Introduction

Most founders preparing for an SME listing focus on eligibility — and miss the fact that compliance doesn't end at listing day. It restructures how your company operates from that point forward.

Pre-listing eligibility covers the financial, governance, and structural requirements that determine whether your company qualifies to list on BSE SME or NSE Emerge. These are threshold criteria — pass them, and you're in.

Post-listing obligation is a different challenge entirely: an ongoing calendar of quarterly, half-yearly, annual, and event-triggered filings that govern how you operate as a public company from day one.

SEBI's July 2025 amendments have tightened both ends of this spectrum. The new rules introduced a mandatory EBITDA threshold, raised minimum application sizes, and capped offer-for-sale structures — shifts that affect both who qualifies and what's required after listing.

This guide covers SEBI's eligibility criteria, the BSE SME vs NSE Emerge comparison, the pre-listing compliance checklist, and the full post-listing filing calendar. By the end, you'll know exactly where your company stands — and what needs to change before you file.

Key Takeaways

- Post-issue paid-up capital must be ₹25 crore or less to qualify for an SME platform listing

- Minimum EBITDA of ₹1 crore in at least 2 of the last 3 financial years is now mandatory under July 2025 SEBI rules

- Post-listing compliance is governed by SEBI LODR Regulations 2015 — covering quarterly, half-yearly, annual, and event-based filings

- Missing deadlines can trigger penalties, trading restrictions, or placement under GSM/ASM surveillance

- Migration to the main board requires minimum 3 years of listing on the SME exchange

SEBI Eligibility Criteria for SME Listing

Paid-Up Capital and Profitability Thresholds

The foundational eligibility gate is straightforward: post-issue paid-up capital must not exceed ₹25 crore on a face value basis. Companies in the ₹10–25 crore band have the option to choose between the SME platform and the main board, subject to additional conditions under Chapter IX of SEBI ICDR Regulations 2018.

The more significant change from July 2025 is the profitability requirement. SEBI now mandates minimum EBITDA of ₹1 crore in at least 2 of the preceding 3 financial years, per the SEBI Board decision of December 18, 2024.

This signals a deliberate shift toward listing-readiness quality: demonstrated operating surplus, not just revenue growth.

Beyond financial thresholds, eligibility also depends on operational history and governance structure.

Track Record and Conversion Rules

- Companies must have at least 3 years of operational track record — either at the company level or through the promoter's track record

- Entities converted from proprietorship, partnership, or LLP must complete at least one full financial year as a company before filing the DRHP

- If promoters change by more than 50%, a one-year cooling-off period applies before DRHP filing is permitted

Promoter and Share Structure Requirements

- Minimum promoter contribution of 20% of post-issue capital, subject to lock-in under ICDR provisions

- 100% of promoter shareholding must be in demat form before filing

- OFS by selling shareholders is capped at 20% of total issue size, with each selling shareholder limited to offloading no more than 50% of their pre-issue holding

- IPO proceeds cannot be used to repay loans from promoters, the promoter group, or related parties

Disqualification Conditions

Under Regulation 228 of SEBI ICDR, the following conditions disqualify a company from listing:

- SEBI debarment of the issuer, promoters, directors, or selling shareholders

- Wilful defaulters or fraudulent borrowers declared by banks or financial institutions

- Fugitive economic offenders under the Fugitive Economic Offenders Act 2018

- Outstanding convertible securities or rights entitling any person to subscribe for equity shares

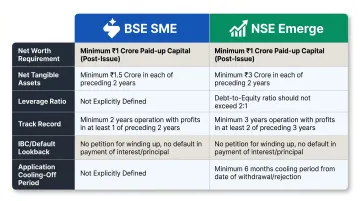

BSE SME vs NSE Emerge: Platform-Specific Requirements

Eligibility Comparison

| Criteria | BSE SME | NSE Emerge |

|---|---|---|

| Net worth requirement | ₹1 crore for 2 consecutive preceding years | Positive net worth |

| Net tangible assets | ₹3 crore | ₹3 crore in last financial year |

| Leverage ratio | Up to 3:1 | Up to 3:1 |

| Track record | 3 years | 3 years |

| IBC/default lookback | No defaults in last 3 years | No defaults in last 3 years |

| Application rejection cooling-off | 6 months | 6 months |

Both platforms align with SEBI ICDR Chapter IX on the post-issue capital ceiling and EBITDA requirements. The platform-level gates add financial depth filters on top of the SEBI baseline.

NSE Emerge also imposes higher net worth thresholds for specific sectors — broking companies and microfinance institutions face additional requirements. Both exchanges mandate an active company website and full compliance with Companies Act 2013 board constitution requirements before granting approval.

Once you've confirmed eligibility across these thresholds, the next practical question is where and how to file.

