Introduction

Most Indian founders approach an IPO convinced they are ready—only to discover, weeks into the process, that their financials need restatement, key documents are missing, or their governance structure falls short of SEBI's requirements. This harsh reality often surfaces after engaging advisors, filing forms, and committing resources.

IPO readiness is not a feeling. It is a verifiable state across financials, legal structure, governance, and compliance. According to PRIME Database, 18 companies allowed their SEBI approvals to lapse in FY26, and 15 withdrew their offer documents entirely—representing over ₹31,600 crore in unexecuted mandates. These failures typically trace back to gaps that could have been identified months earlier.

The checklist below covers six critical areas of IPO readiness under SEBI's framework—financials, legal structure, governance, compliance, and more. Work through each section to identify exactly where you stand before engaging advisors or filing anything.

TLDR: IPO Readiness Checklist at a Glance

- Financial readiness: Three years of Ind AS financials, independently audited, with clean working capital statements

- Legal readiness: Public limited conversion done, promoter lock-ins confirmed, related party transactions disclosed at arm's length

- Governance readiness: Independent directors appointed, audit and nomination committees in place, KMPs experienced

- SEBI compliance: Eligibility thresholds met, DRHP documentation assembled, no outstanding regulatory issues

- Team readiness: Merchant banker, legal counsel, auditor, and registrar engaged — with a 12–18 month roadmap locked in

What Is IPO Readiness?

IPO readiness means a company has addressed every financial, legal, governance, and regulatory requirement needed to file a Draft Red Herring Prospectus (DRHP) and function as a listed entity.

This differs from simply being a good business. Strong revenue growth and a compelling market story don't compensate for gaps in restated financials, incomplete disclosures, or a weak board structure.

Two Listing Pathways in India

Indian companies face two distinct listing routes:

| Route | Exchange | Key Difference |

|---|---|---|

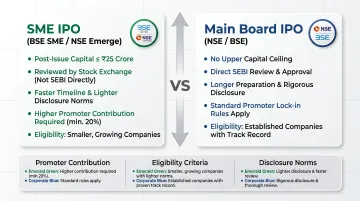

| SME IPO | BSE SME / NSE Emerge | Post-issue capital ≤ ₹25 crore; reviewed by stock exchange |

| Main Board | NSE / BSE | No capital limit; direct SEBI review |

Eligibility thresholds, promoter contribution rules, and disclosure norms differ materially between these tracks — founders must confirm which route they qualify for before any preparation work begins, as the choice shapes the entire timeline and regulatory path.

Why Early Preparation Matters

IPO readiness is not a one-time snapshot. SEBI's review process, the due diligence conducted by lead managers, and the scrutiny of institutional investors during bookbuilding create multiple checkpoints where gaps surface.

Discovering a gap late costs months of delay and damages your credibility with bankers and investors at exactly the wrong moment.

According to SEBI's ICDR Regulations, SEBI issues observations on Main Board DRHPs within 30 days of receiving a satisfactory reply to clarifications. The 30-day clock starts only after all clarifications are addressed — meaning multiple rounds of back-and-forth can push the actual timeline well beyond 30 days.

For SME IPOs, the stock exchange (not SEBI) conducts the review, but the iterative nature of the process remains the same. With 240 companies filing offer documents in FY26—up from 166 in FY25—the pipeline is crowded. Early, clean filings move through the queue faster and signal credibility to institutional investors.

Financial and Accounting Readiness

Restated Financial Statements

SEBI requires three full financial years of restated consolidated and standalone financial statements prepared under Ind AS (Indian Accounting Standards), as mandated by Schedule VI, Part A of the ICDR Regulations. Additionally, a stub period is required if the last audited year is more than six months old at the time of filing.

"Restated" means more than reprinting audited accounts. It requires adjusting for:

- Accounting policy changes

- Prior period errors

- Changes in group structure

Present all years on a consistent basis. This restatement exercise alone typically takes 2–3 months and demands close collaboration between management and auditors.

Auditor independence carries significant weight here. SEBI and stock exchanges require the statutory auditor to issue a restated financials report. Any history of auditors providing non-audit services must be reviewed carefully, and switching auditors mid-process forces the incoming auditor to re-examine prior year work — a delay founders should eliminate before filing prep begins.

