This guide serves two audiences: founders evaluating whether their company is IPO-ready, and investors trying to understand what they are actually participating in. Both groups routinely underestimate how different this segment is from mainboard listings — which is why approximately 65% of 2024 SME listings were trading below issue price by the time NISM reviewed the cohort.

This article covers the meaning, eligibility criteria, step-by-step process, key differences from mainboard listings, and the factors that separate successful issues from troubled ones.

Key Takeaways

- Post-issue paid-up capital must not exceed ₹25 crore to qualify for SME listing

- The exchange (not SEBI) reviews the DRHP for SME issues

- Minimum application size is above ₹2 lakh; cut-off bidding is not permitted

- Mandatory market-making runs for three years post-listing

- Meeting minimum eligibility thresholds is not the same as being IPO-ready

What Is an SME IPO?

SME IPO stands for Small and Medium Enterprise Initial Public Offering. A company going this route does not list on the main NSE or BSE boards — it lists on specialised platforms built to accommodate smaller balance sheets, shorter track records, and lighter compliance requirements.

The two platforms are BSE SME (launched March 2012) and NSE Emerge (launched 2012). Both are regulated under Chapter IX of the SEBI ICDR Regulations, 2018. As of June 2026, BSE SME had 730 companies listed, having raised ₹16,010 crore in total. NSE Emerge has seen 700 companies collectively raise over ₹21,252 crore.

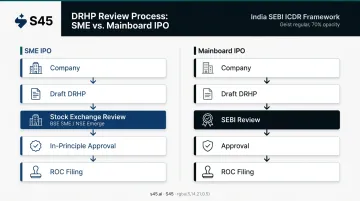

One structural difference separates SME IPOs from mainboard listings at the review stage. For mainboard IPOs, SEBI directly reviews the Draft Red Herring Prospectus (DRHP). For SME IPOs, the stock exchange itself — BSE SME or NSE Emerge — conducts that review. SEBI sets the regulatory framework; the exchange applies it. Draft offer documents are published on the exchange website for at least 21 days for public comments before in-principle approval is granted.

Three other structural differences set SME IPOs apart:

- Smaller issue size — post-issue paid-up capital capped at ₹25 crore

- Higher minimum investment — above ₹2 lakh versus approximately ₹14,000–₹15,000 for mainboard retail

- Mandatory market-making — a requirement that does not exist for mainboard listings

Who Qualifies: SME IPO Eligibility Criteria

The ₹25 crore post-issue paid-up capital ceiling is the defining threshold. Companies exceeding it must use the mainboard route. That makes capital structure a planning decision, not a last-minute adjustment — one to resolve well before you approach an exchange.

Financial Requirements

| Criterion | Threshold |

|---|---|

| Post-issue paid-up capital | Must not exceed ₹25 crore |

| Net tangible assets | Minimum ₹3 crore |

| Net worth | Minimum ₹1.5 crore |

| Positive cash accruals (EBITDA) | Required for at least 2 of the 3 preceding financial years |

Note: NSE's April 2026 circular adds a positive Free Cash Flow to Equity (FCFE) requirement for at least 2 out of 3 preceding financial years. These thresholds have been tightened through 2024–2025 — verify the current amended ICDR text and exchange circulars before relying on any single source.

Operational and Governance Prerequisites

- Functional corporate website with an investor relations section

- No change in company name in the preceding year

- No history of referral to BIFR (Board for Industrial and Financial Reconstruction)

- Promoters must commit to no change for at least one year post-application

IPO Structure Requirements

- Issue must be 100% underwritten

- A SEBI-registered merchant banker must be appointed as lead manager

- Minimum allottees required: SEBI's January 2025 Board memorandum proposed increasing this from 50 to 200 — check the current amended ICDR text before relying on either figure

Mandatory Market-Making

A registered market maker must provide buy and sell quotes for at least 75% of trading hours for three years post-listing. This is compulsory for SME listings and has no mainboard equivalent. It exists because SME stocks attract lower trading volumes — without market-making obligations, liquidity could effectively disappear between transactions. For founders, this is a contractual obligation starting on listing day and running for 36 months — regardless of stock performance; for investors, it provides a baseline floor of activity throughout that period.

How the SME IPO Process Works Step by Step

The end-to-end process mirrors a mainboard IPO in structure — appointing a merchant banker, preparing the DRHP, obtaining exchange approval, running the subscription window, completing allotment, and listing. The difference is timeline and regulatory touchpoints. The typical end-to-end journey takes 4 to 6 months, depending on company readiness and exchange review speed.

