According to PRIME Database, 37 of 102 Main Board IPOs that listed in 2025 were trading below issue price by year-end — a reminder that oversubscription doesn't guarantee outcomes, and that pricing discipline and disclosure quality matter from day one.

This guide covers a structured, phase-by-phase checklist for Indian CFOs targeting Main Board or SME listings on BSE or NSE — from financial readiness and SEBI compliance to DRHP preparation, team assembly, investor strategy, and post-listing obligations.

Key Takeaways

- IPO preparation in India requires 12–24 months of lead time before listing

- The CFO owns financial reporting upgrades, SEBI compliance, DRHP drafting, and investor communications

- Accounting issues — audit gaps, revenue recognition, internal controls — are the most common cause of IPO delays

- Assembling the right external team early — BRLM, legal counsel, registrar, auditor — determines how cleanly the process runs

- Roadshow and bookbuilding preparation must begin well before SEBI approval — pricing and subscription outcomes depend on it

Is Your Company Ready to IPO? The Pre-IPO Readiness Test

Before committing to a timeline, the CFO must conduct an honest internal assessment across three dimensions:

- Audited financials, clean books, and consistent quarterly closes (financial readiness)

- Scalable systems, documented internal controls, and governance structures (operational readiness)

- Investor-grade equity story, defensible valuation, and comparable listed peers (market readiness)

Skipping this step leads to avoidable surprises mid-process: the kind that require expensive restatements or force a delay past your target listing window.

SEBI Eligibility Thresholds You Must Verify First

For Main Board (Profitability Route — Regulation 6(1)), CFOs must simultaneously satisfy all three thresholds:

| Criterion | Threshold | Period |

|---|---|---|

| Net Tangible Assets | ₹3 crore minimum | Each of 3 preceding years |

| Average Pre-tax Operating Profit | ₹15 crore average | 3 of preceding 5 years |

| Net Worth | ₹1 crore minimum | Each of 3 preceding years |

One overlooked disqualifier: if more than 50% of net tangible assets are held in monetary assets (cash/liquid investments), the company may not qualify under the Profitability Route unless structured as a pure OFS.

Companies without a profit track record can use the QIB Route (Regulation 6(2)), but at least 75% of the net offer must be allotted to Qualified Institutional Buyers. If that threshold isn't met during subscription, the entire issue is refunded.

For SME IPOs (BSE SME / NSE Emerge), post-issue paid-up capital must fall between ₹3 crore and ₹25 crore. The 2025 amendments introduced tighter norms: OFS by promoters capped at 50% of pre-IPO holdings, minimum allottees raised from 50 to 200, and General Corporate Purpose allocations limited to 15% of fresh issue proceeds or ₹10 crore (whichever is lower).

What a Readiness Assessment Should Surface

S45's AI-led readiness scan evaluates financial track, free float, board independence, demat readiness (NSDL/CDSL), statutory dues, and material litigation against SEBI ICDR criteria. The most common gaps it surfaces:

- ESOP dilution not reflected in the cap table

- Audit committee composition issues

- Undisclosed contingent liabilities

- Inconsistent revenue recognition

- Unexplained working capital movements

The output is a readiness score with red/amber/green flags, a route recommendation, an indicative raise range, and a fix-list across governance, disclosure, and controls. CFOs get a clear-eyed view of timeline and risk before intermediaries are engaged.

The CFO's Financial and Accounting Preparation Checklist

Clean, audited financials are the foundation of every IPO. SEBI requires audited financial statements for the last three financial years (or from incorporation, if younger), restated under Ind AS. Quarterly financials must be consistently closed — irregular books require costly "quarterisation" work that extends timelines.

Upgrading Accounting Systems and Internal Controls

ERP and reporting systems must support the full disclosure requirements of a listed company, including:

- Segment reporting under Ind AS 108

- Related party disclosures under the Companies Act 2013

- Revenue recognition policies under Ind AS 115 (critical for SaaS, construction, and milestone-based businesses)

- Share-based payment disclosures under Ind AS 102

The CFO should assess whether existing systems can produce investor-grade financials without manual overrides — because manual workarounds create inconsistencies that attract SEBI queries.

