This guide is written for founders, CFOs, and senior management of companies preparing for listing on India's Main Board or SME platform. It explains what roadshow management actually involves at an operational level — from investor targeting to bookbuilding outcomes — and why treating it as a logistics exercise rather than a demand intelligence process is one of the most expensive mistakes a pre-IPO company can make.

Key Takeaways

- An IPO roadshow is a structured series of investor presentations held between DRHP approval and the subscription window opening

- Core purpose: generate qualified demand, validate the price band, and build the institutional book

- Audiences include QIBs, NIIs/HNIs, and anchor investors — each requiring a distinct message and engagement approach

- A poorly managed roadshow produces weak subscription, mispriced offerings, and post-listing volatility

- Effective roadshow management runs demand intelligence, messaging discipline, and regulatory compliance in parallel — with no room for gaps

What Is IPO Roadshow Management?

IPO roadshow management is the end-to-end process of planning, coordinating, executing, and tracking all investor-facing presentations during the pre-IPO marketing window. It covers investor outreach, presentation preparation, scheduling, meeting logistics, feedback capture, and price band calibration.

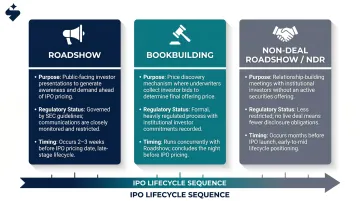

Roadshow vs. Bookbuilding vs. NDR

These three terms are frequently conflated, and the confusion causes real operational problems:

- Roadshow: The marketing and investor engagement phase where demand signals are gathered informally through meetings and Q&A sessions

- Bookbuilding: The formal, SEBI-regulated mechanism for collecting bids within an announced price band — governed by the SEBI ICDR Regulations

- Non-Deal Roadshow (NDR): Investor relations meetings outside an offering context, used for relationship maintenance rather than capital raising

The roadshow informs the price band; bookbuilding formalises it. How well the roadshow is managed — the quality of signals gathered, the investor segments engaged — directly shapes whether the price band holds through subscription.

Where the Roadshow Sits in the Indian IPO Timeline

The roadshow occupies a fixed position: after SEBI issues observations on the DRHP, and before the Red Herring Prospectus (RHP) is filed with the price band. Once this window closes, it cannot be reopened or corrected.

Two regulatory anchors define this window:

- Price band announcement: Must be made at least two working days before the subscription window opens

- Minimum band width: SEBI's January 2022 bookbuilding review introduced a mandatory 5% minimum price band width, preventing ultra-narrow bands that effectively mimic fixed pricing

Why the IPO Roadshow Is Critical to a Successful Listing

QIB Demand Drives Pricing and Listing Outcomes

Investor demand generated during the roadshow directly determines where within the price band an IPO is priced. QIB subscription, in particular, acts as the leading indicator of both listing day performance and long-term institutional support.

India's FY25 IPO cohort illustrates this clearly: according to KPMG's FY2025 IPO report, 80 mainboard IPOs raised ₹1,630 billion, with average QIB subscription of 102x against retail subscription of 35x. The QIB book consistently anchors price discovery — when institutional investors bid with conviction, retail and NII participation follows.

The contrast between Zomato and Paytm makes the mechanism concrete:

| IPO | Issue Price | Listing Day Outcome | Key Driver |

|---|---|---|---|

| Zomato (Jul 2021) | ₹76 | +53% on listing | Heavy institutional demand, favourable pricing |

| Paytm (Nov 2021) | ₹2,150 | -27% on debut | Aggressive pricing, QIB conviction questioned |

| LIC (May 2022) | ₹949 | -8.1% on listing | Macro volatility, FII risk-off environment |

Zomato priced with headroom and attracted strong QIB participation. Paytm priced at the ceiling, tested investor patience on profitability, and paid for it immediately on listing day.

