysts track closely

- Price-to-book divergence becomes a live benchmark: The gap between market cap and book value (net worth) is not a balance sheet item, but it shapes investor confidence and the P/B ratio the market assigns from day one

Both issues are easier to manage before the DRHP is filed than after. S45's IPO Readiness service includes ESOP dilution modelling and cap table cleanup — the AI Risk Radar flags mismatches between ESOP grants and cap table entries before filing, preventing the disclosure inconsistencies that SEBI observations routinely surface.

Conclusion

The balance sheet impact of an IPO is precise and mechanical. Fresh issue proceeds increase cash and equity in equal measure. Issuance costs reduce the Securities Premium Reserve, not profits. OFS does not touch the company's balance sheet at all. And subsequent use of proceeds reshapes the asset and liability mix over months, according to the objects committed in the offer document.

Understanding this sequence allows founders and CFOs to model post-IPO ratios accurately, communicate with investors with clarity, and deploy capital in line with regulatory commitments.

That sequence only holds if the balance sheet is clean, properly structured, and audit-ready before the DRHP is filed. S45's IPO Readiness Scan — a 30-minute AI-powered assessment — surfaces the issues that create problems later:

- Undisclosed contingent liabilities

- Tax disputes with material financial impact

- ESOP dilution not reflected in the cap table

- Inconsistent revenue recognition

- Unexplained working capital movements

These are caught 12–18 months before filing, not during SEBI review when remediation options are far more limited.

Frequently Asked Questions

How does an IPO affect a company's balance sheet?

An IPO increases cash (assets) and equity simultaneously. Share Capital rises by the face value of new shares issued, Securities Premium Reserve rises by the premium collected, and IPO issuance costs are charged against that reserve—not the P&L. The net result is a stronger equity base with no new debt created.

What happens after a company files for an IPO?

After filing the DRHP, the company undergoes SEBI review, opens the IPO for public subscription, completes allotment, and lists on the exchange. From listing onward, quarterly financial disclosures become mandatory: balance sheet management becomes a permanent, public exercise under LODR.

What happens to existing shareholders' shares when a company goes public?

Existing shares are not cancelled. Fresh issue shares expand the total share count, so each existing shareholder's ownership percentage decreases proportionally. If the IPO prices at a premium to the pre-IPO valuation, per-share value may still rise even as that percentage falls.

Does an Offer for Sale (OFS) affect the company's balance sheet?

No. An OFS has zero impact on the company's balance sheet. No new shares are created, no cash enters the company, and no accounting entries are made in the company's books. Proceeds flow directly to the selling shareholders.

How are IPO expenses treated on the balance sheet?

Under Companies Act 2013 Section 52(2)(c) and Ind AS 32, IPO issuance costs (underwriting fees, legal, SEBI filing fees, marketing) are charged against the Securities Premium Reserve. They reduce equity slightly but do not affect reported profits or retained earnings.

What happens to a company's debt after an IPO?

If the prospectus earmarks fresh issue proceeds for debt repayment, outstanding borrowings decrease post-listing, improving the debt-to-equity ratio and reducing interest costs. If debt repayment isn't included in the Objects of the Issue (the stated use-of-proceeds section), existing liabilities remain unchanged and the IPO adds equity without retiring any debt.