Introduction

India's IPO market has shifted from a periodic opportunity to a genuine strategic consideration for growth-stage founders. According to KPMG's FY2025 IPO report, Indian companies raised ₹1,630 billion through 80 mainboard IPOs in FY25 — a 163% increase in capital raised compared to FY24. The NSE ranked #1 globally by funds raised in CY2024, ahead of NASDAQ.

A buoyant market doesn't make an IPO the right move for every company.

Going public permanently changes your company's structure, obligations, and rhythm. Founders who file because the market is hot — without addressing governance gaps, compliance readiness, or investor messaging — typically struggle post-listing. Those who prepare deliberately, with a clear capital thesis and clean books, tend to capture the upside.

The decision deserves more than market timing. This guide helps you make it with clear eyes.

Key Takeaways

- Going public unlocks growth capital, ESOP liquidity, brand credibility, and acquisition currency — provided the business is genuinely ready.

- SEBI's LODR regime imposes ongoing compliance obligations — quarterly filings, independent board oversight, and 24-hour material event disclosure.

- India offers two distinct listing paths — Main Board (NSE/BSE) and SME platforms (NSE Emerge/BSE SME) — with meaningfully different eligibility thresholds, costs, and investor profiles.

- Readiness spans more than financials — governance, disclosure infrastructure, and a credible investor narrative matter as much as revenue.

The Real Reasons Companies Go Public

Access to Capital at Scale

The primary draw is straightforward: public markets offer growth capital without the dilution dynamics of a PE round or the repayment pressure of debt. When a company lists on the BSE or NSE, it raises funds from QIBs, NIIs, and retail investors simultaneously — at a scale no private round typically matches.

In FY25, the OFS component alone across mainboard IPOs totalled ₹324 billion, confirming that existing investor liquidity is as significant a driver as fresh capital. Both motivations are legitimate; the key is knowing which is primary for your company.

Brand Credibility and Market Validation

A successful IPO functions as third-party validation. Institutional investors — domestic mutual funds, FPIs, insurance companies — conduct rigorous diligence before allocating. When QIBs subscribed at an average of 102x in FY25 (up from 81x in FY24), that signal carries weight with customers, partners, and future hires.

For B2B companies in particular, a public listing changes procurement conversations. Being listed shifts the perception of counterparty risk in ways that no private funding announcement replicates.

Liquidity for Founders and Early Investors

Going public creates a liquid secondary market for shares. Promoters, angel investors, and PE/VC backers can monetise stakes over time without forcing a full exit or negotiating complex secondary transactions. This staged liquidity is structurally different from a trade sale or secondary buyout, and is often more tax-efficient for promoters and early backers alike.

ESOP Liquidity and Talent Attraction

According to Hissa, the average Indian startup takes 10–12 years to go public. Until then, ESOPs are largely illiquid promises. Once listed, employee shares become freely tradeable — solving a retention problem that affects hundreds of thousands of startup employees across India.

Public companies can offer ESOPs with genuine liquidity, making them structurally more competitive against private-company offers for senior talent. For companies competing for senior operators in a tight talent market, that difference in ESOP value is often what closes the hire.

Acquisition Currency

Beyond the operational advantages, listing also unlocks a strategic tool: the ability to use listed stock as acquisition currency, reducing cash outlays and enabling inorganic growth. This mechanism is well-established in Indian corporate law and has been used across technology, financial services, and consumer sectors. For founders in consolidating industries, this optionality alone can justify the listing.

The Trade-offs You Must Understand Before Filing

The Compliance Burden Is Permanent

Under SEBI's LODR Regulations, listing is not a one-time event — it is the start of an ongoing compliance cadence:

- Quarterly financial results must be filed within 45 days of each quarter end

- Annual results must be filed within 60 days of year end

- Material events must be disclosed within 24 hours of occurrence

- Board composition requires at minimum one-third independent directors; audit committees need at least two-thirds independent directors

Companies often build compliance infrastructure reactively — after listing. That's expensive and disruptive. The smarter approach is to treat compliance readiness as a pre-listing workstream, not a post-listing problem.

What Going Public Actually Costs

Cost structures vary significantly between platforms:

| Cost Component | SME IPO | Main Board IPO |

|---|---|---|

| Merchant Banker Fee | ₹25–30 lakhs | ₹3–5 crore |

| Underwriting Cost | 8–10% of issue size | 2–6% of issue size |

| NSE Annual Listing Fee (up to ₹100 Cr capital) | ₹3,00,000 | ₹3,00,000 |

The asymmetry matters: SME issuers pay proportionally higher underwriting fees despite raising less capital. For an SME IPO raising ₹30–50 crore, total issue costs can consume a meaningful portion of proceeds. This makes cost planning a critical pre-mandate exercise — not an afterthought.

Post-listing, recurring costs include investor relations, quarterly filing support, compliance team headcount, and company secretary fees.

