Introduction

Most founders preparing for an IPO hear "anchor book" mentioned in the same breath as regulatory checklists. What rarely gets explained is that the anchor book is the first public signal of institutional conviction in your offering — and how you build it shapes everything that follows in the subscription period.

The day before your IPO subscription opens, institutional investors examine who else has committed and at what price. That information, disclosed publicly per SEBI's Schedule XIII requirements, either builds momentum or creates doubt before retail and HNI investors have placed a single bid.

A 2025 study in the International Review of Finance found that anchor-backed IPO firms are more profitable, sell at higher valuations, and raise more equity than non-anchor firms — though anchor participation signals conviction, not a guarantee of outcomes.

That distinction matters operationally. This article covers how anchor book building actually works, how allocation decisions get made, what separates a strong book from a weak one, and the regulatory framework governing the entire process under SEBI's ICDR regulations including the October 2025 amendments.

Key Takeaways

- Anchor bidding opens one working day before IPO subscription; allotment is discretionary and confirmed the same day

- SEBI's October 2025 amendment restructured the reserved anchor portion to 40%, split between domestic mutual funds and IRDAI/PFRDA-registered institutions

- Allocation decisions involve deliberate choices about investor diversity, ticket sizes, and holding horizons — not just filling a quota

- Anchor book quality, not just size, drives downstream subscription momentum across HNI and retail categories

- Starting anchor outreach too late forces issuers into reactive allocation rather than deliberate curation

What Is Anchor Book Building in an IPO?

The anchor book is the aggregate of institutional bids placed one working day before the IPO subscription opens. "Building" refers to the deliberate, weeks-long process of identifying suitable investors, managing outreach, collecting indications of interest, and finalising allotments.

The mechanism locks in a meaningful share of institutional demand ahead of the public subscription window. This reduces pricing uncertainty, narrows the effective price discovery range, and creates visible early momentum.

How anchor investors differ from regular QIBs:

- Anchor investors are invited and allotted shares before the subscription window opens

- Regular QIBs bid during the open subscription period alongside NII and retail investors

- Anchor allotment effectively pre-fills a defined portion of the institutional quota

- Anchor allocations are disclosed publicly before the IPO opens: names, quantities, and price — letting the market see exactly which institutions committed and at what price before bidding opens

The regulatory parameters are specific. Per BSE's exchange FAQ, anchor investors are QIBs applying for ₹10 crore or more in a Main Board book-built public issue. The anchor portion can be up to 60% of the QIB quota, governed by SEBI's Regulation 28 and Schedule XIII of the ICDR Regulations.

How the Anchor Book Building Process Works

The process begins weeks before IPO opening and culminates in a formalised bidding and allotment sequence the day before subscription. Here is how each phase works in practice.

Investor Identification and Outreach

Lead managers build a target list of eligible anchor investors, shortlisting names based on:

- Sector fit and historical IPO participation patterns

- Fund mandate alignment (growth, value, sectoral, thematic)

- Anticipated ticket size relative to the anchor portion being built

- Relationship history and internal investment committee timelines

Eligible categories include domestic mutual funds, IRDAI-registered life insurance companies, PFRDA-registered pension funds, FIIs, and sovereign wealth funds. Outreach is relationship-driven and involves formal management presentations, often running parallel to DRHP preparation.

S45's investor mapping covers 50,000+ domestic and offshore institutional relationships. This informs anchor shortlisting by investor archetype — differentiating, for example, PSU-focused anchors from global sector specialists and dual-use funds.

Indication of Interest and Pricing Discussion

Before any formal bid is submitted, anchor investors signal indicative interest during pre-IPO roadshows. They typically provide:

- Indicative ticket sizes at various price points within the band

- Conditions or concerns that affect their willingness to commit at the upper end

- Sector-specific questions that shape due diligence requirements

This informal feedback helps the issuer and lead managers calibrate the price band and assess whether the book will clear at the top without anchors having formally committed. How anchors respond at this stage — and at what price — directly determines how aggressively the final band can be set.

Formalised Bidding and Allotment

Once informal signals harden into conviction, the process moves to the formal bid window. Per Schedule XIII of the ICDR Regulations, the mechanics run as follows:

- Day: Bidding opens one day before the issue opening date

- Minimum ticket: Each eligible investor must bid for at least ₹5 crore

- Allotment basis: Discretionary (not pro-rata), confirmed the same day

- Disclosure: Investor names, quantities, and price are filed with stock exchanges before the public subscription window opens

MobiKwik's December 2024 IPO illustrates this sequence: the company finalised its anchor allocation on December 10, 2024 — one day before public subscription opened on December 11 — allotting 92.26 lakh shares at ₹279 per share to 21 funds, including Norges Fund, Morgan Stanley, HDFC MF, and SBI MF, raising ₹257.4 crore.

