Introduction

Going public is one of the highest-stakes decisions a founder will make. Timing and preparation determine outcomes — launch too early and you invite regulatory pushback, weak demand, and a damaging first-day stumble. Start late and you face last-minute chaos: delayed filings, strained investor confidence, and a valuation that reflects your urgency rather than your business.

The question every founder eventually confronts is: how do I objectively know if my business is ready?

This article lays out a practical, India-specific framework to self-assess readiness across five dimensions — what to measure, where most companies fall short, and what to do about it. True IPO readiness means withstanding the full scrutiny of institutional investors, regulators, and public markets from Day 1 of filing, then sustaining that confidence well after listing. Meeting SEBI's minimum eligibility conditions is just the starting point.

Key Takeaways

- IPO readiness means operating like a public company before you become one — not just meeting minimum filing criteria

- Five dimensions determine readiness: financial health, legal eligibility, governance quality, narrative for investors, and operational infrastructure

- Each dimension gets a traffic-light score: Green (ready now), Amber (fixable gaps), or Red (structural problems that must be resolved before filing)

- Typical time from readiness review to DRHP-filing: 12-24 months of remediation, depending on gaps identified

- Founders who self-assess poorly face DRHP delays, forced valuation reductions, and SEBI clarification rounds

What Does "IPO Ready" Actually Mean in India?

IPO readiness means more than clearing SEBI's minimum eligibility thresholds. It means withstanding the scrutiny of institutional investors, regulators, and public markets — before the ink dries on your DRHP.

The modern definition of IPO readiness has shifted since 2021. Following the IPO corrections where 38% of 2021 Main Board stocks traded below their issue price, the bar has risen. Readiness now means "can we sustain investor confidence after listing?" not just "can we file?"

That question gets answered differently depending on which listing route applies to your business.

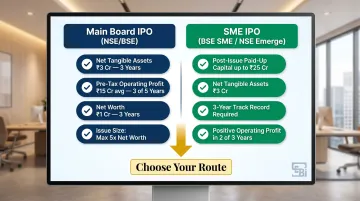

Main Board vs. SME IPO Paths

Eligibility thresholds differ between Main Board (NSE/BSE) and SME IPO (BSE SME/NSE Emerge) routes.

Main Board Eligibility - Profitability Route (SEBI ICDR Regulation 6(1)):

- Net tangible assets: At least ₹3 Cr in each of the preceding 3 years

- Average pre-tax operating profit: At least ₹15 Cr during any 3 of the last 5 years

- Net worth: At least ₹1 Cr in each of the preceding 3 years

- Issue size: Cannot exceed 5x pre-issue net worth

Main Board - QIB Route (Regulation 6(2)):

- Profitability thresholds above do not apply

- At least 75% of the net offer must be allocated to Qualified Institutional Buyers (QIBs) via book building

SME IPO Eligibility (BSE SME and NSE Emerge):

- Post-issue paid-up capital: Up to ₹25 Cr (ceiling)

- Net tangible assets: ₹3 Cr minimum

- Track record: At least 3 years

- Operating profit: Positive in 2 of 3 latest financial years

- Net worth: ₹1 Cr for 2 preceding years (BSE SME)

Sources: SEBI ICDR Regulations 2018; BSE SME Criteria.

Companies approaching the ₹25 Cr paid-up capital ceiling face a hard fork: push toward Main Board or consolidate on the SME route. Getting that call wrong early costs months of repositioning later.

The Five Dimensions of IPO Readiness

A business needs to be honest across all five dimensions, not just the ones it performs well in. This is a structured self-assessment framework covering the areas that underwriters, SEBI, and institutional investors scrutinize most rigorously.

Financial Readiness

Three-Year Audit Requirements:

Your audited financials must cover three years of accounts audited to Indian Accounting Standards (Ind AS), not PCAOB standards as some founders assume. SEBI requires financial statements prepared under Ind AS and audited by ICAI-registered firms with valid Peer Review Certificates.

Core requirements:

- Clean revenue recognition policies

- Consistent segment reporting

- Restated consolidated financial statements across all periods

- Credible path to profitability or demonstrated sustained profitability

Source: EY - Restatement of Financial Statements.