Working Capital Assessment

SEBI scrutinises the objects of the issue closely. If a company is raising funds to meet working capital needs, it must provide a detailed working capital computation certified by a banker. Weak documentation here is one of the most common SEBI observation points, so prepare the working capital memorandum well before DRHP drafting begins — during the readiness assessment phase, not after.

Key Financial Metrics and Operating Data

Beyond GAAP financials, SEBI's DRHP disclosures require Key Performance Indicators (KPIs) that management uses to run the business.

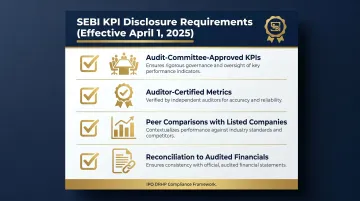

In February 2025, SEBI introduced industry-standardised KPI disclosure requirements effective April 1, 2025. All DRHPs filed from that date onward must include:

- Audit-committee-approved KPIs

- Auditor-certified metrics

- Peer comparisons with Indian (and global, where available) listed companies

- Clear reconciliation to audited financials

Any metric mentioned in the investor narrative must be backed by a consistent calculation methodology. Undisclosed changes to how KPIs are defined across periods will draw SEBI observations.

Financial Forecasting Infrastructure

Forward projections are not filed with SEBI, but institutional buyers and QIBs expect credible internal financial models during bookbuilding. Companies that arrive at roadshows without them signal weak governance — and that perception is difficult to reverse mid-process.

Build planning and forecasting infrastructure well before the IPO window. During pricing discussions, bankers need to stress-test assumptions quickly; a live model with auditable inputs is what separates a confident pricing conversation from a delayed one.

Legal, Corporate, and Governance Readiness

Corporate Structure and Promoter Holdings

A company must be incorporated as a public limited company under the Companies Act 2013 before filing a DRHP. If currently private limited, conversion is required.

Conversion process timeline: 60–90 days, involving:

- Altering the memorandum of association

- Filing forms with the Registrar of Companies (RoC)

- Obtaining shareholder approvals

Any subsidiaries, step-down subsidiaries, or associate companies must be accurately disclosed in the corporate structure. SEBI requires full group-level disclosures.

Promoter Lock-In and Minimum Contribution

Under SEBI's ICDR Regulations, promoters must:

- Contribute a minimum 20% of post-issue paid-up capital

- Lock in this contribution for 18 months (or 3 years if majority of proceeds used for capex)

- Lock in excess promoter holding for 6 months (or 1 year if capex route)

Action items:

- Map current promoter holding

- Identify any pledge or encumbrance on shares

- Audit all historical share transfers to ensure a clean, auditable cap table

Pledged shares or disputed transfers will trigger queries and delay SEBI review — often at the worst possible moment in the filing timeline.

Related Party Transactions (RPTs)

All transactions with promoters, promoter group entities, directors, and their relatives must be identified, disclosed in the DRHP, and demonstrably at arm's length.

SEBI will flag RPTs that were not approved through the appropriate board or audit committee process.

Conduct an internal RPT audit at least 12 months before filing. Put proper approval frameworks in place immediately — retroactive fixes rarely hold up under scrutiny.

Board Composition and Key Management

SEBI's Listing Obligations and Disclosure Requirements (LODR) Regulations govern board composition for listed companies:

Independent Director Requirements:

- At least one-third of the board (or one-half if chairperson is executive or promoter-related)

- At least one woman director (top 1,000 entities must have at least one independent woman director)

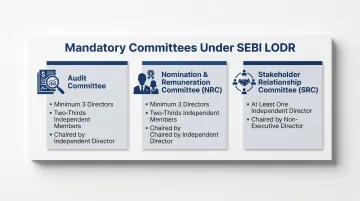

Mandatory Committees:

| Committee | Composition | Chair |

|---|---|---|

| Audit | Minimum 3 directors; two-thirds independent | Independent director |

| Nomination & Remuneration (NRC) | Minimum 3 directors; two-thirds independent | Independent director |

| Stakeholder Relationship (SRC) | At least one independent director | Non-executive director |

Begin recruiting independent directors 12–18 months before filing. These directors need time to understand the business deeply. The recruitment process itself takes 3–6 months for quality candidates with relevant sector and public-company experience.