How Anchor Allocation Decisions Are Made

Anchor allocation is discretionary, not lottery-based. The issuer, working with lead managers, decides how to distribute available shares among interested investors. The quality of this decision directly affects how the broader book builds.

Key Allocation Principles

These principles guide anchor book structuring:

- Holding horizon first — prioritise investors with genuine sector interest and longer holding periods over momentum-driven names that are likely to exit at the 30-day lock-in

- Geographic mix — a combination of domestic and foreign institutional investors signals cross-border credibility and broadens the validation base

- Spread over concentration — distributing allocation across multiple names rather than concentrating in one or two prevents the book from appearing thin; SEBI's minimum investor count rules reinforce this logic

- Recognisability — names that retail and HNI investors recognise carry more signalling weight than technically eligible but little-known funds

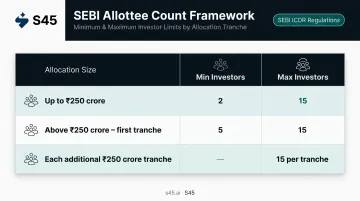

SEBI's Allottee Count Structure

Under SEBI notification SEBI/LAD-NRO/GN/2025/271 (October 31, 2025):

| Allocation Size | Minimum Investors | Maximum Investors |

|---|---|---|

| Up to ₹250 crore | 2 | 15 |

| Above ₹250 crore (first ₹250 crore tranche) | 5 | 15 |

| Each additional ₹250 crore | — | 15 per tranche |

The Pricing Signal Embedded in Allotment

Anchors are allotted at the upper end of the price band. MobiKwik's allotment at ₹279 (the upper end of its band) is one example. That willingness to commit at that price validates the issuer's pricing discipline publicly. If the anchor portion cannot be filled at the target price, that signal reaches the market before the subscription window even opens.

A well-allocated anchor book also shapes what happens after listing. Anchors that hold through the lock-in period tend to anchor analyst interest, stabilise post-listing trading, and show up in future QIP and rights issue books — compounding the value of the original allocation decision.

What Separates a Strong Anchor Book from a Weak One

Size alone does not define quality. A fully subscribed anchor book filled with little-known domestic funds provides limited credibility compared to a moderately subscribed book anchored by well-regarded names with genuine sector conviction.

Markers of a Strong Anchor Book

- Presence of marquee domestic mutual fund houses (SBI MF, HDFC MF, Axis MF, Mirae Asset)

- Participation from one or more credible foreign institutional investors

- Names that retail and HNI participants recognise and respect

- Spread across investment mandates — growth, value, sectoral — indicating broad institutional agreement on valuation

What the IPO Data Shows

The anchor-to-outcome relationship is real but not deterministic. Two contrasting examples illustrate this:

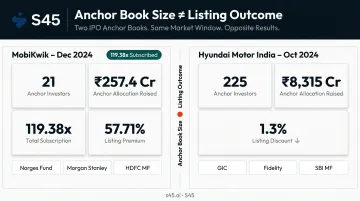

MobiKwik (December 2024): Named institutional anchors including Norges Fund, Morgan Stanley, and White Oak. Result: 119.38x total subscription, 57.71% listing premium on NSE. Strong anchor composition and strong outcomes occurred together.

Hyundai Motor India (October 2024): ₹8,315 crore raised from 225 anchor investors including GIC, Fidelity, SBI MF, and HDFC MF — one of the largest anchor books in Indian IPO history. The stock listed at a 1.3% discount on NSE. A marquee anchor book does not override issue size dynamics or market conditions.

That distinction points to a deeper question in anchor allocation: who holds the book after listing day.

Post-Lock-In Behaviour Matters

When a disproportionate share of the anchor book sits with investors known for short-term exits, the 30-day lock-in expiry creates a supply overhang that depresses the stock. Issuers should factor in anticipated post-lock-in behaviour when making allocation decisions — not just pre-listing sentiment. Allocating to patient capital (insurance companies, pension funds, long-only global funds) carries strategic value precisely because it reduces this risk.

SEBI's Regulatory Framework for Anchor Allocation

Three rules define who qualifies as an anchor investor and how allocations work before a single retail application comes in.

Core Parameters

- Anchor investors may receive up to 60% of the QIB portion (Regulation 28, SEBI ICDR)

- Minimum application: ₹10 crore or more per investor (BSE FAQ definition for Main Board issues)

- Minimum allotment per investor: ₹5 crore (confirmed in SEBI/LAD-NRO/GN/2025/271)

- Allotment confirmed one working day before IPO opening

- Full public disclosure of names, quantities, and price mandatory before subscription opens

Within that 60% QIB quota, SEBI has since tightened how the pie is divided — a change that directly affects which investor types a banker must prioritize during anchor outreach.