Loss of Founder Control and Operational Flexibility

Once public, major decisions require shareholder approval. Minority shareholders, proxy advisors, and institutional investors will scrutinise capital allocation, related-party transactions, and management compensation. Founders accustomed to moving quickly will find that public-market governance slows certain decisions.

This isn't necessarily a problem — but it is a permanent shift. Founders who haven't thought through how they'll manage board dynamics and quarterly scrutiny are often caught off guard within the first year of listing.

Disclosure Creates Competitive Exposure

Your DRHP — and every subsequent filing — becomes public. Competitors gain visibility into your financials, margin structure, customer concentration, and strategic priorities. For companies in competitive or early-stage sectors, this transparency can be a genuine disadvantage.

SEBI's disclosure requirements under ICDR are comprehensive: revenue by segment, risk factors, related-party transactions, litigation, and material contracts are all public once you file. Build your disclosure strategy deliberately — not as a reactive exercise once SEBI observations start coming in.

Short-Term Market Pressure

Research on Indian stock markets confirms that stock prices react significantly to quarterly earnings surprises — both positive and negative. Missing consensus estimates, even once, can trigger immediate stock price declines.

This creates a structural tension with long-term thinking. Founders who run 3–5 year strategic cycles must learn to communicate those horizons clearly to public investors — without sacrificing quarterly transparency. The management attention shift is real: investor calls, analyst briefings, and earnings prep will compete directly with operational priorities from day one of listing.

Is Your Company Ready to Go Public?

SEBI Eligibility Basics

Main Board — Profitability Route (Regulation 6(1)):

| Criterion | Threshold |

|---|---|

| Net Tangible Assets | Minimum ₹3 crore in each of 3 preceding years |

| Average Pre-Tax Operating Profit | Minimum ₹15 crore (average over 3 years) |

| Net Worth | Minimum ₹1 crore in each of 3 preceding years |

Main Board — QIB Route (Regulation 6(2)): Companies not meeting profitability norms can list if at least 75% of the net offer is allotted to QIBs through book building.

SME Platforms (NSE Emerge / BSE SME): Post-issue paid-up capital capped at ₹25 crore; minimum 3 years operating track record; BSE SME requires minimum ₹3 crore net worth; SEBI's December 2024 reforms now require minimum ₹1 crore operating profit in at least one of three preceding years.

Financial Readiness Beyond Eligibility

Meeting the minimum SEBI bar is necessary but not sufficient. Investors — particularly QIBs — look for:

- Consistent revenue growth across at least 3 years

- Healthy and stable operating margins

- Clean, audited books with no material restatement risk

- Predictable cash flows and working capital patterns

- A credible, specific use-of-proceeds story

A company that clears the eligibility threshold but has inconsistent revenue recognition or unexplained working capital movements will struggle to generate institutional demand — regardless of what the DRHP says.

Governance and Operational Readiness

Public markets require independent directors, properly constituted audit committees, formal board processes, documented internal controls, and PIT (Prohibition of Insider Trading) compliance frameworks. Companies consistently underestimate how much governance restructuring this requires.

Common gaps that surface during pre-IPO readiness work include:

- Audit committee composition not meeting LODR standards

- ESOP dilution not reflected in the cap table

- Undisclosed contingent liabilities

- Inconsistent revenue recognition policies

- Related-party transaction documentation gaps

S45's IPO Readiness Scan covers all of these dimensions — financial track record, board independence, demat readiness, statutory dues, and material litigation — delivering a preliminary assessment within 5 business days of a 30-minute intake. Surfacing these gaps 12–18 months before filing is what makes remediation practical rather than frantic.

Signals That the Timing Is Right

Eligibility and governance tell you whether you can list. These four questions tell you whether you should — right now:

- Does the company have a credible growth story that institutional investors will find compelling?

- Can the management team sustain investor relations obligations — quarterly results, earnings calls, analyst coverage — without disrupting operations?

- Are sector sentiment and market conditions favourable for your industry?

- Is there a clear capital deployment plan that justifies the valuation you're targeting?

A "no" on any of these doesn't disqualify you — it tells you exactly where to focus over the next 12–18 months before you file.

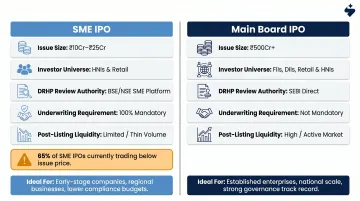

Main Board vs. SME IPO: Choosing the Right Path

Structural Differences

| Dimension | Main Board IPO | SME IPO |

|---|---|---|

| Average Issue Size (FY25) | ~₹800 crore | ~₹36 crore |

| Post-Issue Paid-Up Capital | No upper cap | Maximum ₹25 crore |

| DRHP Review | Directly by SEBI | By stock exchange (NSE/BSE) |

| Underwriting | Not compulsory | Compulsory (100% underwritten) |

| Market Maker | Not required | Compulsory |

| Typical Timeline | 6–12 months | 2–3 months |

Trade-offs of Each Path

SME IPO suits companies that need faster execution and lower absolute costs, but the trade-offs are real:

- Execution in 2–3 months from mandate to listing

- Simpler DRHP review through the exchange rather than SEBI directly

- Accessible eligibility thresholds

- Higher proportional underwriting costs (8–10%) and a smaller investor pool

- Post-listing liquidity is the most critical concern: NISM research shows 65% of SME listings from CY2024 are currently trading below their issue price, and roughly 10–12% of SME-listed companies face trading suspensions for non-compliance

Main Board IPO offers larger raises and a deeper investor universe, with corresponding demands:

- Access to the full institutional universe — mutual funds, FPIs, insurance, pension funds

- Greater post-listing liquidity and stronger brand signal

- Demonstrated profit track record required (or QIB route)

- Longer preparation timelines and higher absolute costs

- More rigorous ongoing disclosure obligations

The platform decision should be driven by your company's financials and capital requirements, not by which process feels simpler. S45 applies the same structured approach — data rooms, evidence-linked DRHP drafting, live demand mapping — to both routes.

A Simple Decision Heuristic

- Revenue below ~₹100 crore, growth-capital need below ₹50 crore, 3+ years of profitability: Start with the SME route, with a clear migration plan to Main Board in 2–3 years.

- Demonstrated institutional-scale appetite, capital requirement above ₹200 crore, profit track record meeting Regulation 6(1): Target Main Board directly.

- Pre-profitability but strong QIB backing: Main Board QIB route, with careful structuring.

Sector dynamics, business model complexity, and advisor quality all influence this decision. The route analysis should happen at the start of readiness work, not after months of preparation.

How Going Public Affects Your Employees

ESOP Liquidity and Employer Brand

Employees with ESOPs gain genuine liquidity once a company lists — the shares become freely tradeable after the lock-in period. This is a concrete financial benefit that private-company ESOPs rarely deliver. A public listing also boosts employer brand: candidates who were hesitant to join a private company often become more receptive once there's a listed equity stake on the table.

For companies that have been building for 5–10 years, the listing moment is also a genuine cultural milestone — one that validates the journey for the team that built it.

Operational Shifts That Hit Finance, Legal, and Leadership

Going public changes the operational rhythm of a company in ways that affect specific functions heavily:

- Finance teams shift to quarterly close cycles with hard 45-day filing deadlines

- Legal and compliance functions take on material event monitoring, insider trading policies, and continuous LODR obligations

- Executives face analyst calls, investor queries, and board reporting cadences that didn't exist pre-listing

- Management bandwidth narrows during the 3–6 months preceding the IPO — this affects product, sales, and operations more than most founders anticipate

Set honest expectations with the team before filing. The compliance overhead post-listing is real, and finance and legal functions in particular need to be fully staffed before listing day.

Frequently Asked Questions

Should I take my company public?

The decision comes down to whether the benefits — capital access, ESOP liquidity, brand credibility — outweigh the costs of continuous SEBI compliance, reduced operational flexibility, and public scrutiny. If your company meets SEBI's financial and governance thresholds and has a clear use-of-proceeds story, the question shifts to timing and readiness, not the merit of listing itself.

How does going public affect employees?

Employees with ESOPs gain real liquidity once shares are freely tradeable post-listing, and a public listing typically strengthens employer brand. The adjustment is that finance, legal, and executive functions face significantly higher workloads during the pre-IPO phase and an ongoing quarterly compliance cadence afterward.

What is the difference between an SME IPO and a Main Board IPO in India?

SME IPOs on NSE Emerge or BSE SME have lower eligibility thresholds, smaller issue sizes (average ~₹36 crore), and a faster process with DRHP review by the exchange rather than SEBI. Main Board IPOs, by contrast, target larger companies seeking institutional-scale capital with full QIB participation, higher disclosure obligations, and longer preparation timelines.

How long does it take to take a company public in India?

Main Board IPOs typically take 6–12 months from engagement to listing, depending on company readiness, SEBI review timelines, and market conditions. SME IPOs can be completed in 2–3 months from mandate to listing, with DRHP drafting taking 30–45 days once a clean data room is in place.

What are the basic SEBI eligibility requirements to go public?

Under the profitability route, companies need minimum ₹3 crore net tangible assets and ₹15 crore average pre-tax profit across three years; the QIB route allows pre-profitability companies to list if at least 75% of the issue is allotted to QIBs. SME platforms have separate, more accessible thresholds. Verify current norms with a SEBI-registered merchant banker before mapping your timeline.

Is it better to stay private or go public?

Private companies retain operational flexibility and confidentiality; public companies gain capital access and credibility at the cost of compliance overhead and founder control. There is no universal answer — the right choice depends on the company's growth stage, capital requirements, governance maturity, and the founder's long-term objectives.