Introduction

Applying as an HNI in an SME IPO is not the same as placing a large retail bid — and many investors find this out after submitting incorrect applications or receiving far less allotment than expected.

The mechanics are distinct from mainboard participation. In SME IPOs on BSE SME and NSE Emerge:

- NII classification is lot-based, not value-based — three lots qualifies you regardless of whether the rupee total crosses ₹2 lakh

- Allotment is proportionate, not lottery-based

- Bidding at cut-off price is not permitted

- Post-listing liquidity is thinner than anything you'll encounter on the mainboard

This guide covers the full picture: SEBI's quota structure, how to apply correctly, what actually drives allotment outcomes, and the risks that commonly catch HNI investors off-guard. Whether you're an individual investor, NRI, HUF, or corporate entity, this guide will help you avoid the most common application errors and size positions more realistically.

Key Takeaways

- HNIs in SME IPOs apply under the NII category — the threshold is 3+ lots, not the ₹2 lakh value threshold used in mainboard IPOs

- The NII quota is split into sNII (3 lots to ₹10L) and bNII (above ₹10L), each with ring-fenced allocations and proportionate allotment

- Explicit price within the band is mandatory — HNIs cannot bid at cut-off price

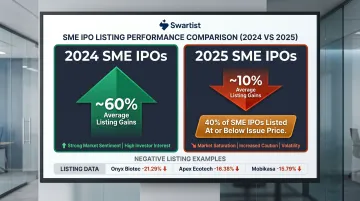

- Average SME IPO listing gains dropped from ~60% in 2024 to ~10% in 2025

- ~40% of early 2025 SME IPOs listed below issue price

- Post-listing liquidity is the most underestimated risk — mandatory market-making provides a floor, not depth

What Is HNI Investment in SME IPOs and Why It Matters

In SME IPOs, the Non-Institutional Investor (NII) category — commonly called the HNI category — applies to any applicant who bids for 3 or more lots, regardless of total rupee value. Understanding this distinction shapes every downstream decision: which category to select, how allotment works, and what risks come with larger applications.

The Lot-Based NII Threshold

In mainboard IPOs, the NII category applies when your application exceeds ₹2 lakh in total value. SME IPOs work differently. Under SEBI ICDR Regulation 253, Chapter IX, any application covering 3 or more lots in an SME IPO automatically classifies you as a Non-Institutional Investor — regardless of the rupee amount.

Since SME IPO lot sizes are typically structured around ₹1 lakh per lot, the NII threshold usually sits around ₹3 lakh or higher per issue. The defining criterion is lot count, not rupee value. Selecting the wrong investor category during application results in rejection.

Why HNIs Find SME IPOs Attractive

Several structural features draw HNI capital toward SME issues:

- Proportionate allotment rather than retail's lottery system — larger bids get larger allotments

- Lower institutional competition pre-listing compared to mainboard issues with heavy QIB participation

- Smaller issue sizes that can respond more sharply to demand

- Potential for meaningful listing gains — HOAC Foods India, for example, listed at ₹144 against an issue price of ₹48 in May 2024, a 200% listing gain

Smaller free floats, however, mean thinner secondary market depth, and exit constraints post-listing are a genuine operational risk worth pricing in before you apply.

Who Qualifies as NII in an SME IPO

HNI status in SME IPOs is determined by application size, not wealth level. The following investor types qualify for the NII category, provided they apply for 3+ lots:

| Investor Type | Account Requirement |

|---|---|

| Resident Indian Individuals | Demat + ASBA-enabled bank account |

| Non-Resident Indians (NRIs) | NRE/NRO account under FEMA |

| Hindu Undivided Families (HUFs) | Applied in name of the Karta |

| Companies / Corporate Bodies | Standard KYC compliance |

| Trusts and LLPs | Per trust deed / constitutive document |

NII investors do not require SEBI registration, unlike QIBs.

SEBI Rules and Quota Structure for HNIs in SME IPOs

Allocation Percentages Under Regulation 253

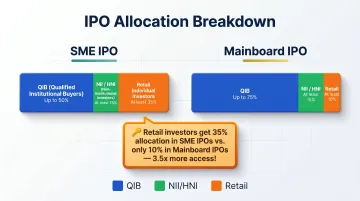

SME IPOs follow a different allocation split from mainboard book-built issues:

| Category | SME IPO | Mainboard IPO |

|---|---|---|

| QIB | Up to 50% | Up to 75% |

| NII/HNI | At least 15% | At least 15% |

| Retail / Individual | At least 35% | At least 10% |

The retail allocation in SME IPOs is considerably larger than mainboard — 35% versus 10% — reflecting the SME platform's orientation toward non-institutional participation. The NII share holds at 15% in both venues, but the competitive dynamic is different: lower QIB interest in SME issues means the NII pool is contested by a narrower, more concentrated set of applicants. That dynamic shapes how the sub-category split below plays out in practice.