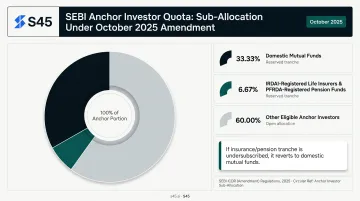

The October 2025 Amendment

SEBI notification SEBI/LAD-NRO/GN/2025/271 (dated October 31, 2025, effective 30 days from gazette publication) restructured the reserved portion within the anchor investor quota:

- 33.33% reserved for domestic mutual funds

- 6.67% reserved for IRDAI-registered life insurance companies and PFRDA-registered pension funds

- If the 6.67% insurance/pension tranche is undersubscribed, it reverts to domestic mutual funds

SEBI's September 2025 board memorandum flagged a clear intent: drawing in insurance and pension capital — which carries longer holding horizons than typical QIB allocation — to reduce the post-listing volatility that has drawn regulatory scrutiny in high-subscription SME issues.

Understanding the sub-allocation rules shapes outreach sequencing. But the lock-in schedule shapes how anchor investors think about committing in the first place.

Lock-In Structure

Per SEBI's investor education framework:

- 50% of anchor-allotted shares — locked in for 30 days from allotment

- 50% of anchor-allotted shares — locked in for 90 days from allotment

For issuers, this matters beyond compliance. Anchors who hold through the 90-day tranche tend to signal conviction to the secondary market — and that signal influences how institutional buyers approach the open subscription window.

Common Mistakes Issuers Make in Anchor Book Strategy

Treating It as a Compliance Formality

The most prevalent error: filling the required anchor quota with any willing institutional names rather than curating a book that sends a clear credibility signal. The result is a technically complete but strategically weak anchor book that fails to generate downstream momentum.

The anchor book is the first public signal of institutional conviction. Founders who treat it as an administrative checkbox hand over one of the most valuable pre-IPO signalling tools without using it.

Concentrating Allocation in Too Few Names

Allocating a large portion to one or two investors simplifies the process but concentrates lock-in expiry risk and makes the book appear thin to observers who track anchor disclosures. SEBI's minimum investor count requirements exist to guard against this — but the rules set a floor, not a target. A well-curated book spreads allocation deliberately across multiple mandates and geographies.

Starting Anchor Outreach Too Late

Anchor investors need time for:

- Internal investment committee approvals

- Sector due diligence

- Sizing decisions

Beginning outreach only after DRHP filing leaves too little lead time to build a quality book.

S45's IPO Readiness Assessment — typically initiated 12–18 months before filing — includes an investor map starter with anchor investor archetypes and positioning. Framing anchor strategy at the readiness stage, rather than at the roadshow stage, is what separates deliberate curation from reactive allocation.

Anchor strategy is not a closing task. It is a founding one — and the issuers who get it right start building long before the roadshow begins.

Frequently Asked Questions

What is anchor book allocation?

Anchor book allocation is the pre-IPO process by which a company and its lead managers distribute shares among selected institutional investors one working day before public subscription opens. Allotment is discretionary, governed by SEBI's ICDR regulations, and requires mandatory disclosure of investor names, quantities, and price before the IPO opens.

How does SEBI regulate anchor investor allocation in IPOs?

Anchors can receive up to 60% of the QIB portion. Within that, 33.33% is reserved for domestic mutual funds and 6.67% for IRDAI-registered insurers and PFRDA-registered pension funds (per the October 2025 amendment). Minimum allotment per anchor investor is ₹5 crore, and all details must be publicly disclosed before subscription opens.

What percentage of an IPO can be allocated to anchor investors?

Up to 60% of the QIB portion, governed by Schedule XIII under Regulation 28 of the SEBI ICDR Regulations. In practice, this means anchors lock in a significant slice of institutional allocation before retail and HNI bidding even opens.

How does anchor book quality affect IPO subscription and listing performance?

A well-composed anchor book with recognisable institutional names reduces information asymmetry for retail and HNI investors, often driving higher oversubscription across categories. Anchor presence consistently correlates with stronger valuations and larger equity raises — but it is a quality signal, not a listing guarantee.

When should anchor book building begin?

Outreach should begin during DRHP preparation or roadshow planning — several weeks before the IPO opens. Institutional investors need time for internal approvals and due diligence, and a late start forces issuers to fill the book with whoever is available rather than who is strategically right.

Can anchor investors cancel or revise their bids after allocation?

No. Once allotment is confirmed, anchor investors cannot withdraw or revise bids. Their shares are subject to a two-tranche lock-in: 50% for 30 days and 50% for 90 days from the allotment date, after which they may sell in the secondary market.