Introduction

For founders and promoters of Indian companies considering an IPO—whether Main Board or SME—restructuring isn't an afterthought. It's a prerequisite in the SEBI-regulated listing environment. Pre-IPO restructuring is the process of reorganising a company's corporate, financial, and governance structure before filing for public listing.

The term is widely used but rarely explained at the operational level. Most companies discover what it actually involves only after engaging a merchant banker or receiving SEBI observations. By then, compressed timelines and correction costs have already begun to mount.

This article covers the specific steps involved: corporate simplification, shareholding cleanup, financial restatements, governance upgrades, and the SEBI eligibility conditions that determine whether a company is ready to file.

Key Takeaways

- Pre-IPO restructuring is the set of legal, financial, and governance steps required before filing a DRHP

- Begin 18 to 36 months before your intended listing date—not six months before filing

- Key areas — corporate structure, cap table, financials, governance, and debt — must each meet SEBI ICDR Regulations and exchange requirements before filing

- Skipping or rushing this phase is a leading cause of delayed or rejected filings in India

- Each phase — audit, DRHP drafting, and bookbuilding — builds on the last; gaps at any stage surface at the worst possible time

What Is Pre-IPO Restructuring?

Pre-IPO restructuring is the deliberate reorganisation of a company's core structure to meet public market standards before a listing application is submitted. It typically covers four areas:

- Shareholding pattern — clearing promoter holdings, resolving related-party stakes, and ensuring clean title

- Corporate entities — simplifying group structures and eliminating dormant or non-compliant subsidiaries

- Financial statements — restating accounts, aligning accounting policies, and preparing audited financials fit for DRHP disclosure

- Internal governance — establishing independent boards, audit committees, and functional compliance frameworks

The end result is a company that is clean, independently governed, financially transparent, and compliant with SEBI ICDR Regulations and relevant exchange listing rules.

Critically, this process differs from post-IPO compliance or general corporate restructuring. It is specifically triggered by listing intent and governed by SEBI's disclosure and eligibility norms, not internal management preferences alone.

Why Pre-IPO Restructuring Matters Before You File

SEBI and stock exchanges conduct rigorous scrutiny of the DRHP. Structural anomalies—undisclosed related-party transactions, messy shareholding patterns, or governance gaps—trigger observations that delay or derail filings.

In FY 2023-24, SEBI received 123 DRHPs for Main Board IPOs, issued final observations on 81, returned 10 for non-compliance, and 11 were withdrawn by issuers. Roughly 17% of filings never reached listing.

Since 2019, 94 IPOs have let their SEBI approvals lapse, representing ₹1.35 lakh crore in intended capital raises—a pattern that points to structural readiness failures, not market timing.

What goes wrong without restructuring:

- Inconsistent financials that don't reconcile with GST filings or bank statements

- Opaque promoter relationships and undisclosed RPTs

- Unresolved litigation and unexplained audit qualifications

These issues regularly cause Indian companies to withdraw DRHPs or face repeated SEBI queries that compress timelines and erode investor confidence.

The regulatory consequences don't stop there. Structural gaps affect how investors price the deal too.

Restructuring is valuation-critical

Investors and QIBs discount companies with complex, unexplained structures. A clean, audit-ready business commands better pricing and stronger institutional demand.

In FY24, average QIB oversubscription reached 90x, and 100.89x from April-October 2024. But when market sentiment softens—as it did in November 2024, when QIB subscription dropped 77% to 22.76x—governance clarity and structural readiness become the differentiators.

S45's AI-led readiness assessment surfaces these issues before DRHP drafting begins — so founders aren't caught off guard during bookbuilding.

The Core Steps of Pre-IPO Restructuring

Pre-IPO restructuring isn't a single event. It's a sequenced set of actions typically executed across 18 to 36 months, each dependent on the previous step being resolved cleanly. The goal is to move from an operationally run private company to a governance-ready public entity.

Step 1: Corporate Structure Audit and Simplification

Map all legal entities—subsidiaries, holding companies, dormant shells, and SPVs—and eliminate or merge those without clear operational or tax rationale. SEBI expects a consolidated, explainable group structure. Unexplained entities generate observations.

Specific risks to address:

- Intercompany loans between group entities

- Related-party transactions lacking arm's-length documentation

- Undisclosed cross-holdings

- Circular transactions through shell companies

SEBI ICDR Schedule VI requires specific disclosures for the top 5 listed and unlisted group companies, and all related-party transactions per Ind AS 24.

Step 2: Cap Table Cleanup and Shareholding Rationalisation

Every equity transaction since incorporation must be documented—angel rounds, convertible notes, informal equity promises—because SEBI requires full disclosure of shareholders above a specified threshold.