On internal controls: India's equivalent of SOX sits in Section 143(3)(i) of the Companies Act 2013, which requires the statutory auditor to report on the adequacy and operating effectiveness of Internal Financial Controls (IFC). The Audit Committee, under Section 177, must evaluate IFC and risk management systems.

Treat this as a 12–18 month workstream. Deficiencies flagged in the auditor's IFC report can trigger SEBI observations during DRHP review — and remediating them under scrutiny is far more disruptive than catching them early.

Identifying and Resolving Complex Accounting Issues

The accounting areas that most frequently attract SEBI and investor scrutiny in Indian IPOs:

- Revenue recognition — especially multi-element, milestone-based, or subscription contracts

- Related party transactions above SEBI's disclosure threshold

- Cheap stock from pre-IPO equity grants not reflected in the cap table

- Acquisition accounting — goodwill treatment and purchase price allocation for deals in the last three years

- Non-GAAP metrics — consistency and reconciliation of KPIs presented in the DRHP

A study reported by Moneycontrol found that SEBI issues approximately 100 comments per DRHP review, with nearly half focused on risk factors — specifically targeting vague, unquantified, or promotional language. Granular, evidence-backed disclosure from the outset is not optional.

S45's AI Risk Radar surfaces these issues before SEBI filing, with source documents linked to DRHP disclosures in a live data room. When SEBI raises a query, the evidence is already organised and attributed.

Financial Modelling and Forecasting Discipline

One of the most important pre-IPO habits is acting like a public company at least 12 months before listing: setting internal targets, running mock earnings calls, and building a consistent "beat and raise" track record.

That internal track record is what investors measure during the roadshow. A CFO who can demonstrate forecasting accuracy over multiple quarters commands a stronger valuation case than one presenting a model that can't withstand basic stress testing.

Building the Right IPO Team: Internal Hires and External Advisors

Most companies underestimate the bandwidth required for an IPO and attempt to run preparation alongside normal finance operations. This is the single most common reason timelines slip.

Internal Finance Team Upgrades

Hire or develop the following roles before DRHP drafting begins:

- Controller or VP Finance with public company experience

- Technical accounting resource for Ind AS and SEBI disclosure work

- Investor Relations function — typically engaged 6–9 months before listing

- Dedicated financial reporting resource for quarterly close discipline

External Advisory Team

| Advisor | Role |

|---|---|

| SEBI-registered BRLM (Merchant Banker) | Regulatory filing, SEBI interface, investor outreach |

| Legal counsel (issuer-side) | DRHP documentation, SEBI correspondence |

| Statutory auditor | Financial restatement, IFC reporting, SEBI certifications |

| Registrar to the Issue (RTA) | Share allotment, subscription data, demat coordination |

| Monitoring Agency | Required if fresh issue component exceeds ₹100 crore |

S45 executes IPOs in partnership with Narnolia as Category-I SEBI-Registered Merchant Banker. S45 leads AI-driven readiness, demand mapping, pricing analytics, and post-listing IR — Narnolia manages the formal regulatory filings and SEBI interaction that require merchant banking credentials. In practice, this means SEBI observations get closed faster and pricing decisions are backed by live demand data rather than banker intuition.

Getting your advisory team assembled early also feeds directly into the governance restructuring your board will need before listing.

Governance Layer

SEBI LODR requires three mandatory board committees before listing:

| Committee | Key Requirement |

|---|---|

| Audit Committee (Reg 18) | Minimum 3 directors; at least 2/3 independent; chaired by an independent director |

| Nomination & Remuneration Committee (Reg 19) | All non-executive; at least 2/3 independent |

| Stakeholders Relationship Committee (Reg 20) | Minimum 1 independent director; chaired by a non-executive director |

Your independent director ratio depends on board structure: at least one-third if the chairperson is non-executive and non-promoter; at least half if the chairperson is executive or a promoter. Board composition gaps are one of the most common delay triggers — start governance restructuring 12–18 months before your target filing date.