What Goes Wrong Without Disciplined Roadshow Management

Common failure patterns in Indian IPO roadshows:

- Inconsistent messaging across cities, with executives going off-script in Q&A

- Feedback captured as informal verbal summaries rather than structured data

- Pricing decisions made without clear demand curves from QIBs

- Anchor allocation disconnected from broader institutional interest

- No distinction between soft expressions of interest and genuine demand indications

The result is erratic listing performance: an unjustified pop driven by retail froth, or a post-listing sell-off when institutional support proves shallow. Both outcomes trace back to the same root cause — a roadshow that generated noise instead of conviction.

The Regulatory Guardrails

SEBI's framework for pre-issue communications is explicit: all roadshow content must be consistent with disclosures in the DRHP/RHP. SEBI prohibits selective disclosure — and the failure patterns above are precisely what the regulatory structure is designed to prevent.

The November 2022 SEBI amendment introduced Chapter IIA, creating a formal pre-filing mechanism with Testing the Waters (TTW) provisions for QIBs only. TTW allows issuers to gauge institutional appetite on a confidential basis, but with a 7-working-day cooling-off before the public DRHP filing. All materials used in TTW interactions must be strictly limited to information in the Pre-DRHP. Every investor interaction during this phase should be logged to evidence compliance.

How the IPO Roadshow Process Works: Step-by-Step

The roadshow typically runs 2 to 4 weeks, concurrently with RHP preparation. The sequence moves from investor identification through city-by-city presentations to price band finalisation.

Pre-Roadshow Preparation

Effective preparation typically begins 2 to 4 weeks before the first investor meeting:

- Assemble the presentation team: CEO, CFO, and sector bankers from the lead investment bank

- Prepare materials: Pitch deck and supporting financials aligned with DRHP disclosures; any claim not in the DRHP is a regulatory risk

- Build the investor universe: Target QIBs by AUM, sector expertise, typical ticket size, and past participation in comparable IPOs

- Sequence the meeting schedule: Tier-1 investors first — anchor candidates, sector-specialist funds, and long-only institutions

S45's Demand Thesis (a cohort-level investor demand mapping exercise conducted before mandate signing) feeds directly into this preparation. It identifies expected QIB-NII-Retail subscription patterns and produces a city-wise roadshow plan with day-by-day priorities. By the time the first meeting is scheduled, the team is working from demand intelligence, not cold outreach.

Conducting Investor Meetings

Indian IPO roadshows follow a consistent geographic pattern for Main Board issues:

- Mumbai: Primary hub — the largest concentration of domestic mutual funds, insurance companies, and FPIs

- Delhi, Bengaluru, Ahmedabad, Chennai, Hyderabad: Secondary city meetings, sequenced based on investor concentration by sector

- Virtual sessions: FII/FPI engagement and geographically dispersed domestic investors

Each meeting follows a structured format: a 20-30 minute pitch followed by Q&A. Management's ability to answer financial questions under pressure is scrutinised heavily. Institutional investors form lasting impressions in these sessions — impressions that influence not just whether they bid, but at what price sensitivity.

Tracking Investor Feedback and Demand Signals

This is where most roadshows fail operationally. Feedback on valuation comfort, sector risk concerns, and ticket size indications must be captured and shared with the bookrunner in real time — not summarised in email threads two days after the meeting.

S45's platform addresses this directly through two core tools:

- Live Pricing Band dashboard: Shows floor price, cap, and indicated price as bids update in real time across all investor sub-categories

- Demand Map: Real-time subscription multiples by category (QIB, NII/HNI, Retail), with daily bidding reports and bid quality analysis

Pricing decisions are anchored in structured demand data, not banker memory. The 50,000+ mapped investors in S45's distribution network are signal-scored by mandate fit, peer holdings, recent roadshow attendance, win rates, and ticket bands — so targeting stays precise from the first meeting onward.

