That's the mistake.

Investment banking fees, known as BRLM (Book Running Lead Manager) fees, can catch founders off guard — not because they're hidden, but because most founders only track that one number. The BRLM fee is often less than half the total cost of going public. Budget only for it, and you'll hit a shortfall at the worst possible moment.

This guide breaks down exactly what investment bankers charge for IPOs in India, what those fees cover, what else adds to the bill, and how to build an accurate budget before you sign a mandate.

Key Takeaways

- BRLM fees in India range from 1% to 7%+ of issue size — SME issues sit at the higher end, Main Board at the lower

- SME IPOs carry higher fee percentages than Main Board deals; execution work doesn't shrink proportionally when issue size drops

- The BRLM fee typically represents ~50% of total issue expenses — legal, registrar, SEBI, advertising, and broker costs add the rest

- Fees compress at scale but absolute payouts remain large; Hyundai India's 10 bankers shared ~₹330 crore

- Total issue costs routinely run 5–10% of issue size for SME IPOs — founders who map this before mandate selection avoid expensive surprises

How Much Do Investment Bankers Charge for an IPO in India?

There is no fixed, regulated rate. SEBI does not prescribe what a BRLM may charge — fees are commercially negotiated between the issuer and the merchant banker(s), then disclosed in full in the DRHP and RHP under Schedule VI of SEBI's ICDR Regulations. This transparency mechanism is available to any founder: pull the offer documents from recent comparable deals on SEBI's EDGAR portal and you'll see exactly what peer companies paid.

That openness has a practical implication: founders who skip this homework often either overpay or underestimate what they need to budget.

SME IPOs (Issue Size ₹10 Cr – ₹200 Cr)

Key fee benchmarks for SME issues:

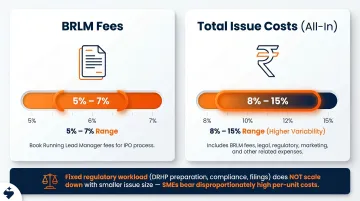

- BRLM fees: 5% to 7% of issue size (typical range)

- Total issue costs (all-in, including legal, registrar, advertising): 8% to 15%

- Average fee trend: peaked at 5.5% in FY22 for sub-₹250 crore issues; moderated to 3.93% in FY24 for sub-₹500 crore issues, per Economic Times analysis of DRHP disclosures

Why so high as a percentage? The absolute work of an IPO — DRHP drafting, due diligence, SEBI filings, roadshows — doesn't scale down proportionally with issue size. A ₹50 crore SME IPO requires essentially the same regulatory effort as a ₹300 crore deal. The fixed-cost burden falls harder on smaller issuers.

Mid-Size Main Board IPOs (₹200 Cr – ₹1,000 Cr)

This tier has seen the steepest fee inflation in recent years. According to Economic Times, BRLM fees for ₹500–1,000 crore issues nearly doubled from 1.6% in FY20 to 3.1% in FY24 as demand for quality banker capacity surged.

SEBI mandates a minimum of 2 BRLMs for issues in the ₹500–1,000 crore range and 3 BRLMs for ₹1,000–2,500 crore deals. Total fees are split across the syndicate, but the issuer's total payout doesn't fall proportionally just because more bankers are involved.

Large/Mega Main Board IPOs (₹1,000 Cr+)

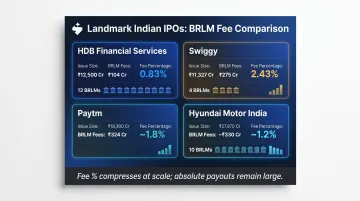

At scale, fee percentages compress — but absolute amounts are significant:

| IPO | Issue Size (₹ Cr) | BRLM Fees (₹ Cr) | Fee % | BRLMs |

|---|---|---|---|---|

| HDB Financial Services | 12,500 | 104 | 0.83% | 12 |

| Swiggy | 11,327 | 275 | 2.43% | 4 |

| Paytm | 18,300 | 324 | ~1.8% | Multiple |

| Hyundai Motor India | 27,870 | ~330 | ~1.2% | 10 |

Leela Hotels (Schloss Bangalore), with an ~₹5,000 crore filing and 11 appointed BRLMs, illustrates how even luxury or niche issuers at this scale attract large syndicates. Syndicate size, however, is only one variable. Sector also moves the number: new-age tech companies consistently pay above-average fees. Swiggy's 2.43% is roughly double what a comparably sized traditional issuer would pay — the premium reflects higher investor education effort and roadshow intensity for loss-making businesses.

What the Investment Banking Fee Actually Covers

The BRLM fee is not payment for a document. It is a success-linked fee paid upon listing — one that compensates for the full span of work from first engagement through listing day, including post-listing IR where the engagement letter specifies it.

What the Fee Compensates For

- **IPO readiness and eligibility assessment** — identifying gaps before filing, not after SEBI raises observations

- DRHP drafting and due diligence coordination — coordinating auditors, legal counsel, secretarial teams, and internal finance

- SEBI filing and observations management — responding to SEBI queries, managing the back-and-forth through the observation letter stage

- Roadshow preparation and investor outreach — developing the equity story, preparing management presentations, identifying the right investor cohorts

- Bookbuilding and demand management — running the price discovery process, managing subscription across QIB, NII, and retail categories

- Listing day coordination and stabilisation — managing anchor allocation, grey market signals, and post-listing stability for issues where a stabilising agent is appointed

Retainer vs. Success Fee

Most engagements involve two fee components:

- Engagement/retainer fee — paid at or shortly after mandate signing; covers early readiness work, DRHP drafting, and regulatory preparation

- Success fee — paid upon successful listing; the larger component, calculated as a percentage of total issue proceeds

The retainer is typically credited against or offset from the final success fee. S45 structures this differently from legacy banks. Its 0% upfront fee model means founders are not charged large front-loaded retainers before meaningful work begins. All fees are milestone-linked and fully documented in the engagement letter before mandate signing.

How Fees Split in Multi-BRLM Deals

In large Main Board IPOs with multiple BRLMs, the total fee pool is negotiated at the deal level, then divided among lead managers based on role (BRLM vs. Co-BRLM) and contribution. Appointing more BRLMs does not reduce the issuer's total cost proportionally. It redistributes the same pool across more parties, with added coordination overhead layered on top.

SEBI's ICDR Regulations mandate full disclosure of all fee arrangements — including retainer amounts, success fee percentages, and any differential splits among BRLMs — in the DRHP filed with the regulator.