Key Management Personnel (KMP) Continuity

SEBI and investors assess management depth closely. Fill these roles with professionals who have done this before:

- CFO — owns the MD&A section of the DRHP; public-company reporting experience is non-negotiable

- Company Secretary — serves as the primary compliance officer throughout the process

- Compliance heads — sector-specific regulatory knowledge matters, especially for financial services, healthcare, and defence

Investors notice gaps here fast. A management team without credible depth in these roles will face pointed questions during roadshows — and the answers matter.

SEBI Compliance and Regulatory Readiness

Eligibility and ICDR Requirements

Main Board IPO — Profitability Route (Regulation 6(1)):

| Criterion | Threshold | Period |

|---|---|---|

| Net tangible assets | At least ₹3 crore | Each of preceding 3 years |

| Average pre-tax operating profit | At least ₹15 crore | 3 of preceding 5 years |

| Net worth | At least ₹1 crore | Each of preceding 3 years |

| Issue size cap | Not more than 5x pre-issue net worth | Per audited balance sheet |

Main Board IPO — QIB Route (Regulation 6(2)):

For issuers not meeting the profitability track record, the issue must allocate at least 75% of the net offer to Qualified Institutional Buyers (QIBs).

SME IPO — NSE Emerge Eligibility:

| Criterion | Threshold |

|---|---|

| Post-issue paid-up capital | Must not exceed ₹25 crore |

| Operating profit (EBITDA) | At least ₹1 crore in 2 of preceding 3 years |

| Net worth | Positive |

| Promoter holding | At least 20% of post-issue equity |

Action item: Confirm your eligibility route early. Companies not meeting Main Board profitability thresholds have a viable QIB alternative—but the distribution strategy and investor base differ fundamentally.

Legal and Regulatory Issues

Any pending legal proceedings against the company, promoters, or directors that are material (above SEBI's prescribed thresholds) must be disclosed in the DRHP.

Outstanding items requiring resolution or disclosure:

- Tax demands

- Regulatory penalties

- Litigation involving amounts exceeding materiality thresholds

A pre-filing legal audit by experienced capital markets counsel is essential. This audit should be completed at least 6 months before target DRHP filing to allow time for remediation.

DRHP Documentation and Disclosure Readiness

With legal issues identified and remediated, the next step is assembling the documentation that underpins every disclosure. The DRHP covers:

- Restated financials

- Management biographies

- Risk factors

- Objects of the issue

- Capital structure

- Related party disclosures

- Material contracts

- Industry and business sections

The DRHP is drafted jointly by the lead manager (merchant banker), legal counsel, and management—but management must own the accuracy of every disclosure.

Founders should collect and organise all material agreements, licenses, regulatory approvals, and key contracts into a data room before drafting begins. Incomplete documentation is the primary reason DRHP drafting timelines overrun.

S45's AI-powered data room and evidence-linked drafting workflow delivers a DRHP-ready draft in 30–45 days—versus the 3–6 months typical of traditional processes. The platform links every disclosure statement directly to supporting source documents, ensuring accuracy and minimising SEBI observation risk.

SEBI Observation Process

After DRHP filing, SEBI typically issues observations:

- Main Board: Within 30 days (from receipt of satisfactory reply)

- SME: Stock exchange review (NSE Emerge / BSE SME)

Observations are clarifications and modifications SEBI requires before the Red Herring Prospectus (RHP) can be filed and the IPO opened.

Companies that address common SEBI observations proactively—around financial disclosures, promoter background, and risk factor language—reach listing faster with fewer rounds of clarification.

In FY26, 144 companies received SEBI approval to raise approximately ₹1.75 lakh crore, while 63 companies await approval seeking ₹1.37 lakh crore. The pipeline is at a structural high—clean, complete filings move faster.

Assembling Your IPO Team and Setting a Realistic Timeline

Mandatory Advisors

Before DRHP filing, a company must appoint:

| Advisor | Role | Typical Fee Range |

|---|---|---|

| Category I Merchant Banker (Lead Manager) | Drives entire IPO process—readiness, DRHP drafting, bookbuilding, listing | 1–5% of issue size (higher for smaller deals); ₹4,113 crore total fees in 2025 |

| Statutory Auditor | Issues restated financials report | ₹2–5 lakhs (SME); negotiated for Main Board |

| Registrar to the Issue (RTI) | Manages application processing and allotment | ₹5–10 lakhs (SME); negotiated for Main Board |

| Legal Counsel | Drafts legal opinions, reviews DRHP | ₹2–5 lakhs (SME); up to ₹15 crore for large/complex Main Board deals |

| Bankers to the Issue | Manages escrow and refunds | Varies |

For Main Board IPOs, a syndicate of co-managers and sub-brokers is also assembled.