Preparation Phase

Before approaching any exchange, the company must complete internal due diligence: audited financials for at least three years, regulatory compliance review, corporate restructuring where needed, and valuation work. Governance gaps — board composition issues, undisclosed contingent liabilities, related-party transactions, inconsistent revenue recognition — surface here, not during the exchange review. Finding them late is expensive.

Engaging an experienced banker early compresses this phase significantly. S45's 30-minute AI-powered Readiness Scan screens for exactly these issues — covering financial track, free float, board independence, demat readiness, statutory dues, and material litigation — before they reach the DRHP stage. From a clean data room, S45 delivers DRHP-ready drafts within 30 days.

Documentation and Approval Phase

Once preparation is complete, the DRHP is filed with the relevant SME exchange — BSE SME or NSE Emerge. Both exchanges host draft offer documents and public comment material on their platforms. The exchange (not SEBI) reviews for completeness and regulatory compliance. After in-principle approval, the final prospectus is filed with the Registrar of Companies (ROC).

SME DRHP queries frequently focus on related-party transactions and promoter track record. Having clean documentation from the start determines whether this phase takes two weeks or two months.

Subscription and Allotment Phase

Key mechanics that differ from mainboard IPOs:

- Minimum application: Above ₹2 lakh (equivalent to a minimum of 2 lots), per NSE's June 2025 circular

- Cut-off price option: Not available for any investor category in SME IPOs

- Bid revision or cancellation: Not permitted once submitted

- Application method: ASBA or UPI

The ₹2 lakh minimum is intentional — it restricts participation to investors who can conduct their own due diligence and absorb the liquidity risk that comes with SME-listed stocks. This is not a regulatory inconvenience; it is a design choice based on the post-listing performance data that SEBI reviewed when tightening the framework in 2024–2025.

Post-Listing Phase

Listing day is not the finish line. After listing:

- Market-making obligations run for three years — the company is contractually bound regardless of trading performance

- Quarterly disclosure requirements apply under LODR regulations

- Ongoing compliance covers filing templates for Regulation 30 events, shareholding patterns, and results

The period from listing day to the three-month mark is where investor confidence is either built or lost. S45's post-listing IR service covers this window directly — market maker coordination, quarterly earnings materials, compliance calendar management, and trading activity monitoring — because what happens after the bell rings is what determines long-term market performance.

SME IPO vs. Mainboard IPO: Key Differences

| Feature | SME IPO | Mainboard IPO |

|---|---|---|

| DRHP review authority | Stock exchange (BSE SME / NSE Emerge) | SEBI |

| Post-issue capital ceiling | ≤₹25 crore | No upper cap |

| Minimum allottees | 200 (post-2025 amendment) | 1,000 |

| Minimum investment | Above ₹2 lakh | ~₹14,000–₹15,000 |

| Market-making | Mandatory, 3 years | Not mandatory |

| Cut-off price bidding | Not permitted | Permitted |

| Bid revision/cancellation | Not permitted | Permitted |

| Typical listing timeline | 2–3 months from mandate | 6–12 months from mandate |

The Migration Pathway

SME-listed companies that grow past the ₹25 crore paid-up capital threshold — or meet mainboard eligibility criteria — can apply to migrate to the main board. BSE's migration eligibility criteria include a threshold of revenue from operations of ₹100 crore or more for each of the immediately preceding three full financial years. As of June 2026, 201 companies had migrated from BSE SME to the main board.

For founders with mainboard ambitions, the SME listing is the starting point — not the ceiling. The three years of mandatory market-making and public reporting create the audited track record and institutional familiarity that mainboard investors expect before they commit capital at scale.

A Deliberate Trade-Off, Not a Compromise

The SME framework is designed to reduce compliance cost and listing burden for growing businesses. Lower liquidity, a narrower investor base, and limited analyst coverage come with the territory — but these are deliberate features of the architecture, not oversights. The exchange-level DRHP review and the ₹2 lakh minimum investment threshold exist specifically to limit retail exposure to early-stage risk while the company matures.

Key Factors That Determine SME IPO Success

Financial Quality and Documentation Readiness

Three-year audited financials and a clean promoter background are non-negotiable. The exchange review will surface gaps in both. According to NISM, governance risk and disclosure quality are among the primary differentiators between SME issues that compound post-listing and those that decline. SEBI's August 2024 advisory specifically warned that some SME companies projected an "unrealistic picture" of operations — meaning the regulator is watching disclosure quality, not just eligibility compliance.

Common issues that create delays or kill momentum:

- ESOP dilution not reflected in the cap table

- Audit committee composition deficiencies

- Undisclosed contingent liabilities

- Tax disputes with material financial impact

- Unexplained working capital movements

Pricing Discipline

Over-valuing an SME IPO relative to comparable listed peers leads directly to poor subscription and weak listing performance. Pricing on aspiration rather than market reality is a costly mistake. Demand mapping before the book-build — comparing the company against India-listed SME peers and sector benchmarks — prevents this.