Filing Infrastructure

The submission portals are distinct and non-interchangeable:

- BSE SME uses the BSE Listing Centre portal for all compliance submissions

- NSE Emerge uses NEAPS (NSE Electronic Application Processing System)

The key structural difference: NSE Emerge uses an Integrated Governance Filing that consolidates Regulations 13(3), 27(2), and portions of Regulation 30 into a single submission. BSE files these separately.

This distinction directly affects how your compliance team organises quarterly submissions and who owns each filing component — something worth mapping before your first reporting cycle.

Pre-Listing Compliance Checklist and Listing Process

Corporate Governance Foundations

Before the DRHP is filed, the following governance structures must be in place — and must remain operational after listing:

- Appointment of independent directors in required numbers

- Constitution of an audit committee with appropriate composition

- Establishment of a risk management policy

- Adoption of a code of conduct for directors and senior management

- Creation of an investor grievance redressal mechanism

Financial and Documentation Readiness

- 3 years of audited financial statements prepared under Schedule III of the Companies Act 2013

- Audits certified by an ICAI Peer Review Board-certified auditor — not all chartered accountants qualify

- Clean audit reports without qualifications that would require explanation in the DRHP

- Firm financial arrangements for at least 75% of proposed project financing, excluding IPO proceeds themselves

- All securities in dematerialised form with NSDL or CDSL

DRHP Preparation and Regulatory Approval

A SEBI-registered merchant banker (lead manager) prepares the DRHP after conducting due diligence across financials, key contracts, statutory approvals, and promoter credentials. The process runs as follows:

- DRHP submission to the chosen exchange for in-principle approval

- Site inspection and Listing Advisory Committee interaction by the exchange

- In-principle approval issued by the exchange

- Final RHP filing with the exchange and the Registrar of Companies

For IPOs exceeding ₹50 crore, appointment of a monitoring agency is mandatory under ICDR.

One practical note on timing: SEBI's July 2025 rules raised the minimum application size to 2 lots with a value exceeding ₹2 lakh across all investor categories. The intent is to attract research-backed investors who have evaluated the issue — not retail applicants chasing listing gains. This affects lot size modeling and distribution strategy during the marketing phase. This affects lot size modeling and distribution strategy during the marketing phase — and it's one more reason why preparation timelines can't be compressed at the back end.

The 12–18 Month Preparation Window

Founders should begin IPO readiness work at least 12–18 months before the target listing date. This lead time isn't arbitrary — most of the gaps that delay DRHP filing or invite SEBI observations take months to fix, not weeks.

S45's AI-powered IPO Readiness Scan covers the dimensions most likely to surface issues: financial track, free float, board independence, demat readiness, statutory dues, and material litigation — all screened against SEBI ICDR criteria in 30 minutes.

The AI Risk Radar goes further, flagging problems before formal diligence begins:

- ESOP dilution not reflected in the cap table

- Audit committee composition gaps

- Undisclosed contingent liabilities

- Inconsistent revenue recognition across periods

For companies that arrive with clean inputs, S45's structured DRHP drafting process — executed with Narnolia (Category-I SEBI-Registered Lead Manager) — delivers a DRHP-ready draft in 30–45 days. That beats the 90+ day conventional drafting timeline and compresses the overall SME IPO engagement-to-listing window to 2–3 months.

Post-Listing Compliance for SME-Listed Companies

Once listed, SME companies operate under SEBI LODR Regulations 2015, the Companies Act 2013, and exchange-specific guidelines from BSE SME or NSE Emerge. Obligations fall into four categories: quarterly, half-yearly, annual, and event-based — each with distinct deadlines and consequences for missing them.

Quarterly Compliance Obligations

| Filing | Regulation | Deadline |

|---|---|---|

| Integrated Governance Filing (investor grievances + governance report) | Regs 13(3) and 27(2) | Within 30 days from quarter end |

| Reconciliation of Share Capital Audit Report | Reg 76, SEBI DP Regulations | Within 30 days from quarter end |

| RTA Certificate (demat compliance) | Reg 74(5), SEBI DP Regulations | Within 15 days of receipt from RTA |

Half-Yearly Compliance Obligations

SME-listed companies file financial results half-yearly — not quarterly like mainboard companies. This is a meaningful difference and must be built into the finance team's close calendar.

| Filing | Regulation | Deadline |

|---|---|---|

| Shareholding pattern | Reg 31(1)(b) | Within 21 days from half-year end |

| Financial results | Reg 33(5) | Within 45 days (H1) / 60 days (H2) |

| Statement of deviation/variation in IPO proceeds | Reg 32(8) | 45 days (H1 end) / 60 days (H2 end), if deviation exists |

| Trading window closure intimation | PIT Regulations | 2 working days before half-year end |

Annual Compliance Obligations

- Annual audited financial results (Reg 33(5)): within 60 days from financial year end

- Annual report (Reg 34(1)): dispatched to shareholders by AGM date

- Structured Digital Database (SDD) certificate under PIT Regulations: within 60 days from financial year end

- Promoter shareholding disclosure under SAST Regulations: within 7 working days from financial year end

Event-Based Compliance Obligations

Event-based disclosures are the most time-sensitive category, and in practice the most frequently missed.

