Introduction

Building a profitable business is hard. Getting it listed is a different challenge — and most Indian founders only discover that gap once they're already in the room with a merchant banker.

Financial screening is the first formal gate between a growth-stage company and a public listing. It is where SEBI's eligibility criteria, auditor standards, and capital structure rules collide with how most Indian SMEs and mid-market businesses actually operate.

A company can have ₹100 crore in revenue, three years of positive EBITDA, and still fail screening — not because the business is weak, but because the financials carry structural issues that were never a priority when the focus was on growth.

That gap is expensive. In FY2024-25, 79 Main Board IPOs raised ₹1,62,517 crore and 241 SME IPOs raised ₹9,811 crore on Indian exchanges. Behind those numbers is a much larger group of companies that delayed, withdrew, or had their offer documents returned by SEBI — often because issues that surface during formal due diligence could have been caught and fixed much earlier.

This guide walks through how financial screening works in the Indian IPO context: what SEBI checks, how the process runs, what disqualifies companies, and how to close the gap before engaging a merchant banker.

Key Takeaways

- Financial screening determines whether a company's financial history and capital structure can survive SEBI scrutiny — before the DRHP process begins.

- SEBI sets specific eligibility thresholds — net tangible assets, operating profit, net worth, and capital structure — under ICDR Regulations, 2018.

- The quality of financials matters as much as the numbers — restated statements, clean revenue recognition, and unqualified audits are non-negotiable.

- Most companies fail screening over structural issues (promoter loans, demat gaps, qualified audits), not poor business performance.

- Starting a financial screening exercise 12–24 months before the target IPO date significantly improves the odds of a clean, on-time listing.

What Is Financial Screening for IPO Readiness?

Financial screening in the IPO context is a structured diagnostic process that evaluates whether a company's financial history, reporting systems, and capital structure meet the minimum eligibility thresholds and quality standards required for a public listing in India.

It is distinct from full legal due diligence. Legal due diligence covers contracts, litigation, regulatory filings, and title to assets. Financial screening happens earlier — typically before a merchant banker is formally engaged — and focuses specifically on whether the numbers and the financial reporting infrastructure are fit for SEBI review.

The process covers two dimensions:

- Quantitative: Do the financials meet SEBI's numerical thresholds for net tangible assets, operating profit, and net worth?

- Qualitative: Are the financials clean, consistently prepared, and able to hold up under SEBI review and institutional investor diligence?

Both dimensions matter. A company that clears the quantitative thresholds but carries qualitative problems will draw SEBI observations and face hard questions from institutional investors during bookbuilding. Common triggers include:

- Qualified or emphasis-of-matter audit opinions in any of the last three financial years

- Aggressive revenue recognition policies that deviate from industry norms

- Undisclosed or inadequately disclosed related-party transactions

Key Financial Criteria in SEBI's IPO Screening Framework

The Two Listing Routes

Before mapping against any threshold, a company must first determine which route it is targeting. The financial requirements differ significantly between the two:

- Main Board (NSE/BSE): Stricter profitability and NTA criteria; post-issue paid-up capital of at least ₹10 crore with market capitalisation of at least ₹25 crore.

- SME Route (NSE Emerge / BSE SME): Post-issue paid-up capital capped at ₹25 crore; lower profitability thresholds; simplified filing process.

Many founders default to the SME route without running the Main Board numbers first. Run them. The two routes carry different investor profiles, liquidity outcomes, and post-listing trajectories — and the gap between them compounds over time.

Main Board Financial Thresholds

Under SEBI ICDR Regulations, 2018 (last amended May 17, 2024), the standard Main Board eligibility criteria under Regulation 6 are:

| Criterion | Requirement |

|---|---|

| Net Tangible Assets (NTA) | ₹3 crore minimum in each of the last 3 financial years |

| Average Pre-Tax Operating Profit | ₹15 crore average over last 3 years, with profitability in each year |

| Net Worth | ₹1 crore minimum in each of the last 3 financial years |

| Post-Issue Paid-Up Capital | ₹10 crore minimum |

| Market Capitalisation | ₹25 crore minimum post-issue |

| Monetary Assets Cap | Not more than 50% of NTA may be monetary assets |

The QIB Alternative Route

Companies that do not meet the standard Regulation 6(1) profitability criteria can still proceed with an IPO through book building — provided at least 75% of the net offer is allotted to Qualified Institutional Buyers (QIBs). This route demands a stronger institutional narrative and verifiable demand-side confidence. The 75% QIB allotment threshold is not a relaxed standard — it shifts the burden of proof from historical profitability to institutional conviction, which is harder to manufacture and easier to lose.

