Key Takeaways

- IPO pricing is the output of months of financial preparation, valuation work, and demand aggregation — not a single decision made at the price band stage

- The goal is not the highest possible price but a price that attracts sustained institutional demand and delivers a healthy listing pop

- Overpricing destroys early investor trust; underpricing leaves significant capital on the table

- Book building in India follows SEBI-mandated rules, with QIB demand serving as the clearest signal of institutional conviction

- Companies that engage 12–18 months before filing enter book building with cleaner financials, stronger governance, and more credible demand signals

What Is IPO Pricing and Why It's a Founder's Most Critical Decision

Most founders treat IPO pricing as a final-week decision. It isn't. By the time a price band is announced, the damage from a mispriced issue is already done — built into flawed financial statements, mis-applied valuation methods, and demand signals that were never properly read.

IPO pricing is the process of determining the offer price at which a company sells its shares to the public for the first time. It is not the company's value divided by share count — it is a strategic call that balances capital raised, investor demand, and post-listing performance. Get it wrong, and there is no corrective mechanism.

Two outcomes define pricing failure:

- Overpricing — the stock opens below the offer price, early investors lose money, and institutional trust evaporates

- Underpricing — the company raises less capital than it could have, and insiders signal they had more conviction than the market warranted

Between these extremes lies the concept of the listing pop — the premium at which shares trade above the offer price on day one. A healthy listing pop signals that demand was well-calibrated, rewards investors, and builds credibility for the company's future equity story.

According to Prime Database, main board IPOs in CY2024 delivered a 30% average listing gain, while SME IPOs averaged 60% — a benchmark that reflects what disciplined pricing produces in a favourable market.

Pricing errors rarely originate at the price band announcement. They begin months earlier — in how financial statements were prepared, which valuation methods were applied, and whether real demand signals were captured before the price band was set.

This article covers each of those variables: valuation frameworks, bookbuilding mechanics, SEBI pricing norms, demand signal interpretation, and the timing decisions that determine whether a listing pops or drops.

How to Value a Company for an IPO

Before a price band is set, the company must establish an intrinsic valuation anchor. This foundational estimate (based on financial performance, growth outlook, and sector positioning) becomes the starting point from which the investment bank builds the pricing case.

Three methods are used in practice, and experienced bankers triangulate across all three.

Comparable Company Analysis (Comps)

Comps identify publicly listed companies in the same sector with similar revenue scale, margins, and growth profile, then apply their valuation multiples (P/E, EV/EBITDA, EV/Revenue) to the issuing company's financials.

Sector multiples in India vary considerably. RHP disclosures from recent IPOs illustrate the range:

| Sector / IPO | Peer P/E Range | Source |

|---|---|---|

| Industrial / CNC machinery (Jyoti CNC) | 37–68x | SEBI RHP, Jan 2024 |

| Consumer / stationery (DOMS Industries) | 16–64x | SEBI RHP, Dec 2023 |

| Engineering services (Tata Technologies) | 37–80x | SEBI RHP, Nov 2023 |

| Travel tech platform (TBO Tek) | 38–60x P/E; 26–39x EV/EBITDA | SEBI RHP, May 2024 |

These ranges confirm that applying a generic market multiple without sector-specific calibration is a meaningful source of mispricing risk.

Discounted Cash Flow (DCF) Analysis

DCF projects the company's future free cash flows over a forecast period (typically five years), discounts them to present value using a risk-adjusted discount rate (WACC), and adds a terminal value. It is most reliable for companies with stable, predictable cash flows.

For early-stage or high-growth businesses with lumpy earnings, DCF assumptions become too sensitive to small changes in growth rate or margin trajectory to anchor pricing with confidence.

Precedent Transactions

Precedent transactions look at valuations achieved by comparable companies in recent IPOs or acquisitions in the same sector. This method grounds the analysis in what the market has actually paid — not just what financial models suggest. It is useful for calibrating the price band against current market appetite rather than theoretical value.

In practice, the final valuation range is a judgment call informed by all three methods, tested against current market conditions, and ultimately validated by investor demand during the bookbuilding process. No single method wins — the triangulation itself is the discipline.

