This guide is written for founders, CFOs, and senior management of Indian companies considering a public listing on the Mainboard or SME exchanges. The DRHP is not a formality. It is the document SEBI uses to determine whether a company is ready for public investors — and errors or omissions can delay your listing by months.

Key Takeaways

- The DRHP is filed with SEBI for Mainboard IPOs and with BSE SME or NSE Emerge for SME IPOs — not the ROC

- SEBI typically issues its Observation Letter within 30 days of receiving satisfactory responses to queries

- The DRHP requires three years of restated audited financials, certified use of proceeds, specific risk factors, and complete related party disclosures

- SEBI most commonly returns DRHPs for: promotional risk factor language, incomplete related party disclosures, or unquantified use of proceeds

- Appoint your BRLM early, lock down the data room before drafting, and run a pre-filing review — issuers who do this consistently receive cleaner Observation Letters

What Is the DRHP Filing Process?

The DRHP (Draft Red Herring Prospectus) is the initial disclosure document filed with SEBI — or with the relevant stock exchange for SME IPOs — before launching an IPO. It contains everything material about the company: business overview, financials, promoters, risk factors, litigation, regulatory approvals, and intended use of proceeds. It does not include the final offer price or issue dates.

Filing the DRHP serves three distinct purposes:

- Initiates SEBI's regulatory review

- Ensures all material information reaches potential investors before subscription opens

- Requires the issuer and lead manager to certify every disclosure for accuracy

How the DRHP Differs from What Comes After

Understanding the document sequence matters. Each filing has a distinct role:

| Document | Filed With | What It Contains |

|---|---|---|

| DRHP | SEBI (Mainboard) / Stock Exchange (SME) | All disclosures; no price or issue dates |

| UDRHP | Made public | Incorporates SEBI observations; 21-day public comment window |

| RHP | ROC (at least 3 days before issue opens) | Price band, IPO dates, updated financials |

| Final Prospectus | ROC + SEBI | Confirmed issue price, total capital raised |

This sequence is established under SEBI ICDR Regulations 2018 (last amended March 21, 2026) and Companies Act 2013 Section 32.

Before You File: What the Preparation Phase Requires

The filing is the midpoint of the process — not the start. Companies should begin 12 to 18 months before their target listing date to address the issues that most commonly delay filings.

Pre-Filing Housekeeping

Before drafting begins, resolve:

- Pending litigations above your board-approved materiality threshold

- Outstanding tax demands and statutory dues

- ROC compliance defaults

- ESOP and SAR scheme documentation

- Availability of three years of audited financials for restatement

Internal Governance Requirements

SEBI expects these to be in place before filing:

- Board resolution authorising the IPO

- IPO committee formation

- Shareholder approvals where required

- A board-approved litigation materiality threshold (this number must appear in the DRHP and be applied consistently — SEBI reviewers will check items left out against the stated threshold)

With governance in order, the next step is making sure your documentation is ready to support drafting from day one.

Building the Data Room

A structured data room is the foundation for a fast, clean DRHP. Organise the following before drafting begins:

- Audited financials (three years)

- Shareholder agreements and cap table documentation

- All operating licences and government approvals

- Board resolutions and committee minutes

- Related party transaction documentation

- Litigation files categorised against your materiality threshold

Gaps in the data room are the most common cause of delays during DRHP drafting. S45's IPO Readiness Scan runs a structured assessment across financial track record, board independence, demat readiness, statutory dues, and litigation — so these gaps surface before they stall your process.

