Introduction

Most fast-growing startups in India treat IPO planning as a last-minute sprint — assembling disclosures, chasing documentation, and debating pricing only after deciding to list. The outcome is predictable: DRHPs rewritten five times, communications lost between advisors, and pricing mechanisms with no defensible logic.

Even fundamentally strong companies end up with derailed timelines, SEBI observation letters packed with avoidable queries, and listing outcomes well below their potential.

An IPO is not a funding event bolted onto a private company. It is a structural transformation that reshapes governance, reporting, disclosure, and accountability. The difference between a smooth listing and a derailed one is decided 18–24 months before the DRHP is filed. Companies that wait until they are "ready to file" typically discover gaps in board independence, messy cap tables, inconsistent revenue recognition, and related-party transactions that each require months to remediate.

This guide covers five critical areas every founder should address before filing:

- Assessing readiness across financial, operational, governance, and market dimensions

- Building the financial foundation that withstands SEBI and institutional scrutiny

- Restructuring corporate governance to meet LODR requirements

- Crafting an investor story with a disciplined pricing strategy

- Executing a phased planning timeline specific to India's public markets

Key Takeaways

- Pre-IPO planning in India should begin 18–24 months before listing, not at DRHP filing

- Arrive with three years of Ind AS audited financials, a clean cap table, defined KPIs, and fast close cycles — before anyone asks

- Restructure your board and committees before SEBI scrutiny begins — not in the final quarter before filing

- Map institutional demand before engaging intermediaries so your price band is anchored, not guessed

- SME and Main Board IPOs differ on eligibility thresholds, compliance depth, and realistic timelines — know which path fits before you start

What Pre-IPO Planning Actually Means for Fast-Growing Startups

Pre-IPO planning is the process of transforming a privately-run company into one that can operate under public scrutiny, quarterly reporting standards, and investor accountability. It spans six domains — financial hygiene, governance restructuring, systems scalability, regulatory compliance, investor narrative, and demand strategy — each of which must be addressed in sequence, not compressed into the 90 days before filing.

In practice, that scope includes:

- Restating three years of financials under Ind AS

- Cleaning up convertible instruments and ESOP pools

- Restructuring the board to include independent directors and audit committees

- Implementing ERP systems that support 45-day quarterly reporting cycles

- Defining 5–8 investor-grade KPIs specific to your sector

- Building a bottoms-up use-of-proceeds model that can withstand SEBI scrutiny

It also requires understanding where demand will originate — across QIBs, NIIs, and retail segments — before you begin syndicating the deal.

India-Specific Context: SME vs Main Board

India offers two listing routes with distinct eligibility criteria and regulatory obligations:

Main Board (BSE/NSE) requires minimum post-issue paid-up capital of ₹10 crore. Two routes apply:

- Regulation 6 (Profitability): Net tangible assets of at least ₹3 crore in each of the last three years; average pre-tax operating profit of ₹15 crore in any three of the last five years

- Regulation 7 (QIB): Profitability requirements waived, but at least 75% of the net issue must be allocated to QIBs, with a minimum subscription threshold that triggers full refund if not met

SME IPO (BSE SME/NSE Emerge) is designed for companies with maximum post-issue paid-up capital of ₹25 crore. Eligibility requires:

- Positive net worth in two of the last three years

- An operating track record of at least three years

- Positive operating profit in two of three years

SME listings are exempt from SEBI LODR Regulations 17-27 and file only half-yearly results instead of quarterly. The trade-off: mandatory market makers for three years and minimum lot sizes of ₹1,00,000 that limit retail liquidity.

Regardless of route, SEBI's Disclosure and Investor Protection Guidelines govern both, and DRHP quality directly determines subscription outcomes. Each DRHP receives approximately 100 comments from SEBI, with 46% of observations targeting the Risk Factors section. Companies that file with incomplete disclosures, vague use-of-proceeds narratives, or unsubstantiated working capital projections face extended review cycles and, in some cases, rejection.

Assessing Your IPO Readiness: The First Step Most Founders Skip

IPO readiness is a multi-dimensional assessment across four areas: financial, operational, governance, and market. Founders who only assess finances miss the gaps that cause SEBI comment rounds and delayed listings.

Financial Readiness

SEBI reviewers and auditors look for three years of restated Ind AS-compliant financials, revenue trajectory clarity, EBITDA or a credible path to it, and a clean statement of cash flows.

Common gaps that surface during DRHP drafting include:

- Inconsistent revenue recognition — particularly deferred revenue or milestone-based billing treatment

- Unreconciled related-party transactions that auditors flag for disclosure

- Incomplete liability profiles — lender concentration or undisclosed covenant breaches

Each of these causes costly rewrites and compresses listing timelines.