The lead manager shapes every phase of the IPO — from readiness through listing. Choosing a banker with genuine sector depth and a track record of well-subscribed, disciplined deals determines whether the process moves with speed or stalls at each gate.

Realistic IPO Preparation Timeline

Main Board IPO:

- Pre-filing preparation (financials restatement, legal audit, DRHP drafting): 9–12 months

- SEBI observations and RHP finalisation: 1–3 months

- Roadshow and bookbuilding: 2–4 weeks

- Total: 12–18 months from decision to listing

SME IPO:

- Pre-filing preparation: 6–9 months

- Exchange review and observations: 1–2 months

- Bookbuilding and listing: 2–4 weeks

- Total: 6–9 months

Industry benchmarks from PRIME Database recommend an 18-month runway minimum for Main Board IPOs to institutionalise governance and financial discipline.

Companies that skip preparation steps do not compress the timeline. They recover it later — under pressure, with SEBI observations queued and bookbuilding stalled by inadequate demand mapping.

The Value of a Readiness Assessment

Before engaging advisors, a structured readiness assessment evaluates the company across all six dimensions in this checklist, identifies gaps with time and cost implications, and prioritises remediation actions.

This prevents founders from walking into a banker meeting blind.

S45's AI-led readiness assessment maps the company across six dimensions before a single advisor is engaged:

- ICDR eligibility

- Disclosure gaps

- Governance and control weaknesses

- Documentation completeness

That analysis produces a concrete output founders can act on immediately:

- Readiness score with a prioritised fix list

- Timeline and critical milestones

- Resource requirements

- Clear action plan

Timelines:

- Preliminary assessment: 5 business days

- Comprehensive assessment: 2–3 weeks

Founders arrive at the mandate stage with documented evidence rather than assumptions—and can move from first call to signed mandate in approximately 7 days when readiness work is complete.

S45 operates as an AI-native investment bank, partnering with Narnolia as SEBI-registered Category-I Merchant Banker. Sector bankers work inside a live data room with proprietary AI analytics — enabling DRHP-ready drafts in 30–45 days and the same institutional discipline across both Main Board and SME mandates.

Since July 2023, S45 has executed 26 IPOs, raised over ₹1,180 crore in capital, and generated ₹1,83,000+ crore in bids — with an average subscription of 168x and a listing pop of 43%.

Frequently Asked Questions

What is IPO readiness?

IPO readiness is the state in which a company has addressed all financial, legal, governance, and regulatory requirements to file a DRHP with SEBI and operate as a publicly listed company. It goes beyond strong revenue or a compelling business case — structural, legal, and governance gaps will block a filing regardless of fundamentals.

How to prepare a company for IPO?

Core preparation steps include:

- Restate three years of financials under Ind AS with independent audit certification

- Audit corporate structure, promoter holdings, and related party transactions

- Constitute a SEBI-compliant board with independent directors and mandatory committees

- Resolve outstanding legal, regulatory, and contingent liability issues

- Engage a SEBI-registered merchant banker to lead the DRHP drafting process

How long does IPO readiness take?

For a Main Board IPO in India, the preparation phase typically takes 9–12 months before DRHP filing, with the full journey from decision to listing taking 12–18 months. SME IPOs can be faster at 6–9 months, assuming the company begins with clean financials and governance already in place.

What is IPO compliance?

IPO compliance in India means adhering to three overlapping frameworks: SEBI's ICDR Regulations (eligibility, disclosures, issue structure), the Companies Act 2013, and the LODR Regulations. LODR governs ongoing post-listing obligations — board composition, periodic disclosures, and related party transaction approvals.

What is the IPO process in accounting?

The accounting component covers five areas:

- Restating historical financial statements under Ind AS

- Obtaining independent audit certification of restated financials

- Preparing a working capital adequacy report

- Disclosing non-GAAP KPIs with reconciliation to audited figures

- Ensuring consistent accounting policies across the full disclosure period