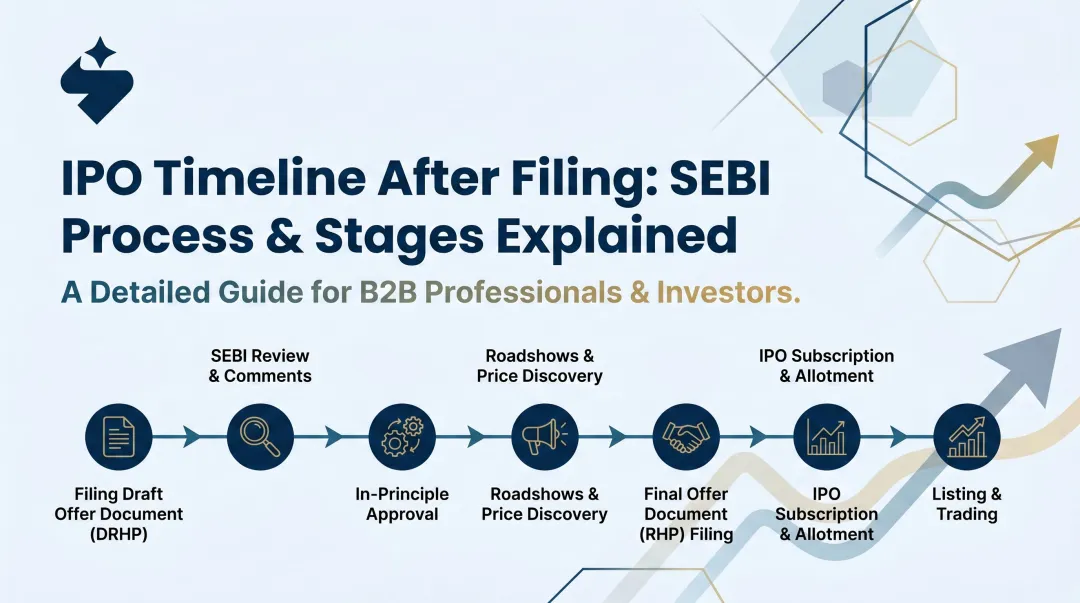

How to File a DRHP with SEBI: Step-by-Step

The process runs across six steps — from internal readiness and intermediary appointment through drafting, filing, SEBI review, and UDRHP filing. The full cycle from preparation to Observation Letter typically takes 4 to 6 months before listing preparations can begin.

Step 1: Appoint the Book Running Lead Manager and Key Intermediaries

The BRLM (merchant banker) must be appointed before due diligence begins. Under Schedule V of the SEBI ICDR Regulations, the lead manager must certify that all disclosures in the DRHP are true and complete — which requires them to supervise the full due diligence process. Appointing the BRLM after drafting starts creates a certification problem.

Appoint these intermediaries at this stage:

- BRLM (Lead Manager): Category-I SEBI merchant banking registration required; certifies all DRHP disclosures

- Legal counsel: Handles legal due diligence and transaction documentation

- Statutory auditor: Certifies financial restatement

- Registrar to the issue: Manages application processing and allotment

- Bankers to the issue: Configures escrow and ASBA rail

S45 executes IPOs in partnership with Narnolia as the Category-I SEBI-Registered Merchant Banker. S45 leads the AI-driven readiness, drafting, and SEBI query management layer; Narnolia holds the regulatory filing obligation.

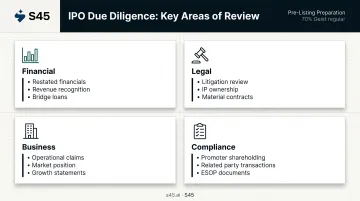

Step 2: Conduct Due Diligence Across All Material Areas

Due diligence typically takes 6 to 10 weeks and covers four areas:

- Financial: Restating three years of audited financials, verifying revenue recognition, checking bridge loans and material obligations

- Legal: Reviewing all pending litigation, regulatory filings, IP ownership, and material contracts

- Business: Verifying accuracy of all operational claims, market position assertions, and growth statements

- Compliance: Checking promoter shareholding records, related party transactions, ESOP/SAR scheme documents, and any prior regulatory action

Any undisclosed or incorrectly classified item will trigger a SEBI clarification notice after filing.

Step 3: Draft the DRHP

The DRHP requires these chapters, at minimum:

- Cover page, summary, and glossary

- Risk factors

- Business overview and operations

- Financial information (restated)

- Promoter and management details

- Objects of the issue (with certified use of proceeds)

- Capital structure and shareholding pattern

- Outstanding litigations and regulatory disclosures

- Government approvals

- Issue-related information

Internal consistency across all sections is non-negotiable. SEBI reviewers specifically check for contradictions between chapters — if the business overview claims 40% YoY revenue growth, the risk factors cannot describe demand conditions as stable.

S45's evidence-linked drafting process uses a live data room where every claim ties to a source document. This catches cross-section inconsistencies before filing and produces a DRHP-ready document in 30 to 45 days from a clean data room handoff.