Post-Roadshow to Subscription Window

Once roadshow meetings conclude, the sequence moves quickly:

- Synthesise demand signals: Management and bankers consolidate feedback into a coherent demand curve

- Finalise the price band — anchored in QIB feedback, not promoter preference

- File the RHP with SEBI and the stock exchange

- Confirm anchor allocation — must be completed one day before the subscription window opens

- Open the subscription window — with the anchor book already set as a demand signal for QIB and retail participants

Anchor allocation is a direct output of roadshow conversations. Anchor investors (long-only funds, sector specialists, insurance companies) are engaged in parallel with the broader roadshow, with separate documentation and SEBI PIT-compliant wall-crossing logs. Their commitment sets the tone for the entire book.

What an Effective IPO Roadshow Presentation Must Cover

The Investment Thesis

The pitch deck must allow sophisticated institutional investors to assess return potential and risk within the first 10 minutes. Overly complex or internally inconsistent narratives rank among the most common reasons QIBs disengage early — before your management team has finished the opening slide.

A strong investment thesis answers three questions without ambiguity: Why this company? Why now? Why at this valuation? Every subsequent slide should reinforce those answers, not introduce new variables that dilute the core argument.

Key elements of a compelling thesis:

- Market opportunity — addressable size (₹ terms), growth rate, and the company's specific entry point

- Competitive moat — what makes the position defensible over a 3-5 year horizon

- Revenue model clarity — how the company earns, retains, and scales revenue

- Promoter skin in the game — post-IPO promoter shareholding and lock-in structure

Institutional fund managers reviewing 15-20 roadshow decks in a single subscription window will not chase a thesis that requires decoding. If the narrative cannot survive a 10-minute read by a senior analyst, it will not survive a 45-minute meeting with a QIB portfolio manager.

Financial Performance and Forward Projections

Numbers anchor conviction. Investors expect three full fiscal years of audited financials — revenue, EBITDA, PAT, and cash flows — presented in a format that is consistent with the DRHP disclosures already filed with SEBI.

Projections, where included, must be grounded in stated assumptions. Overly optimistic forward guidance without operational logic invites hard questions during Q&A and, more damaging, post-listing disappointment that erodes institutional trust.

Present financials alongside operating metrics that explain the numbers:

- Revenue per unit, per outlet, per customer cohort — whichever is sector-relevant

- Gross margin trajectory and what drives compression or expansion

- Working capital cycle and its impact on free cash flow

- Debt structure, debt-service coverage, and net debt-to-EBITDA

For SME IPO companies listing on NSE Emerge or BSE SME, the same discipline applies — the scale differs, but institutional scrutiny from anchor investors and market makers does not.

Use of Proceeds

SEBI's ICDR regulations require a specific use-of-proceeds disclosure in the RHP. The roadshow presentation must reflect those stated objects precisely — not reframe them for investor appeal.

This section matters more than most management teams expect. Investors use it to assess capital discipline and promoter intent. Vague categories like "general corporate purposes" beyond the permitted threshold, or proceeds directed toward promoter exits without operational reinvestment, draw scepticism from domestic mutual funds and FPIs alike.

State clearly:

- The specific capex, working capital, or debt-repayment allocation by rupee amount

- The timeline for deployment against each object

- How deployment connects to the revenue or margin improvement being projected

Management Team and Governance

Institutional investors back people as much as business models. The management slide must go beyond designations — it needs to demonstrate that the leadership team has navigated operating cycles, managed capital, and built repeatable systems.

Board composition is scrutinised equally. Independent director credentials, audit committee composition, and any related-party transaction history are read carefully by compliance teams at domestic mutual funds and FPIs before an allocation is approved.

Risk Factors — Address Them, Don't Bury Them

Sophisticated investors read the risk factors section. Presenting risks in vague, boilerplate language signals that management has not thought through the business carefully — or worse, is deliberately obscuring known challenges.

Effective risk disclosure in a roadshow presentation:

- Names the specific risk (customer concentration, regulatory dependency, promoter litigation)

- States the potential financial impact in quantifiable terms where possible

- Explains the mitigation already in place or planned

A management team that addresses risks directly during the roadshow builds significantly more institutional credibility than one that deflects or minimises.