Operational Readiness

Public company standards require scalable ERP systems, defined KPI reporting cadence, and financial close timelines that meet post-listing demands. Under SEBI LODR Regulation 33, newly listed Main Board entities must submit their first financial results within 21 days from the listing date, with subsequent quarterly results due within 45 days. An analysis of 64 companies listed on the Main Board in 2021 found that 37.5% failed to disclose financial results for one full quarter post-listing. Companies that simulate this reporting cadence pre-IPO avoid post-listing compliance failures.

Governance Readiness

SEBI mandates specific board and committee structures before listing:

- Independent directors: At least one-third of the board (or half if the chairperson is a promoter)

- Audit committee: Minimum three members — two-thirds independent, all financially literate, at least one accounting expert

- Nomination and remuneration committee: Required and operational before filing

Companies caught restructuring governance mid-review face significant delays. Recruiting independent directors, operationalizing committee procedures, and documenting related-party policies takes three to six months at minimum — time that compounds against your filing window.

Market Readiness

Once governance and financial readiness are in place, market timing becomes the final variable. Assessing sector-level IPO sentiment, comparable company valuations, and QIB appetite prevents founders from filing into unfavorable windows. In October 2025, QIB subscriptions averaged 60x, with 13 companies exceeding 100x subscription, signaling robust institutional demand. However, SEBI extended observation letter validity for approximately 40 companies worth $5.4 billion due to geopolitical volatility, demonstrating that external factors can derail even fully prepared candidates.

S45's AI-led readiness platform runs this four-dimensional assessment early, identifying issues in financial reporting, governance structure, and documentation before they reach the DRHP stage. The preliminary scan completes within 48 hours and delivers a banker-grade diagnosis — actionable, prioritized, and sequenced for your filing timeline.

Building the Financial Foundation Investors and Regulators Expect

Three Years of Audited Ind AS Financials

The financial foundation requires three years of audited financials under Ind AS, with restatement if accounting policies changed mid-period. SEBI's ICDR Regulations mandate restated consolidated financial statements for the last three financial years, presented per Schedule III to the Companies Act, 2013. If the latest full financial year in the offer document is older than six months from filing, a stub period is required.

Cap Table Hygiene

Pre-IPO cap tables frequently arrive with unresolved issues that surface at the worst possible moment — during SEBI review. Common problems include:

- Unconverted instruments (convertible notes, SAFEs, warrants)

- Uncleaned ESOP pools with lapsed or undocumented grants

- Related-party loans with ambiguous repayment terms

- Embedded rights from earlier rounds: anti-dilution protections, liquidation preferences, veto rights

A messy cap table in the DRHP triggers investor distrust and SEBI queries about promoter contribution, related-party hygiene, and disclosure adequacy. Resolving these issues requires legal counsel, board resolutions, and shareholder approvals — a process that routinely takes months to complete cleanly.

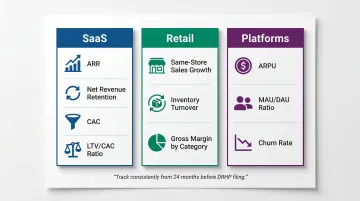

KPI Definition and Disclosure Readiness

Founders must identify 5–8 investor-grade KPIs specific to their sector and track them consistently from at least 24 months before filing. These metrics will appear in the DRHP and face direct scrutiny on the roadshow.

Sector-specific KPIs to establish early:

| Sector | Key Metrics |

|---|---|

| SaaS | ARR, net revenue retention, CAC, LTV/CAC ratio |

| Retail | Same-store sales growth, inventory turnover, gross margin by category |

| Platforms | ARPU, MAU/DAU ratio, churn rate |

Inconsistent definitions or gaps in historical data are among the most common reasons SEBI issues clarification queries. Define each metric precisely, document the methodology, and apply it uniformly across all periods.

Financial Close Velocity

Fast-growing startups operating with informal monthly closes must shift to disciplined reporting. Public companies close books and file quarterly results within 45 days, and annual results within 60 days. Simulating this rhythm pre-IPO — implementing month-end close procedures, reconciling accounts within 10 days, and producing management accounts within 15 days — prepares the finance function for post-listing demands.

Use of Proceeds and Working Capital Narrative

SEBI requires a detailed, justified use-of-proceeds section in the DRHP. Vague or overly optimistic projections attract regulatory queries. 24% of total IPO proceeds in H1 FY2025-26 were designated for working capital, reflecting continued SEBI scrutiny. Founders should build a bottoms-up working capital model that aligns capital deployment with the stated growth strategy, backed by vendor quotes, facility contracts, and phased hiring plans.

