For founders, promoters, and CFOs who have filed — or are preparing to file — that knowledge gap is expensive. The post-filing stage is where timelines slip, observations pile up, and companies that thought they were six weeks from listing find themselves six months out.

This article maps the exact regulatory stages SEBI moves through after your DRHP is submitted, the defined deadlines at each checkpoint, and the factors that determine whether your process takes 3 months or stretches to 12.

Key Takeaways

- Five stages follow DRHP filing: public comment period → exchange in-principle approval → SEBI Observation Letter → RHP with RoC → subscription, allotment, and listing

- SEBI issues its Observation Letter within 30 days of receiving satisfactory clarifications — not 30 days from your filing date

- The Observation Letter is valid for 12 months; if it lapses, you refile from scratch

- From IPO closure, shares must list within 3 working days (T+3), mandatory since December 2023

- Companies with clean financials and no SEBI queries typically list within 3–6 months; heavy query loads can stretch the process to the full 12-month validity window

What Happens After You File the DRHP With SEBI?

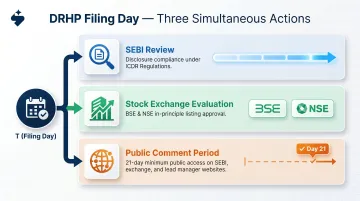

Filing the DRHP doesn't hand control to SEBI — it triggers three parallel processes simultaneously.

Three things happen on filing day (T):

- SEBI begins its review of the draft document for disclosure compliance under the ICDR Regulations

- Stock exchanges (BSE and NSE) evaluate in-principle listing eligibility — their approval formally starts SEBI's observation clock

- The DRHP goes public on SEBI's website, the stock exchanges' websites, and the lead manager's website for a minimum 21-day public comment period per Regulation 25(4) of the SEBI ICDR Regulations 2018

DRHP vs. RHP — The Critical Distinction

The DRHP is a draft. It doesn't carry a price band or final issue size. The Red Herring Prospectus (RHP) is the document you file with the Registrar of Companies (RoC) after incorporating SEBI's observations. The price band is disclosed at least 2 working days before the issue opens.

Pre-Issue Publicity During the Review Period

While SEBI reviews your filing, marketing is permitted — but with strict guardrails under Regulation 42 and Schedule IX of the SEBI ICDR Regulations. Permitted materials must meet all of the following conditions:

- Factual only, consistent with the company's past communications

- No financial projections or forward-looking statements

- No issue-specific claims, performance guarantees, or return promises

Most companies use this window to sharpen their investor narrative and prepare roadshow materials — not to solicit investors directly.

The SEBI IPO Timeline: Stage-by-Stage Breakdown

The clock starts at T (DRHP filing date). Each subsequent stage has defined regulatory deadlines — but actual elapsed time depends heavily on filing quality and response speed.

Stage 1: Public Comment Period and Stock Exchange Review (T to T+21 and beyond)

From filing day, the DRHP must remain open for public comment for a minimum of 21 days. Simultaneously, BSE and NSE review the filing and work toward granting in-principle listing approval.

That exchange approval is what formally starts SEBI's 30-day observation clock — not the date of filing.

The March 2025 SEBI ICDR Amendment extended the mandatory 21-day public comment period to SME IPOs, which previously weren't uniformly required to observe this window.

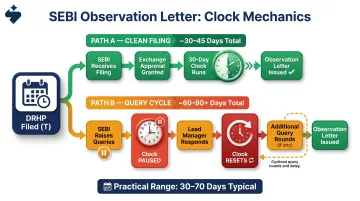

Stage 2: SEBI Issues Its Observation Letter (30 days from satisfactory clarifications)

The SEBI Observation Letter confirms that SEBI has reviewed the DRHP and is satisfied with the disclosures. It covers disclosure compliance only — not an endorsement of your valuation or business model.

The 30-day clock runs from whichever is later:

- Date SEBI receives the DRHP, or

- Date SEBI receives satisfactory clarifications from the lead manager

If SEBI raises queries and the lead manager takes two weeks to respond, those two weeks don't count. The clock resets. SEBI's own consultation paper acknowledges that the practical window from DRHP filing to Observation Letter receipt runs 30 to 70 days — sometimes longer in complex cases.

Stage 3: Incorporating SEBI's Observations and Filing the Updated DRHP

After the Observation Letter, the company and its lead managers must incorporate SEBI's observations into an updated DRHP (UDRHP), which must be uploaded publicly. How long this takes is largely within the company's control — SEBI's query response time aside.