Restated Financial Statements

Past financials must be restated — corrected for errors, aligned with Ind AS, and prepared in compliance with the Companies Act 2013 framework. The signing auditor must hold a valid peer review certificate issued by the ICAI Peer Review Board.

Two timing rules apply:

- Coverage period: At least the last 3 full financial years, plus a stub period (the partial financial year between the last full year and the DRHP filing date) if applicable.

- Staleness cap: Restated financials cannot be more than 6 months old at the time of DRHP filing.

Capital Structure Requirements

Before a DRHP can be filed, the following capital structure conditions must be satisfied:

- All promoter-held shares must be in dematerialised form

- No outstanding convertibles or rights issues that would result in equity issuance post-IPO (with limited ESOP exceptions)

- Minimum public shareholding of 25% post-issue

- No promoter or director debarred by SEBI from accessing capital markets

- No promoter or director classified as a wilful defaulter or fraudulent borrower

- All partly paid-up shares must be made fully paid-up or forfeited

Each condition is a hard stop. A single unresolved item — partly paid-up shares not yet cleared, or a promoter with an outstanding SEBI debarment — will block DRHP acceptance outright, regardless of how strong the financials are.

How Financial Screening Works — Step by Step

Financial screening runs in phases — from eligibility mapping through to gap remediation. Each phase builds on the last, and catching issues early protects both the timeline and the company's credibility with intermediaries.

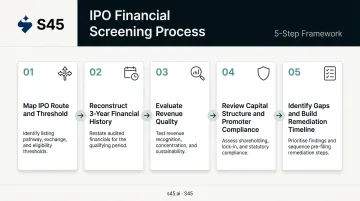

Step 1 – Map the IPO Route and Eligibility Threshold

Determine whether the Main Board or SME route is more appropriate based on company size, sector, and capital structure. Run a preliminary quantitative check against the relevant thresholds before going any deeper. This step alone eliminates ambiguity about which criteria apply and which do not.

Determine whether the Main Board or SME route is more appropriate based on company size, sector, and capital structure. Run a preliminary quantitative check against the relevant thresholds before going any deeper. This step eliminates ambiguity about which criteria apply — and prevents wasted effort preparing documentation for the wrong exchange.

Key inputs at this stage:

- Paid-up capital and net worth relative to exchange minimums

- Operating revenue scale and sector classification

- Free float structure and existing shareholder composition

Step 2 – Reconstruct and Stress-Test the 3-Year Financial History

Pull the last three years of audited financials and evaluate them against SEBI's profitability, NTA, and net worth criteria. Flag any years with:

- Qualified audit opinions

- Accounting policy changes

- Restatements already completed or pending

- One-time items that distort the operating profit track record

Step 3 – Evaluate Revenue Quality and Accounting Integrity

Assess:

- How revenue is recognised and whether it aligns with the applicable Ind AS standard

- Whether related-party transactions are material and verifiably at arm's length and documented

- Whether receivables and debtors are clean, or whether there is a working capital problem masked by accrual accounting

- Any contingent liabilities or off-balance-sheet exposures that will require disclosure or restatement

Step 4 – Review the Capital Structure and Promoter Compliance

Once the financial statements are clean, the review shifts to structural and compliance factors that SEBI scrutinises independently. Check that all promoter shares are dematerialised, that there are no pending convertibles, and that the company's capital history from incorporation is fully documented. Verify that no promoter or director carries any SEBI debarment, wilful default classification, or BIFR reference.