Corporate Governance and SEBI Compliance

Board and Committee Restructuring

SEBI's LODR requirements mandate specific board composition at listing: at least one-third independent directors, an audit committee with a minimum of three members (two-thirds independent, all financially literate, with at least one having accounting expertise), and a nomination/remuneration committee with at least three non-executive directors (two-thirds independent).

These structures take longer to build than most founders expect. Identifying qualified independent directors, running background checks, securing board approvals, and onboarding them into governance processes typically takes three to six months — time that cannot be compressed at the last minute.

Key audit committee requirements under LODR:

- Meets at least four times per year, with no more than 120 days between consecutive meetings

- All members must be financially literate — able to read balance sheets, P&L accounts, and cash flow statements

- At least one member must hold accounting or related financial management expertise

Internal Controls and Material Weakness Remediation

SEBI comment letters and underwriter concerns cluster around the same root causes: undocumented processes, manual approval chains, and no functioning internal audit. Identifying and resolving control weaknesses before DRHP drafting is far less costly than addressing them during regulatory review. A basic internal audit framework for pre-IPO companies includes:

- Financial controls: Revenue recognition policies, expense approvals, cash reconciliation, accounts receivable aging

- Operational controls: Inventory management, procurement approvals, vendor due diligence

- Compliance controls: Statutory filings (ROC, GST, TDS), board resolution tracking, related-party transaction registers

- IT controls: Access management, data backup, change control procedures

Secretarial Compliance and Related-Party Hygiene

The Company Secretary ensures compliant board minutes, statutory registers, ROC filings, and related-party transaction policies. Gaps in secretarial compliance—missing board resolutions, incomplete statutory registers, delayed ROC filings—surface during legal due diligence and cause delays. Related-party transaction policies must document approval thresholds, arm's-length pricing methodologies, and disclosure requirements to meet SEBI scrutiny.

Crafting Your Investor Story and Demand Map

Building the Investment Thesis

The investment thesis—why your company deserves a public valuation premium—must be built before roadshow conversations begin. It needs to answer four questions cleanly:

- Market size: A bottom-up TAM with clear sizing methodology, not a top-down industry estimate

- Growth credibility: Historical performance plus forward contracts or pipeline data supporting your rate

- Competitive moat: Technology IP, regulatory licenses, network effects, or switching costs—one defensible angle argued deeply

- Capital deployment: A specific use-of-proceeds story that ties each rupee raised to a revenue milestone

Pricing Discipline and Valuation Band Strategy

IPO pricing is one of the highest-stakes decisions in the process. SEBI mandates that the cap price cannot exceed 120% of the floor price, creating a maximum 20% spread. Founders who overprice relative to sector benchmarks and comparable company multiples risk poor subscription, weak listing performance, and damaged institutional relationships. Underpricing slightly to generate oversubscription is a deliberate strategy that builds momentum, not leaving money on the table.

Bankers determine the price band through valuation analysis using sector comparables and cash-flow methods, refined through pre-IPO soundings and bookbuilding demand signals.

Demand Mapping Before Engaging Intermediaries

A critical pre-IPO step most founders skip is understanding QIB, NII, and retail demand segments before engaging intermediaries. Walking into banker conversations without a demand hypothesis leads to chaotic pricing, last-minute anchor misalignment, and subscription uncertainty.

S45 maps demand before engaging intermediaries, using proprietary analytics to build a structured picture of the offer before pricing conversations begin. The analysis covers:

- State-wise and regional demand heat maps

- Subscription pattern scenarios across QIB, NII, and retail categories

- Anchor investor targeting by archetype: long-only funds, sector specialists, insurance companies, and AIFs

- ESG exclusion filters for sectors with environmental or social governance sensitivities

This structured picture shapes the entire offer design—allocation strategy, price band anchoring, and roadshow sequencing.

Pre-IPO Investor Relations

Pre-IPO investor relations—analyst briefings, sector positioning, and press groundwork—should begin 6–9 months before listing. Companies that arrive at roadshow without prior institutional awareness are starting cold, and institutional investors notice. Early engagement includes teach-ins with sector analysts, pre-soundings with anchor investors to gauge pricing appetite, and media positioning within SEBI's publicity guidelines to build awareness without crossing selective disclosure boundaries.