Companies with clean, well-structured filings — where every disclosure is linked to a source and the data room is organised — can move through this stage in days. Companies cycling through multiple query rounds can spend weeks or months here.

S45's SEBI Query Board is built for this stage: observations are tracked with assigned owners, due dates, and evidence-linked closure documentation — CFO ownership for financial queries, legal counsel for governance, the lead banker for business-related matters. Once all observations are closed, the process moves to prospectus filing.

Stage 4: Filing the RHP With the RoC and Setting the Price Band

Once observations are incorporated, the RHP (including the price band) is filed with SEBI and then the RoC. Key timing requirements:

- Price band must be announced at least 2 working days before the issue opens (Regulation 29(4))

- A combined pre-issue advertisement announcing both the price band and IPO opening date is required under the 2025 SEBI ICDR Amendments

- Under Section 26(8) of the Companies Act, 2013, the prospectus must be issued within 90 days of delivery to the RoC — after that, it lapses and must be refiled

Stage 5: Subscription Window, Allotment, and Listing (T+3 from IPO closure)

The IPO subscription window runs a minimum of 3 working days and a maximum of 10 working days under Regulation 46(1) of the SEBI ICDR Regulations. Standard market practice is 3 working days.

After the window closes:

- Basis of allotment is finalized

- Shares are credited to successful applicants' demat accounts

- Refunds are processed for unsuccessful applicants

- Listing must happen within 3 working days from IPO closure

SEBI Circular SEBI/HO/CFD/TPD1/CIR/P/2023/140 reduced the listing timeline from T+6 to T+3, mandatory from December 1, 2023.

Key Factors That Affect the SEBI Review Timeline

Disclosure Quality — The Biggest Variable

The single most reliable predictor of timeline speed is whether the DRHP is complete and consistent on the first submission. SEBI's observation volume increases sharply when:

- Financial statements have inconsistencies between quarterly results and audited figures

- Revenue recognition practices don't align with Ind-AS

- Related-party transactions are vague or incompletely disclosed

- KPI justifications lack audit support

- Revenue jumps close to filing are unexplained

Companies with restatements or inadequately disclosed pending litigations face the most extended Q&A cycles.

Business Model Complexity and Sector Scrutiny

Companies in regulated sectors — NBFCs, insurance, fintech — or those with complex group structures and high valuation-to-revenue multiples typically draw more scrutiny. Additional regulatory clearances from bodies like RBI or IRDAI can extend the practical timeline to 70+ days from DRHP filing to Observation Letter, as SEBI's own consultation paper acknowledges.

Lead Manager Quality

The lead manager (BRLM) is your primary interface with SEBI. Their preparation quality and response speed directly determine whether the 30-day clock runs straight through or resets repeatedly. A well-coordinated team compresses the observation cycle. A fragmented email-based process extends it.

What separates a tight execution from a drawn-out one:

- Legal counsel, auditors, registrar, and banker working from a shared, versioned data room

- Clear ownership of each SEBI query with defined response timelines

- No version-control gaps between the DRHP draft and supporting evidence

Main Board vs. SME Exchange

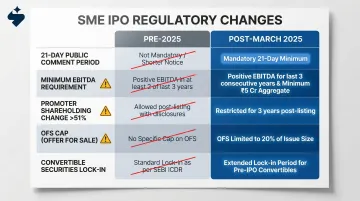

How your BRLM coordinates also depends on which exchange you're listing on. For SME IPOs, the exchange (BSE SME or NSE Emerge) historically acted as the primary reviewer. The March 2025 ICDR Amendments changed this significantly:

| Requirement | Pre-2025 | Post-March 2025 |

|---|---|---|

| 21-day public comment | Not uniformly required | Mandatory |

| Minimum EBITDA | None | ₹1 crore in 2 of 3 preceding FYs |

| Promoter change >51% | Exchange-specific rules | 1-year wait from change |

| OFS cap | No specific cap | 20% of total issue size |

| Convertible securities | No specific rule | Must convert before RHP filing (except ESOPs) |

SME issuers who haven't prepared for these requirements pre-filing will now face revision cycles comparable to Main Board.

The 12-Month Validity Window

Once issued, the Observation Letter is valid for 12 months (18 months in certain cases). Companies often wait for favorable market conditions before launching — a reasonable strategic choice, but one with a hard deadline.

If the Observation Letter expires, the company must refile and restart the process entirely. SEBI granted a one-time extension for letters expiring between April–September 2026, citing weak market conditions — that's the exception, not the rule.