Key Financial Red Flags:

These issues surface during DRHP drafting and kill timelines:

- Inconsistent revenue recognition across periods

- Unresolved related-party transactions without clear arm's-length pricing

- Informal expense booking that can't be independently verified

- Lack of quarterly forecasting discipline

- Audit qualifications in prior years that haven't been resolved

A study by Uniqus and IVCA found that SEBI issues approximately 100 observations per DRHP, with 13% relating to financial disclosures—including restated account inconsistencies and revenue recognition issues.

Legal and Regulatory Eligibility

SEBI ICDR Eligibility Criteria You Must Verify:

Before approaching any banker, verify whether your current financials meet these thresholds:

- Net tangible assets: ₹3 Cr in each of preceding 3 full years

- Distributable profits: Average ₹15 Cr operating profit in any 3 of last 5 years

- Minimum paid-up capital: Post-issue capital above ₹10 Cr; market cap at least ₹25 Cr

- Promoter lock-in: 18 months for minimum promoter contribution (20% of post-issue capital); 6 months for excess holding

Note: SEBI reduced promoter lock-in from 3 years to 18 months in January 2022, signaling earlier liquidity but also greater scrutiny of promoter commitment.

Source: SEBI ICDR Regulations.

Legal Clean-Up That Must Happen Before Filing:

Discovering these issues at the DRHP stage causes the most avoidable delays:

- Pending litigation disclosures: Complete litigation tracker with mitigation plans

- Clear promoter shareholding: No disputes or undisclosed arrangements

- No outstanding regulatory actions: Clean compliance record

- Corporate secretarial records: All board resolutions and shareholder approvals documented

- Charges or encumbrances: No unresolved charges on key assets

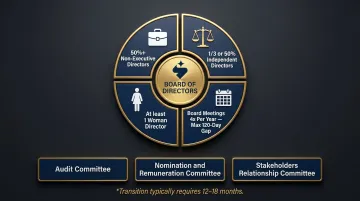

Governance and Management Quality

Minimum Board Structure for Listed Companies:

Public markets require:

- Board with independent directors meeting SEBI LODR Regulation 17 requirements

- Functioning audit committee (Reg 18), nomination and remuneration committee (Reg 19), and stakeholders relationship committee (Reg 20)

- Clear separation between promoter and management roles

Board Composition Requirements:

- At least 50% non-executive directors

- At least one-third independent directors (or 50% if chairperson is executive/promoter-related)

- At least one woman director

- Board meetings at least 4 times per year with maximum 120-day gap

Source: SEBI LODR Regulation 17.

Why Single-Promoter Dependency Gets Flagged:

Investors look for a second layer of leadership that can sustain performance post-listing. Companies where all key relationships and decisions run through a single promoter are flagged as significant governance risks during investor due diligence.

For first-generation Indian founder-promoter companies, this means transitioning governance from informal to institutional—a process that typically requires 12-18 months to establish credibility.

Equity Story and Market Positioning

What Institutional Investors Need to Underwrite Your Story:

This is distinct from your pitch deck or marketing narrative. Institutional investors (QIBs, NIIs) need:

- Clearly defined and defensible total addressable market (TAM)

- Differentiated competitive positioning with pricing power

- Demonstrated unit economics or credible path to them

- Narrative that QIBs can underwrite with conviction

Common Equity Story Weaknesses Underwriters Flag:

- Over-reliance on one or two large customers (16% of SEBI observations relate to customer/supplier concentration)

- Commoditized business models without pricing power

- Operating in a sector with no comparable listed peer for valuation anchoring

- Inability to articulate use of proceeds in a way that links to growth

These weaknesses become harder to paper over once SEBI's disclosure requirements come into play. SEBI requires disclosure of Price-to-Earnings (P/E) Ratio, Return on Net Worth (RoNW), and Net Asset Value (NAV) with comparison to listed industry peers of comparable size. For companies without listed peers, SEBI now mandates standardized Key Performance Indicators (KPIs) with third-party certification.

Source: SEBI Consultation Paper on Basis of Issue Price.