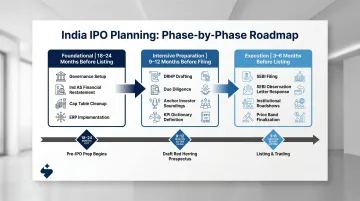

Your Pre-IPO Planning Timeline: A Phase-by-Phase Guide

18–24 Months Before Target Listing: Foundational Phase

This phase sets the structural foundation for everything that follows. The company must begin operating like a public entity internally — governance, financials, and compliance — well before any filing occurs. Key activities:

- Conduct multi-dimensional readiness assessment across financial, operational, governance, and market dimensions

- Appoint independent directors and establish audit committee, nomination/remuneration committee

- Initiate three-year financial restatement under Ind AS

- Begin cap table cleanup: resolve related-party loans, embedded anti-dilution rights, liquidation preferences

- Implement ERP systems to support 45-day quarterly close cycles

- Define 5–8 investor-grade KPIs and begin consistent tracking

9–12 Months Before Filing: Intensive Preparation Phase

DRHP drafting begins with the merchant banker. Financial restatements are finalized, legal and financial due diligence is conducted, and anchor investors are identified.

S45 targets DRHP readiness in 30–45 days when the groundwork is complete: the issuer provides a clean data room with audited financials, complete documentation, and resolved governance gaps. During this phase:

- Draft DRHP sections: Business, Risk Factors, Management's Discussion and Analysis, Corporate Governance, Financial Information

- Complete legal due diligence: title opinions, material contracts, IP verification, compliance certifications, litigation tracker

- Finalize promoter contribution calculations and sourcing plans per ICDR compliance

- Conduct pre-IPO soundings with anchor investors and institutional investors

- Build KPI dictionary linking evidence to disclosure schedules

- Establish secretarial compliance framework: board minutes, statutory registers, ROC filings

3–6 Months Before Listing: Execution Phase

With preparation complete, the filing window opens. SEBI filing occurs, observation letters are addressed, the price band is finalized based on bookbuilding demand signals, roadshows are executed, and the anchor book is locked. Companies that arrive at this stage with gaps in prior phases face compressed timelines, pricing errors, and subscription underperformance.

SEBI typically issues its observation letter within 30 days of filing, though review cycles can extend to 1–3 months depending on disclosure quality. After receiving the observation letter, the company has 12 months to open the issue. The full cycle from filing to listing is typically 3–6 months when documentation is clean.

Key activities:

- Address SEBI observations: update risk factors, resolve related-party transaction queries, justify use-of-proceeds allocations

- Finalize price band through bookbuilding and demand assessment

- Execute roadshows within SEBI publicity guidelines: management training, investor grid creation, city-wise meeting schedules

- Allocate anchor book before issue opens: long-only funds, sector specialists, insurance, AIFs

- Coordinate with registrar, depository, and stock exchanges for listing agreement and post-listing compliance

Frequently Asked Questions

How early should a startup begin pre-IPO planning in India?

18–24 months is the recommended minimum lead time. Governance restructuring, audit preparation, and cap table cleanup require the most runway. Companies beginning later than 12 months before their target listing date often face material weaknesses, governance gaps, and regulatory delays that compress timelines and reduce execution quality.

What is the difference between an SME IPO and a Main Board IPO in India?

The SME route (BSE SME/NSE Emerge) suits smaller companies — post-issue paid-up capital up to ₹25 crore, lighter compliance (half-yearly results, LODR exemptions), and mandatory market makers. Main Board requires higher eligibility thresholds (minimum ₹10 crore post-issue capital, profitability or QIB route), quarterly reporting, and stricter governance — but opens access to a broader institutional investor base.

What financial metrics do SEBI and investors typically scrutinize before an IPO?

SEBI requires three years of audited Ind AS financials and scrutinizes revenue recognition consistency, EBITDA margins (or a credible path to profitability), and working capital health. Investors add sector-specific KPIs — ARR for SaaS, ARPU for platforms — while SEBI focuses closely on use-of-proceeds justification and related-party disclosures.

How do I know if my startup is ready for an IPO?

Readiness covers four areas: financial (clean audited financials, fast close cycles), operational (scalable ERP, KPI tracking), governance (independent directors, audit committee, internal controls), and market (sector sentiment, institutional demand). Most founders who think they're ready still have governance or documentation gaps — a structured assessment catches these before DRHP drafting begins.

What are the most common mistakes founders make in pre-IPO planning?

The most common mistakes: starting fewer than 12 months before target listing, delaying board restructuring until SEBI review, filing with unresolved convertibles or related-party loans on the cap table, setting a price band disconnected from sector comparables, and arriving at the roadshow without prior institutional awareness. Each of these is a process failure — and all are avoidable with adequate runway.

How long does the IPO process take in India from DRHP filing to listing?

SEBI typically issues its observation letter within 30 days of filing, though review cycles can extend to 1–3 months depending on disclosure quality. After the observation letter, the company has 12 months to open the issue. The full cycle from DRHP filing to listing runs 3–6 months when documentation is clean.