S45 conducts cohort-level investor demand mapping before mandate signing, giving founders a realistic view of where subscription will come from before committing to a price band.

Merchant Banker Selection

The lead manager determines DRHP quality, speed of exchange review responses, and strength of investor outreach. When evaluating a merchant banker, the three metrics that matter:

- Number of SME IPOs executed — execution experience in this specific segment, not mainboard work

- Average subscription achieved — demand generation capability across the book

- Post-listing performance of past issues — whether investors actually made money, not just listing-day pops

S45's team has executed 26 IPOs since July 2023, with 168x average subscription and a 43% average listing pop. The firm executes in partnership with Narnolia as the Category-I SEBI-Registered Merchant Banker (the regulated lead manager), with S45 running AI-led readiness, demand mapping, pricing support, and post-listing IR.

Market Timing and Investor Sentiment

Banker selection and market timing work together. Even a well-prepared company launched at the wrong point in the cycle will underperform.

The FY25 data illustrates the gap between a strong market and actual outcomes:

- FY25 saw 235–239 SME IPOs raise around ₹9,133 crore, per Indian Express

- H1 FY25 average listing gains reached 63%, per PRIME Database data cited by ET CFO

- NISM's post-listing review showed around 57% of 2025 SME listings trading below issue price

Sector appetite, broader market conditions, and the concurrent SME IPO pipeline all affect subscription. None of these are within the issuer's control — but an experienced banker can time around all of them.

Common Mistakes and Misconceptions About SME IPOs

Most companies approaching an SME IPO carry at least one assumption that costs them time, money, or credibility. Here are the three that surface most often.

Treating It Like a Smaller Version of a Main Board IPO

The documentation requirements, investor profile, subscription mechanics, and post-listing obligations are all materially different from a main board process. Companies that assume otherwise run into last-minute fire drills, lost documentation, and unclear pricing — which delays listing and erodes investor confidence before the issue even opens.

Confusing Eligibility With Readiness

Meeting minimum financial thresholds — net worth, EBITDA track record, tangible assets — does not mean the company can withstand public scrutiny.

Exchanges and SEBI also examine:

- Board composition and independence

- Related-party transactions and disclosures

- Management depth and succession

- Governance structures and audit committee function

Finding these problems at the DRHP stage costs weeks. Finding them after exchange queries begin costs more.

Underestimating the Liquidity Constraint

Allottees can technically sell shares after listing. In practice, trading volumes on BSE SME and NSE Emerge are significantly lower than mainboard stocks. Exits at desired prices are not always available — particularly outside the initial listing window.

The mandatory market-maker guarantees a floor, not a free exit. Post-listing performance data across SME issues confirms this is a primary risk factor that both issuers and investors frequently underestimate going in.

Frequently Asked Questions

What is the SME IPO scheme?

The SME IPO scheme is a SEBI-facilitated framework enabling small and medium enterprises to raise public capital by listing on BSE SME or NSE Emerge under a lighter compliance regime compared to mainboard listings. The exchange — not SEBI — reviews the draft offer document, and mandatory market-making ensures baseline post-listing liquidity.

Is buying an SME IPO a good investment?

SME IPOs offer high growth potential and early-entry advantage, but carry higher risk — lower liquidity, limited analyst coverage, and shorter operating history. Suitability depends on the investor's risk tolerance and capacity for independent due diligence; the ₹2 lakh minimum application threshold exists precisely to filter for this.

Can I sell SME IPO shares immediately after listing?

Shares are tradeable from listing day, but SME stocks typically have lower trading volumes and fewer buyers than mainboard stocks. Immediate exits at desired prices are not always possible, particularly once the initial listing window closes.

What is the minimum investment required for an SME IPO?

The minimum application size is above ₹2 lakh (minimum 2 lots), per NSE's June 2025 circular — compared to approximately ₹14,000–₹15,000 for mainboard retail applications. The higher threshold restricts participation to more risk-aware investors.

What is the difference between an SME IPO and a mainboard IPO?

Key distinctions: SME issues carry a post-issue capital ceiling of ≤₹25 crore (mainboard has no cap), face exchange-level vetting rather than direct SEBI review, and require a higher minimum investment threshold. Compliance requirements, liquidity depth, and investor base composition differ meaningfully as well.

How long does the SME IPO process take from start to listing?

The typical end-to-end timeline is 4 to 6 months, depending on company readiness, documentation quality, and exchange review speed. Companies that engage experienced bankers early can compress this — S45 targets DRHP-ready in 30 days from a clean data room, with 2–3 months from signed mandate to listing.