Step 5 – Identify Gaps and Build a Remediation Timeline

Compile a structured gap report with every issue that would block DRHP filing, along with an estimated time to resolve each. The most useful output is a clear distinction between:

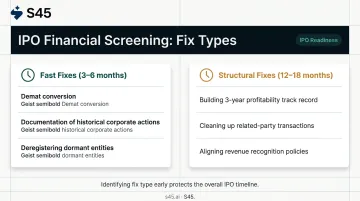

- Fast fixes (3–6 months): Demat conversion, documentation of historical corporate actions, deregistering dormant entities

- Structural fixes (12–18 months): Building a 3-year profitability track record, cleaning up related-party transactions, aligning revenue recognition policies

A well-structured gap report does more than list problems — it tells the founding team exactly how long preparation will take and which issues need to move first to avoid compressing the overall timeline.

Red Flags That Typically Fail Financial Screening

Related-Party Transactions and Promoter Loans

Unsecured loans from promoters, undisclosed related-party transactions, and non-arm's-length revenue arrangements are among the most common disqualifiers. SEBI scrutinises these closely because they distort the true financial picture and signal governance risk to institutional investors. Clearing a promoter loan off the balance sheet typically requires time — it cannot simply be reclassified.

Qualified or Adverse Audit Opinions

A qualified audit opinion — even for a disclosure issue that appears minor — complicates the DRHP filing process. Restating financials to remove qualifications requires the cooperation of both current and prior auditors, and takes time most founders have not budgeted for.

An unresolved qualification is not just a paperwork problem. It tells investors and SEBI that the financial record is under dispute, which can trigger additional observations and extend the review timeline significantly.

Inconsistent or Aggressive Revenue Recognition

SEBI flags several specific revenue recognition patterns during financial due diligence:

- Revenue recognised before delivery or acceptance

- Revenue from connected entities at non-market terms

- Sharp, unexplained jumps concentrated near financial year-end

Each of these either requires restatement or attracts SEBI observations that delay the listing timeline. A ₹5 crore anomaly with no supporting documentation creates as much friction as a ₹50 crore one — the absence of a clean audit trail is what SEBI acts on.

Weak Cash Conversion and Working Capital Stress

A company can show accounting profit but generate negative operating cash flow through high debtors or bloated inventory. SEBI and investors both treat the cash flow statement as a secondary stress test. Poor cash conversion undermines the DRHP narrative even when headline profitability looks adequate. QIBs specifically probe this during roadshows, asking how long debtors have been outstanding and whether collections have deteriorated in the most recent quarter.

Financial Screening in Practice: A Simplified Walkthrough

Consider a hypothetical Indian manufacturing company with ₹80 crore in revenue and three years of positive EBITDA that wants to assess its Main Board eligibility. The example is intentionally simplified, but the structure reflects how a real screening exercise runs.

The company's starting position:

- Revenue: ₹80 crore across 3 years

- EBITDA: Positive in all 3 years

- NTA: Above ₹3 crore in each year — clears the threshold

- Net worth: Above ₹1 crore in each year — clears the threshold

What the screening finds:

Operating profit shortfall in Year 2: A large one-time repair expense depressed operating profit that year. The 3-year average comes in just below ₹15 crore. This does not automatically disqualify the company, but it must either be reclassified (with auditor agreement) or the company must consider whether the QIB route is a realistic option — which requires a very different investor narrative.

Promoter loan of ₹4 crore on the balance sheet: The loan was extended informally and is not documented as arm's-length. This needs to be restructured, repaid, or converted — and the process typically takes 6–12 months depending on the company's liquidity position.

Two promoter shareholders hold shares in physical form: Demat conversion is procedurally straightforward but requires time to coordinate with the depository. This is a fast fix — typically 60–90 days — but it must be completed before the DRHP can be accepted.

What the gap report looks like:

| Issue | Timeline to Resolve |

|---|---|

| Demat conversion for 2 promoters | 60–90 days |

| Document promoter loan as arm's-length or repay | 6–12 months |

| Strengthen Year 2 operating profit position | Requires auditor review; may need restatement |

The outcome: The company is not ready to file today, but it has a clear, time-bound remediation path. Armed with this gap report, the founder can engage a merchant banker knowing exactly what needs fixing and when. Issues found at this stage cost weeks to resolve. The same issues found during formal due diligence cost months — and sometimes the deal itself.