How Book Building Works in India: From Price Band to Final Price

Under SEBI's framework, the company and its Book Running Lead Managers (BRLMs) set a price band with a floor and cap (the cap cannot exceed 120% of the floor). Investors then submit bids within this range over the subscription window, which SEBI requires to remain open for a minimum of three working days and a maximum of ten.

The Three Investor Categories

SEBI mandates allocation across three categories, and how demand is distributed across them directly shapes how the final price is read:

- Qualified Institutional Buyers (QIBs) — mutual funds, FPIs, insurance companies, pension funds. Allocated 50–75% of the issue; their demand is the most-watched signal of institutional conviction

- Non-Institutional Investors (NIIs/HNIs) — allocated approximately 15% of the issue

- Retail Individual Investors (RIIs) — allocated the remainder, and may bid at the cut-off price, meaning they agree to pay whatever final price is discovered

What Oversubscription Signals

When bids exceed shares available, the IPO is oversubscribed. How far oversubscribed — and where that demand concentrates — tells price-setters what the market actually thought of their band. Recent examples show the correlation:

- Premier Energies (2024): subscribed 74.4x overall, QIB portion subscribed 216.67x, listed at approximately 120% premium over the issue price of ₹450

- DOMS Industries (2023): subscribed 93.4x, listed at 77.2% premium

- IREDA (2023): subscribed 38.8x, listed at 56.25% premium

High oversubscription does not automatically mean the price was set correctly . It can also mean the company left capital on the table. The objective is not maximum oversubscription but the right demand concentration at a price the market can sustain.

How the Cut-Off Price Is Determined

After the bidding window closes, the company and BRLMs analyse the demand curve (which price point attracted what volume of bids) and select the price at or below which total demand meets or exceeds the shares on offer. All allotted shares are issued at this uniform price.

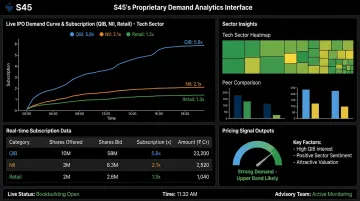

The risk for most issuers is that this analysis happens too late — on the final evening of bidding, when the options to adjust are gone. S45 pairs sector specialists with proprietary analytics to build and read the demand curve in real time, across QIB, NII, and retail categories, so issuers see where demand is building before the window closes — not after.

Key Factors That Influence Your Final IPO Price

Three variables consistently move the needle on where the final price lands — and each one is manageable if you address it early.

Market Conditions and Timing

The same company can command materially different valuations depending on when it goes public. In FY2022-23, when Indian markets were under pressure, main board IPO fundraising fell to ₹52,116 crore — less than half of FY2021-22 — and average listing gains dropped to 9.74% from 32.59% the prior year. By FY2023-24, as sentiment recovered, average listing gains rebounded to 29%. Market timing directly shapes the multiple range investors are willing to apply.

Investor Sentiment and Roadshow Outcomes

Institutional investor feedback during pre-marketing directly shapes where the price band is set. Strong QIB anchor commitments before the issue opens signal pricing confidence to the broader market. Anchor investors bid the day before the public issue opens, creating a credibility effect that drives retail and NII demand.

A poorly received roadshow, on the other hand, forces a price band revision — which extends the bidding period by at least three additional working days — or pushes the final price to the floor end of the band.

Company-Specific Factors

Investors apply higher multiples when they see:

- Consistent revenue growth with expanding or stable EBITDA margins

- Low or manageable debt levels

- Clean promoter credentials and governance practices

- A clear, specific use of proceeds — not a vague capital allocation narrative

- Resolved contingent liabilities and no pending audit qualifications

Companies that arrive at the DRHP stage with these elements in order typically price at the higher end of the comparable range.

Common IPO Pricing Mistakes Founders Make

Anchoring on the Last Private Round Valuation

Many founders enter the IPO process expecting the public market to validate — or exceed — their last private funding round valuation. This is often a mistake. Business Standard reported that Ola Electric was likely targeting a valuation of ₹37,500 crore for its IPO — approximately 18% below its last funding-round valuation of ₹45,800 crore.