The sNII and bNII Split

Effective July 1, 2025 (per SEBI amendments dated March 3, 2025), the NII category is divided into two ring-fenced sub-buckets:

- sNII (Small NII): Applications from 3 lots up to ₹10 lakh → receives 1/3 of the total NII portion

- bNII (Big NII): Applications above ₹10 lakh → receives 2/3 of the total NII portion

The ring-fencing is critical: oversubscription in bNII cannot cannibalise the sNII quota, and vice versa. The reform targets a specific behaviour: HNIs borrowing ₹5–10 crore to inflate their bid size, collecting allotment, and returning the funds post-subscription — driving headline NII multiples that had no connection to actual buying conviction.

How Proportionate Allotment Actually Works

When either NII sub-category is oversubscribed, allotment follows a two-step process:

- Lottery for minimum lot — a draw allocates the minimum bid lot to eligible applicants within that sub-category

- Proportionate distribution — remaining shares are distributed proportionate to bid size

This means bidding the maximum amount no longer guarantees a proportionally larger allotment. If the bNII sub-category is 100x oversubscribed, an applicant for 100 lots can expect to receive roughly 1 lot — and the lottery in step one determines whether they receive even that.

The No Cut-Off Price Rule

Unlike retail investors, HNIs must bid at an **explicit price within the declared price band**. Cut-off price is not an option. Bids placed below the final discovered issue price are ineligible for allotment.

Pricing judgement is a required input. HNIs who default to the upper end of the price band without considering valuation are taking an active position — whether they intend to or not.

Mandatory Market-Making Post-Listing

SEBI requires every SME issuer to maintain market-making for a minimum of 3 years post-listing, with:

- Two-way quotes for at least 75% of daily trading time

- Minimum quote depth of ₹1,00,000

No equivalent obligation applies to mainboard stocks. This provides a structural liquidity backstop — but the depth is limited. Market makers must post two-way quotes, but there is no obligation to absorb large sell orders at favourable prices. For HNIs planning to exit a meaningful position, that distinction matters.

How to Apply as an HNI in an SME IPO

Prerequisites Before You Bid

- Active Demat account with valid DP ID and Client ID

- ASBA-enabled bank account linked to the same PAN

- Completed KYC with the broker or bank

- Correct category selected: NII/HNI (not retail)

- One PAN, one application — duplicate submissions result in all applications being rejected

Step 1: Assess the Offering

Before bidding, review:

- DRHP/RHP for business fundamentals, promoter background, financials, and use of proceeds

- Price band, minimum lot size, and issue dates

- Real-time NII subscription data (sNII vs bNII split) during the bidding window

- Grey market premium (GMP) as a sentiment indicator — cross-check it against fundamentals before making a decision, not as a standalone signal

Step 2: Place the Bid

- Enter an explicit price within the price band (cut-off not available)

- Select minimum 3 lots for NII classification

- Confirm total application value and authorise the ASBA block

- Verify the NII/HNI category is selected, not retail

UPI is available for bids up to ₹5 lakh (per SEBI Circular SEBI/HO/CFD/DIL2/CIR/P/2022/45). For HNI applications above ₹5 lakh, ASBA through a bank account is mandatory. Under ASBA, the bid amount is blocked but not debited unless shares are allotted.

Step 3: Understand Modification Rules

NII investors cannot withdraw bids or revise them downward once submitted — unlike retail investors. You may only revise upward during the open bidding window. Once the issue closes, the application is locked. Size your bid accordingly before you submit.

Step 4: Track Allotment and Plan Your Exit

After the issue closes, check allotment status via the registrar portal or stock exchange website. Unallotted funds are automatically unblocked from ASBA.

Before shares are credited to your Demat account, have a clear exit plan — whether targeting listing-day liquidity or holding for fundamental growth. The post-listing window is not the time to make that call for the first time.

Key Factors That Affect HNI Outcomes in SME IPOs

NII Subscription Rate During the Bidding Window

The live sNII and bNII subscription multiples, visible during the bidding window, are the most direct signal of expected allotment ratio. The HOAC Foods India IPO illustrates the dilemma clearly: NII subscription reached 1,432.65x, and while the stock listed at 200% above issue price, an investor applying ₹10 lakh in the NII category would have received allotment worth approximately ₹7. The headline return was extraordinary; the actual capital deployed was negligible.

According to Moneycontrol's SME IPO coverage, 61 SME IPOs in 2025 were subscribed between 100x and 1,000x — underscoring how common extreme oversubscription has become.

IPO Pricing and Investment Banker Quality

The issue price relative to the company's actual earnings profile and peer valuations is a factor HNIs must evaluate independently. Aggressively priced SME IPOs carry higher post-listing downside risk, particularly in weaker market conditions.

Investment banks that apply disciplined pricing and structured demand mapping produce more consistent outcomes across subscription and listing metrics. Look for bankers who conduct pre-IPO investor soundings and sector comparable analysis rather than setting a price band based on promoter preference alone. Track records across prior mandates — subscription averages, listing pops, capital raised — are a reasonable proxy for execution quality.