Operational and Documentation Readiness

Operational Readiness:

This means your internal systems can generate accurate, timely data at the pace public markets demand:

- Monthly MIS with segment-level detail

- Structured board reporting

- Documented policies covering governance, risk, and compliance

- Clean data room with evidence trails

Most Indian SME and mid-market companies run on informal communication and undocumented decisions — and that structure collapses the moment an underwriter or SEBI reviewer asks for an evidence trail.

Documentation Readiness:

Most Indian companies fail here first. These are not just legal liabilities—they signal to investors that the business cannot be run transparently at scale:

- Lost agreements or contracts with no backup

- Verbal understandings with vendors or customers

- Undocumented inter-company loans

- Missing historical board resolutions

- No evidence-linked disclosure schedules

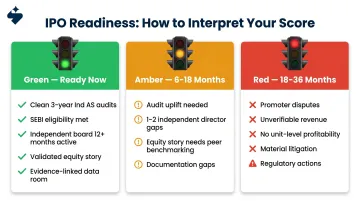

How to Interpret Your Readiness Assessment: Green, Amber, or Red?

After assessing all five dimensions, classify each as Green (ready and verifiable), Amber (gaps identified but addressable within a defined timeline), or Red (fundamental issues requiring structural change).

Most companies will have a mix of Green and Amber signals, not a clean sweep.

Green Signal: Ready to Begin Formal Banker Engagement

A Green readiness profile across each dimension looks like this:

- Financial: Three years of clean audited Ind AS financials with no qualifications

- Legal: SEBI eligibility clearly met; no pending litigation or regulatory actions

- Governance: Board with independent directors in place for 12+ months; audit committee functioning

- Equity story: Validated by sectoral comparables; clear TAM and unit economics

- Operational: Functioning data room with evidence-linked documentation

Green across all five means you can begin formal banker engagement immediately.

Amber Signal: Structured Preparation Required (6-18 Months)

Amber is the most common outcome — gaps exist but are not disqualifying.

Examples of Amber signals:

- Financials need one-year audit uplift to Ind AS standards

- Governance gap requires one or two independent director appointments and committee constitution

- Equity story needs sharper articulation and peer benchmarking

- Documentation gaps in contract archives or board resolutions

Amber typically means 6 to 18 months of structured preparation.

Red Signal: Fundamental Change Required (18-36 Months)

Red signals require fundamental change before IPO is viable:

- Unresolved promoter disputes or unclear shareholding

- Revenue that cannot be independently verified

- Business model that has not demonstrated unit-level profitability

- Material litigation with uncertain outcomes

- Regulatory actions or show-cause notices

Proceeding with Red-signal issues doesn't just delay listing — it invites SEBI scrutiny and can result in failed listings, forced refunds, and reputational damage that follows a company for years. Enforcement cases like Trafiksol ITS Technologies show what happens when material misstatements reach the DRHP stage.

What Early Detection Actually Prevents

S45 runs an AI-led readiness scan before signing any mandate. Catching issues at this stage — before the DRHP is drafted — prevents the three most expensive problems in IPO execution:

- SEBI observation letters that trigger disclosure rewrites and timeline extensions

- Restatements of audited financials that require fresh sign-offs and restart DRHP review clocks

- Investor questions during bookbuilding that expose gaps in the equity story at the worst possible moment

Founders who address Amber signals in pre-filing typically move from mandate to listing 30-60 days faster than those who discover them mid-process.

How Long Does It Take to Get IPO Ready in India?

Timeline Framework

- Green/Amber profile: 12-18 months from first readiness review to DRHP filing

- Significant Amber gaps: 18-24 months

- Red signals: 24-36 months minimum (should not begin formal process until resolved)

Source: EY estimates companies start IPO preparation 12-18 months in advance.

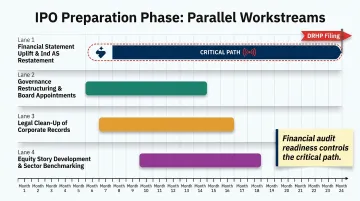

What Happens During the Preparation Phase

These workstreams run in parallel:

- Financial statement uplift and audit preparation — typically the longest lead-time item, involving Ind AS restatement, resolving prior qualifications, and cleaning related-party disclosures

- Governance restructuring and board appointments — independent directors, audit committee composition, and board-level policies per SEBI LODR

- Legal clean-up of corporate records — resolving cap table issues, pending litigation disclosures, and shareholder agreement conflicts

- Equity story development with sector benchmarking — positioning the business against listed peers before bankers engage investors

Financial audit readiness almost always controls the critical path. Everything else can be parallelised around it.