Public market investors apply more conservative multiples than VC or growth-equity investors do. The market cycle that inflated private valuations may no longer exist by the time your IPO launches.

Pricing Aggressively to Maximise Proceeds

Setting the price at the very top of the defensible range in pursuit of maximum capital narrows the margin of safety, reduces oversubscription probability, and risks a flat or negative opening. The goal is not the highest possible price — it is a price that attracts sustained institutional demand.

A well-priced IPO that opens at a 30–40% premium creates more durable value for founders than a maximally priced one that opens flat. That listing pop builds institutional goodwill — which supports every equity story you tell afterward.

Neglecting Financial Preparation Before the Process Starts

The quality and consistency of your DRHP financials directly shape your pricing outcome. Companies that arrive at the IPO process with unresolved issues typically face valuation haircuts or filing delays:

- Undisclosed or unresolved related-party transactions

- Outstanding audit qualifications or modified opinions

- A cap table that hasn't been cleaned up pre-filing

Strong pricing outcomes begin 12–18 months before listing date. By the time the price band is announced, the work that determines your valuation is already done.

How to Build a Disciplined IPO Pricing Strategy

Three actions, executed in sequence, separate well-priced IPOs from mispriced ones.

1. Start financial housekeeping 12–18 months ahead.

Clean financials before the DRHP stage mean fewer surprises during SEBI review and investor diligence. Specifically: consistent revenue recognition, audited statements requiring no restatement, a clean cap table, resolved contingent liabilities, and a clearly articulated use of proceeds. Companies with these in order command stronger valuations — and more negotiating room on price.

2. Engage sector-specialist bankers with real demand visibility.

Generic benchmarks produce generic pricing. Bankers who understand your sector and have mapped actual institutional demand — by cohort, not by assumption — deliver materially better price band calibration than those working from cross-sector averages.

S45 pairs sector specialists with proprietary demand analytics, giving founders concrete subscription signals before committing to a price band. The result: 168x average subscription and a 43% average listing pop across 26 IPOs executed since July 2023.

3. Adopt the principle of under-promise and over-deliver.

Set a price firmly supported by demand, leave investors with a meaningful listing pop, and build the goodwill that funds your next raise. A well-priced IPO opens the public market relationship on the right terms. An aggressive one closes it before it begins.

Frequently Asked Questions

How do companies set IPO prices?

Companies work with investment banks to establish a valuation range using comparable company analysis, DCF, and precedent transactions. This range is then translated into a price band through a book building process, where investor bids over the subscription window determine the final issue price.

How do you value a company for an IPO?

IPO valuation typically triangulates across comparable company multiples, discounted cash flow analysis, and precedent transaction benchmarks to arrive at a defensible range. The final number reflects both intrinsic value and what the current market has demonstrated it will pay for similar businesses.

What is book building in an IPO?

Book building is the process by which a company announces a price band and collects bids from institutional and retail investors over a subscription window, typically three to ten working days. The aggregate demand curve from those bids determines the final issue price at which shares are allotted.

What happens if an IPO is overpriced at listing?

An overpriced IPO lists below its issue price on day one, erodes investor confidence, and limits the company's ability to raise follow-on capital at favourable terms. Paytm's post-listing performance, widely cited as one of the worst first-year declines among large Indian IPOs in recent memory, remains the clearest cautionary case.

What is the difference between SME IPO pricing and Main Board IPO pricing?

SME IPOs on NSE Emerge and BSE SME follow the same book building principles as Main Board issues, but with a post-issue paid-up capital cap of ₹25 crore. The more consequential difference is the investor base: SME platforms are retail-heavy with limited institutional participation, which reduces liquidity depth and shifts pricing dynamics away from QIB-led demand signals.

What role does an investment bank play in IPO pricing?

Investment banks (BRLMs) conduct valuation analysis, set the price band, manage the book building process, and advise on the final issue price. Their sector expertise and institutional network determine the quality of demand signals available to the issuer, which is why banker selection shapes IPO outcomes more than most founders expect.