Current lock-in requirements (post-2021 amendment):

| Category | Lock-In Period | Exception |

|---|---|---|

| Minimum Promoter Contribution (20% post-issue) | 18 months | Reverts to 3 years if majority of proceeds used for capital expenditure |

| Balance Promoter Holding (excess over 20%) | 6 months | N/A |

| Pre-IPO investors (non-promoter) | 6 months | Exemptions for eligible employee holdings and certain funds |

Source: SEBI ICDR Third Amendment 2021

Promoter-specific requirements:

- Pledged shares must be disclosed and addressed; SEBI's 2026 amendment introduced a "non-transferable marking" mechanism for pledged pre-issue shares

- Special shareholder rights (tag-along, anti-dilution) must be waived before filing

- All shareholders holding more than 1% of pre-issue capital must be individually named in the DRHP

Convertible instruments: Under Regulation 5(2), no outstanding convertible securities are permitted at IPO, except outstanding ESOPs and fully paid-up convertibles required to convert by RHP filing date.

Step 3: Financial Statement Preparation and Audit Readiness

SEBI requires restated financial statements for the previous three fiscal years (Main Board) prepared under Ind AS and certified by the statutory auditor. For SME listings, requirements differ but financial quality remains a primary diligence point.

Red flags that create problems:

- Revenue not reconciling with GST filings or bank statements

- Unexplained debtor or inventory jumps

- Unresolved audit qualifications

- Large related-party revenue without arm's-length documentation

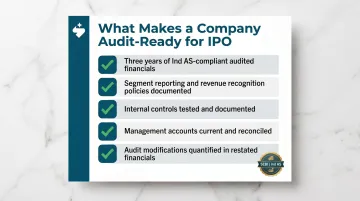

What constitutes "audit-ready":

- Three years of audited financials compliant with Ind AS

- Segment reporting, revenue recognition policies documented

- Internal controls tested and documented

- Management accounts current and reconciled

- Any audit modifications quantified and adjusted in restated financials

Source: BDO India - The Standard Stance

Step 4: Corporate Governance and Board Composition

A listing applicant must have a functional, compliant board with the requisite number of independent directors, functional audit and nomination committees, and an internal audit mechanism.

SEBI LODR Regulation 17 requirements:

- At least one-third independent directors (or one-half if chairperson is promoter-related)

- At least 50% non-executive directors

- At least one woman director

- Audit committee: minimum 3 directors, two-thirds independent; chairperson must be independent

Source: SEBI LODR Regulation 17

Governance restructuring also involves separating promoter roles from management roles where required, and ensuring operational independence from controlling shareholders. With governance structure in place, the final structural risk to address before filing is the balance sheet — specifically, debt positions and related-party transactions that SEBI scrutinises closely.

Step 5: Debt Rationalisation and Related-Party Transaction Cleanup

Document all related-party transactions as arm's-length, disclose them transparently, and justify material ones with clear commercial rationale. Excessive or undisclosed RPTs are among the top reasons for SEBI observations.

RPT materiality thresholds under SEBI LODR Regulation 23:

| Entity Type | Material RPT Threshold |

|---|---|

| Main Board listed entity | Rs 1,000 crore or 10% of annual consolidated turnover (whichever is lower) |

| SME Exchange entity (from April 2025) | Rs 50 crore or 10% of annual consolidated turnover (whichever is lower) |

Source: SEBI LODR Regulation 23

Debt restructuring requirements:

- Ensure loan covenants aren't breached by listing structure

- Discharge or replace personal guarantees by promoters

- Document net debt position clearly for DRHP disclosure

- Resolve any unexplained intercompany loans or advances

Key Factors That Affect Pre-IPO Restructuring in India

Regulatory framework

SEBI ICDR Regulations 2018, Companies Act 2013, and exchange-specific listing requirements impose overlapping obligations. Restructuring must satisfy all three simultaneously. Any change in SEBI guidelines during preparation can require re-work.

Timeline and staging

The earlier structural issues are identified, the lower the remediation cost. Entities that begin restructuring 24 to 36 months before filing have time to merge subsidiaries, restate financials, and clean up RPTs organically. Those starting six months out face compressed timelines that raise costs and increase error risk.

Nature of the business and sector

Capital-intensive sectors (manufacturing, infrastructure) tend to have more complex debt and related-party structures. Technology and services companies often have cap table and ESOP complexity. Restructuring scope and sequencing differ significantly depending on the industry.

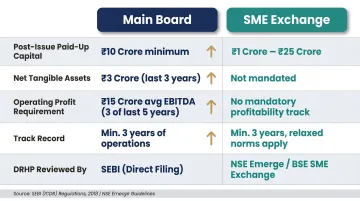

Main Board vs. SME listing

Main Board listings require Ind AS financials, a longer track record, and more extensive governance standards. SME listings carry lighter requirements, though SEBI still scrutinises structure and disclosure quality closely.