Under Regulation 30:

- Board decisions: disclosed within 30 minutes of conclusion

- Events originating within the entity: within 12 hours

- External-trigger events: within 24 hours

Additional event-based timelines:

- Board meeting prior notice: at least 2 working days in advance

- Record date notice for dividends or bonus: at least 7 clear working days (5 days for dividend/bonus)

- Voting results from general meetings: within 2 working days of conclusion

- Company name change: requires prior exchange approval before ROC filing

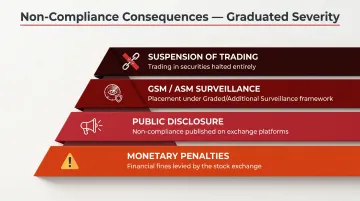

Consequences of Non-Compliance and Migration to Main Board

Penalties for Missing Deadlines

Non-compliance with SEBI LODR obligations attracts graduated consequences:

- Monetary penalties from the exchange, varying by type and frequency of default

- Public disclosure of the non-compliance on exchange platforms

- Placement under GSM (Graded Surveillance Measure) or ASM (Additional Surveillance Measure) frameworks, which restrict trading and impose additional scrutiny on price movements

- Suspension of trading in the company's securities in repeated or egregious cases

SEBI maintains a consolidated index of adjudication orders for LODR non-compliance. The quantum of penalties varies — but the reputational damage of public flagging and surveillance placement often exceeds the monetary fine itself, particularly for SME companies where institutional investor confidence is fragile.

Migration to the Main Board

Migration from BSE SME or NSE Emerge to the respective main board (BSE or NSE) requires:

- Minimum 3 years of listing and trading on the SME exchange

- Main board eligibility criteria at the time of application — industry checklists commonly reference minimum paid-up capital of ₹10 crore and market capitalisation thresholds around ₹100 crore (confirm against the live exchange circular before filing)

- NSE revised its migration criteria under circular CML67671 dated April 24, 2025 — check the current version directly

- Exchange approval, where compliance track record is a central evaluation factor

A clean compliance history — structured filings, timely disclosures, consistent investor relations — directly improves a company's migration case. Exchanges evaluate the full track record, not just the final year.

S45's post-listing IR programme for SME companies covers exactly this ground: compliance calendar management, earnings materials, analyst coverage coordination, and market maker integration across a 30/90-day engagement window. Companies that build institutional-grade investor relations from day one arrive at migration eligibility with documented evidence of governance discipline — not just a clean filing ledger.

Frequently Asked Questions

What compliances apply to SME-listed companies?

Post-listing SMEs must comply with SEBI LODR Regulations 2015, the Companies Act 2013, and exchange-specific norms from BSE SME or NSE Emerge. Key filings include:

- Quarterly governance and share capital reports

- Half-yearly financials and shareholding patterns

- Annual audited financial results and annual report

- Event-based disclosures for material developments under Regulation 30

What are the eligibility criteria to list on the SME platform?

Key thresholds: post-issue paid-up capital of ₹25 crore or less, minimum EBITDA of ₹1 crore in 2 of the last 3 financial years, at least 3 years of operational track record, promoter contribution of 20% or more, 100% demat of promoter shares, and no defaults, SEBI debarment, or IBC proceedings.

What are the new SEBI rules for SME IPOs effective from July 2025?

The main changes: mandatory EBITDA of ₹1 crore in 2 of 3 preceding years, OFS capped at 20% of issue size with a 50% per-shareholder limit, minimum application size raised to 2 lots (value exceeding ₹2 lakh), monitoring agency required for IPOs above ₹50 crore, and a phased lock-in for promoter shareholding exceeding minimum contribution.

What happens if a listed SME misses a compliance deadline?

Missing deadlines attracts monetary penalties from the exchange, public disclosure of non-compliance, and potential placement under GSM or ASM surveillance frameworks. Repeated defaults can result in suspension of trading in the company's securities.

How does SME platform compliance differ from mainboard compliance?

SME-listed companies file financial results half-yearly rather than quarterly, and operate under simplified corporate governance norms. The frequency and volume of filings is lighter than mainboard but still mandatory under SEBI LODR — and the event-based disclosure timelines (30 minutes to 24 hours) apply with the same urgency.

Can an SME company migrate to the main board?

Yes — after a minimum of 3 years of listing and trading on BSE SME or NSE Emerge, subject to meeting main board eligibility criteria and exchange approval. A clean compliance track record is a key factor in the migration review.