Step 4: File the DRHP with SEBI or the Stock Exchange

Filing destination depends on IPO type:

- Mainboard IPOs: File directly with SEBI (under Regulation 25 of the SEBI ICDR Regulations) and simultaneously with NSE or BSE for in-principle approval

- SME IPOs: File with BSE SME or NSE Emerge under Regulation 229; the exchange conducts its own review

From the date of filing, the DRHP enters the public domain for a minimum of 21 days under Regulation 26(1). This public filing period also activates heightened promoter disclosure obligations: all securities transactions by promoters and promoter-group entities — sales, gifts, pledges, or transfers — must be reported to the stock exchanges within 24 hours under Regulation 54.

Step 5: Respond to SEBI Observations and Clarification Queries

SEBI issues its Observation Letter within 30 days of receiving satisfactory responses to all queries and after the stock exchange grants in-principle approval — whichever is later.

The clarification cycle works as follows:

- SEBI issues written queries on specific sections

- The company and BRLM respond with documentary evidence or revised drafts

- This may run for one or multiple rounds depending on complexity

Companies that clear SEBI's review in one round resolve disclosure inconsistencies before filing — not after. S45's Live DRHP Status and SEBI Query Board assigns owners, tracks due dates, and manages evidence attachment for each observation, keeping the response cycle on schedule.

Step 6: File the UDRHP and Progress to the RHP

Once SEBI issues its Observation Letter:

- File the Updated DRHP (UDRHP-I) incorporating all SEBI observations and updated financials

- The UDRHP remains in the public domain for 21 days

- After 21 days, proceed to price band determination with the BRLM

- File the RHP with the ROC at least 3 days before the IPO subscription opens (per Companies Act 2013, Section 32(2))

Observation Letter validity:

- Standard route: 12 months (Regulation 25(4))

- Confidential pre-filing route (Chapter IIA): 18 months, if UDRHP-I is filed within 16 months of SEBI observations

What SEBI Reviews in a DRHP

SEBI's review focuses on whether disclosures are complete, internally consistent, and free of promotional or unverifiable claims — five sections draw the most scrutiny.

Objects of the Issue

Every stated use of proceeds must be quantified and certified by the statutory auditor. Acceptable objects include specific capex amounts, named debt repayments with creditor details, and working capital with a supporting calculation. Vague entries do not pass:

- "Working capital requirements" without a certified number — not acceptable

- "General corporate purposes" beyond the permitted cap — not acceptable

For SME IPOs, the GCP cap is the lower of 15% of fresh issue proceeds or ₹10 crore.

Risk Factors

Risk factors must be specific, quantified, and written in plain language. SEBI does not permit terms like "leading," "robust," or "strong market position" unless backed by independently verifiable data. Risk disclosures must also be internally consistent with every other section of the document.

Restated Financials

Three years of audited financials must be restated per SEBI ICDR Schedule VI requirements, with:

- Consistent revenue recognition treatment

- Disclosed changes in accounting policy

- No undisclosed material obligations

Promoter and Related Party Disclosures

Every transaction between the company and promoter-controlled entities, family members, or associated businesses must be disclosed and cross-referenced across every relevant section. This is the highest-risk area from a regulatory enforcement standpoint.

SEBI's adjudication order against Saffron Capital Advisors in the matter of Acropetal Technologies involved related party disclosure failures by the lead manager. Omissions here carry direct enforcement consequences for both the issuer and the BRLM.

Outstanding Litigations

Every litigation above the board-approved materiality threshold must be individually disclosed. The threshold itself must appear in the DRHP. SEBI reviewers cross-check the stated threshold against items that were left out.

Post-2025 Regulatory Updates to Account For

- Fresh issue sizes can be increased or decreased by up to 50% without refiling a DRHP, for IPOs opening before September 30, 2026 (per a letter SEBI communicated to AIBI, reported April 16, 2026). Confirm the final SEBI circular before citing this in your filing.

- Stock Appreciation Rights exercised into equity before filing must be fully reflected in the cap table and Minimum Promoter Contribution calculation.