Post-Listing Liquidity and Exit Constraints

SME-listed stocks have structurally smaller free floats than mainboard issues. Post-issue capital is capped at ₹25 crore for SME platforms, which directly constrains secondary market depth. HNI investors holding multiple large lots may find it difficult to exit at desired prices in the weeks following listing. When multiple allottees attempt to sell simultaneously, thin order books absorb the pressure quickly.

One practical rule: limit single SME IPO exposure to a defined percentage of your portfolio. Exit may take days, not minutes — size positions accordingly.

Grey Market Premium as a Forward Indicator

GMP is an unofficial, unregulated signal of expected listing performance. SEBI's August 2024 advisory on the SME segment cautions against relying on informal market signals, noting that artificial demand creation and promoter-driven optimism are documented risks in this space.

Use GMP as one signal among several. A more complete picture combines:

- NII subscription multiples — sNII and bNII live figures during the bidding window

- DRHP fundamentals — revenue quality, promoter background, use of proceeds

- Promoter track record — prior business history and any related-party disclosures

- Peer valuation benchmarks — issue price relative to listed comparables in the same sector

Never treat GMP as a primary decision trigger.

Common Misconceptions and Risks HNIs Should Know

Misconception 1: Proportionate Allotment Means You Receive Most of What You Applied For

Proportionate allotment simply means your share of the available pool reflects your bid size relative to total demand. In a 50x oversubscribed bNII sub-category, you receive roughly 2% of the quantity applied. Applying the maximum amount gives you a proportionally larger slice, but when oversubscription is extreme, even the largest bids receive negligible allotment.

Misconception 2: SME IPO HNI Rules Mirror Mainboard Rules

They don't. Key differences:

| Rule | Mainboard | SME IPO |

|---|---|---|

| NII classification threshold | Above ₹2 lakh (value-based) | 3+ lots (lot-based) |

| Allotment method | Proportionate | Two-step (lottery + proportionate) |

| Exchange platform | NSE / BSE | NSE Emerge / BSE SME |

| Market-making obligation | None | Mandatory 3 years |

| Disclosure intervals | Quarterly | Half-yearly (SME companies) |

Conflating the two causes category misclassification, outright application rejection, and a false read on post-listing liquidity depth.

Risk: Treating Listing Gains as a Predictable Outcome

Chittorgarh.com's 2025 SME IPO performance tracker shows 40% of SME IPOs in early 2025 listed at or below issue price, including Onyx Biotec (-21.29%), Apex Ecotech (-16.38%), and Mobikasa (-15.79%). Average listing gains collapsed from ~60% in 2024 to ~10% in 2025.

What this means in practice:

- Past subscription multiples do not predict listing performance — high demand and negative listing gains coexisted in 2025

- GMP is a sentiment signal, not a valuation tool; it shifts in the week before listing

- Fundamental filters — business quality, promoter track record, pricing relative to peers — are non-negotiable screening steps, not optional checks

Frequently Asked Questions

How do I apply as a non-institutional investor in an IPO?

Apply via an ASBA-enabled bank account or authorised broker platform, select the NII/HNI category, and specify an exact price within the price band. For mainboard IPOs, the NII threshold is applications above ₹2 lakh; for SME IPOs, it's 3 or more lots. One PAN per application — duplicates are automatically rejected.

What are the HNI rules for SME IPOs?

Any application covering 3 or more lots in an SME IPO is treated as NII/HNI. The NII quota is split into sNII (3 lots to ₹10 lakh) and bNII (above ₹10 lakh), with ring-fenced allocations for each. Allotment follows a two-step process — lottery for the minimum lot, then proportionate — and HNIs cannot bid at cut-off price.

Is it better to apply as an HNI in an IPO?

HNI status offers a dedicated quota and proportionate allotment rather than lottery. The trade-off: you need more capital, cannot use cut-off price, and your allotment shrinks proportionately with oversubscription. As a rough benchmark, NII oversubscription below 30x typically leaves room for meaningful proportionate allocation.

Who are non-institutional buyers in an IPO?

Non-institutional investors are individuals, NRIs, HUFs, corporates, and trusts who apply above the retail threshold — more than ₹2 lakh in mainboard IPOs, or 3+ lots in SME IPOs. They sit between retail investors and qualified institutional buyers (QIBs) in the investor category hierarchy.

Can HNI investors sell SME IPO shares on listing day?

Yes — there is no mandatory lock-in for NII/HNI investors post-allotment. However, thin trading volumes on BSE SME and NSE Emerge can make large sell orders difficult to execute at desired prices, especially in the first few trading sessions.

What is the minimum application amount for HNI in an SME IPO?

The threshold is lot-based: any application covering 3 or more lots qualifies as NII/HNI. The actual rupee value depends on the specific IPO's lot size and issue price, which varies across issues.