Common Misconceptions About the SEBI IPO Timeline

Misconception 1: Many companies read the Observation Letter as SEBI's approval. It isn't. The letter confirms disclosure compliance only — SEBI does not endorse your valuation, business model, or the merits of the investment. The company retains full legal liability for every statement in the prospectus.

Misconception 2: The 30-day rule is often treated as a guaranteed deadline from filing day. It isn't. The clock starts only after SEBI receives satisfactory clarifications and stock exchange in-principle approval. If queries arise and responses take time, the actual elapsed time from filing to Observation Letter can reach 60–90 days or beyond.

Misconception 3: Once filed, founders often assume the timeline is mostly SEBI's problem. It isn't. Most delay points sit squarely within the company's control:

- How quickly the team responds to SEBI queries

- Whether financials require restatement after submission

- How well-coordinated the intermediaries are during the review window

Companies that treat filing as the finish line experience longer timelines — the ones that stay operationally sharp after submission consistently close faster.

When the SEBI IPO Timeline Extends: Common Triggers

Financial Restatements and Audit Discrepancies

The most frequent delay trigger. When SEBI or the exchanges identify inconsistencies between quarterly results and audited financials, unexplained revenue jumps near filing, or revenue recognition practices that don't align with Ind-AS, the company enters an extended clarification cycle. Every round resets the 30-day clock.

Inadequate Disclosure of Related-Party Transactions, Litigations, and KPIs

SEBI's November 2022 ICDR Amendments mandated KPI disclosures covering the 3 years preceding DRHP filing, audited by the statutory auditor, with period alignment to restated financials. Companies that haven't prepared audited KPI data pre-filing — or whose material litigation disclosures fall short of required thresholds — face the same revision cycles.

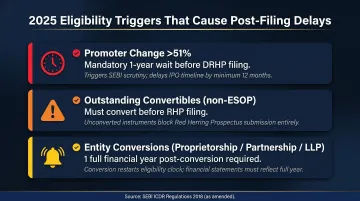

Promoter and Shareholder Eligibility Issues

Under the 2025 SEBI ICDR Amendments:

- Promoter changes exceeding 51% require a mandatory 1-year wait before DRHP filing

- Outstanding convertible securities (other than ESOPs) must be converted before RHP filing

- Companies converted from proprietorship/partnership/LLP must have completed 1 full financial year post-conversion

Catching these issues after filing — rather than during a pre-filing readiness scan — causes some of the longest delays in the process.

Frequently Asked Questions

How long does it take to get an IPO after filing with SEBI?

The typical timeline from DRHP filing to listing runs 3 to 6 months for well-prepared companies. Complex cases can stretch to 12 months, the full validity window of the Observation Letter. The Observation Letter itself is typically issued within 30–75 days of filing, depending on how many clarification rounds SEBI requires.

What is the 30-day rule for IPOs?

SEBI's 30-day rule refers to the regulator's obligation to issue its Observation Letter within 30 days of receiving satisfactory clarifications from the lead manager or in-principle listing approval from the stock exchanges. It does not run from the date of DRHP filing — the clock starts only after SEBI has what it needs to complete its review.

What is the 90-day rule for IPOs?

The 90-day rule comes from Section 26(8) of the Companies Act, 2013, which invalidates any prospectus issued more than 90 days after its delivery to the Registrar of Companies. Once the RHP is filed with the RoC, the company has 90 days to open the public issue — after that, the prospectus lapses and must be refiled.

Can a private company or startup go for an IPO?

Yes. A private limited company must first convert to a public limited company under Section 18 of the Companies Act, 2013, then meet SEBI's eligibility criteria under the ICDR Regulations. Startups may also qualify for the Innovators Growth Platform (IGP) under Chapter X of the ICDR Regulations, provided at least 25% of pre-issue capital has been held by eligible investors (QIBs or accredited investors) for a minimum of 2 years.

Who is not eligible for an IPO in India?

Under Regulation 5(1)(b) of the SEBI ICDR Regulations, ineligible issuers include companies or promoters debarred by SEBI, those with outstanding obligations to prior investors, and issuers where the ultimate promoter cannot be identified. The 2025 SME ICDR Amendments add two more bars: unconverted securities (other than ESOPs) outstanding, and a promoter change exceeding 51% in the preceding year.

What are the different types of IPOs?

Indian IPOs differ across four dimensions:

- Pricing method: Fixed-price or book-building

- Exchange: Main Board (NSE/BSE) or SME (NSE Emerge/BSE SME)

- Issue type: Fresh issue, offer for sale, or a hybrid of both

- Platform: Regular equity, IGP for qualifying startups, or the Social Stock Exchange for social enterprises