The Compounding Cost of Starting Late

SEBI's regulatory target for issuing observation letters is 30 days. In practice, average DRHP processing time was 68 days in 2024 and has stretched to 147 days in 2026 YTD, reflecting tighter scrutiny on disclosures.

Companies that file before they are ready pay for it directly:

- DRHP delays and multiple clarification rounds with SEBI

- Material revisions forced by SEBI observations — sometimes requiring fresh audits

- Forced valuation reductions due to investor skepticism

- Listing windows missed entirely as market conditions shift

The founders who clear SEBI fastest are not the ones who moved quickest to file — they are the ones who resolved every major gap before the banker made the first call.

Common Mistakes Founders Make When Self-Assessing IPO Readiness

Conflating Revenue Growth with IPO Readiness

Founders who have built a business to ₹100-500 Cr in revenue often assume that scale alone qualifies them. In reality, investors scrutinize revenue quality, margin sustainability, and governance discipline, not just the top line.

Of the 97 draft offer documents processed by SEBI in FY 2023-24, 10 were returned and 4 were withdrawn, demonstrating that many companies overestimate their readiness.

Underestimating the Governance Gap

Many founders believe adding two independent directors in the last quarter before filing satisfies governance requirements. In practice, institutional investors look for independent directors who have actually been involved in decision-making for 12-18 months, not recently appointed figureheads.

Board committees must also be fully constituted before listing, per SEBI LODR Regulations 18-20:

- Audit committee: Two-thirds independent, all financially literate, at least one with accounting expertise

- Nomination and remuneration committee: All non-executive, at least 50% independent

- Stakeholders relationship committee: At least one independent director

The Documentation Trap

Most founders assume a smoothly running business means the paperwork is in order. IPO-level documentation standards are far stricter than what most growth-stage companies maintain.

That gap surfaces fast. A banker or auditor asking for evidence-linked disclosures will expose it immediately. SEBI issues approximately 100 observations per DRHP, and the most common triggers are:

- 46% relate to risk factor disclosures

- 16% relate to customer or supplier concentration

Both are areas where documentation quality — not business performance — determines whether a filing clears review.

Frequently Asked Questions

What does it mean to be IPO ready?

Being IPO ready means your company can meet SEBI eligibility requirements, sustain institutional investor scrutiny across financial, governance, and operational dimensions, and operate transparently at the standard public markets demand—not just on listing day, but afterward.

How do you get IPO ready?

Conduct a structured readiness assessment across the five dimensions (financial, legal, governance, equity story, operational). Address identified gaps in 12-24 months through financial restatements, governance restructuring, and legal clean-up. Engaging a lead manager early ensures the formal DRHP filing and regulatory process moves without last-minute disruption.

What does IPO mean?

IPO stands for Initial Public Offering—the first time a company sells its shares to the general public through a stock exchange such as NSE or BSE in India. This creates a primary capital raise for the company and an exit or liquidity window for existing shareholders, typically through a mix of fresh issue and OFS.

What is the difference between an SME IPO and a Main Board IPO in terms of readiness?

SME IPOs (BSE SME or NSE Emerge) have lower eligibility thresholds and a simpler regulatory process than Main Board listings, but both require clean financials, governance compliance, and a credible equity story. The readiness dimensions are the same, but the depth and scale of preparation required differs.

How long does it take to prepare for an IPO in India?

Most companies need 12-24 months of structured preparation before filing a DRHP, depending on gaps identified in their readiness assessment. Companies with clean financials and governance already in place can move faster, while those with significant gaps may need 24-36 months.

What are SEBI's eligibility criteria for an IPO in India?

For Main Board IPOs, SEBI ICDR Regulations set the following minimum thresholds:

- Net tangible assets of ₹3 Cr in each of the preceding 3 years

- Average pre-tax operating profit of ₹15 Cr during any 3 of the last 5 years

- Net worth of ₹1 Cr in each of the preceding 3 years

Verify the latest thresholds on SEBI's official website.