Navigating SEBI Compliance and the DRHP Filing Process

The DRHP is filed with SEBI and the stock exchange(s) simultaneously through the BRLM. SEBI's observation letter is typically issued within 30 days of receiving satisfactory responses to queries under the standard route. Under the confidential pre-filing route (Chapter IIA), the observation letter validity extends to 18 months versus 12 months under the standard route.

The observation letter is conditional clearance — not approval. All SEBI observations must be addressed before the RHP is finalised and the issue opens.

What Must Go Into the DRHP

The CFO owns or co-owns the following DRHP sections:

- Restated financial statements — 3 years under Ind AS, certified by statutory auditor

- MD&A — operating performance, margin analysis, KPIs (peer-benchmarked KPI disclosures are now mandatory under the November 2022 SEBI amendments)

- Use of proceeds — specific allocation of fresh issue proceeds to stated objects

- Risk factors — quantified, evidence-backed; vague risk language is the primary source of SEBI queries

- Related party disclosures — complete and consistent with audited financials

- Objects of the issue — directly linked to the fresh issue size

If the gap between the last audited year-end and issue opening date exceeds six months, a stub-period audit is required — flag this risk early in your timeline planning.

Managing these disclosures across email threads and multiple draft versions is where most SEBI query cycles originate. S45's evidence-linked drafting workflow anchors every disclosure to source documents in a live data room — with a KPI Dictionary and evidence register tied to disclosure schedules. This gives SEBI reviewers an immediate audit trail for each claim, which defines the difference between a clean observation letter and a protracted query cycle.

Pricing, Offer Structure, and Regulatory Decisions

The CFO and BRLM jointly determine the offer structure:

- Fresh issue — primary proceeds to the company; size must align with disclosed objects of the issue

- OFS (Offer for Sale) — secondary proceeds to existing shareholders; SEBI restricts OFS from shareholders with short holding periods

Over-promising use of proceeds creates binding post-listing compliance obligations. Be disciplined about what you commit to deploy.

Pricing discipline starts with the right mechanism. Book-built issues are standard for Main Board IPOs — the price band is set based on peer multiples, anchor feedback, and institutional demand signals, with the final price determined within that band after the subscription window closes.

Fixed-price issues are more common in SME IPOs. Either way, the price band must be announced at least two working days before the offer opens.

S45 builds the live pricing band using sector comparables and global peer multiples, refined through pre-IPO investor soundings. During bookbuilding, a live demand map tracks subscription multiples by category (QIB, NII, Retail) in real time — so the CFO and management can read demand strength across investor segments as the book builds, not after it closes.

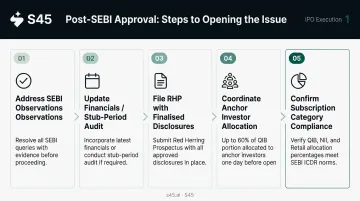

Post-SEBI Approval Steps

After the observation letter:

- Address all SEBI observations with supporting evidence

- Update financials if the observation period has extended beyond six months (stub-period audit)

- File the RHP with finalised disclosures

- Coordinate anchor investor allocation (up to 60% of the QIB portion; anchor bidding occurs one day before the subscription window opens)

- Confirm subscription category compliance — QIB, NII, and retail allocation percentages are fixed under SEBI ICDR

The Roadshow, Bookbuilding, and Life After Listing

The roadshow is where the equity story is stress-tested by people who will actually deploy capital. The CFO and CEO present to institutional investors (domestic mutual funds, FPIs, insurance companies, pension funds) through one-on-one and group meetings before the subscription window opens.

What investors probe at these meetings:

- Quality and sustainability of earnings

- Management's ability to articulate how IPO proceeds will be deployed

- Forecasting credibility — has management delivered on past guidance?