- For SME IPOs: OFS by selling shareholders cannot exceed 50% of pre-IPO promoter holdings; entities converting from LLP or proprietorship must complete one full financial year post-conversion before filing.

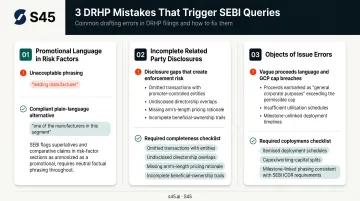

Common Mistakes That Delay DRHP Approval

Promotional Language in Risk Factors

The most frequent drafting error is carrying investor deck language into the DRHP. Phrases like "leading manufacturer," "robust client relationships," or "significant market position" are instinctive in pitch materials — but they are grounds for a returned DRHP. Risk factors must be verifiable and consistent with every other section of the document.

Incomplete Related Party Disclosures

All transactions with promoter-controlled entities must be disclosed — even those considered minor, technical, or at arm's length. Any promoter who has faced SEBI disciplinary action or been declared a wilful defaulter must be disclosed on the cover page. The Acropetal Technologies matter illustrates that partial disclosure creates enforcement exposure for both the issuer and the lead manager.

Objects of the Issue Errors and ESOP Cross-Referencing

Two issues consistently generate SEBI queries post-2025:

- Vague use-of-proceeds language, or GCP entries that exceed the permitted cap

- ESOP and SAR disclosures updated in one section but not consistently cross-referenced across the cap table, shareholding pattern, and Minimum Promoter Contribution calculation

These are precisely the inconsistencies that surface late — after drafting is well advanced — when cross-section review is done manually. S45 runs evidence-linked drafting inside a live data room, flagging promotional language, GCP breaches, and ESOP cross-referencing gaps before the document reaches SEBI. The process moves from first call to signed mandate in 7 days, and from data-room handoff to a DRHP-ready document in 30 to 45 days.

Frequently Asked Questions

Is the DRHP filed with SEBI or the ROC?

For Mainboard IPOs, the DRHP is filed with SEBI and simultaneously with the relevant stock exchange for in-principle approval. For SME IPOs, it is filed directly with BSE SME or NSE Emerge. The RHP — which comes later — is filed with the ROC at least 3 days before the issue opens.

How long does SEBI take to issue its Observation Letter?

SEBI typically issues its Observation Letter within 30 days of receiving satisfactory responses to all queries, and after in-principle approval from the stock exchange. Complex filings requiring multiple clarification rounds can extend this to 45–60 days. The Observation Letter is valid for 12 months under the standard route.

What documents are required to file a DRHP with SEBI?

Key document categories include:

- Three years of restated audited financials

- Board and shareholder resolutions authorising the IPO

- All government and regulatory approvals

- ESOP and SAR scheme documentation

- Related party transaction records and litigation files

- Certified statement of objects of the issue from the statutory auditor

What is the difference between the DRHP and the RHP?

The DRHP is the draft filed with SEBI for regulatory review — it does not include the offer price, price band, or issue dates. The RHP is filed with the ROC just before the issue opens and includes the price band, IPO open and close dates, and updated financials.

What happens after SEBI issues its Observation Letter?

The company files the UDRHP incorporating SEBI's observations, which stays in the public domain for 21 days. The company then finalises the price band with the BRLM, files the RHP with the ROC, and opens the issue for subscription.

Can a company file a DRHP confidentially with SEBI?

Yes. Under Chapter IIA (Regulations 59A–59F) of the SEBI ICDR Regulations 2018, companies can file with SEBI without immediate public disclosure. This route extends Observation Letter validity to 18 months (versus 12 months under the standard route) and allows companies to test QIB appetite before public disclosure.

Conclusion

The DRHP filing process is the formal regulatory gate every Indian company must pass before accessing public markets. Companies that receive clean Observation Letters share three operational habits:

- Start 12 to 18 months before filing — giving governance gaps and financial restatements time to resolve before SEBI sees them

- Appoint the right BRLM before due diligence begins — not after the data room is already messy

- Run a pre-filing review that surfaces SEBI's likely objections internally before submission

If you are at the stage of assessing your readiness for a Mainboard or SME listing, S45's 30-minute AI-powered IPO Readiness Scan surfaces eligibility gaps, disclosure risks, and governance issues before they become SEBI observations.