How S45 Approaches Financial Screening for IPO Readiness

S45 — India's first AI-native investment bank — builds financial screening into the first stage of its IPO engagement, before mandate signing and well before DRHP preparation begins.

The IPO Readiness Scan runs a systematic check across financial eligibility criteria, capital structure compliance, governance gaps, demat readiness, and statutory dues. The output is a Readiness Score and Fix List, delivered within 48 hours, that prioritises every issue by severity and estimated resolution time.

What makes the approach practically useful is what happens after a company clears screening. Readiness findings feed directly into DRHP preparation, with auditors, counsel, and Narnolia (Category-I SEBI-Registered Merchant Banker) working inside a live data room from the same evidence base.

That integration is why S45 can move from a clean data room to a DRHP-ready draft in 30 to 45 days — not starting from zero after a separate assessment exercise.

For companies that are not yet ready to file, S45 typically engages 12–18 months before the target filing date. That pre-filing window covers Ind AS restatements, related-party hygiene, cap table cleanup, board composition, and the documentation required to produce clean restated financials. The goal is to reach the DRHP preparation stage with no open items — not to discover open items after the merchant banker is already engaged.

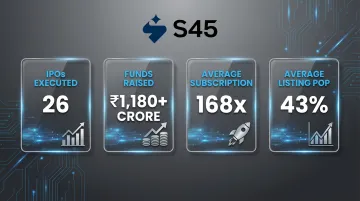

Since July 2023, S45 has delivered:

- 26 IPOs executed across Main Board and SME

- ₹1,180+ crore in capital raised

- 168x average subscription

- 43% average listing pop

Those numbers are the result of treating readiness as the foundation of execution — one that shapes every stage from first engagement to listing day.

Founders preparing for a listing in the next 12–24 months can start with S45's IPO Readiness Checklist to get an initial view of where they stand before engaging further.

Frequently Asked Questions

What is an IPO readiness assessment?

An IPO readiness assessment is a structured review of a company's financial, compliance, and governance position against the requirements of the intended listing route. It identifies gaps before formal DRHP preparation begins, so founders and boards know exactly what needs to be fixed and how long it will take.

Why is financial reporting crucial for an IPO?

Investors and SEBI both rely on audited financial statements to evaluate business quality and risk. Inaccurate, inconsistent, or unaudited financials can delay the listing process, attract SEBI observations, or undermine investor confidence during bookbuilding — and by that stage, a weak financial narrative is the hardest thing to fix.

How long does it take to get an IPO ready?

The full IPO preparation timeline in India typically ranges from 12 to 24 months, depending on the company's current financial and compliance position. A financial screening exercise at the outset establishes a realistic timeline and surfaces the structural issues that cause last-minute delays when left unaddressed.

How do you get ready for an IPO?

Start with a financial screening to check eligibility and identify gaps. From there, the core workstreams are:

- Prepare restated financial statements

- Strengthen corporate governance and board composition

- Resolve related-party and capital structure issues

- Appoint experienced intermediaries

- Begin DRHP documentation well ahead of the target filing date

What are SEBI's key financial eligibility criteria for a Main Board IPO?

Under SEBI ICDR Regulation 6, the key thresholds are:

- Net tangible assets: ₹3 crore minimum in each of the last 3 years

- Pre-tax operating profit: ₹15 crore average over 3 years, with profitability in each year

- Net worth: ₹1 crore minimum

- Post-issue paid-up capital: ₹10 crore minimum, with market capitalisation of at least ₹25 crore

What is the difference between an SME IPO and a Main Board IPO in terms of financial requirements?

SME IPOs on NSE Emerge or BSE SME have lower financial thresholds — including lower profitability requirements and a post-issue paid-up capital cap of ₹25 crore — and a simplified filing process. Main Board IPOs require stricter profitability, NTA, and net worth criteria. The choice of route directly determines how the financial screening process is structured and which thresholds the company must demonstrate it meets.