- Customer concentration, margin durability, and working capital discipline

S45's roadshow preparation covers management training, investor grid and meeting schedule development, city-wise planning across Mumbai, Delhi, Bengaluru, Chennai, Kolkata, Hyderabad, Pune, and Ahmedabad — all structured within SEBI ICDR publicity guidelines.

The Subscription Window: What the CFO Monitors in Real Time

The subscription window for book-built issues runs 3 to 7 working days. During this period, the CFO's real-time responsibilities include:

- Monitoring live subscription data across QIB, NII, and retail categories

- Working with the BRLM on demand assessment and bid quality analysis

- Managing internal communications to avoid premature signalling

Subscription imbalances (low QIB participation relative to retail, for example) can signal pricing issues and affect listing performance. SEBI's own study found that 54% of IPO shares were sold within a week of listing — which means a CFO who chases the highest possible price band without reading category-level demand is pricing against the data.

Listing Day and Post-Listing Obligations

Listing day follows the T+3 framework (allotment to listing in 3 working days). A pre-open session runs from 9:00 AM to 9:45 AM for price discovery, with continuous trading from 10:00 AM.

Immediately post-listing, the CFO transitions to public company reporting obligations:

- Quarterly financial results — within 45 days of quarter end (Q1, Q2, Q3) and 60 days for annual results

- Board meeting protocols under SEBI LODR

- Continuous disclosure — material events must be reported to BSE/NSE under Regulation 30

Building Post-IPO Investor Relations

The quality of IR in the first two to four quarters post-listing sets the market's perception of management credibility — and directly affects the secondary market performance of the stock.

A formal IR function must manage:

- Quarterly earnings calls and investor presentations

- Analyst coverage initiation and coordination

- Statutory filings with BSE/NSE (shareholding patterns, related party disclosures, board changes)

- For SME listings: market maker coordination per exchange obligations and lot size review

S45's 30/90-day post-listing IR service covers this full scope: earnings materials, compliance calendar, and institutional investor targeting. For SME issuers specifically, it includes market maker coordination and migration eligibility planning — the work most banks quietly drop once the listing day is done.

Frequently Asked Questions

What is the role of the CFO in an IPO?

The CFO leads all financial preparation — including audit readiness, DRHP financial disclosures, pricing strategy, and investor communications — while coordinating the broader IPO team and ensuring regulatory compliance with SEBI and the Companies Act. In practice, the CFO is the single point of accountability for the integrity of every number that appears in the offer document.

How should a CFO prepare for an IPO?

IPO preparation should begin 18–24 months before the target listing date, starting with a readiness assessment, followed by financial system upgrades, team building, DRHP drafting, SEBI filing, and roadshow execution. Each phase builds on the previous one, and starting late compresses every step that follows.

What should a CFO report include?

The core CFO-owned disclosures in an Indian IPO include restated audited financials (3 years under Ind AS), MD&A with peer-benchmarked KPIs, and use of proceeds for the fresh issue. These are accompanied by quantified risk factors with financial materiality, related party disclosures, and the internal financial controls assessment.

How long does IPO preparation take in India?

End-to-end preparation for a Main Board IPO typically takes 18–24 months, while an SME IPO can be executed in 9–12 months. The DRHP drafting and SEBI review process alone accounts for 3–6 months of this timeline, and governance restructuring should begin well before that.

What is a DRHP and when should a CFO start preparing it?

The DRHP (Draft Red Herring Prospectus) is the primary disclosure document filed with SEBI and the stock exchanges before an IPO. CFOs should begin gathering underlying data (audited financials, use of proceeds narrative, MD&A inputs, and risk factor evidence) at least 6–9 months before the planned filing date.

What are the most common reasons IPOs get delayed in India?

The top causes: accounting restatements or audit gaps that surface during DRHP drafting, multiple rounds of SEBI query responses triggered by vague risk disclosures, board composition gaps that delay governance compliance, and market condition changes that push the listing window. Structured preparation starting 18–24 months out eliminates most of these before they reach SEBI.