Eligibility comparison:

| Criterion | Main Board | SME |

|---|---|---|

| Post-issue paid-up capital | ≥ Rs 10 crore | Up to Rs 25 crore |

| Net tangible assets | ≥ Rs 3 crore (each of 3 years) | ≥ Rs 3 crore (last year) |

| Operating profit | Avg ≥ Rs 15 crore (3 years) | ≥ Rs 1 crore EBITDA (2 of 3 years) |

| Track record | 3 years | 3 years |

| DRHP reviewed by | SEBI | Stock Exchange |

Sources: SEBI ICDR Regulations 2018, NSE Emerge

SME IPO activity has surged: 243 SME IPOs launched in 2024, up 36% from 178 in 2023, with total capital raised across all platforms reaching Rs 1,71,051 crore.

Promoter profile and group complexity

Regardless of whether a company targets Main Board or SME, promoter history is reviewed with equal rigour. Promoters with prior regulatory actions, litigation, or directorial disqualifications require specific disclosure and, in some cases, resolution before SEBI will clear a DRHP. The larger and older the promoter group, the more extensive this diligence.

Common Misconceptions and Mistakes in Pre-IPO Restructuring

Most pre-IPO delays trace back to the same avoidable errors. These are the misconceptions and mistakes that surface most often — and cost the most time to fix.

"Restructuring can start once we decide to file"

Restated financials, merged subsidiaries, and discharged pledges take 12 to 24 months to resolve legally and reflect in audited accounts. Starting late is the single most common reason for delayed IPOs.

The Cap Table Is an Administrative Afterthought

Any ambiguity in ownership, unresolved convertible instruments, or undocumented equity promises create legal risks that can stall a listing for months. SEBI's disclosure requirements leave no room for informal arrangements.

Strong Financials Offset Governance Gaps

SEBI evaluates financials and governance independently. A company can have excellent EBITDA margins and still receive observations because its board lacks independent directors or its RPTs aren't properly documented.

An ESOP Scheme Equals ESOP Readiness

Schemes built without accounting for vesting timelines, exercise pricing, dilution impact on post-IPO capital structure, and tax events at listing often need to be rebuilt before filing.

Key compliance points before listing:

- Perquisite taxation: Taxed under Section 17(2) of the Income Tax Act at exercise — not at grant or vesting. Value = FMV minus exercise price.

- Post-listing LTCG: Taxed at 12.5% for holdings exceeding 12 months on listed shares.

- Regulation 5(2): Prohibits outstanding convertible instruments at IPO except ESOPs — schemes must be structured to comply before filing.

Conclusion

Pre-IPO restructuring is a sequenced, multi-month process covering structure, cap table, financials, governance, and debt. No element can be skipped without creating downstream risk in the SEBI review or bookbuilding process.

Companies that consistently achieve clean filings, strong institutional demand, and disciplined pricing are those that began restructuring early and treated it as a strategic priority—not a compliance formality.

Poor sequencing has a cost: SEBI observations that extend timelines by months, restatements that erode investor confidence, and pricing decisions made without clean demand data. Working with an advisor who owns the full sequence — from eligibility assessment through bookbuilding — removes those failure points before they surface.

S45 operates on this principle directly: sector bankers working inside a live data room, AI-led readiness scans that flag issues before DRHP drafting begins, and a 30-45 day drafting window once the data room is clean. The mandate covers readiness through post-listing investor relations — no handoffs, no gaps.

Frequently Asked Questions

What is pre-IPO restructuring?

Pre-IPO restructuring is the process of reorganising a company's corporate entities, shareholding pattern, financials, and governance to meet SEBI and exchange requirements before filing a listing application. It's a regulatory prerequisite, not an afterthought.

How long do I have to hold pre-IPO shares?

Under ICDR Regulations, promoters face an 18-month lock-in post-allotment for minimum promoter contribution and 6 months for balance holding. If the majority of IPO proceeds go toward capital expenditure, the minimum promoter contribution lock-in reverts to 3 years.

What happens to pre-IPO shares after IPO?

Pre-IPO shares become part of the listed company's equity post-IPO, subject to applicable lock-in periods. Once lock-in lapses, shareholders can trade freely on the exchange.

How early should a company start pre-IPO restructuring?

Serious preparation should begin 18 to 36 months before the intended listing date, since structural, financial, and governance issues each take different amounts of time to resolve and surface cleanly in audited records. Starting late compresses timelines and drives up remediation costs.

What are SEBI's key requirements for pre-IPO restructuring?

Under SEBI ICDR Regulations 2018, core requirements include:

- Compliant shareholding structure

- Restated Ind AS financials for three years (Main Board)

- Minimum promoter lock-in per ICDR norms

- Related-party transaction disclosure per Ind AS 24

- Independent directors and a functional audit committee

What is the difference between pre-IPO restructuring for SME and Main Board listings?

Main Board listings require more extensive financials (three years restated, Ind AS), stricter governance standards (independent directors, audit committees), and higher minimum issue sizes. SME listings have lighter requirements but SEBI still evaluates structural clarity, disclosure quality, and promoter track record with equal scrutiny.